Key Insights

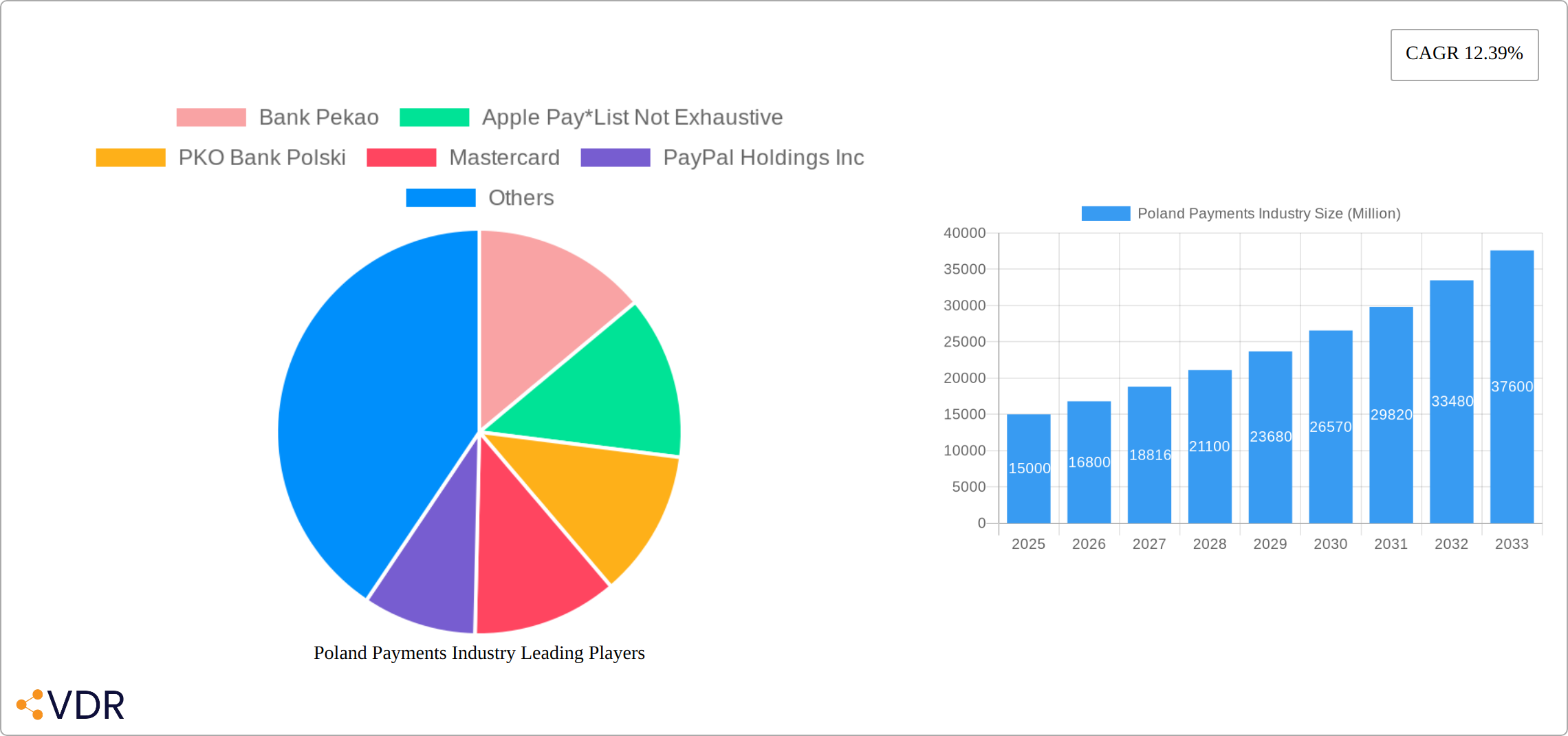

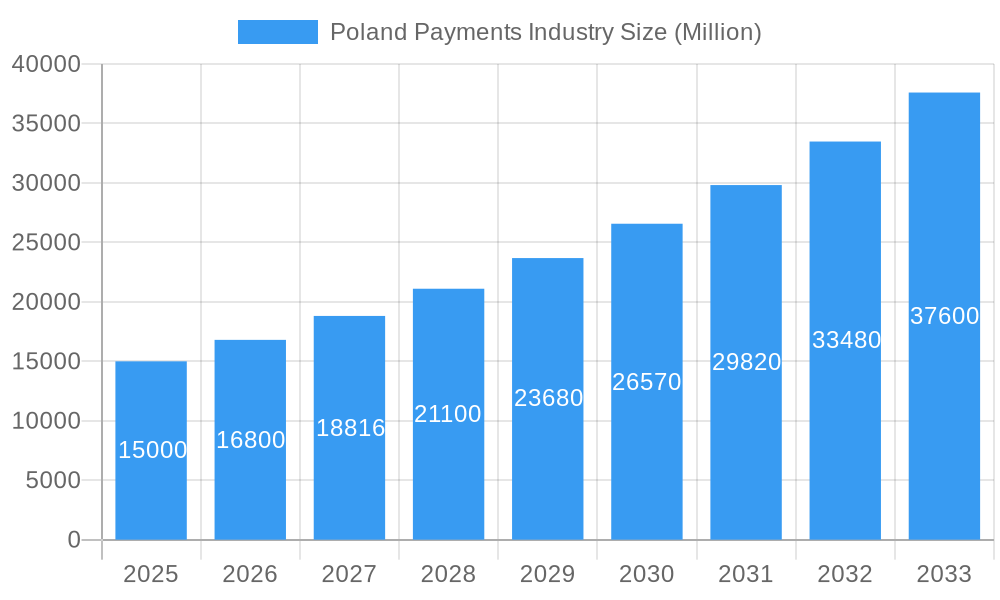

The Poland payments industry, currently experiencing robust growth, presents a compelling investment opportunity. With a Compound Annual Growth Rate (CAGR) of 12.39% from 2019 to 2024, the market exhibits strong momentum driven by increasing digitalization, expanding e-commerce adoption, and rising smartphone penetration. Key drivers include the government's push for digital financial inclusion, a growing young and tech-savvy population readily adopting contactless payments, and the increasing prevalence of online banking and mobile wallets. The market is segmented by payment mode (point-of-sale and online) and end-user industry (retail, entertainment, healthcare, hospitality, and others). Major players like Bank Pekao, PKO Bank Polski, Mastercard, PayPal, and others compete in this dynamic landscape, shaping the future of payments within the country. The growth is further fueled by innovations in mobile payment technologies and increasing consumer preference for secure and convenient digital transaction methods. The increasing adoption of Buy Now Pay Later (BNPL) services also contributes to the growth, although regulatory challenges may influence the sector’s expansion. While data limitations prevent precise market sizing, considering the CAGR and the market trends, a reasonable projection for 2025 could be several billion PLN, with further significant growth expected until 2033.

Poland Payments Industry Market Size (In Billion)

The competitive landscape is characterized by both domestic and international players, each leveraging their strengths in technology, network reach, and brand recognition. While point-of-sale transactions still dominate, online payments are witnessing exponential growth, fueled by the rise of e-commerce and the increasing comfort level of consumers with digital transactions. Future growth is expected to be driven by the expansion of mobile payment services, the adoption of innovative payment technologies like biometric authentication, and initiatives to enhance cybersecurity and fraud prevention measures. Continued regulatory oversight will play a crucial role in shaping the industry’s trajectory, ensuring a secure and transparent payment ecosystem for consumers and businesses alike. The Polish payments market offers a significant growth potential for businesses seeking to capitalize on the trends of digitization and financial inclusion.

Poland Payments Industry Company Market Share

This comprehensive report provides a detailed analysis of the Poland payments industry, covering market dynamics, growth trends, dominant segments, key players, and future outlook. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report is an invaluable resource for industry professionals, investors, and strategic decision-makers. The report leverages extensive primary and secondary research to offer actionable insights and projections for this rapidly evolving market. Market values are presented in millions.

Poland Payments Industry Market Dynamics & Structure

The Polish payments market is characterized by a dynamic interplay of established players and emerging fintechs, fostering intense competition and driving innovation. Market concentration is moderate, with a few major banks holding significant market share, but a growing number of smaller players and fintech companies increasingly challenging the status quo. Technological advancements, particularly in mobile payments and contactless solutions, are key drivers of growth. The regulatory framework, while evolving, generally supports innovation while ensuring consumer protection. The increasing adoption of e-commerce and digital channels is fueling the growth of online payment methods, while traditional methods like cash remain relevant in certain segments. Substitutes, such as cryptocurrencies, are gaining traction, albeit slowly. The end-user demographic is increasingly digitally savvy, particularly amongst younger generations, driving demand for advanced payment solutions. M&A activity has been moderate, with larger players acquiring smaller fintechs to expand their capabilities and market reach. The overall market is valued at xx Million in 2025.

- Market Concentration: Moderate, with top 5 players holding approximately 60% market share (2025).

- Technological Innovation: Driven by mobile payments, contactless technology, and BNPL solutions.

- Regulatory Framework: Supportive of innovation with a focus on consumer protection.

- Competitive Substitutes: Cryptocurrencies and alternative payment methods are emerging but represent a small market share (xx Million in 2025).

- End-User Demographics: Growing digital literacy, particularly among younger generations.

- M&A Trends: Moderate activity, with larger players acquiring smaller fintechs. xx M&A deals in the historical period.

Poland Payments Industry Growth Trends & Insights

The Polish payments market has witnessed robust growth in recent years, driven by rising e-commerce adoption, increasing smartphone penetration, and the government's push for digitalization. The market size expanded significantly from xx Million in 2019 to xx Million in 2024, exhibiting a CAGR of xx%. This growth is anticipated to continue, with the market projected to reach xx Million by 2033, reflecting a CAGR of xx% during the forecast period. Key factors driving this growth include the increasing preference for contactless payments, the expansion of BNPL services, and the growing popularity of mobile wallets. Consumer behavior is shifting towards greater convenience and digitalization, fostering the adoption of innovative payment solutions. Technological disruptions, such as the rise of open banking and embedded finance, are reshaping the competitive landscape.

Dominant Regions, Countries, or Segments in Poland Payments Industry

The Polish payments landscape is dynamic, with the retail sector leading the charge, fueled by robust e-commerce expansion and rising consumer spending. Point-of-sale (POS) transactions maintain the largest market share, significantly boosted by widespread card adoption and the rapid growth of contactless payments. Online sales represent a substantial and rapidly growing portion of the market, mirroring the increasing popularity of online shopping platforms. While urban centers demonstrate higher digital payment penetration, a considerable opportunity exists to expand financial inclusion in rural areas.

- By Mode of Payment (projected 2025): Point-of-Sale (POS) commands the largest market share ([Insert Specific Value in Millions]), followed closely by online sales ([Insert Specific Value in Millions]). Other payment methods contribute [Insert Specific Value in Millions].

- By End-user Industry (projected 2025): The retail sector is the dominant player ([Insert Specific Value in Millions]), with entertainment ([Insert Specific Value in Millions]) and hospitality ([Insert Specific Value in Millions]) following closely. Healthcare and other industries contribute [Insert Specific Value in Millions] and [Insert Specific Value in Millions] respectively.

- Key Drivers: The Polish payments industry thrives on several key factors: the explosive growth of e-commerce, soaring smartphone penetration rates, and government-backed initiatives aimed at accelerating digitalization. These factors work synergistically to foster innovation and growth.

Poland Payments Industry Product Landscape

Poland's diverse payments ecosystem offers a comprehensive range of products, encompassing credit and debit cards, mobile wallets, secure online payment gateways, and the increasingly popular Buy Now, Pay Later (BNPL) solutions. Continuous innovation defines this market, with ongoing enhancements to existing products and the introduction of new features to optimize user experience and bolster security. Key advancements include biometric authentication, advanced tokenization for enhanced security, and sophisticated fraud prevention systems. The market is experiencing a significant upswing in contactless payment adoption and the seamless integration of payments into various platforms and applications.

Key Drivers, Barriers & Challenges in Poland Payments Industry

Key Drivers:

- Unprecedented growth of e-commerce adoption

- Rapidly increasing smartphone penetration rates

- Government support through strategic digitalization initiatives

- Significant expansion of BNPL services, creating new market segments

Challenges:

- Maintaining robust, constantly evolving security measures to combat sophisticated fraud attempts.

- Ensuring seamless interoperability across diverse payment systems and platforms.

- Adapting rapidly to evolving consumer preferences and the accelerating pace of technological advancements.

- Addressing the persistent digital divide and ensuring access to digital financial services for all citizens. An estimated [Insert Specific Percentage]% of the population lacked reliable internet access in 2025 (projected).

Emerging Opportunities in Poland Payments Industry

- Expansion of BNPL services to reach underserved market segments.

- Meeting the increasing demand for embedded finance solutions integrated into various applications and services.

- Capitalizing on the growing adoption of mobile wallets and contactless payment methods.

- Developing innovative payment solutions specifically tailored to the unique needs of different industry sectors.

Growth Accelerators in the Poland Payments Industry

Continued growth will be fueled by technological advancements, strategic partnerships between banks and fintech companies, and expansion into new markets. The increasing integration of payments into everyday applications and the rise of open banking will further accelerate market growth.

Key Players Shaping the Poland Payments Industry Market

- Bank Pekao

- Apple Pay

- PKO Bank Polski

- Mastercard

- PayPal Holdings Inc

- PayU

- Santander Bank Polska

- DotPay

- American Express

- Tap2Pay me

Notable Milestones in Poland Payments Industry Sector

- May 2022: Allegro launched a new cash-on-delivery payment option enabling card and smartphone contactless payments via courier devices.

- May 2022: PKO BP announced the completion of its BNPL (Buy Now, Pay Later) solution, intending to make it widely available across Polish online stores.

In-Depth Poland Payments Industry Market Outlook

The Polish payments market is poised for sustained growth, driven by ongoing digitalization, increasing e-commerce adoption, and the emergence of innovative payment solutions. Strategic partnerships, technological advancements, and government support will play a crucial role in shaping the future of the market. The expansion of financial inclusion and the integration of payments into various applications will create significant opportunities for players in the coming years.

Poland Payments Industry Segmentation

-

1. Mode of Payment

-

1.1. Point of Sale

- 1.1.1. Card Pay

- 1.1.2. Digital Wallet (includes Mobile Wallets)

- 1.1.3. Cash

- 1.1.4. Others

-

1.2. Online Sale

- 1.2.1. Others (

-

1.1. Point of Sale

-

2. End-user Industry

- 2.1. Retail

- 2.2. Entertainment

- 2.3. Healthcare

- 2.4. Hospitality

- 2.5. Other End-user Industries

Poland Payments Industry Segmentation By Geography

- 1. Poland

Poland Payments Industry Regional Market Share

Geographic Coverage of Poland Payments Industry

Poland Payments Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.39% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Advancements in the Polish Payments Market; Initiatives by the Government to improve cashless payment methods

- 3.3. Market Restrains

- 3.3.1. Lack of a standard legislative policy remains especially in the case of cross-border transactions

- 3.4. Market Trends

- 3.4.1. Advancements in the Polish Payments Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Poland Payments Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 5.1.1. Point of Sale

- 5.1.1.1. Card Pay

- 5.1.1.2. Digital Wallet (includes Mobile Wallets)

- 5.1.1.3. Cash

- 5.1.1.4. Others

- 5.1.2. Online Sale

- 5.1.2.1. Others (

- 5.1.1. Point of Sale

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Retail

- 5.2.2. Entertainment

- 5.2.3. Healthcare

- 5.2.4. Hospitality

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Poland

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Bank Pekao

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Apple Pay*List Not Exhaustive

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 PKO Bank Polski

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Mastercard

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 PayPal Holdings Inc

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 PayU

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Santander Bank Polska

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 DotPay

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 American Express

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Tap2Pay me

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Bank Pekao

List of Figures

- Figure 1: Poland Payments Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Poland Payments Industry Share (%) by Company 2025

List of Tables

- Table 1: Poland Payments Industry Revenue Million Forecast, by Mode of Payment 2020 & 2033

- Table 2: Poland Payments Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 3: Poland Payments Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Poland Payments Industry Revenue Million Forecast, by Mode of Payment 2020 & 2033

- Table 5: Poland Payments Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Poland Payments Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Poland Payments Industry?

The projected CAGR is approximately 12.39%.

2. Which companies are prominent players in the Poland Payments Industry?

Key companies in the market include Bank Pekao, Apple Pay*List Not Exhaustive, PKO Bank Polski, Mastercard, PayPal Holdings Inc, PayU, Santander Bank Polska, DotPay, American Express, Tap2Pay me.

3. What are the main segments of the Poland Payments Industry?

The market segments include Mode of Payment, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Advancements in the Polish Payments Market; Initiatives by the Government to improve cashless payment methods.

6. What are the notable trends driving market growth?

Advancements in the Polish Payments Market.

7. Are there any restraints impacting market growth?

Lack of a standard legislative policy remains especially in the case of cross-border transactions.

8. Can you provide examples of recent developments in the market?

May 2022 - Allegro announced a new service implemented in one of the platform's delivery methods - One Kurier. Customers using this method and paying for cash-on-delivery purchases can pay by card or smartphone using the contactless method on the courier's device used to manage shipments.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Poland Payments Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Poland Payments Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Poland Payments Industry?

To stay informed about further developments, trends, and reports in the Poland Payments Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence