Key Insights

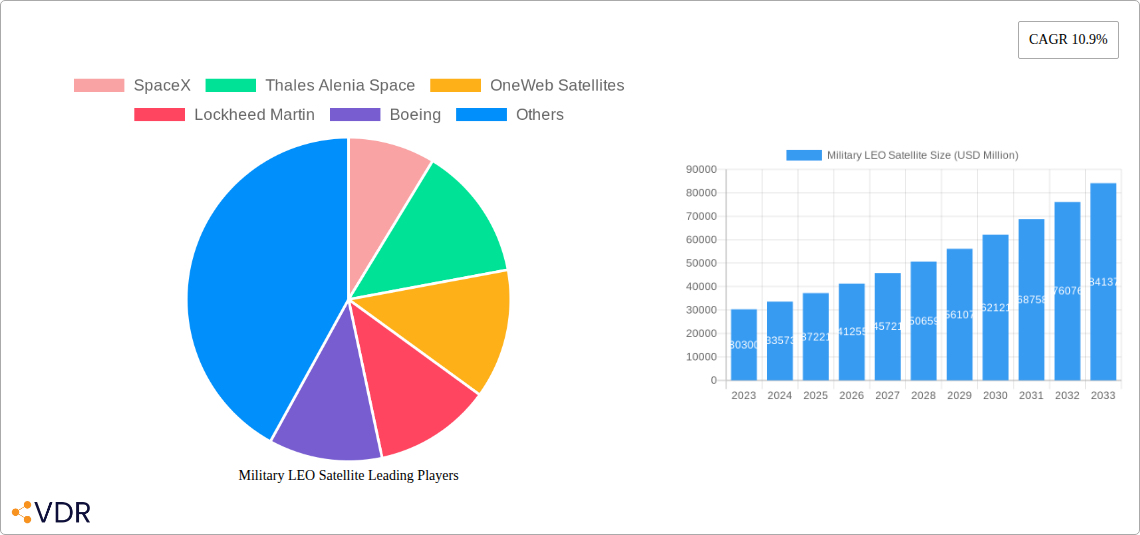

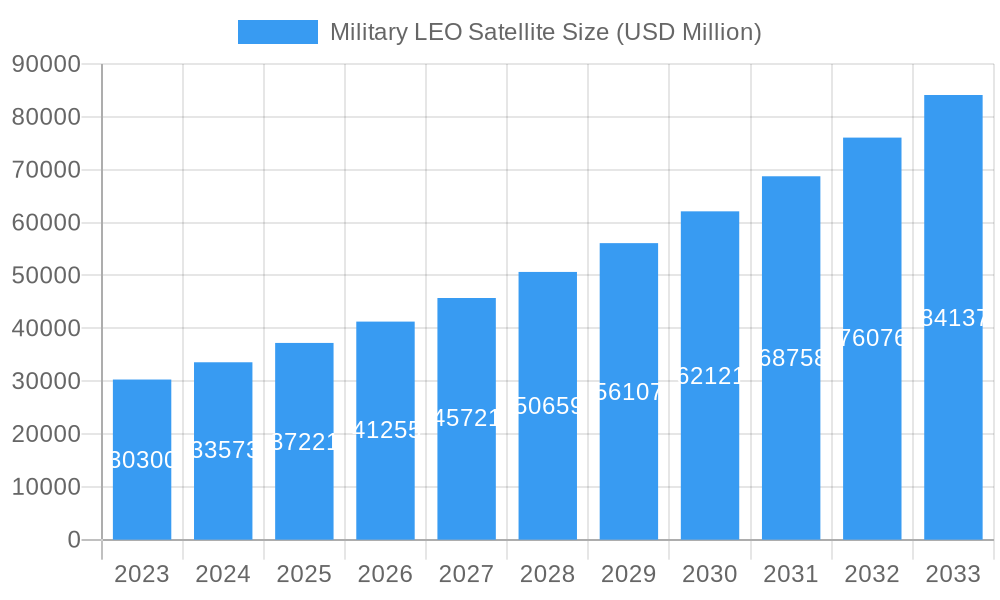

The Military LEO Satellite market is experiencing robust expansion, projected to reach an impressive $30.3 billion by 2023, with a compelling Compound Annual Growth Rate (CAGR) of 10.9% throughout the forecast period. This significant growth is primarily propelled by the escalating demand for enhanced global communication capabilities, advanced reconnaissance and navigation systems, and increasingly sophisticated weather monitoring for military operations. The strategic advantages offered by Low Earth Orbit (LEO) satellites, including lower latency and higher bandwidth compared to traditional geostationary satellites, are making them indispensable for modern defense forces. Furthermore, the increasing deployment of constellations of small satellites is democratizing access to space-based assets, fostering innovation and driving down costs, which further fuels market expansion.

Military LEO Satellite Market Size (In Billion)

The market is characterized by a dynamic interplay of several key drivers and trends. The growing geopolitical tensions and the need for real-time intelligence, surveillance, and reconnaissance (ISR) are paramount drivers. Advancements in miniaturization, propulsion systems, and payload technologies are enabling the development of more capable and cost-effective LEO satellites. Key applications such as secure military communications, precision navigation and timing (PNT), and tactical data links are seeing substantial investment. The market segments are broadly categorized by satellite weight, with satellites below 50 Kg and those between 50-500 Kg exhibiting particularly strong growth potential due to the rise of small satellite constellations. Major industry players like SpaceX, Lockheed Martin, and Northrop Grumman are heavily investing in LEO satellite technology, pushing the boundaries of what's possible and shaping the future of defense in space.

Military LEO Satellite Company Market Share

This comprehensive report delves into the dynamic Military LEO Satellite Market, analyzing its structure, growth trajectory, and future outlook from 2019 to 2033. We provide in-depth insights into key market segments, technological advancements, and the competitive landscape, empowering stakeholders with actionable intelligence. The report covers both the parent market and its critical child markets, offering a holistic view of opportunities within this evolving domain.

Military LEO Satellite Market Dynamics & Structure

The Military LEO Satellite market exhibits a moderately consolidated structure, with a few dominant players like Lockheed Martin, Boeing, and Northrop Grumman holding significant market share. However, the emergence of agile companies such as SpaceX and OneWeb Satellites is injecting dynamism and driving innovation, particularly in the constellation deployment and cost reduction aspects. Technological innovation, fueled by advancements in miniaturization, propulsion systems, and advanced sensor technology, remains a primary driver. Regulatory frameworks, driven by national security interests and international treaties, also play a crucial role in market access and operational deployment. Competitive product substitutes, while limited in the dedicated military LEO domain, can emerge from advancements in terrestrial communication and airborne platforms. End-user demographics are primarily national defense agencies and allied military forces. Mergers and acquisitions (M&A) trends are observed as larger players seek to acquire specialized capabilities or expand their LEO constellations.

- Market Concentration: Moderate, with leading primes and emerging disruptors.

- Technological Innovation: Driven by miniaturization, AI integration, and advanced sensor payloads.

- Regulatory Frameworks: National security priorities and international space law are key influences.

- Competitive Substitutes: Emerging as integrated terrestrial and airborne solutions advance.

- End-User Demographics: Primarily government defense entities.

- M&A Trends: Focus on capability acquisition and constellation expansion.

Military LEO Satellite Growth Trends & Insights

The Military LEO Satellite market is poised for robust growth, projected to expand significantly from its 2025 base year value of $XX billion to $XX billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of XX% during the forecast period (2025-2033). This expansion is underpinned by escalating geopolitical tensions, the increasing need for secure and resilient communication networks, and the growing demand for persistent surveillance and reconnaissance capabilities. Adoption rates of LEO satellite constellations for military applications are accelerating as defense agencies recognize the strategic advantages offered by lower latency and higher bandwidth compared to traditional GEO satellites. Technological disruptions, including the development of proliferated LEO (P-LEO) architectures, the integration of artificial intelligence for data processing and autonomous operations, and advancements in on-orbit servicing and refueling, are fundamentally reshaping the market. Consumer behavior shifts, though distinct from commercial markets, are evident in defense procurement strategies, favoring more agile, adaptable, and cost-effective solutions. The historical period (2019-2024) has seen significant investment in foundational LEO technologies and initial constellation planning, laying the groundwork for the accelerated growth anticipated in the coming years. The market penetration of LEO satellites for military use is expected to increase substantially as operational deployments become more widespread and cost-efficiencies of LEO constellations become more pronounced for various defense applications.

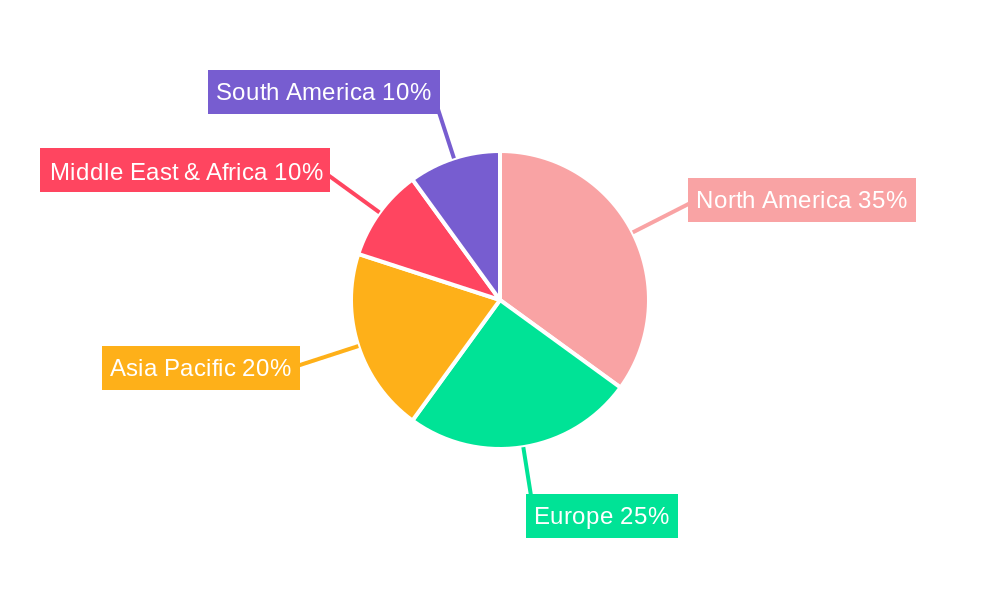

Dominant Regions, Countries, or Segments in Military LEO Satellite

The Application segment of Military Communications is a dominant growth driver within the Military LEO Satellite market, projected to hold a substantial market share throughout the forecast period (2025-2033). This dominance is propelled by the ever-increasing demand for secure, real-time, and high-bandwidth communication channels for deployed forces, enabling seamless command and control, intelligence sharing, and operational coordination across vast distances. The United States stands out as the leading country driving market growth, owing to its significant defense spending, ongoing modernization efforts, and proactive investment in advanced space-based capabilities, including LEO constellations. Key drivers in the US include robust government initiatives, a well-established defense industrial base, and the critical need to maintain global situational awareness and communication superiority.

- Dominant Application Segment: Military Communications, driven by the imperative for secure, low-latency global connectivity for dispersed forces.

- Leading Country: United States, characterized by substantial defense budgets, advanced technological development, and a strong strategic focus on space-based assets.

- Key Drivers in the US:

- Economic Policies: Ample defense funding and incentives for private sector innovation.

- Infrastructure Development: Extensive ground station networks and secure communication backbones.

- Technological Advancements: Leading edge in satellite design, manufacturing, and launch capabilities.

- Strategic Imperatives: Maintaining global command and control, enhanced ISR capabilities, and resilient communication networks.

- Dominance Factors: The US government's consistent investment in space programs, its leadership in satellite technology, and its strategic requirement for pervasive communication and intelligence, surveillance, and reconnaissance (ISR) capabilities directly contribute to the dominance of Military Communications applications and the United States as a leading market. The Above 500 Kg satellite type is also expected to see significant growth within this segment, catering to the sophisticated payload requirements of advanced military systems.

Military LEO Satellite Product Landscape

The product landscape of Military LEO Satellites is characterized by increasing sophistication and specialization. Innovations are focused on enhancing payload capabilities, improving satellite resilience, and reducing operational costs. This includes the development of multi-band communication systems, advanced electro-optical and radar imaging payloads for reconnaissance and surveillance, and precise navigation payloads. The trend towards miniaturization allows for the deployment of larger constellations with diverse functionalities, while larger satellites (Above 500 Kg) are being developed for more demanding missions requiring substantial power and complex sensor suites. LeoStella is notable for its rapid satellite manufacturing capabilities, enabling faster deployment of constellations. Thales Alenia Space contributes advanced payload integration and satellite bus technologies, enhancing performance and reliability. SpaceX's Starshield initiative focuses on adapting its Starlink constellation for secure government and military use, offering a blend of global coverage and rapid deployment.

Key Drivers, Barriers & Challenges in Military LEO Satellite

Key Drivers:

- Escalating Geopolitical Tensions: Increased demand for real-time intelligence, surveillance, reconnaissance (ISR), and secure communications to maintain strategic advantage.

- Technological Advancements: Miniaturization of satellites, development of advanced sensor payloads, and the evolution of AI for data processing are enabling more capable and cost-effective LEO solutions.

- Need for Resilient Communication: The inherent redundancy and lower latency of LEO constellations offer a more robust communication alternative to traditional systems.

- Cost-Effectiveness: LEO constellations, particularly proliferated LEO, offer a more economically viable approach for widespread coverage compared to GEO satellites for certain applications.

Barriers & Challenges:

- Space Debris and Congestion: The increasing number of satellites poses a significant risk of collisions, necessitating stringent debris mitigation strategies.

- Regulatory Hurdles and Spectrum Allocation: Obtaining the necessary licenses and ensuring interference-free operation in congested radio frequency spectrum can be complex.

- Cybersecurity Threats: Protecting sensitive military data transmitted and processed by LEO satellites from cyberattacks is paramount.

- High Initial Investment and Long Development Cycles: While individual LEO satellites can be more affordable, building and launching large constellations require substantial upfront capital and lengthy development timelines.

- Supply Chain Vulnerabilities: Reliance on specialized components and manufacturing processes can create potential bottlenecks.

- Competitive Pressures: The rapid pace of innovation and the emergence of new players create intense competition, demanding continuous adaptation and investment.

Emerging Opportunities in Military LEO Satellite

Emerging opportunities in the Military LEO Satellite market lie in the development of highly integrated, multi-functional constellations capable of delivering a wide array of services from a single platform. This includes advanced electronic warfare capabilities, resilient satellite-based internet of things (IoT) for battlefield logistics, and highly secure quantum communication payloads. The increasing focus on "space as a service" models, where militaries can subscribe to specific functionalities rather than owning entire systems, presents a significant growth avenue. Furthermore, the expansion of LEO capabilities to support allied nations and international coalition operations offers untapped market potential. The development of on-orbit servicing, assembly, and manufacturing (OSAM) capabilities for military satellites in LEO will also unlock new operational paradigms and extend satellite lifespans.

Growth Accelerators in the Military LEO Satellite Industry

Growth accelerators in the Military LEO Satellite industry are primarily driven by continuous technological breakthroughs in satellite design, propulsion, and payload technology, enabling enhanced capabilities and reduced costs. Strategic partnerships between established defense contractors and innovative NewSpace companies, such as potential collaborations between Lockheed Martin and OneWeb Satellites or SpaceX and defense agencies, are fostering rapid development and deployment. Market expansion strategies are focusing on offering tailored LEO solutions for specific military domains, including tactical communications, intelligence gathering, and missile defense early warning systems. The increasing adoption of modular and scalable satellite architectures, allowing for rapid constellation expansion and upgrades, also acts as a significant growth catalyst, ensuring that military forces can adapt to evolving threats and operational requirements.

Key Players Shaping the Military LEO Satellite Market

- SpaceX

- Thales Alenia Space

- OneWeb Satellites

- Lockheed Martin

- Boeing

- Northrop Grumman

- Iridium Communications

- LeoStella

Notable Milestones in Military LEO Satellite Sector

- 2019: SpaceX successfully launches its first batch of Starlink satellites, demonstrating the viability of large LEO constellations.

- 2020: Lockheed Martin announces its collaboration with Omnispace to develop LEO-based mobile satellite services for government and commercial users.

- 2021: Northrop Grumman expands its space portfolio with the acquisition of several smaller aerospace companies, strengthening its LEO capabilities.

- 2022: OneWeb Satellites secures significant government contracts for its LEO constellation, highlighting its growing importance in the defense sector.

- 2023 (Early): Thales Alenia Space announces advancements in its flexible LEO satellite bus designs, enabling rapid customization for military payloads.

- 2023 (Mid): LeoStella delivers its first batch of custom-built satellites for a major defense contractor, showcasing its rapid manufacturing prowess.

- 2024 (Ongoing): Iridium Communications continues to upgrade its LEO constellation, enhancing its secure voice and data services for government applications.

In-Depth Military LEO Satellite Market Outlook

The Military LEO Satellite market is projected for substantial and sustained growth, driven by the undeniable strategic imperative for advanced, resilient, and globally accessible space-based capabilities. The continued evolution of proliferated LEO constellations, offering unprecedented connectivity and data processing power, will be a key catalyst. Opportunities abound for companies that can provide secure, cost-effective, and rapidly deployable solutions tailored to the specific needs of defense agencies. Strategic partnerships and continuous innovation in areas such as AI-driven analytics, quantum communications, and on-orbit servicing will further accelerate this expansion, solidifying LEO satellites' indispensable role in modern military operations and national security.

Military LEO Satellite Segmentation

-

1. Application

- 1.1. Military Communications

- 1.2. Reconnaissance and Navigation

- 1.3. Weather Monitoring

- 1.4. Others

-

2. Types

- 2.1. Below 50 Kg

- 2.2. 50-500 Kg

- 2.3. Above 500 Kg

Military LEO Satellite Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Military LEO Satellite Regional Market Share

Geographic Coverage of Military LEO Satellite

Military LEO Satellite REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Military Communications

- 5.1.2. Reconnaissance and Navigation

- 5.1.3. Weather Monitoring

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Below 50 Kg

- 5.2.2. 50-500 Kg

- 5.2.3. Above 500 Kg

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Military LEO Satellite Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Military Communications

- 6.1.2. Reconnaissance and Navigation

- 6.1.3. Weather Monitoring

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Below 50 Kg

- 6.2.2. 50-500 Kg

- 6.2.3. Above 500 Kg

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Military LEO Satellite Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Military Communications

- 7.1.2. Reconnaissance and Navigation

- 7.1.3. Weather Monitoring

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Below 50 Kg

- 7.2.2. 50-500 Kg

- 7.2.3. Above 500 Kg

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Military LEO Satellite Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Military Communications

- 8.1.2. Reconnaissance and Navigation

- 8.1.3. Weather Monitoring

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Below 50 Kg

- 8.2.2. 50-500 Kg

- 8.2.3. Above 500 Kg

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Military LEO Satellite Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Military Communications

- 9.1.2. Reconnaissance and Navigation

- 9.1.3. Weather Monitoring

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Below 50 Kg

- 9.2.2. 50-500 Kg

- 9.2.3. Above 500 Kg

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Military LEO Satellite Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Military Communications

- 10.1.2. Reconnaissance and Navigation

- 10.1.3. Weather Monitoring

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Below 50 Kg

- 10.2.2. 50-500 Kg

- 10.2.3. Above 500 Kg

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Military LEO Satellite Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Military Communications

- 11.1.2. Reconnaissance and Navigation

- 11.1.3. Weather Monitoring

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Below 50 Kg

- 11.2.2. 50-500 Kg

- 11.2.3. Above 500 Kg

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 SpaceX

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Thales Alenia Space

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 OneWeb Satellites

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Lockheed Martin

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Boeing

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Northrop Grumman

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Iridium Communications

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 LeoStella

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.1 SpaceX

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Military LEO Satellite Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Military LEO Satellite Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Military LEO Satellite Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Military LEO Satellite Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Military LEO Satellite Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Military LEO Satellite Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Military LEO Satellite Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Military LEO Satellite Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Military LEO Satellite Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Military LEO Satellite Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Military LEO Satellite Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Military LEO Satellite Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Military LEO Satellite Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Military LEO Satellite Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Military LEO Satellite Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Military LEO Satellite Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Military LEO Satellite Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Military LEO Satellite Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Military LEO Satellite Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Military LEO Satellite Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Military LEO Satellite Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Military LEO Satellite Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Military LEO Satellite Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Military LEO Satellite Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Military LEO Satellite Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Military LEO Satellite Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Military LEO Satellite Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Military LEO Satellite Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Military LEO Satellite Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Military LEO Satellite Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Military LEO Satellite Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Military LEO Satellite Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Military LEO Satellite Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Military LEO Satellite Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Military LEO Satellite Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Military LEO Satellite Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Military LEO Satellite Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Military LEO Satellite Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Military LEO Satellite Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Military LEO Satellite Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Military LEO Satellite Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Military LEO Satellite Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Military LEO Satellite Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Military LEO Satellite Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Military LEO Satellite Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Military LEO Satellite Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Military LEO Satellite Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Military LEO Satellite Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Military LEO Satellite Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Military LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Military LEO Satellite?

The projected CAGR is approximately 10.9%.

2. Which companies are prominent players in the Military LEO Satellite?

Key companies in the market include SpaceX, Thales Alenia Space, OneWeb Satellites, Lockheed Martin, Boeing, Northrop Grumman, Iridium Communications, LeoStella.

3. What are the main segments of the Military LEO Satellite?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Military LEO Satellite," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Military LEO Satellite report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Military LEO Satellite?

To stay informed about further developments, trends, and reports in the Military LEO Satellite, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence