Key Insights

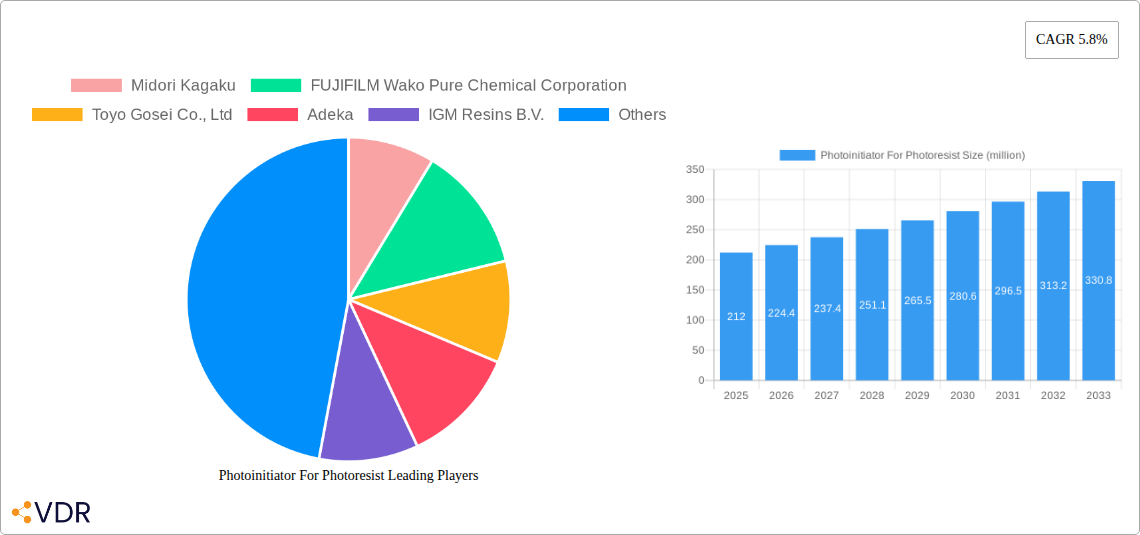

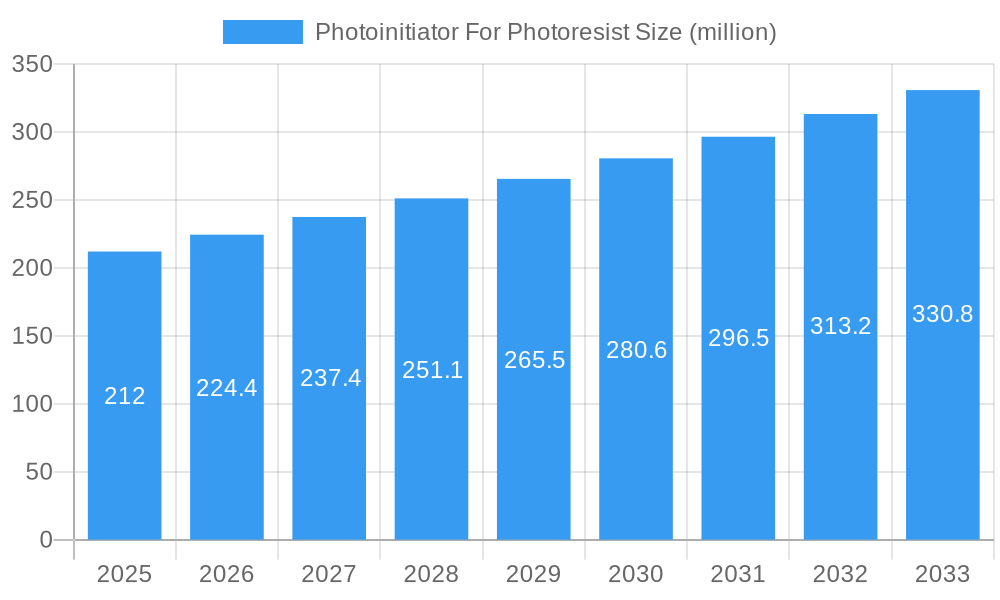

The global market for photoinitiators used in photoresists is poised for substantial growth, driven by the ever-increasing demand for advanced semiconductor manufacturing and the miniaturization of electronic devices. With a current market size estimated at $212 million, the industry is projected to expand at a Compound Annual Growth Rate (CAGR) of 5.8% over the forecast period of 2025-2033. This robust growth is underpinned by key drivers such as the relentless innovation in semiconductor technology, particularly the shift towards smaller and more complex chip designs that necessitate sophisticated photoresist materials. The rising adoption of EUV (Extreme Ultraviolet) lithography, which requires highly sensitive and efficient photoinitiators, is a significant catalyst. Furthermore, the burgeoning Internet of Things (IoT) market, the expansion of 5G networks, and the increasing use of artificial intelligence are all fueling the demand for more powerful and efficient semiconductors, thereby boosting the photoinitiator market.

Photoinitiator For Photoresist Market Size (In Million)

The market is segmented by application into EUV Photoresist, ArF Photoresist, KrF Photoresist, and g/i-Line Photoresist, with EUV photoresists representing a critical growth area due to their role in next-generation chip production. By type, the market is divided into Photo Acid Generator (PAG) and Photo Acid Compound (PAC) photoinitiators, both of which are essential components in the photolithography process. Restraints such as the high cost of R&D for novel photoinitiator formulations and stringent environmental regulations concerning chemical usage in semiconductor manufacturing could pose challenges. However, ongoing research and development efforts focused on enhancing photoinitiator performance, improving their safety profiles, and developing more cost-effective synthesis routes are expected to mitigate these constraints. Key players like FUJIFILM Wako Pure Chemical Corporation, Toyo Gosei Co., Ltd, and Adeka are actively investing in innovation to capture market share and address the evolving needs of the semiconductor industry. Asia Pacific, particularly China and South Korea, is expected to dominate the market owing to its strong presence in semiconductor manufacturing.

Photoinitiator For Photoresist Company Market Share

Here is a compelling, SEO-optimized report description for Photoinitiator For Photoresist, integrated with high-traffic keywords and market segmentation:

Report Title: Global Photoinitiator For Photoresist Market: In-Depth Analysis, Trends, Opportunities & Forecasts (2019-2033)

Report Description:

Unlock critical insights into the dynamic global Photoinitiator for Photoresist market, a vital component in the advanced electronics and semiconductor industries. This comprehensive report provides an in-depth analysis of photoinitiator compounds and photo acid generators (PAGs), essential for EUV photoresist, ArF photoresist, KrF photoresist, and g/i-Line photoresist applications. Dive deep into market growth trends, technological innovations, and competitive strategies shaping the future of lithography.

The photoinitiator market is experiencing robust growth driven by the escalating demand for advanced semiconductor devices and microelectronics. This report meticulously examines key market drivers, including the relentless pursuit of miniaturization in integrated circuits, the proliferation of high-performance computing, and the increasing sophistication of display technologies. We analyze the intricate supply chain, from photoinitiator raw material suppliers to end-users in the semiconductor fabrication sector.

Explore the evolving landscape of photoresist chemicals, focusing on the critical role of photoinitiators in enabling high-resolution patterning. Understand the impact of stringent quality standards and the continuous innovation required to meet the demanding specifications of next-generation lithography processes. This report offers a granular view of regional market dynamics, competitive intelligence on leading manufacturers like Midori Kagaku, FUJIFILM Wako Pure Chemical Corporation, Toyo Gosei Co., Ltd, Adeka, IGM Resins B.V., Heraeus Epurio, Miwon Commercial Co., Ltd., Daito Chemix Corporation, CGP Materials, ENF Technology, NC Chem, TAKOMA TECHNOLOGY CORPORATION, Xuzhou B & C Chemical, Changzhou Tronly New Electronic Materials, Tianjin Jiuri New Material, and Suzhou Weimas.

With a study period from 2019 to 2033, this report offers a robust outlook based on a base year of 2025 and an estimated year of 2025, projecting trends through the forecast period of 2025–2033 and analyzing historical data from 2019–2024. Gain a strategic advantage by understanding the parent market of specialty chemicals and the child market of photoinitiators for advanced lithography. This report is an indispensable resource for stakeholders seeking to navigate the complexities and capitalize on the immense opportunities within the global Photoinitiator for Photoresist market.

Photoinitiator For Photoresist Market Dynamics & Structure

The global photoinitiator for photoresist market exhibits a moderately concentrated structure, with a few key players holding significant market shares. Technological innovation is the primary driver, fueled by the relentless demand for higher resolution and sensitivity in semiconductor lithography processes, particularly for advanced nodes like EUV. Regulatory frameworks primarily focus on environmental safety and chemical handling, indirectly influencing product development towards more sustainable and less hazardous formulations. Competitive product substitutes are limited due to the specialized nature of photoinitiators in photoresist formulations, but ongoing research into novel photoacid generator (PAG) and photo acid compound (PAC) chemistries aims to improve performance and reduce costs. End-user demographics are dominated by semiconductor manufacturers, advanced display producers, and microelectronics fabrication facilities. Mergers and acquisitions (M&A) trends are observed as larger chemical companies seek to consolidate their portfolios and gain access to proprietary technologies.

- Market Concentration: Dominated by a blend of established chemical giants and specialized photoinitiator manufacturers.

- Technological Innovation: Driven by demands for EUV lithography, ArF immersion, and improved performance in KrF and g/i-line processes.

- Regulatory Landscape: Focus on environmental impact reduction and REACH compliance.

- Competitive Substitutes: Limited in core photoresist applications but explored through novel chemical synthesis and formulation.

- End-User Demographics: Primarily semiconductor fabs, R&D institutions, and advanced packaging firms.

- M&A Trends: Strategic acquisitions aimed at broadening product portfolios and securing intellectual property.

Photoinitiator For Photoresist Growth Trends & Insights

The global photoinitiator for photoresist market is poised for significant expansion, projected to grow at a robust Compound Annual Growth Rate (CAGR) of xx% from 2019 to 2033. This growth trajectory is fundamentally underpinned by the insatiable global appetite for advanced semiconductor devices, which are integral to virtually every facet of modern life, from artificial intelligence and 5G networks to the Internet of Things (IoT) and autonomous vehicles. The relentless pursuit of smaller, more powerful, and energy-efficient microchips necessitates continuous advancements in lithography techniques, and photoinitiators are at the forefront of this evolution. Specifically, the increasing adoption of Extreme Ultraviolet (EUV) lithography for cutting-edge chip manufacturing is a major catalyst, as EUV resists require highly efficient and specialized photoinitiators to achieve the sub-10nm feature sizes demanded by advanced nodes. Similarly, the ongoing reliance on ArF immersion lithography for mid-node production continues to drive demand for advanced ArF photoinitiators, known for their high resolution and sensitivity.

The adoption rates for specific photoinitiator types are directly correlated with the dominant lithography technologies in use. While g/i-line and KrF photoresists still hold significant market share in certain legacy and specialized applications, the market's future growth is heavily skewed towards ArF and, more critically, EUV applications. Technological disruptions, such as the development of novel photoacid generator (PAG) and photo acid compound (PAC) chemistries, are continuously pushing the boundaries of lithographic performance. These innovations aim to enhance quantum efficiency, reduce line edge roughness (LER), and improve process latitude, thereby enabling manufacturers to produce more complex and performant integrated circuits at a faster pace and potentially lower cost. Consumer behavior shifts, while indirect, play a role through the demand for end-products like smartphones, laptops, and wearable devices, which directly influence the volume requirements for semiconductor manufacturing. The market penetration of advanced lithography techniques, therefore, directly translates into higher demand for sophisticated photoinitiators. The estimated market size for photoinitiators in the photoresist segment is projected to reach approximately $xx billion by 2025, with substantial growth expected throughout the forecast period, driven by investments in new fabrication facilities and the ongoing technological race among leading semiconductor manufacturers.

Dominant Regions, Countries, or Segments in Photoinitiator For Photoresist

The global Photoinitiator for Photoresist market is experiencing pronounced dominance from specific application segments and geographical regions, driven by concentrated semiconductor manufacturing capabilities and strategic technological investments. Among the applications, ArF Photoresist currently represents a significant portion of the market share, owing to its widespread use in manufacturing advanced logic and memory chips. However, the trajectory clearly indicates that EUV Photoresist is the segment with the highest growth potential. The increasing investment in EUV lithography by leading semiconductor foundries for sub-10nm nodes is propelling demand for highly specialized EUV photoinitiators. While KrF Photoresist and g/i-line Photoresist applications continue to be relevant for older technology nodes and specific niche markets, their growth is outpaced by the rapid advancements in ArF and EUV.

In terms of market type, Photo Acid Generator (PAG) dominates the market. PAGs are a cornerstone of modern chemically amplified photoresists (CARs) and are crucial for generating acids upon irradiation, which then catalyze the deprotection or cross-linking reactions necessary for pattern formation. Their superior performance characteristics, including high quantum efficiency and tunability for different wavelengths, make them indispensable for advanced lithography. Photo Acid Compounds (PACs), while historically important and still utilized in certain formulations, generally offer lower performance for the most demanding lithography applications compared to PAGs.

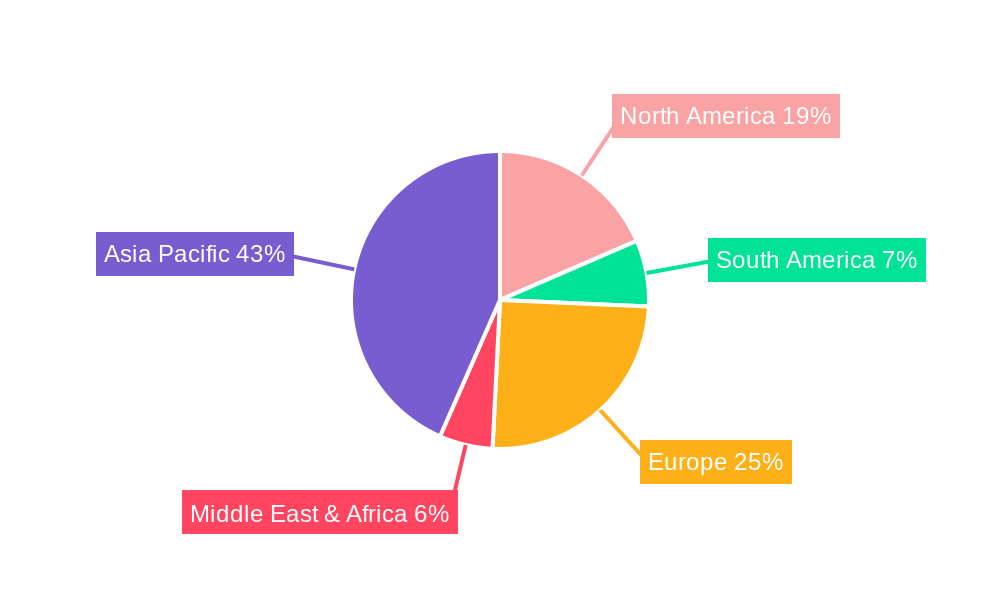

Geographically, Asia-Pacific stands out as the dominant region in the Photoinitiator for Photoresist market. This dominance is primarily attributed to the concentration of major semiconductor manufacturing hubs in countries like South Korea, Taiwan, and China. South Korea, with its leading memory and foundry players, and Taiwan, home to the world's largest contract chip manufacturer, are significant consumers of photoresists and their constituent photoinitiators. China's aggressive expansion in its domestic semiconductor industry further bolsters demand. The presence of established chemical manufacturing infrastructure and a skilled workforce in these regions also contributes to their leading position. Government initiatives aimed at promoting domestic semiconductor production and R&D, coupled with substantial foreign direct investment, continue to fuel market growth in this region. The market share within Asia-Pacific is substantial, estimated to be around xx% of the global market, with a projected CAGR of xx% over the forecast period. Infrastructure development, supportive economic policies, and a strong ecosystem of electronics manufacturing are key drivers of this regional dominance.

Photoinitiator For Photoresist Product Landscape

The Photoinitiator for Photoresist market is characterized by a landscape of highly specialized and performance-driven products. Innovations are focused on developing photoinitiators with enhanced quantum efficiencies, lower absorption at specific wavelengths, and improved thermal stability to meet the stringent requirements of advanced lithography. Key product advancements include the synthesis of novel Photo Acid Generators (PAGs) for EUV lithography that can efficiently generate acids with minimal outgassing, crucial for maintaining vacuum environments. Formulations are increasingly tailored for specific photoresist types, such as ArF immersion, KrF, and g/i-line, to optimize resolution, sensitivity, and line edge roughness. Unique selling propositions often lie in proprietary chemical structures that enable faster curing, reduced defectivity, and compatibility with emerging resist chemistries, ensuring sharper and more accurate pattern transfer.

Key Drivers, Barriers & Challenges in Photoinitiator For Photoresist

The photoinitiator for photoresist market is propelled by several key drivers. The relentless miniaturization of semiconductor devices, driven by the demand for higher computing power and increased functionality in electronics, is a primary catalyst. Advancements in lithography technologies, particularly the adoption of EUV and next-generation ArF immersion, necessitate the development of more sophisticated and efficient photoinitiators. Furthermore, the growth of the display industry, including high-resolution OLED and micro-LED displays, also contributes to demand. Economic factors like increased global electronics consumption and investments in new semiconductor fabrication plants further bolster market growth.

However, the market faces significant barriers and challenges. The high cost and complexity of developing and manufacturing novel photoinitiator chemistries represent a substantial barrier to entry. Stringent purity requirements for semiconductor-grade materials demand rigorous quality control, adding to production costs. Regulatory hurdles related to chemical safety and environmental impact can also influence product development and market access. Supply chain disruptions, particularly for key raw materials, can lead to price volatility and production delays. Competitive pressures from established players and the ongoing need for continuous innovation to keep pace with evolving lithography demands are persistent challenges.

Emerging Opportunities in Photoinitiator For Photoresist

Emerging opportunities in the photoinitiator for photoresist market lie in the expanding applications beyond traditional semiconductor manufacturing. The growing demand for advanced packaging techniques, which require high-resolution patterning for interconnects, presents a significant untapped market. Furthermore, the development of new photopolymer formulations for additive manufacturing (3D printing) in the electronics sector, requiring specialized photoinitiators for precise curing, offers substantial growth potential. The exploration of novel photoinitiator chemistries for bio-sensor fabrication and microfluidic devices also represents a promising avenue. As consumer preferences lean towards thinner, more flexible, and high-performance electronic devices, the demand for photoinitiators capable of enabling these new form factors will surge.

Growth Accelerators in the Photoinitiator For Photoresist Industry

Several factors are acting as significant growth accelerators for the photoinitiator for photoresist industry. The accelerated pace of technological innovation in semiconductor manufacturing, particularly the push towards smaller nodes using EUV lithography, is a primary driver. Strategic partnerships between photoinitiator manufacturers and photoresist formulators are crucial for co-developing optimized solutions. The increasing global investment in semiconductor fabrication facilities, both by established players and emerging economies, directly translates into higher demand for photoinitiators. Moreover, the trend towards vertical integration within the semiconductor supply chain can lead to greater collaboration and faster adoption of new photoinitiator technologies. The continuous improvement in the performance metrics of photoinitiators, such as increased quantum yield and reduced latency, also fuels market expansion.

Key Players Shaping the Photoinitiator For Photoresist Market

- Midori Kagaku

- FUJIFILM Wako Pure Chemical Corporation

- Toyo Gosei Co., Ltd

- Adeka

- IGM Resins B.V.

- Heraeus Epurio

- Miwon Commercial Co., Ltd.

- Daito Chemix Corporation

- CGP Materials

- ENF Technology

- NC Chem

- TAKOMA TECHNOLOGY CORPORATION

- Xuzhou B & C Chemical

- Changzhou Tronly New Electronic Materials

- Tianjin Jiuri New Material

- Suzhou Weimas

Notable Milestones in Photoinitiator For Photoresist Sector

- 2019: Introduction of next-generation PAGs optimized for high-NA EUV lithography, enabling improved resolution and process latitude.

- 2020: Significant advancements in low-outgassing photoinitiators for EUV resist development.

- 2021: Increased M&A activity as larger chemical companies acquire specialized photoinitiator producers to expand their semiconductor materials portfolio.

- 2022: Development of novel photoinitiator chemistries offering enhanced sensitivity for ArF immersion lithography, reducing exposure times.

- 2023: Emerging research into photoinitiators for advanced packaging applications, targeting high-density interconnects.

- 2024: Continued R&D focus on sustainable and environmentally friendly photoinitiator formulations.

In-Depth Photoinitiator For Photoresist Market Outlook

The future outlook for the photoinitiator for photoresist market is exceptionally promising, fueled by ongoing technological advancements and expanding applications. The relentless drive towards miniaturization in the semiconductor industry, particularly the widespread adoption of EUV lithography for advanced nodes, will continue to be a primary growth accelerator. Investments in new semiconductor fabrication plants globally will directly translate into sustained demand for high-performance photoinitiators. Emerging opportunities in advanced packaging and next-generation display technologies further diversify and expand the market. Strategic collaborations between photoinitiator suppliers and photoresist formulators will be crucial for innovation and rapid market penetration. The market is poised for significant growth, driven by a convergence of technological necessity and burgeoning end-market demand, offering substantial strategic opportunities for stakeholders.

Photoinitiator For Photoresist Segmentation

-

1. Application

- 1.1. EUV Photoresist

- 1.2. ArF Photoresist

- 1.3. KrF Photoresist

- 1.4. g/i-Line Photoresist

-

2. Type

- 2.1. Photo Acid Generator (PAG)

- 2.2. Photo Acid Compound (PAC)

Photoinitiator For Photoresist Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Photoinitiator For Photoresist Regional Market Share

Geographic Coverage of Photoinitiator For Photoresist

Photoinitiator For Photoresist REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. EUV Photoresist

- 5.1.2. ArF Photoresist

- 5.1.3. KrF Photoresist

- 5.1.4. g/i-Line Photoresist

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Photo Acid Generator (PAG)

- 5.2.2. Photo Acid Compound (PAC)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Photoinitiator For Photoresist Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. EUV Photoresist

- 6.1.2. ArF Photoresist

- 6.1.3. KrF Photoresist

- 6.1.4. g/i-Line Photoresist

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Photo Acid Generator (PAG)

- 6.2.2. Photo Acid Compound (PAC)

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Photoinitiator For Photoresist Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. EUV Photoresist

- 7.1.2. ArF Photoresist

- 7.1.3. KrF Photoresist

- 7.1.4. g/i-Line Photoresist

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Photo Acid Generator (PAG)

- 7.2.2. Photo Acid Compound (PAC)

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Photoinitiator For Photoresist Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. EUV Photoresist

- 8.1.2. ArF Photoresist

- 8.1.3. KrF Photoresist

- 8.1.4. g/i-Line Photoresist

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Photo Acid Generator (PAG)

- 8.2.2. Photo Acid Compound (PAC)

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Photoinitiator For Photoresist Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. EUV Photoresist

- 9.1.2. ArF Photoresist

- 9.1.3. KrF Photoresist

- 9.1.4. g/i-Line Photoresist

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Photo Acid Generator (PAG)

- 9.2.2. Photo Acid Compound (PAC)

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Photoinitiator For Photoresist Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. EUV Photoresist

- 10.1.2. ArF Photoresist

- 10.1.3. KrF Photoresist

- 10.1.4. g/i-Line Photoresist

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Photo Acid Generator (PAG)

- 10.2.2. Photo Acid Compound (PAC)

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Photoinitiator For Photoresist Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. EUV Photoresist

- 11.1.2. ArF Photoresist

- 11.1.3. KrF Photoresist

- 11.1.4. g/i-Line Photoresist

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Photo Acid Generator (PAG)

- 11.2.2. Photo Acid Compound (PAC)

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Midori Kagaku

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 FUJIFILM Wako Pure Chemical Corporation

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Toyo Gosei Co. Ltd

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Adeka

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 IGM Resins B.V.

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Heraeus Epurio

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Miwon Commercial Co. Ltd.

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Daito Chemix Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 CGP Materials

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 ENF Technology

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 NC Chem

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 TAKOMA TECHNOLOGY CORPORATION

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Xuzhou B & C Chemical

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Changzhou Tronly New Electronic Materials

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Tianjin Jiuri New Material

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Suzhou Weimas

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.1 Midori Kagaku

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Photoinitiator For Photoresist Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Photoinitiator For Photoresist Revenue (million), by Application 2025 & 2033

- Figure 3: North America Photoinitiator For Photoresist Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Photoinitiator For Photoresist Revenue (million), by Type 2025 & 2033

- Figure 5: North America Photoinitiator For Photoresist Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Photoinitiator For Photoresist Revenue (million), by Country 2025 & 2033

- Figure 7: North America Photoinitiator For Photoresist Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Photoinitiator For Photoresist Revenue (million), by Application 2025 & 2033

- Figure 9: South America Photoinitiator For Photoresist Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Photoinitiator For Photoresist Revenue (million), by Type 2025 & 2033

- Figure 11: South America Photoinitiator For Photoresist Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Photoinitiator For Photoresist Revenue (million), by Country 2025 & 2033

- Figure 13: South America Photoinitiator For Photoresist Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Photoinitiator For Photoresist Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Photoinitiator For Photoresist Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Photoinitiator For Photoresist Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Photoinitiator For Photoresist Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Photoinitiator For Photoresist Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Photoinitiator For Photoresist Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Photoinitiator For Photoresist Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Photoinitiator For Photoresist Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Photoinitiator For Photoresist Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Photoinitiator For Photoresist Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Photoinitiator For Photoresist Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Photoinitiator For Photoresist Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Photoinitiator For Photoresist Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Photoinitiator For Photoresist Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Photoinitiator For Photoresist Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Photoinitiator For Photoresist Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Photoinitiator For Photoresist Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Photoinitiator For Photoresist Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Photoinitiator For Photoresist Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Photoinitiator For Photoresist Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Photoinitiator For Photoresist Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Photoinitiator For Photoresist Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Photoinitiator For Photoresist Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Photoinitiator For Photoresist Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Photoinitiator For Photoresist Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Photoinitiator For Photoresist Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Photoinitiator For Photoresist Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Photoinitiator For Photoresist Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Photoinitiator For Photoresist Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Photoinitiator For Photoresist Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Photoinitiator For Photoresist Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Photoinitiator For Photoresist Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Photoinitiator For Photoresist Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Photoinitiator For Photoresist Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Photoinitiator For Photoresist Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Photoinitiator For Photoresist Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Photoinitiator For Photoresist Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Photoinitiator For Photoresist?

The projected CAGR is approximately 5.8%.

2. Which companies are prominent players in the Photoinitiator For Photoresist?

Key companies in the market include Midori Kagaku, FUJIFILM Wako Pure Chemical Corporation, Toyo Gosei Co., Ltd, Adeka, IGM Resins B.V., Heraeus Epurio, Miwon Commercial Co., Ltd., Daito Chemix Corporation, CGP Materials, ENF Technology, NC Chem, TAKOMA TECHNOLOGY CORPORATION, Xuzhou B & C Chemical, Changzhou Tronly New Electronic Materials, Tianjin Jiuri New Material, Suzhou Weimas.

3. What are the main segments of the Photoinitiator For Photoresist?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 212 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Photoinitiator For Photoresist," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Photoinitiator For Photoresist report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Photoinitiator For Photoresist?

To stay informed about further developments, trends, and reports in the Photoinitiator For Photoresist, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence