Key Insights

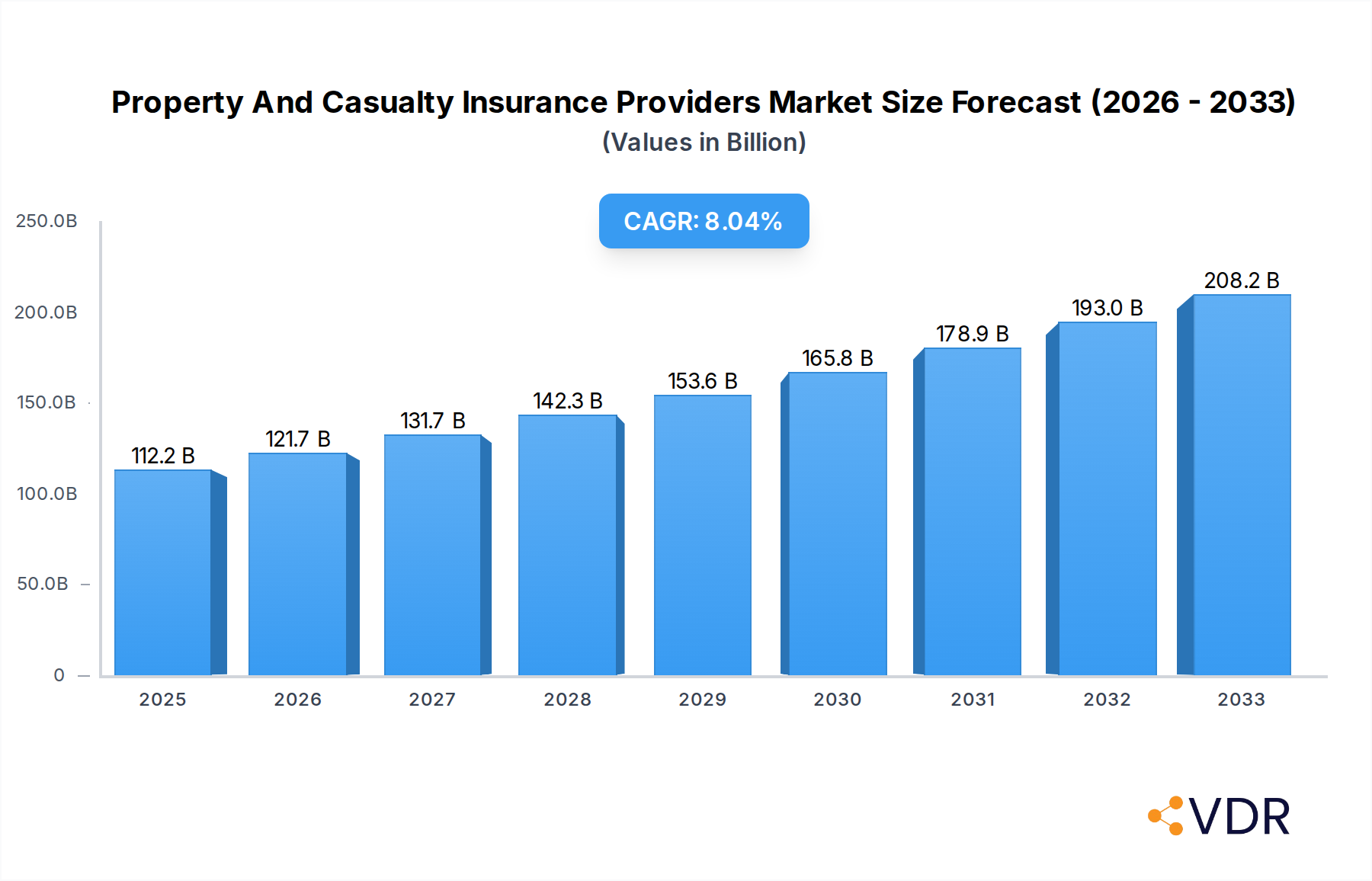

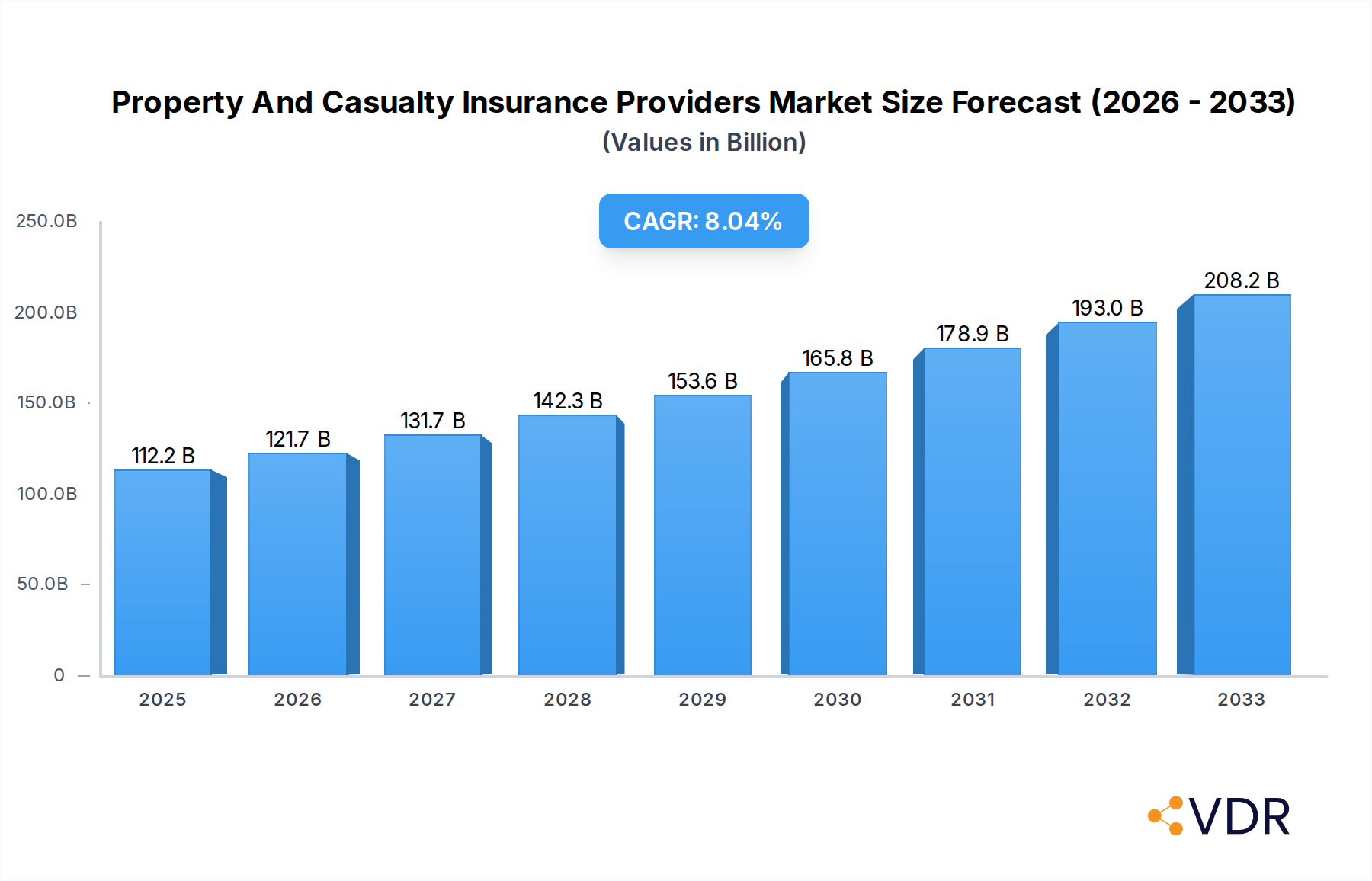

The global Property and Casualty (P&C) Insurance Providers market is poised for robust expansion, projected to reach an estimated $103.1 billion in 2024, with a compelling Compound Annual Growth Rate (CAGR) of 8.8% anticipated through 2033. This significant growth is primarily propelled by evolving consumer needs and increasing awareness of risk management across various sectors. The market's dynamism is further fueled by the increasing complexity of risks, from climate-related events to cyber threats, necessitating comprehensive insurance solutions. Furthermore, advancements in digital technologies are transforming the distribution landscape, with a growing emphasis on direct selling channels and the integration of data analytics to offer more personalized and efficient intermediary services. The P&C insurance sector is a cornerstone of financial stability, offering protection against unforeseen events for individuals and businesses alike.

Property And Casualty Insurance Providers Market Size (In Billion)

The P&C insurance market is characterized by a diverse range of applications and product types, catering to an extensive spectrum of risks. Key applications include intermediary services, which facilitate the complex relationship between insurers and policyholders, and direct selling, which is gaining traction through digital platforms and direct-to-consumer models. Within product types, Automobile Insurance Carriers, Liability Insurance Carriers, and Homeowners Insurance Carriers represent substantial segments, reflecting the widespread need for coverage against common risks. The market is segmented by the type of insurance provided, including Malpractice/Indemnity, Fidelity, Mortgage Guaranty, and Surety Insurance, each addressing specific industry and individual liabilities. Major players like Allstate, Berkshire Hathaway, Liberty Mutual, and Travelers Companies are actively shaping the market through innovation, strategic acquisitions, and a focus on customer-centric solutions, all contributing to the projected sustained growth and evolution of the P&C insurance industry.

Property And Casualty Insurance Providers Company Market Share

Here's a compelling, SEO-optimized report description for Property and Casualty Insurance Providers, designed for immediate use:

Property And Casualty Insurance Providers Market Dynamics & Structure

The global Property and Casualty (P&C) insurance market exhibits a moderately concentrated structure, with major players like Allstate, Berkshire Hathaway, Liberty Mutual, and Travelers Companies holding significant market share. Technological innovation, particularly in AI-driven underwriting and claims processing, acts as a primary driver, enhancing efficiency and customer experience. Robust regulatory frameworks, while ensuring consumer protection, also present compliance challenges. Competitive product substitutes, ranging from parametric insurance to alternative risk transfer mechanisms, are increasingly influencing market dynamics. End-user demographics are shifting towards digital-native consumers demanding personalized and accessible insurance solutions. Mergers and acquisitions (M&A) continue to reshape the landscape, with substantial deal volumes, for instance, an estimated $25 billion in M&A activity in 2023, as companies seek to consolidate portfolios and achieve economies of scale.

- Market Concentration: Dominated by a few key enterprises, indicating strong brand recognition and established distribution networks.

- Technological Innovation: Driven by insurtech advancements, predictive analytics, and IoT integration.

- Regulatory Frameworks: Evolving to address cyber risks, climate change impacts, and data privacy.

- Competitive Landscape: Increasing presence of insurtech startups and non-traditional players.

- End-User Demographics: Growing demand for mobile-first solutions and transparent policy terms.

- M&A Trends: Focus on acquiring technological capabilities and expanding market reach.

Property And Casualty Insurance Providers Growth Trends & Insights

The global Property and Casualty Insurance Providers market is projected for robust growth, driven by evolving consumer needs and technological advancements. The market size, estimated at $750 billion in 2025, is anticipated to expand at a Compound Annual Growth Rate (CAGR) of 5.2% through 2033, reaching an estimated $1.1 trillion. Adoption rates for digital insurance platforms and personalized policy offerings are accelerating, significantly influenced by increasing awareness of risks such as cyber threats and climate-related events. Technological disruptions, including the integration of AI for fraud detection and automated claims handling, are enhancing operational efficiency and customer satisfaction, pushing adoption rates of digital insurance products upwards by an estimated 15% annually.

Consumer behavior is shifting towards proactive risk management and a preference for bundled insurance products that offer comprehensive coverage. The rise of the sharing economy and the gig workforce is also creating new demand for specialized P&C insurance solutions. For example, the demand for commercial auto insurance for ride-sharing services has seen a significant uptick. Furthermore, the increasing focus on environmental, social, and governance (ESG) factors is influencing investment decisions and product development within the P&C sector. Insurers are increasingly developing parametric insurance products triggered by specific environmental events, reflecting a growing market penetration of these innovative solutions. The estimated market penetration for digital insurance services is expected to reach 60% by 2033.

The penetration of telematics in auto insurance, for instance, has grown by 20% over the past five years, enabling personalized pricing and incentivizing safer driving habits. This trend is a prime example of how technology is reshaping the industry, making insurance more dynamic and customer-centric. Moreover, the increasing complexity of global supply chains and the associated risks are driving demand for cargo and business interruption insurance, further contributing to market expansion. The estimated growth in demand for specialized commercial lines insurance is around 6% CAGR.

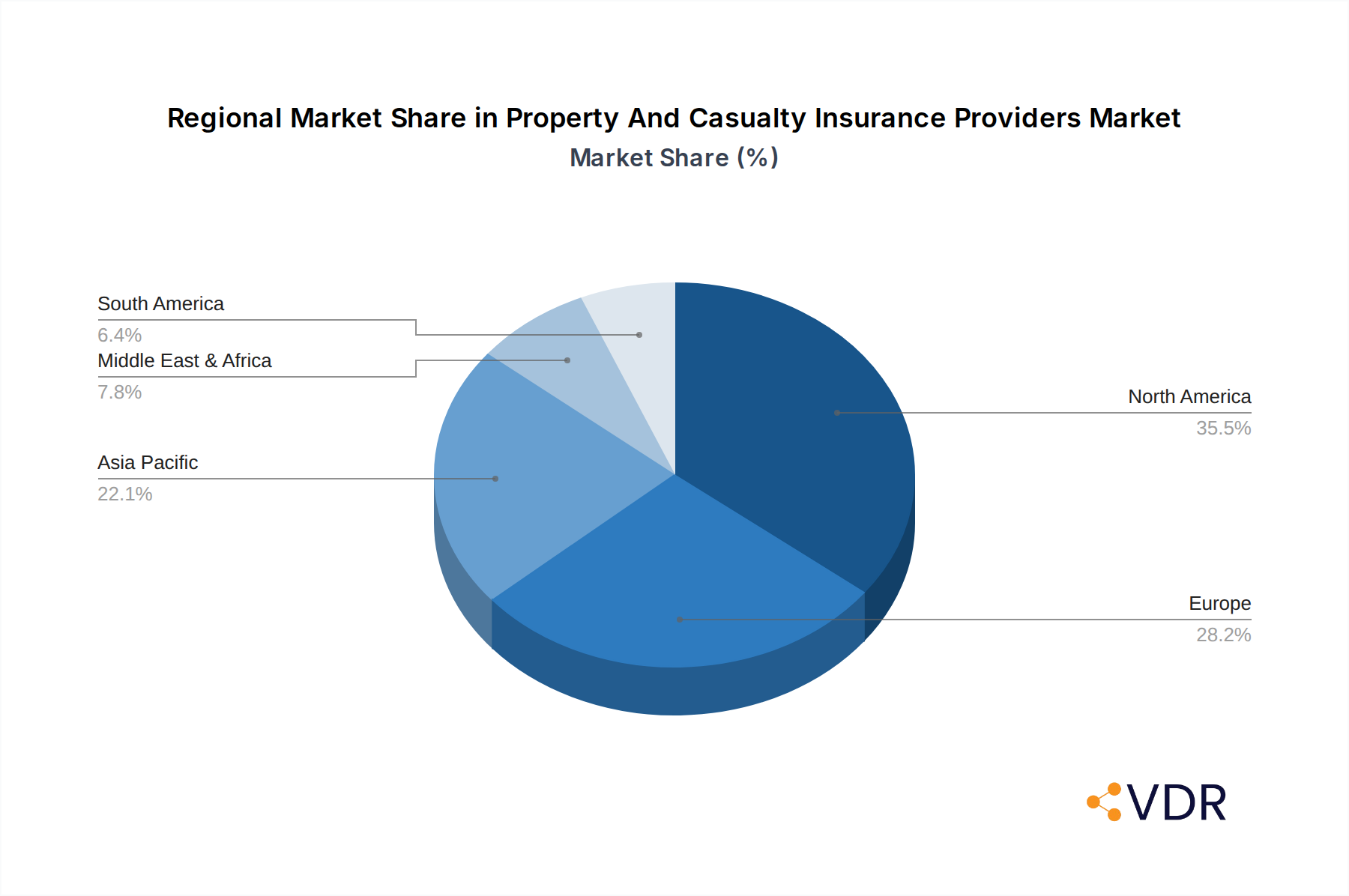

Dominant Regions, Countries, or Segments in Property And Casualty Insurance Providers

The North American region consistently dominates the global Property and Casualty Insurance Providers market, driven by a mature regulatory environment, high disposable incomes, and a strong emphasis on risk management. The United States, in particular, represents a significant portion of this dominance, accounting for an estimated 60% of the regional market share. Within the US, Automobile Insurance Carriers and Homeowners Insurance Carriers are the largest segments, reflecting the prevalence of vehicle ownership and property investments.

The dominance of North America is further bolstered by advanced technological adoption and a well-established intermediary channel. The intermediary segment, which includes agents and brokers, continues to be a crucial distribution avenue, facilitating an estimated 70% of P&C insurance sales. This segment's strength lies in its ability to offer personalized advice and complex product solutions to a diverse customer base. In contrast, the Direct Selling segment is experiencing rapid growth, driven by digital platforms and a younger demographic seeking convenience and cost-effectiveness.

Key Drivers of Dominance in North America:

- Economic Stability and Wealth: High per capita income translates to greater demand for comprehensive insurance coverage.

- Mature Regulatory Frameworks: Provides a stable and predictable operating environment for insurers.

- Technological Adoption: Early and widespread integration of insurtech solutions enhances efficiency and customer engagement.

- Consumer Awareness of Risk: A proactive approach to risk mitigation drives demand for various P&C insurance products.

- Robust Intermediary Network: Agents and brokers play a vital role in distributing complex insurance products.

Among the types of insurance carriers, Automobile Insurance Carriers and Homeowners Insurance Carriers are projected to maintain their leading positions, with estimated market sizes of $300 billion and $250 billion respectively in 2025. However, Liability Insurance Carriers are exhibiting a higher growth trajectory, fueled by increasing litigation and evolving corporate risk profiles, with an estimated CAGR of 6.5%. Malpractice/Indemnity Insurance Carriers also show steady growth, particularly in healthcare and professional services sectors. The mortgage Guaranty Insurance Carriers segment, while significant, is more susceptible to economic cycles.

Property And Casualty Insurance Providers Product Landscape

The Property and Casualty Insurance Providers sector is characterized by continuous product innovation, driven by evolving risk landscapes and technological advancements. Key product developments include the integration of AI and machine learning for dynamic risk assessment and personalized policy pricing, particularly in Automobile Insurance and Homeowners Insurance. Insurtech innovations are leading to the development of usage-based insurance (UBI) models and parametric insurance solutions that offer faster payouts for specific events. Performance metrics are increasingly focused on customer satisfaction scores, claims processing times, and risk-adjusted profitability. Unique selling propositions often revolve around seamless digital experiences, transparent policy terms, and tailored coverage options for emerging risks like cyber threats and climate change.

Key Drivers, Barriers & Challenges in Property And Casualty Insurance Providers

Key Drivers:

- Technological Advancements: AI, IoT, and big data analytics are revolutionizing underwriting, claims processing, and customer engagement, leading to increased efficiency and personalized offerings.

- Growing Awareness of Risks: Increasing frequency and severity of natural disasters, cyber-attacks, and global health crises are driving demand for P&C insurance.

- Economic Growth and Urbanization: Expanding economies and increasing urban populations lead to more insurable assets and higher demand for property and liability coverage.

- Regulatory Support for Innovation: Favorable regulatory environments in certain regions encourage the adoption of new technologies and business models.

Barriers & Challenges:

- Intense Competition: A saturated market with numerous players, including traditional insurers and emerging insurtechs, drives premium pressure and limits profitability.

- Regulatory Hurdles: Complex and varying regulatory landscapes across different jurisdictions can impede market entry and product standardization.

- Climate Change Impacts: Increasing frequency and severity of extreme weather events are leading to higher claims payouts and rising reinsurance costs, impacting profitability. The estimated increase in claims due to climate events is 10% annually.

- Talent Shortage: A critical shortage of skilled professionals in data science, actuarial science, and cybersecurity poses a significant challenge.

- Cybersecurity Threats: Insurers themselves are targets of sophisticated cyber-attacks, requiring substantial investment in security infrastructure.

Emerging Opportunities in Property And Casualty Insurance Providers

Emerging opportunities in the P&C insurance sector lie in catering to the needs of the gig economy and sharing economy, with tailored insurance products for freelancers and shared asset owners. The growing adoption of IoT devices in homes and vehicles presents a significant opportunity for preventative insurance and usage-based models. Furthermore, the increasing focus on ESG initiatives is opening doors for specialized insurance products covering climate-related risks, renewable energy projects, and corporate sustainability commitments. The burgeoning demand for cyber insurance, particularly among small and medium-sized enterprises (SMEs), represents a substantial untapped market, estimated to grow at 20% annually.

Growth Accelerators in the Property And Casualty Insurance Providers Industry

Growth accelerators for the P&C insurance industry are primarily driven by the widespread adoption of advanced digital technologies, including artificial intelligence and blockchain, which are streamlining operations and enhancing customer experience. Strategic partnerships between traditional insurers and insurtech startups are fostering innovation and expanding market reach. The increasing global awareness of climate change and its associated risks is stimulating demand for specialized insurance products. Moreover, proactive government initiatives aimed at improving financial literacy and promoting insurance penetration in developing economies are creating new avenues for market expansion.

Key Players Shaping the Property And Casualty Insurance Providers Market

- Allstate

- Berkshire Hathaway

- Liberty Mutual

- Travelers Companies

Notable Milestones in Property And Casualty Insurance Providers Sector

- 2019: Launch of advanced AI-powered claims processing systems by several major insurers, reducing processing times by an average of 30%.

- 2020: Significant increase in demand for cyber insurance products due to a surge in remote work and digital operations.

- 2021: Major insurers invest heavily in parametric insurance solutions to offer faster payouts for weather-related events.

- 2022: Increased M&A activity as larger players acquire insurtechs to gain technological capabilities.

- 2023: Greater emphasis on ESG factors influencing product development and investment strategies, with an estimated $50 billion allocated to sustainable insurance products globally.

- 2024: Rollout of enhanced telematics programs for auto insurance, offering personalized discounts based on driving behavior.

In-Depth Property And Casualty Insurance Providers Market Outlook

The outlook for the Property and Casualty Insurance Providers market remains exceptionally strong, fueled by the relentless pace of technological innovation and evolving risk landscapes. Growth accelerators such as the ubiquitous adoption of AI for predictive analytics and personalized customer experiences, alongside the expanding reach of IoT devices for real-time risk assessment, will continue to redefine the industry. Strategic collaborations between established carriers and agile insurtech firms are crucial for navigating complex market dynamics and unlocking new revenue streams. The increasing global awareness of climate change and its unpredictable impacts is not only driving demand for specialized coverages but also spurring innovation in resilience and adaptation solutions. Furthermore, proactive regulatory support and initiatives aimed at enhancing financial inclusion in emerging economies will create fertile ground for market expansion. The P&C insurance sector is poised for sustained growth, with an estimated market CAGR of 5.2% from 2025 to 2033.

Property And Casualty Insurance Providers Segmentation

-

1. Application

- 1.1. Intermediary

- 1.2. Direct Selling

-

2. Types

- 2.1. Automobile Insurance Carriers

- 2.2. Malpractice/Indemnity Insurance Carriers

- 2.3. Fidelity Insurance Carriers

- 2.4. Mortgage Guaranty Insurance Carriers

- 2.5. Homeowners Insurance Carriers

- 2.6. Surety Insurance Carriers

- 2.7. Liability Insurance Carriers

Property And Casualty Insurance Providers Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Property And Casualty Insurance Providers Regional Market Share

Geographic Coverage of Property And Casualty Insurance Providers

Property And Casualty Insurance Providers REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Intermediary

- 5.1.2. Direct Selling

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Automobile Insurance Carriers

- 5.2.2. Malpractice/Indemnity Insurance Carriers

- 5.2.3. Fidelity Insurance Carriers

- 5.2.4. Mortgage Guaranty Insurance Carriers

- 5.2.5. Homeowners Insurance Carriers

- 5.2.6. Surety Insurance Carriers

- 5.2.7. Liability Insurance Carriers

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Property And Casualty Insurance Providers Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Intermediary

- 6.1.2. Direct Selling

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Automobile Insurance Carriers

- 6.2.2. Malpractice/Indemnity Insurance Carriers

- 6.2.3. Fidelity Insurance Carriers

- 6.2.4. Mortgage Guaranty Insurance Carriers

- 6.2.5. Homeowners Insurance Carriers

- 6.2.6. Surety Insurance Carriers

- 6.2.7. Liability Insurance Carriers

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Property And Casualty Insurance Providers Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Intermediary

- 7.1.2. Direct Selling

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Automobile Insurance Carriers

- 7.2.2. Malpractice/Indemnity Insurance Carriers

- 7.2.3. Fidelity Insurance Carriers

- 7.2.4. Mortgage Guaranty Insurance Carriers

- 7.2.5. Homeowners Insurance Carriers

- 7.2.6. Surety Insurance Carriers

- 7.2.7. Liability Insurance Carriers

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Property And Casualty Insurance Providers Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Intermediary

- 8.1.2. Direct Selling

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Automobile Insurance Carriers

- 8.2.2. Malpractice/Indemnity Insurance Carriers

- 8.2.3. Fidelity Insurance Carriers

- 8.2.4. Mortgage Guaranty Insurance Carriers

- 8.2.5. Homeowners Insurance Carriers

- 8.2.6. Surety Insurance Carriers

- 8.2.7. Liability Insurance Carriers

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Property And Casualty Insurance Providers Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Intermediary

- 9.1.2. Direct Selling

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Automobile Insurance Carriers

- 9.2.2. Malpractice/Indemnity Insurance Carriers

- 9.2.3. Fidelity Insurance Carriers

- 9.2.4. Mortgage Guaranty Insurance Carriers

- 9.2.5. Homeowners Insurance Carriers

- 9.2.6. Surety Insurance Carriers

- 9.2.7. Liability Insurance Carriers

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Property And Casualty Insurance Providers Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Intermediary

- 10.1.2. Direct Selling

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Automobile Insurance Carriers

- 10.2.2. Malpractice/Indemnity Insurance Carriers

- 10.2.3. Fidelity Insurance Carriers

- 10.2.4. Mortgage Guaranty Insurance Carriers

- 10.2.5. Homeowners Insurance Carriers

- 10.2.6. Surety Insurance Carriers

- 10.2.7. Liability Insurance Carriers

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Property And Casualty Insurance Providers Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Intermediary

- 11.1.2. Direct Selling

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Automobile Insurance Carriers

- 11.2.2. Malpractice/Indemnity Insurance Carriers

- 11.2.3. Fidelity Insurance Carriers

- 11.2.4. Mortgage Guaranty Insurance Carriers

- 11.2.5. Homeowners Insurance Carriers

- 11.2.6. Surety Insurance Carriers

- 11.2.7. Liability Insurance Carriers

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Allstate

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Berkshire Hathaway

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Liberty Mutual

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Travelers Companies

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.1 Allstate

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Property And Casualty Insurance Providers Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Property And Casualty Insurance Providers Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Property And Casualty Insurance Providers Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Property And Casualty Insurance Providers Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Property And Casualty Insurance Providers Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Property And Casualty Insurance Providers Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Property And Casualty Insurance Providers Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Property And Casualty Insurance Providers Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Property And Casualty Insurance Providers Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Property And Casualty Insurance Providers Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Property And Casualty Insurance Providers Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Property And Casualty Insurance Providers Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Property And Casualty Insurance Providers Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Property And Casualty Insurance Providers Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Property And Casualty Insurance Providers Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Property And Casualty Insurance Providers Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Property And Casualty Insurance Providers Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Property And Casualty Insurance Providers Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Property And Casualty Insurance Providers Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Property And Casualty Insurance Providers Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Property And Casualty Insurance Providers Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Property And Casualty Insurance Providers Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Property And Casualty Insurance Providers Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Property And Casualty Insurance Providers Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Property And Casualty Insurance Providers Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Property And Casualty Insurance Providers Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Property And Casualty Insurance Providers Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Property And Casualty Insurance Providers Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Property And Casualty Insurance Providers Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Property And Casualty Insurance Providers Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Property And Casualty Insurance Providers Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Property And Casualty Insurance Providers?

The projected CAGR is approximately 8.8%.

2. Which companies are prominent players in the Property And Casualty Insurance Providers?

Key companies in the market include Allstate, Berkshire Hathaway, Liberty Mutual, Travelers Companies.

3. What are the main segments of the Property And Casualty Insurance Providers?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 103.1 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Property And Casualty Insurance Providers," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Property And Casualty Insurance Providers report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Property And Casualty Insurance Providers?

To stay informed about further developments, trends, and reports in the Property And Casualty Insurance Providers, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence