Key Insights

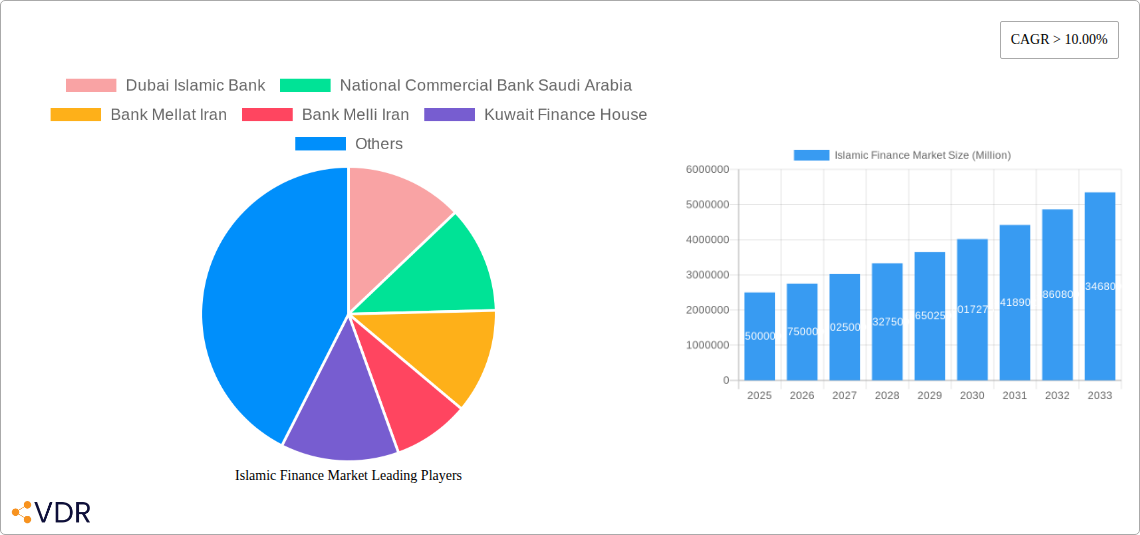

The Islamic finance market, exhibiting a Compound Annual Growth Rate (CAGR) exceeding 10% from 2019 to 2024, is poised for substantial expansion. This robust growth is fueled by several key drivers. The increasing global Muslim population, coupled with rising awareness and acceptance of Sharia-compliant financial products and services, are significant factors. Furthermore, supportive government regulations in many Islamic finance hubs like the Gulf Cooperation Council (GCC) countries and Southeast Asia are fostering a conducive environment for market expansion. Technological advancements, particularly in fintech, are also streamlining processes and making Islamic finance more accessible to a wider range of individuals and businesses. However, challenges remain. The relatively nascent stage of development in certain regions, coupled with a need for greater standardization and transparency of Sharia-compliant products, are potential restraints. The market segmentation includes various financial services, such as Islamic banking, Takaful (Islamic insurance), and Sukuk (Islamic bonds), each contributing uniquely to the overall growth. Key players such as Dubai Islamic Bank, National Commercial Bank Saudi Arabia, and several prominent Iranian and Malaysian banks are leading the industry, continuously innovating to meet the evolving demands of the market.

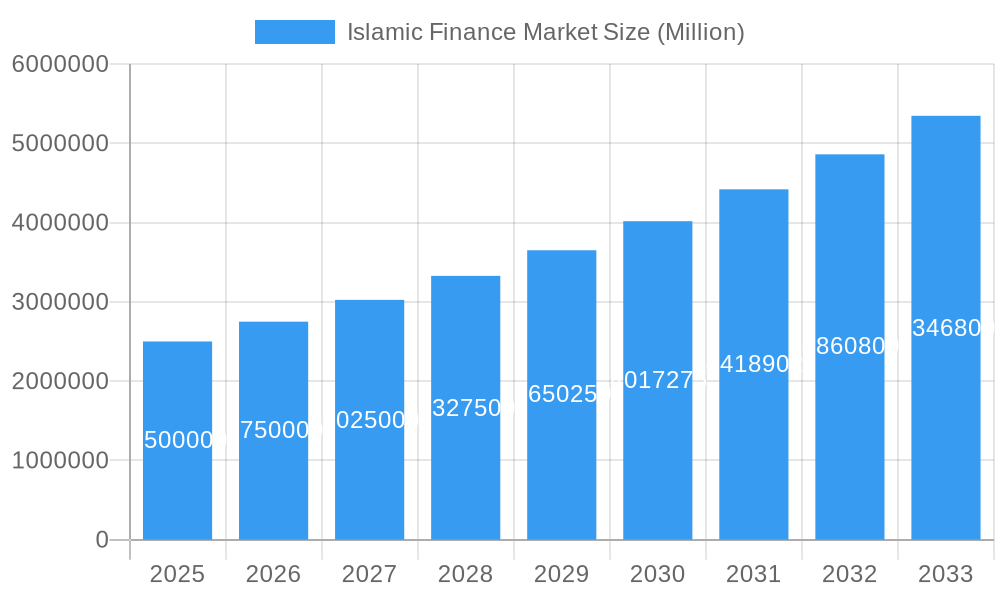

Islamic Finance Market Market Size (In Million)

The forecast period (2025-2033) projects continued expansion for the Islamic finance sector. Building upon the strong CAGR of the past years, conservative projections suggest a market size exceeding $5 trillion by 2033. This growth will be regionally diverse, with some areas experiencing more rapid expansion based on regulatory support, economic growth, and the density of the Muslim population. The focus on sustainable and ethical investments is also expected to contribute to future growth, positioning Islamic finance as a key driver of responsible finance globally. To maintain this growth trajectory, the industry will need to focus on overcoming the aforementioned restraints, emphasizing greater investor education, and enhancing the integration of technological advancements. This will facilitate greater participation from both established financial institutions and innovative fintech companies, leading to a more inclusive and efficient Islamic finance ecosystem.

Islamic Finance Market Company Market Share

Islamic Finance Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Islamic finance market, covering its dynamics, growth trends, dominant players, and future outlook. With a study period spanning 2019-2033, a base year of 2025, and an estimated year of 2025, this report offers invaluable insights for industry professionals, investors, and researchers. The report segments the market into various categories, including but not limited to, Islamic banking, Takaful (Islamic insurance), and Sukuk (Islamic bonds). The parent market is the broader global financial market, while child markets include specific Islamic financial products and services.

Islamic Finance Market Dynamics & Structure

The Islamic finance market is characterized by a moderate level of concentration, with a few major players holding significant market share. However, the market is also witnessing increased competition from new entrants and the expansion of existing players. Technological innovation, particularly in fintech, is a key driver, enabling the development of more efficient and accessible Islamic financial products and services. Regulatory frameworks play a crucial role in shaping market growth, with varying levels of supportive policies across different jurisdictions. While Islamic finance offers unique solutions, it also faces competition from conventional financial products. The end-user demographic is predominantly Muslim populations globally, with increasing adoption in non-Muslim countries as well. M&A activity is moderate, with notable deals reshaping market dynamics. In 2024, the estimated value of M&A deals was xx Million.

- Market Concentration: Moderately concentrated, with top 10 players holding approximately xx% market share (2024).

- Technological Innovation: Fintech driving efficiency, accessibility, and new product development.

- Regulatory Frameworks: Varying levels of support across jurisdictions, influencing market growth.

- Competitive Substitutes: Conventional financial products remain a competitive force.

- End-User Demographics: Primarily Muslim populations, expanding into non-Muslim markets.

- M&A Trends: Moderate activity, with significant deals influencing market landscape (xx deals in 2024).

Islamic Finance Market Growth Trends & Insights

The Islamic finance market exhibits robust growth, fueled by factors like rising Muslim populations, increasing awareness of Islamic principles, and supportive government initiatives. The market size is projected to expand significantly over the forecast period (2025-2033), driven by an increasing adoption rate of Islamic financial products and services. Technological advancements are transforming consumer behavior, leading to greater demand for digital Islamic banking and finance solutions. The Compound Annual Growth Rate (CAGR) for the period 2025-2033 is estimated at xx%, with market penetration expected to increase from xx% in 2025 to xx% by 2033. XXX (Source needed to replace XXX) will be leveraged for in-depth insights, particularly concerning regional variations and product-specific growth patterns.

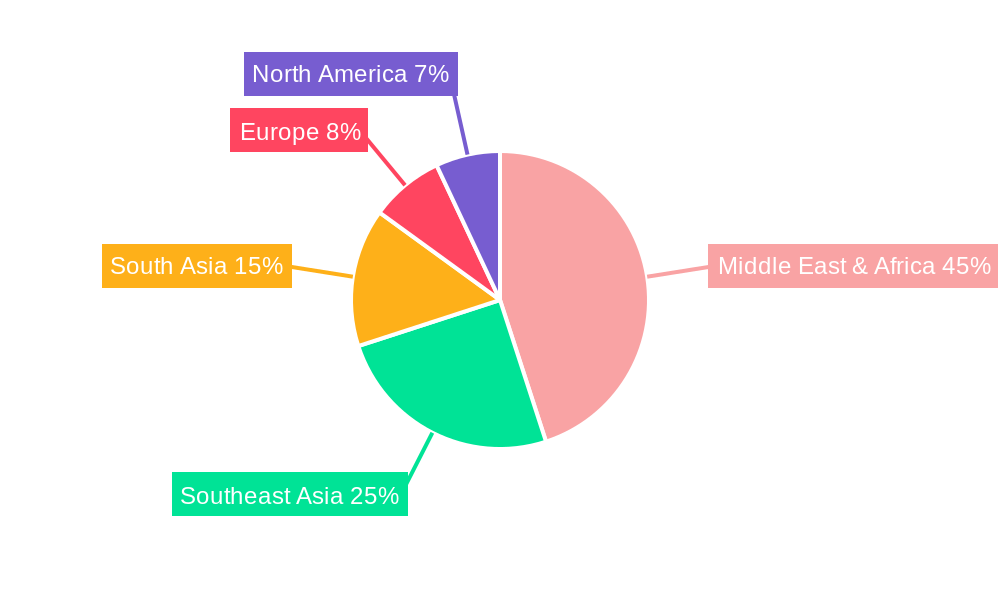

Dominant Regions, Countries, or Segments in Islamic Finance Market

The Gulf Cooperation Council (GCC) countries, particularly Saudi Arabia and the UAE, are currently the dominant regions in the Islamic finance market. This dominance is attributed to several key factors: supportive government policies, robust infrastructure, and significant investments in the sector. Other regions, such as Southeast Asia and parts of Africa, are also exhibiting strong growth potential, driven by expanding Muslim populations and increasing demand for Sharia-compliant financial products. However, regulatory frameworks and infrastructure still present challenges for expansion in some areas.

- Key Drivers:

- Supportive government policies and regulations (e.g., Saudi Vision 2030).

- Strong economic growth in major regions.

- Well-developed infrastructure in leading markets.

- Increasing awareness and adoption of Islamic finance principles.

- Dominance Factors:

- High concentration of Islamic financial institutions.

- Large Muslim populations and high disposable incomes.

- Government initiatives to promote Islamic finance.

- Significant investment in financial infrastructure.

Islamic Finance Market Product Landscape

The Islamic finance product landscape is diverse, ranging from Islamic banking services (including Murabaha, Ijarah, and Mudarabah financing) to Takaful insurance and Sukuk bonds. Recent innovations include the development of Islamic fintech solutions, offering greater convenience and accessibility. These solutions leverage technologies like blockchain and AI to streamline processes and enhance security. The focus is on enhancing transparency, ethical compliance, and meeting the evolving needs of a digitally-savvy customer base. Performance metrics such as return on investment (ROI) for Sukuk issuances and customer satisfaction scores for Islamic banking services are key indicators of product success.

Key Drivers, Barriers & Challenges in Islamic Finance Market

Key Drivers:

- Rising Muslim population globally.

- Increasing demand for ethically compliant financial products.

- Government initiatives promoting Islamic finance.

- Technological advancements improving efficiency and accessibility.

Challenges & Restraints:

- Regulatory complexities and varying standards across jurisdictions.

- Lack of awareness and understanding of Islamic finance principles in some regions.

- Competition from conventional financial products.

- Dependence on oil prices in some key markets. (Quantifiable impact: xx% fluctuation in oil prices can lead to a xx% change in market growth).

Emerging Opportunities in Islamic Finance Market

- Untapped markets in Sub-Saharan Africa and South Asia.

- Growth of green finance initiatives within the Islamic finance sector.

- Increasing demand for innovative digital solutions (e.g., Islamic robo-advisors).

- Expansion of Takaful insurance products to cater to evolving needs.

Growth Accelerators in the Islamic Finance Market Industry

Strategic partnerships between Islamic and conventional financial institutions are fostering innovation and market expansion. Technological breakthroughs, particularly in fintech, are streamlining operations and enhancing customer experience. Governments are actively promoting the sector through supportive policies and initiatives. These collaborative efforts are expected to accelerate the long-term growth trajectory of the Islamic finance market.

Key Players Shaping the Islamic Finance Market Market

- Dubai Islamic Bank

- National Commercial Bank Saudi Arabia

- Bank Mellat Iran

- Bank Melli Iran

- Kuwait Finance House

- Bank Maskan Iran

- Qatar Islamic Bank

- Abu Dhabi Islamic Bank

- May Bank Islamic

- CIMB Islamic Bank

Notable Milestones in Islamic Finance Market Sector

- January 2023: Abu Dhabi Islamic Bank (ADIB) increased its ownership in ADIB Egypt to over 52%, acquiring 9.6 million shares from the National Investment Bank (NIB).

- July 2022: Kuwait Finance House (KFH) agreed to acquire Ahli United Bank (AUB) through a share swap deal, creating a major player in the Gulf region.

In-Depth Islamic Finance Market Market Outlook

The Islamic finance market is poised for sustained growth, driven by the factors outlined above. Strategic opportunities exist in leveraging technological advancements, expanding into new markets, and developing innovative products catering to diverse customer segments. The long-term outlook is positive, with significant potential for market expansion and increased diversification.

Islamic Finance Market Segmentation

-

1. Financial Sector

- 1.1. Islamic Banking

- 1.2. Islamic Insurance : Takaful

- 1.3. Islamic Bonds 'Sukuk'

- 1.4. Other Islamic Financial Institution (OIFI's)

- 1.5. Islamic Funds

Islamic Finance Market Segmentation By Geography

-

1. GCC

- 1.1. Saudi Arabia

- 1.2. UAE

- 1.3. Qatar

- 1.4. Kuwait

- 1.5. Bahrain

- 1.6. Oman

-

2. MENA

- 2.1. Iran

- 2.2. Egypt

- 2.3. Rest of Middle East

- 3. Southeast Asia

-

4. Malaysia

- 4.1. Indonesia

- 4.2. Brunei

- 4.3. Pakistan

- 4.4. Rest of Southeast Asia and Asia Pacific

-

5. Europe

- 5.1. United Kingdom

- 5.2. Ieland

- 5.3. Italy

- 5.4. Rest of Europe

- 6. Rest of the World

Islamic Finance Market Regional Market Share

Geographic Coverage of Islamic Finance Market

Islamic Finance Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Financial Sector

- 5.1.1. Islamic Banking

- 5.1.2. Islamic Insurance : Takaful

- 5.1.3. Islamic Bonds 'Sukuk'

- 5.1.4. Other Islamic Financial Institution (OIFI's)

- 5.1.5. Islamic Funds

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. GCC

- 5.2.2. MENA

- 5.2.3. Southeast Asia

- 5.2.4. Malaysia

- 5.2.5. Europe

- 5.2.6. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Financial Sector

- 6. Islamic Finance Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Financial Sector

- 6.1.1. Islamic Banking

- 6.1.2. Islamic Insurance : Takaful

- 6.1.3. Islamic Bonds 'Sukuk'

- 6.1.4. Other Islamic Financial Institution (OIFI's)

- 6.1.5. Islamic Funds

- 6.1. Market Analysis, Insights and Forecast - by Financial Sector

- 7. GCC Islamic Finance Market Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Financial Sector

- 7.1.1. Islamic Banking

- 7.1.2. Islamic Insurance : Takaful

- 7.1.3. Islamic Bonds 'Sukuk'

- 7.1.4. Other Islamic Financial Institution (OIFI's)

- 7.1.5. Islamic Funds

- 7.1. Market Analysis, Insights and Forecast - by Financial Sector

- 8. MENA Islamic Finance Market Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Financial Sector

- 8.1.1. Islamic Banking

- 8.1.2. Islamic Insurance : Takaful

- 8.1.3. Islamic Bonds 'Sukuk'

- 8.1.4. Other Islamic Financial Institution (OIFI's)

- 8.1.5. Islamic Funds

- 8.1. Market Analysis, Insights and Forecast - by Financial Sector

- 9. Southeast Asia Islamic Finance Market Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Financial Sector

- 9.1.1. Islamic Banking

- 9.1.2. Islamic Insurance : Takaful

- 9.1.3. Islamic Bonds 'Sukuk'

- 9.1.4. Other Islamic Financial Institution (OIFI's)

- 9.1.5. Islamic Funds

- 9.1. Market Analysis, Insights and Forecast - by Financial Sector

- 10. Malaysia Islamic Finance Market Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Financial Sector

- 10.1.1. Islamic Banking

- 10.1.2. Islamic Insurance : Takaful

- 10.1.3. Islamic Bonds 'Sukuk'

- 10.1.4. Other Islamic Financial Institution (OIFI's)

- 10.1.5. Islamic Funds

- 10.1. Market Analysis, Insights and Forecast - by Financial Sector

- 11. Europe Islamic Finance Market Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Financial Sector

- 11.1.1. Islamic Banking

- 11.1.2. Islamic Insurance : Takaful

- 11.1.3. Islamic Bonds 'Sukuk'

- 11.1.4. Other Islamic Financial Institution (OIFI's)

- 11.1.5. Islamic Funds

- 11.1. Market Analysis, Insights and Forecast - by Financial Sector

- 12. Rest of the World Islamic Finance Market Analysis, Insights and Forecast, 2021-2033

- 12.1. Market Analysis, Insights and Forecast - by Financial Sector

- 12.1.1. Islamic Banking

- 12.1.2. Islamic Insurance : Takaful

- 12.1.3. Islamic Bonds 'Sukuk'

- 12.1.4. Other Islamic Financial Institution (OIFI's)

- 12.1.5. Islamic Funds

- 12.1. Market Analysis, Insights and Forecast - by Financial Sector

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Dubai Islamic Bank

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 National Commercial Bank Saudi Arabia

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Bank Mellat Iran

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Bank Melli Iran

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Kuwait Finance House

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Bank Maskan Iran

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Qatar Islamic Bank

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Abu Dhabi Islamic Bank

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 May Bank Islamic

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 CIMB Islamic Bank**List Not Exhaustive

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.1 Dubai Islamic Bank

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Islamic Finance Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Islamic Finance Market Share (%) by Company 2025

List of Tables

- Table 1: Islamic Finance Market Revenue billion Forecast, by Financial Sector 2020 & 2033

- Table 2: Islamic Finance Market Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Islamic Finance Market Revenue billion Forecast, by Financial Sector 2020 & 2033

- Table 4: Islamic Finance Market Revenue billion Forecast, by Country 2020 & 2033

- Table 5: Saudi Arabia Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: UAE Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: Qatar Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Kuwait Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Bahrain Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Oman Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Islamic Finance Market Revenue billion Forecast, by Financial Sector 2020 & 2033

- Table 12: Islamic Finance Market Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Iran Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Egypt Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of Middle East Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Islamic Finance Market Revenue billion Forecast, by Financial Sector 2020 & 2033

- Table 17: Islamic Finance Market Revenue billion Forecast, by Country 2020 & 2033

- Table 18: Islamic Finance Market Revenue billion Forecast, by Financial Sector 2020 & 2033

- Table 19: Islamic Finance Market Revenue billion Forecast, by Country 2020 & 2033

- Table 20: Indonesia Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Brunei Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Pakistan Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Rest of Southeast Asia and Asia Pacific Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Islamic Finance Market Revenue billion Forecast, by Financial Sector 2020 & 2033

- Table 25: Islamic Finance Market Revenue billion Forecast, by Country 2020 & 2033

- Table 26: United Kingdom Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Ieland Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Italy Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Rest of Europe Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Islamic Finance Market Revenue billion Forecast, by Financial Sector 2020 & 2033

- Table 31: Islamic Finance Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Islamic Finance Market?

The projected CAGR is approximately 11.5%.

2. Which companies are prominent players in the Islamic Finance Market?

Key companies in the market include Dubai Islamic Bank, National Commercial Bank Saudi Arabia, Bank Mellat Iran, Bank Melli Iran, Kuwait Finance House, Bank Maskan Iran, Qatar Islamic Bank, Abu Dhabi Islamic Bank, May Bank Islamic, CIMB Islamic Bank**List Not Exhaustive.

3. What are the main segments of the Islamic Finance Market?

The market segments include Financial Sector.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.46 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Malaysia is the top Score Value for Islamic Finance Development Indicator.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

January 2023: Abu Dhabi Islamic Bank (ADIB) has increased its ownership in ADIB Egypt to more than 52%. The UAE-based bank has acquired 9.6 million shares from the National Investment Bank (NIB), representing 2.4% of ADIB Egypt's share capital, the bank told the Abu Dhabi Securities Exchange (ADX). The deal has raised ADIB UAE's ownership in the Egyptian unit to 52.607%.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Islamic Finance Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Islamic Finance Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Islamic Finance Market?

To stay informed about further developments, trends, and reports in the Islamic Finance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence