Key Insights

The Qatari freight and logistics industry, valued at approximately $XX million in 2025, is projected to experience robust growth, driven by the nation's strategic location, substantial investments in infrastructure development related to the FIFA World Cup 2022 and ongoing mega-projects, and the burgeoning e-commerce sector. The industry's 5.98% Compound Annual Growth Rate (CAGR) indicates a steady expansion over the forecast period (2025-2033). Key growth drivers include the increasing volume of international trade, particularly in energy and related products, the expansion of industrial activities, and the government's commitment to diversifying the economy beyond hydrocarbons. Significant segments include temperature-controlled logistics, crucial for food and pharmaceutical imports, and courier, express, and parcel (CEP) services catering to the growing e-commerce market. While the industry faces challenges like global supply chain disruptions and geopolitical uncertainties, the ongoing infrastructure development and government support are expected to mitigate these risks and drive sustained growth. The competitive landscape is characterized by a mix of international players like Maersk, DHL, and FedEx, and local companies like Qatar Navigation and Gulf Agency Company, indicating a blend of established expertise and local market knowledge. The dominance of specific segments and the impact of global events will shape future market performance, requiring adaptable strategies and close monitoring.

The forecast period will see increasing demand for efficient and reliable logistics solutions across various sectors including construction (tied to ongoing infrastructure projects), manufacturing (with diversification efforts), and oil and gas (as a significant part of the economy). Logistics companies will need to invest in technology and infrastructure to maintain competitiveness, including enhancing digitalization, optimizing warehousing, and improving cold chain management. The government's emphasis on sustainability will also play a role, pushing companies to adopt eco-friendly practices. This will create opportunities for innovative companies to serve emerging needs and potentially capture substantial market share. The strategic focus on developing a robust digital infrastructure also creates opportunities for those offering digital freight forwarding services and real-time tracking solutions. Overall, the Qatari freight and logistics industry presents a promising investment landscape for both established players and innovative startups.

Qatar Freight & Logistics Industry Report: 2019-2033

This comprehensive report provides a detailed analysis of the Qatar freight and logistics industry, covering market dynamics, growth trends, key players, and future outlook. With a focus on the period 2019-2033, this report is an essential resource for industry professionals, investors, and policymakers seeking to understand and capitalize on opportunities within this dynamic sector. The report utilizes a parent-child market approach, segmenting the industry by both end-user industry and logistics function, for granular insights. Market values are presented in millions of units.

Qatar Freight and Logistics Industry Market Dynamics & Structure

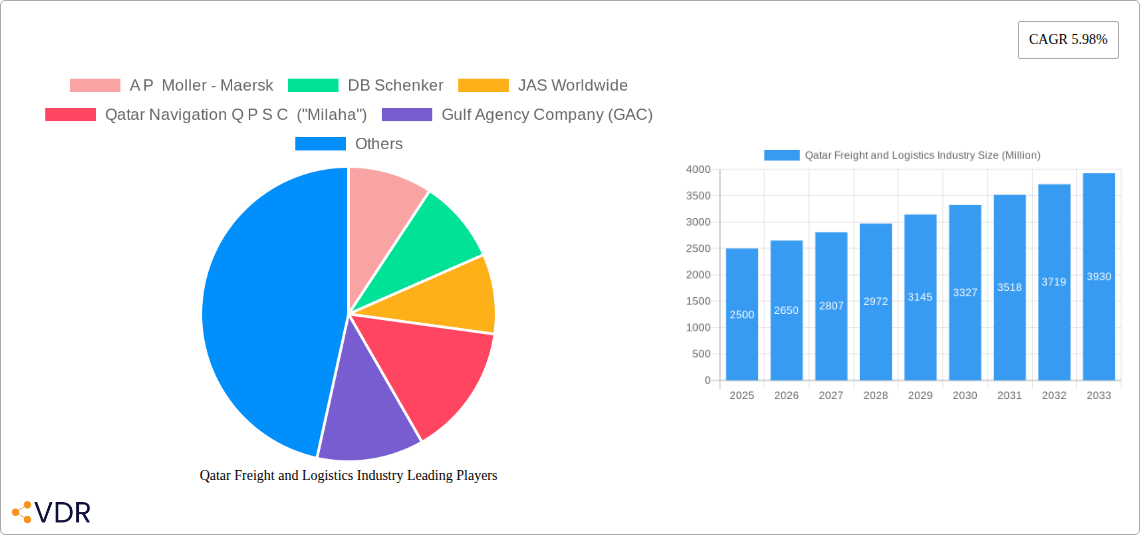

The Qatari freight and logistics market, valued at xx million in 2024, exhibits a moderately concentrated structure, with key players like A P Moller - Maersk, DHL Group, and Kuehne + Nagel holding significant market share. Technological innovation, driven by the increasing adoption of automation, AI, and blockchain solutions, is a key driver of growth. However, regulatory frameworks and the need for infrastructure upgrades present challenges. The competitive landscape includes both established global players and local companies, with increasing M&A activity observed in recent years. The prevalence of substitute products, like private fleet operations, also impacts market dynamics. End-user demographics, shifting towards a more diversified economy beyond oil and gas, are influencing demand.

- Market Concentration: Moderately concentrated, with top 5 players holding approximately xx% market share in 2024.

- Technological Innovation: Strong adoption of automation, AI, and blockchain impacting efficiency and transparency.

- Regulatory Framework: Government initiatives focusing on logistics infrastructure development and ease of doing business influence growth.

- Competitive Substitutes: Private fleet operations and alternative transportation methods present competition.

- End-User Demographics: Shifting towards diversification beyond Oil & Gas influences demand across various segments.

- M&A Trends: xx M&A deals recorded between 2019 and 2024, primarily focused on consolidation and expansion into new segments.

Qatar Freight and Logistics Industry Growth Trends & Insights

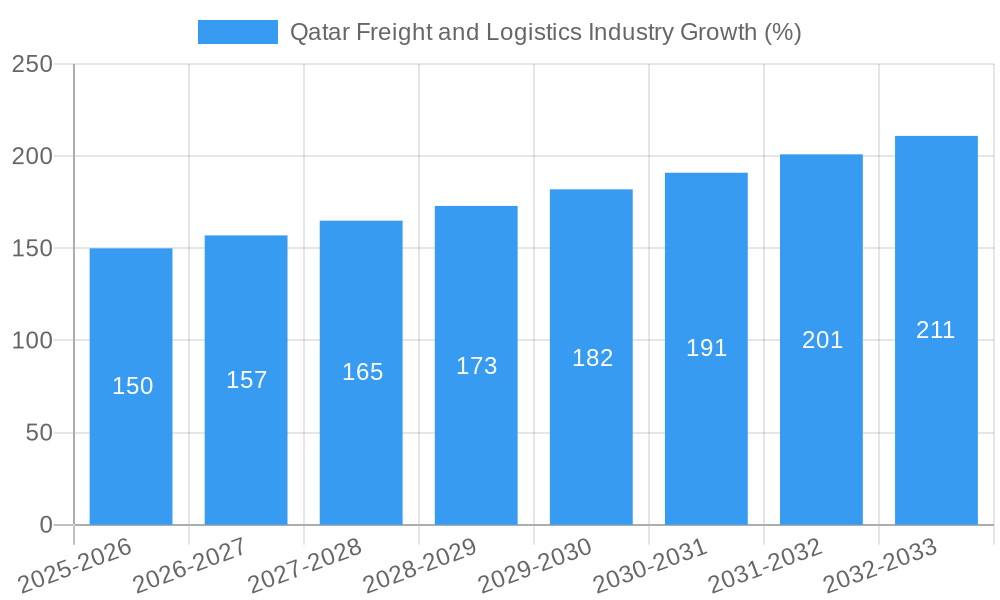

The Qatari freight and logistics market demonstrates robust growth, driven by increasing trade volumes, infrastructural investments, and government support for economic diversification. The market size exhibited a CAGR of xx% during the historical period (2019-2024), reaching xx million in 2024. Adoption rates for advanced logistics technologies are accelerating, while technological disruptions are transforming operational efficiencies and customer experience. Consumer behavior shifts reflect a growing preference for faster and more reliable delivery services. The forecast period (2025-2033) projects continued growth, with a projected CAGR of xx%, driven by major infrastructure projects and increasing e-commerce penetration.

Dominant Regions, Countries, or Segments in Qatar Freight and Logistics Industry

The Oil & Gas sector remains a dominant end-user industry, accounting for xx% of the market in 2024. However, Construction and Wholesale & Retail Trade are exhibiting significant growth, projected to increase their market share in the coming years. Within logistics functions, Temperature Controlled logistics and Courier, Express, and Parcel (CEP) services are experiencing the highest growth rates, fueled by demand for specialized handling and e-commerce expansion.

- Key Growth Drivers:

- Robust economic growth and large-scale infrastructure projects.

- Government initiatives promoting private sector investment and logistics development.

- Increasing e-commerce penetration and demand for faster delivery services.

- Growing importance of temperature-sensitive goods transportation.

- Dominant Segments: Oil & Gas (xx% market share), Construction (xx%), Wholesale & Retail Trade (xx%). High growth in Temperature Controlled and CEP logistics.

Qatar Freight and Logistics Industry Product Landscape

The product landscape is characterized by the increasing integration of technology, with solutions ranging from advanced warehouse management systems to real-time tracking and delivery optimization tools. Innovative offerings include the use of autonomous vehicles and drones for last-mile delivery, and the application of blockchain technology for enhanced supply chain transparency and security. Companies are focusing on unique selling propositions such as improved speed, reliability, and cost-effectiveness.

Key Drivers, Barriers & Challenges in Qatar Freight and Logistics Industry

Key Drivers: Government investment in infrastructure, rising e-commerce adoption, the 2022 FIFA World Cup legacy and ongoing diversification of the economy beyond oil and gas.

Key Challenges: Limited skilled workforce, high operational costs, competition from regional hubs, and potential regulatory changes. These challenges are estimated to collectively impede the market growth by approximately xx% by 2033.

Emerging Opportunities in Qatar Freight and Logistics Industry

Emerging opportunities include the growth of e-commerce, the expansion of cold chain logistics to support the growing food and pharmaceutical sectors, and the development of sustainable logistics solutions to address environmental concerns. Untapped potential exists in last-mile delivery solutions and specialized logistics services tailored to specific industry needs.

Growth Accelerators in the Qatar Freight and Logistics Industry Industry

Technological advancements, strategic partnerships between logistics providers and technology companies, and proactive government policies designed to streamline logistics operations and improve infrastructure are key growth accelerators. The focus on sustainability and the development of green logistics solutions will also propel growth.

Key Players Shaping the Qatar Freight and Logistics Industry Market

- A P Moller - Maersk

- DB Schenker

- JAS Worldwide

- Qatar Navigation Q P S C ("Milaha")

- Gulf Agency Company (GAC)

- Bin Yousef Group of Companies W L L

- DHL Group

- Tokyo Freight Service

- DSV A/S (De Sammensluttede Vognmænd af Air and Sea)

- E2E Global Lines

- Gulf Warehousing Company (GWC)

- Qatar Post

- FedEx

- Target Logistics Qatar

- Al Faisal Holding

- Kuehne + Nagel

- BCC Logistics

- Aerofrt (Aero Freight Company Ltd)

- Mannai Corporation QPSC

- Nakilat

- Qatar Airways Group

- Aramex

- Ali Bin Ali Holding

- Rumaillah Group

Notable Milestones in Qatar Freight and Logistics Industry Sector

- January 2024: Kuehne + Nagel launches Book & Claim insetting solution for electric vehicles, enhancing decarbonization efforts.

- September 2023: Kuehne+Nagel and Capgemini form a strategic partnership to create a supply chain orchestration service.

- March 2023: Maersk announces the divestment of Maersk Supply Service, focusing on integrated logistics.

In-Depth Qatar Freight and Logistics Industry Market Outlook

The future of the Qatari freight and logistics industry looks promising, with continued growth fueled by government investments in infrastructure, technological advancements, and the ongoing diversification of the economy. Strategic partnerships and the development of innovative solutions will create significant opportunities for growth and expansion in the coming years. The market is expected to reach xx million by 2033, presenting substantial opportunities for both established players and new entrants.

Qatar Freight and Logistics Industry Segmentation

-

1. End User Industry

- 1.1. Agriculture, Fishing, and Forestry

- 1.2. Construction

- 1.3. Manufacturing

- 1.4. Oil and Gas, Mining and Quarrying

- 1.5. Wholesale and Retail Trade

- 1.6. Others

-

2. Logistics Function

-

2.1. Courier, Express, and Parcel (CEP)

-

2.1.1. By Destination Type

- 2.1.1.1. Domestic

- 2.1.1.2. International

-

2.1.1. By Destination Type

-

2.2. Freight Forwarding

-

2.2.1. By Mode Of Transport

- 2.2.1.1. Air

- 2.2.1.2. Sea and Inland Waterways

- 2.2.1.3. Others

-

2.2.1. By Mode Of Transport

-

2.3. Freight Transport

- 2.3.1. Pipelines

- 2.3.2. Road

-

2.4. Warehousing and Storage

-

2.4.1. By Temperature Control

- 2.4.1.1. Non-Temperature Controlled

-

2.4.1. By Temperature Control

- 2.5. Other Services

-

2.1. Courier, Express, and Parcel (CEP)

Qatar Freight and Logistics Industry Segmentation By Geography

- 1. Qatar

Qatar Freight and Logistics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.98% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing trade relations; Increased demand for perishable goods

- 3.3. Market Restrains

- 3.3.1. Cargo theft; High cost of maintainig

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Qatar Freight and Logistics Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 5.1.1. Agriculture, Fishing, and Forestry

- 5.1.2. Construction

- 5.1.3. Manufacturing

- 5.1.4. Oil and Gas, Mining and Quarrying

- 5.1.5. Wholesale and Retail Trade

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Logistics Function

- 5.2.1. Courier, Express, and Parcel (CEP)

- 5.2.1.1. By Destination Type

- 5.2.1.1.1. Domestic

- 5.2.1.1.2. International

- 5.2.1.1. By Destination Type

- 5.2.2. Freight Forwarding

- 5.2.2.1. By Mode Of Transport

- 5.2.2.1.1. Air

- 5.2.2.1.2. Sea and Inland Waterways

- 5.2.2.1.3. Others

- 5.2.2.1. By Mode Of Transport

- 5.2.3. Freight Transport

- 5.2.3.1. Pipelines

- 5.2.3.2. Road

- 5.2.4. Warehousing and Storage

- 5.2.4.1. By Temperature Control

- 5.2.4.1.1. Non-Temperature Controlled

- 5.2.4.1. By Temperature Control

- 5.2.5. Other Services

- 5.2.1. Courier, Express, and Parcel (CEP)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Qatar

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 A P Moller - Maersk

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 DB Schenker

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 JAS Worldwide

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Qatar Navigation Q P S C ("Milaha")

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Gulf Agency Company (GAC)

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Bin Yousef Group of Companies W L L

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 DHL Group

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Tokyo Freight Service

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 DSV A/S (De Sammensluttede Vognmænd af Air and Sea)

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 E2E Global Lines

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Gulf Warehousing Company (GWC)

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Qatar Post

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 FedEx

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.14 Target Logistics Qatar

- 6.2.14.1. Overview

- 6.2.14.2. Products

- 6.2.14.3. SWOT Analysis

- 6.2.14.4. Recent Developments

- 6.2.14.5. Financials (Based on Availability)

- 6.2.15 Al Faisal Holding

- 6.2.15.1. Overview

- 6.2.15.2. Products

- 6.2.15.3. SWOT Analysis

- 6.2.15.4. Recent Developments

- 6.2.15.5. Financials (Based on Availability)

- 6.2.16 Kuehne + Nagel

- 6.2.16.1. Overview

- 6.2.16.2. Products

- 6.2.16.3. SWOT Analysis

- 6.2.16.4. Recent Developments

- 6.2.16.5. Financials (Based on Availability)

- 6.2.17 BCC Logistics

- 6.2.17.1. Overview

- 6.2.17.2. Products

- 6.2.17.3. SWOT Analysis

- 6.2.17.4. Recent Developments

- 6.2.17.5. Financials (Based on Availability)

- 6.2.18 Aerofrt (Aero Freight Company Ltd)

- 6.2.18.1. Overview

- 6.2.18.2. Products

- 6.2.18.3. SWOT Analysis

- 6.2.18.4. Recent Developments

- 6.2.18.5. Financials (Based on Availability)

- 6.2.19 Mannai Corporation QPSC

- 6.2.19.1. Overview

- 6.2.19.2. Products

- 6.2.19.3. SWOT Analysis

- 6.2.19.4. Recent Developments

- 6.2.19.5. Financials (Based on Availability)

- 6.2.20 Nakilat

- 6.2.20.1. Overview

- 6.2.20.2. Products

- 6.2.20.3. SWOT Analysis

- 6.2.20.4. Recent Developments

- 6.2.20.5. Financials (Based on Availability)

- 6.2.21 Qatar Airways Group

- 6.2.21.1. Overview

- 6.2.21.2. Products

- 6.2.21.3. SWOT Analysis

- 6.2.21.4. Recent Developments

- 6.2.21.5. Financials (Based on Availability)

- 6.2.22 Aramex

- 6.2.22.1. Overview

- 6.2.22.2. Products

- 6.2.22.3. SWOT Analysis

- 6.2.22.4. Recent Developments

- 6.2.22.5. Financials (Based on Availability)

- 6.2.23 Ali Bin Ali Holding

- 6.2.23.1. Overview

- 6.2.23.2. Products

- 6.2.23.3. SWOT Analysis

- 6.2.23.4. Recent Developments

- 6.2.23.5. Financials (Based on Availability)

- 6.2.24 Rumaillah Group

- 6.2.24.1. Overview

- 6.2.24.2. Products

- 6.2.24.3. SWOT Analysis

- 6.2.24.4. Recent Developments

- 6.2.24.5. Financials (Based on Availability)

- 6.2.1 A P Moller - Maersk

List of Figures

- Figure 1: Qatar Freight and Logistics Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Qatar Freight and Logistics Industry Share (%) by Company 2024

List of Tables

- Table 1: Qatar Freight and Logistics Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Qatar Freight and Logistics Industry Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 3: Qatar Freight and Logistics Industry Revenue Million Forecast, by Logistics Function 2019 & 2032

- Table 4: Qatar Freight and Logistics Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Qatar Freight and Logistics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Qatar Freight and Logistics Industry Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 7: Qatar Freight and Logistics Industry Revenue Million Forecast, by Logistics Function 2019 & 2032

- Table 8: Qatar Freight and Logistics Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Qatar Freight and Logistics Industry?

The projected CAGR is approximately 5.98%.

2. Which companies are prominent players in the Qatar Freight and Logistics Industry?

Key companies in the market include A P Moller - Maersk, DB Schenker, JAS Worldwide, Qatar Navigation Q P S C ("Milaha"), Gulf Agency Company (GAC), Bin Yousef Group of Companies W L L, DHL Group, Tokyo Freight Service, DSV A/S (De Sammensluttede Vognmænd af Air and Sea), E2E Global Lines, Gulf Warehousing Company (GWC), Qatar Post, FedEx, Target Logistics Qatar, Al Faisal Holding, Kuehne + Nagel, BCC Logistics, Aerofrt (Aero Freight Company Ltd), Mannai Corporation QPSC, Nakilat, Qatar Airways Group, Aramex, Ali Bin Ali Holding, Rumaillah Group.

3. What are the main segments of the Qatar Freight and Logistics Industry?

The market segments include End User Industry, Logistics Function.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Growing trade relations; Increased demand for perishable goods.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Cargo theft; High cost of maintainig.

8. Can you provide examples of recent developments in the market?

January 2024: Kuehne + Nagel has announced its Book & Claim insetting solution for electric vehicles, to improve its decarbonization solutions. Developing Book & Claim insetting solutions for road freight was a strategic priority for Kuehne + Nagel. Customers who use Kuehne + Nagel's road transport services can now claim the carbon reductions of electric trucks when it is not possible to physically move their goods on these vehicles.September 2023: Kuehne+Nagel and Capgemini have entered into a strategic agreement to create a supply chain orchestration service offering to provide end-to-end services across the supply chain network.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Qatar Freight and Logistics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Qatar Freight and Logistics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Qatar Freight and Logistics Industry?

To stay informed about further developments, trends, and reports in the Qatar Freight and Logistics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence