Key Insights

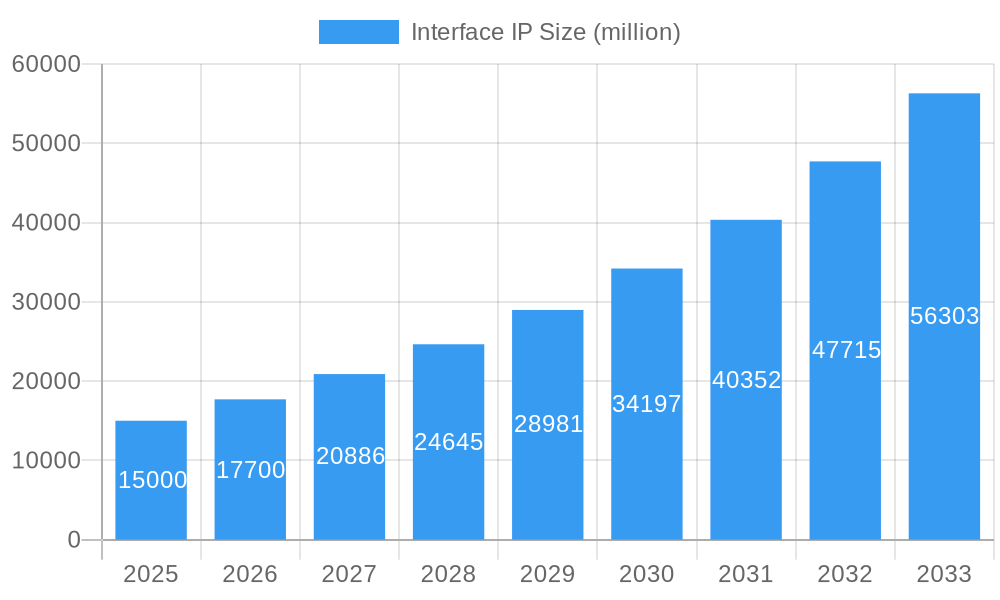

The global Interface IP market is poised for significant expansion, projected to reach a valuation of approximately $15,000 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of roughly 18% anticipated through 2033. This dynamic growth is primarily fueled by the escalating demand for advanced connectivity solutions across burgeoning sectors such as Automotive Electronics and the Internet of Things (IoT). The proliferation of electric vehicles (EVs) and the increasing integration of sophisticated electronic systems in automobiles are creating a substantial need for high-performance and reliable interface IP to manage complex data flows. Simultaneously, the rapid adoption of smart devices, industrial automation, and connected infrastructure within the IoT landscape necessitates scalable and efficient interface IP to ensure seamless communication and data exchange. Cloud computing also remains a pivotal driver, as data centers continuously upgrade their infrastructure to handle ever-increasing data volumes, further propelling the demand for advanced interface IP solutions.

Interface IP Market Size (In Billion)

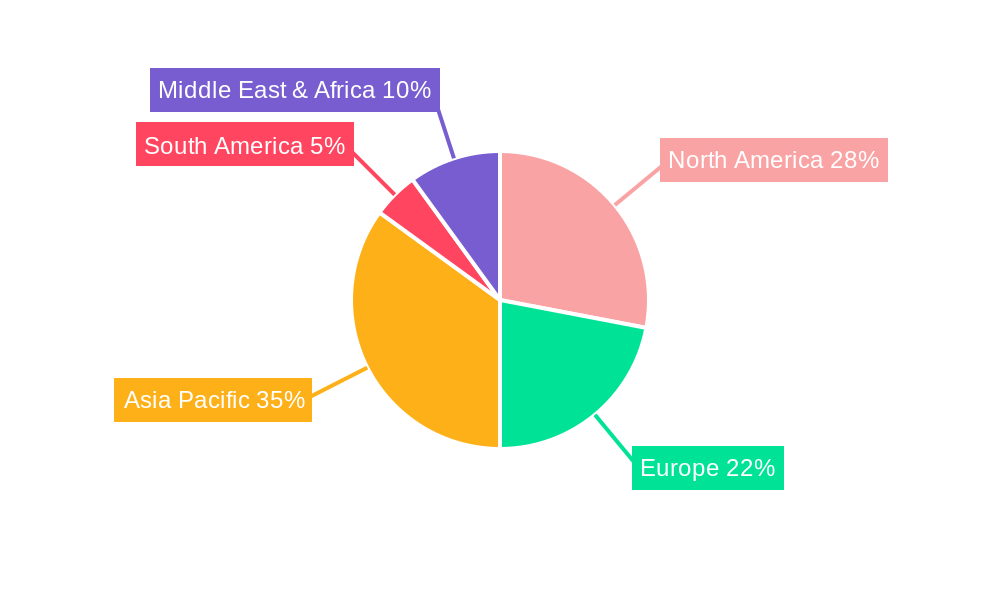

Key trends shaping the Interface IP market include the growing adoption of PCIe and CXL (Compute Express Link) technologies, which are revolutionizing high-speed interconnectivity in data-intensive applications and enabling tighter integration between CPUs and accelerators. The evolution of DDR memory interfaces also continues to be a critical area of development, supporting the performance demands of advanced computing. However, the market faces certain restraints, including the escalating complexity and cost associated with IP development and verification, alongside the stringent regulatory requirements and evolving standards that necessitate continuous adaptation. Furthermore, the potential for supply chain disruptions and geopolitical uncertainties could present challenges to sustained market growth. Despite these hurdles, the underlying technological advancements and the insatiable demand for enhanced data processing and communication capabilities are expected to steer the Interface IP market towards a prosperous future, with Asia Pacific emerging as a dominant region due to its strong manufacturing base and rapid technological adoption.

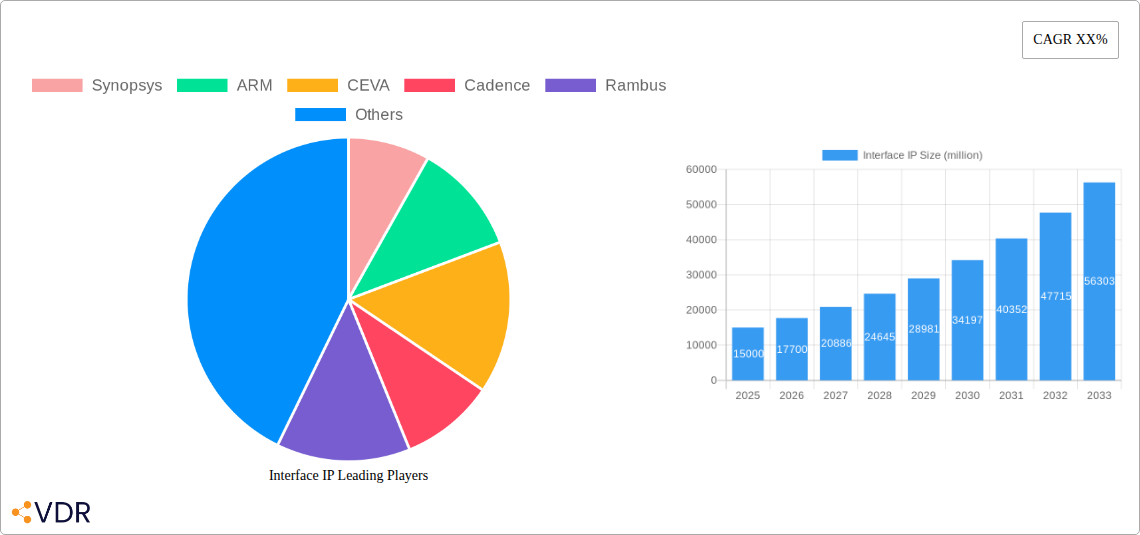

Interface IP Company Market Share

Here is a comprehensive, SEO-optimized report description for Interface IP, designed for maximum visibility and engagement with industry professionals, with all values presented in million units.

Interface IP Market Dynamics & Structure

The global Interface IP market, valued at approximately $15,200 million in 2025, is characterized by a moderately concentrated structure with key players like Synopsys, ARM, CEVA, Cadence, and Rambus holding significant market shares. Technological innovation acts as the primary driver, with constant advancements in high-speed serial links, low-power designs, and emerging protocols like CXL fueling market expansion. The regulatory landscape, particularly concerning data security and interoperability standards, plays a crucial role in shaping product development and market entry. Competitive product substitutes are limited, given the specialized nature of IP licensing, but alternative architectural approaches can emerge. End-user demographics are diverse, spanning the burgeoning automotive electronics sector, the ubiquitous IoT ecosystem, and the ever-expanding cloud computing infrastructure, each with unique performance and power demands. Mergers and acquisition (M&A) trends, while not rampant, are strategically employed by larger entities to acquire niche technologies or expand their IP portfolios, with an estimated 5 M&A deals in the historical period of 2019-2024. Innovation barriers include the high cost of R&D, long development cycles, and the need for extensive verification and validation.

- Market Concentration: Moderately concentrated, with major players dominating specific IP segments.

- Technological Innovation Drivers: High-speed SerDes, CXL, AI/ML acceleration IPs, low-power design.

- Regulatory Frameworks: Emphasis on industry standards (PCIe, DDR), cybersecurity, and regional compliance.

- Competitive Product Substitutes: Primarily architectural alternatives rather than direct IP replacements.

- End-User Demographics: Automotive Electronics (XX%), IoT (XX%), Cloud Computing (XX%), Other (XX%).

- M&A Trends: Strategic acquisitions for technology integration and portfolio expansion.

Interface IP Growth Trends & Insights

The Interface IP market is poised for robust growth, projected to expand from an estimated $15,200 million in 2025 to a substantial $38,500 million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 12.5%. This expansion is driven by the insatiable demand for higher bandwidth, lower latency, and increased power efficiency across a multitude of electronic devices and systems. The adoption rates of advanced interface technologies are accelerating, particularly in the automotive sector, where the integration of autonomous driving features and sophisticated infotainment systems necessitates high-performance data transfer. Similarly, the proliferation of smart devices in the IoT landscape and the ever-increasing data processing needs of cloud computing environments are creating unprecedented demand for robust and versatile interface IP solutions. Technological disruptions, such as the emergence and standardization of PCIe 6.0/7.0 and the growing importance of CXL for memory and I/O coherency, are reshaping the market landscape, compelling IP providers to continuously innovate. Consumer behavior shifts towards more data-intensive applications, including immersive gaming, high-definition video streaming, and advanced AI-powered services, further amplify the need for cutting-edge interface IP. The market penetration of advanced interface IP is projected to grow from approximately 60% in 2025 to over 85% by 2033 as legacy interfaces become obsolete.

The historical period (2019-2024) saw the market grow from approximately $9,500 million to an estimated $13,500 million, showcasing a steady upward trajectory. The base year, 2025, marks a critical inflection point with significant investments in next-generation interface technologies. The forecast period (2025-2033) anticipates an accelerated growth phase, fueled by widespread adoption of these advanced standards. Market size evolution will be primarily dictated by the increasing complexity and interconnectedness of modern electronic systems. Adoption rates for specific interface types, such as SerDes for high-speed connectivity and DDR for memory access, are expected to surge. Technological disruptions like the transition to optical interfaces in certain data center applications and the integration of AI accelerators directly into the data path will also influence growth. Consumer behavior, increasingly reliant on seamless and high-performance digital experiences, will continue to be a primary demand driver.

Dominant Regions, Countries, or Segments in Interface IP

The Application segment of Automotive Electronics is emerging as a dominant force in the global Interface IP market, projected to account for a significant portion of market share and drive growth throughout the forecast period. This dominance is underpinned by several key factors. The escalating complexity of modern vehicles, driven by the integration of advanced driver-assistance systems (ADAS), autonomous driving capabilities, sophisticated infotainment systems, and the increasing electrification of powertrains, necessitates an unprecedented level of data processing and communication. This translates directly into a high demand for high-bandwidth, low-latency, and highly reliable interface IP solutions.

- Key Drivers in Automotive Electronics:

- ADAS and Autonomous Driving: Requirements for real-time sensor data processing (e.g., LiDAR, radar, cameras) and inter-ECU communication.

- In-Vehicle Networking: Transition to Ethernet and advanced SerDes for high-speed data transmission within the vehicle.

- Infotainment Systems: Demand for high-resolution displays, complex graphics processing, and seamless connectivity.

- Electrification: Increased data exchange for battery management systems, charging infrastructure, and power control.

- Safety and Security Standards: Stringent regulatory requirements for functional safety and data integrity.

The Type segment of PCIe and CXL is another significant growth engine, closely tied to the expansion of cloud computing and high-performance computing. PCIe 6.0/7.0 and the advent of CXL are revolutionizing data center architectures by enabling faster interconnects between CPUs, GPUs, accelerators, and memory. This surge in demand is fueled by the growing need for scalable and efficient memory pooling and coherent I/O expansion. Cloud computing's relentless expansion, driven by big data analytics, AI/ML workloads, and the burgeoning metaverse, requires immense computational power and data throughput, making PCIe and CXL IP indispensable. The market share for PCIe and CXL IP is expected to grow exponentially, surpassing other interface types in terms of CAGR.

- Key Drivers in PCIe and CXL:

- Cloud Data Centers: Supporting high-speed networking, storage, and accelerator interconnects.

- High-Performance Computing (HPC): Enabling massive parallel processing and data-intensive simulations.

- AI/ML Acceleration: Facilitating high-bandwidth communication between AI accelerators and host processors.

- Memory Expansion and Pooling: CXL’s ability to disaggregate memory and I/O creates new architectural possibilities.

Geographically, North America and Asia-Pacific are anticipated to lead the market due to their robust semiconductor manufacturing ecosystems, significant investments in cloud infrastructure, and strong automotive R&D. Europe’s stringent automotive regulations also act as a catalyst for advanced interface adoption.

Interface IP Product Landscape

The Interface IP product landscape is characterized by rapid innovation, focusing on delivering higher bandwidth, lower power consumption, and enhanced signal integrity. Key product developments include advanced SerDes technologies supporting speeds up to 200 Gbps and beyond, crucial for data centers and high-performance networking. PCIe 6.0 and the emerging PCIe 7.0 standards are enabling unprecedented data transfer rates for accelerators and storage. The integration of CXL provides a unified memory and I/O architecture, essential for next-generation computing. Furthermore, specialized IPs for automotive applications are being developed to meet stringent functional safety and real-time processing requirements. Unique selling propositions often revolve around the IP’s power efficiency, area optimization, ease of integration, and comprehensive verification suites.

Key Drivers, Barriers & Challenges in Interface IP

Key Drivers: The Interface IP market is propelled by the escalating demand for higher data bandwidth and lower latency across diverse applications, including AI/ML, 5G, automotive electronics, and cloud computing. Technological advancements in semiconductor fabrication processes enable the development of more complex and higher-performing IP cores. The growth of IoT devices also contributes to the demand for efficient and compact interface solutions. Government initiatives supporting digital transformation and semiconductor innovation further fuel market expansion.

- Technological Drivers: AI/ML adoption, 5G rollout, autonomous vehicles, data center expansion.

- Economic Drivers: Increasing semiconductor investments, growing consumer electronics market.

- Policy Drivers: Digital India initiatives, national semiconductor strategies.

Barriers & Challenges: The primary challenges facing the Interface IP market include the high costs associated with R&D and the lengthy verification cycles required for complex IP cores. Intense competition among IP providers necessitates continuous innovation and price optimization. Supply chain disruptions, particularly for essential components and advanced manufacturing capabilities, can impede production and delivery timelines. Evolving industry standards and the need for backward compatibility add to the complexity of IP development and integration. The threat of intellectual property infringement also presents a constant concern for IP vendors.

- Supply Chain Issues: Global chip shortages impacting development and production schedules.

- Regulatory Hurdles: Evolving cybersecurity regulations and interoperability standards.

- Competitive Pressures: Intense competition driving down margins and demanding constant innovation.

- R&D Costs: High investment required for developing cutting-edge IP.

Emerging Opportunities in Interface IP

Emerging opportunities in the Interface IP market are abundant, driven by the rapid evolution of technology and changing consumer demands. The metaverse and augmented/virtual reality (AR/VR) sectors present a significant untapped market for high-bandwidth, low-latency interface IP to support immersive experiences. Advancements in edge computing and AI at the edge will require specialized interface IP for localized data processing and faster inference. The increasing adoption of advanced connectivity standards like Wi-Fi 7 and USB4 will also create new avenues for IP providers. Furthermore, the ongoing transition to more power-efficient and compact designs for mobile and wearable devices opens up opportunities for innovative low-power interface IP.

Growth Accelerators in the Interface IP Industry

The Interface IP industry's long-term growth is significantly accelerated by breakthroughs in interconnect technologies, such as the commercialization of CXL and the widespread adoption of PCIe 6.0 and 7.0. Strategic partnerships between IP vendors and System-on-Chip (SoC) designers, as well as foundries, are crucial for ensuring seamless integration and rapid time-to-market. The expanding reach of cloud computing, coupled with the increasing computational demands of AI and machine learning, acts as a powerful catalyst. Moreover, the continuous expansion of the IoT ecosystem, encompassing smart homes, industrial automation, and connected healthcare, fuels the demand for a wide array of interface IP solutions. Market expansion into emerging economies and the development of specialized IP for niche applications also contribute to sustained growth.

Key Players Shaping the Interface IP Market

- Synopsys

- ARM

- CEVA

- Cadence

- Rambus

- Actt

- Intel

- Marvell

- Broadcom

- Xilinx (now AMD)

Notable Milestones in Interface IP Sector

- 2019: Introduction of PCIe 5.0, enabling 32 GT/s per lane, significantly boosting data throughput.

- 2020: Growing adoption of high-speed SerDes IP for 5G infrastructure and data centers.

- 2021: Initial specifications and early implementations of CXL begin to emerge, promising memory coherency.

- 2022: Release of PCIe 6.0 specifications, doubling the bandwidth of PCIe 5.0 and introducing PAM4 signaling.

- 2023: Increased focus on power-efficient interface IP for edge computing and IoT applications.

- 2024: First commercial deployments and broader industry support for CXL 1.1.

- 2025 (Estimated): Anticipated release of PCIe 7.0 specifications, targeting 128 GT/s per lane.

- 2026 (Estimated): Maturation of CXL ecosystem, with widespread adoption in server and workstation platforms.

In-Depth Interface IP Market Outlook

The Interface IP market is set for an optimistic future, driven by the relentless pursuit of performance and efficiency across the digital landscape. The continued evolution of high-speed interconnects like PCIe and the transformative potential of CXL will be central to this growth. The increasing integration of AI and machine learning at the edge, coupled with the expanding capabilities of cloud infrastructure, will create sustained demand for sophisticated IP solutions. Opportunities in emerging sectors such as the metaverse and advanced automotive electronics will further fuel market expansion. Strategic alliances and continued investment in R&D will be critical for players to capitalize on these evolving trends and maintain a competitive edge in this dynamic and indispensable industry.

Interface IP Segmentation

-

1. Application

- 1.1. Automotive Electronics

- 1.2. IoT

- 1.3. Cloud Computing

- 1.4. Other

-

2. Types

- 2.1. PCIe and CXL

- 2.2. DDR

- 2.3. SerDes

- 2.4. D2D

- 2.5. Ethernet

- 2.6. HDMI

- 2.7. Other

Interface IP Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Interface IP Regional Market Share

Geographic Coverage of Interface IP

Interface IP REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.53% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Automotive Electronics

- 5.1.2. IoT

- 5.1.3. Cloud Computing

- 5.1.4. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. PCIe and CXL

- 5.2.2. DDR

- 5.2.3. SerDes

- 5.2.4. D2D

- 5.2.5. Ethernet

- 5.2.6. HDMI

- 5.2.7. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Interface IP Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Automotive Electronics

- 6.1.2. IoT

- 6.1.3. Cloud Computing

- 6.1.4. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. PCIe and CXL

- 6.2.2. DDR

- 6.2.3. SerDes

- 6.2.4. D2D

- 6.2.5. Ethernet

- 6.2.6. HDMI

- 6.2.7. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Interface IP Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Automotive Electronics

- 7.1.2. IoT

- 7.1.3. Cloud Computing

- 7.1.4. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. PCIe and CXL

- 7.2.2. DDR

- 7.2.3. SerDes

- 7.2.4. D2D

- 7.2.5. Ethernet

- 7.2.6. HDMI

- 7.2.7. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Interface IP Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Automotive Electronics

- 8.1.2. IoT

- 8.1.3. Cloud Computing

- 8.1.4. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. PCIe and CXL

- 8.2.2. DDR

- 8.2.3. SerDes

- 8.2.4. D2D

- 8.2.5. Ethernet

- 8.2.6. HDMI

- 8.2.7. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Interface IP Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Automotive Electronics

- 9.1.2. IoT

- 9.1.3. Cloud Computing

- 9.1.4. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. PCIe and CXL

- 9.2.2. DDR

- 9.2.3. SerDes

- 9.2.4. D2D

- 9.2.5. Ethernet

- 9.2.6. HDMI

- 9.2.7. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Interface IP Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Automotive Electronics

- 10.1.2. IoT

- 10.1.3. Cloud Computing

- 10.1.4. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. PCIe and CXL

- 10.2.2. DDR

- 10.2.3. SerDes

- 10.2.4. D2D

- 10.2.5. Ethernet

- 10.2.6. HDMI

- 10.2.7. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Interface IP Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Automotive Electronics

- 11.1.2. IoT

- 11.1.3. Cloud Computing

- 11.1.4. Other

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. PCIe and CXL

- 11.2.2. DDR

- 11.2.3. SerDes

- 11.2.4. D2D

- 11.2.5. Ethernet

- 11.2.6. HDMI

- 11.2.7. Other

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Synopsys

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 ARM

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 CEVA

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Cadence

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Rambus

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Actt

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.1 Synopsys

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Interface IP Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Interface IP Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Interface IP Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Interface IP Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Interface IP Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Interface IP Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Interface IP Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Interface IP Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Interface IP Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Interface IP Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Interface IP Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Interface IP Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Interface IP Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Interface IP Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Interface IP Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Interface IP Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Interface IP Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Interface IP Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Interface IP Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Interface IP Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Interface IP Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Interface IP Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Interface IP Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Interface IP Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Interface IP Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Interface IP Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Interface IP Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Interface IP Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Interface IP Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Interface IP Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Interface IP Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Interface IP Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Interface IP Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Interface IP Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Interface IP Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Interface IP Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Interface IP Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Interface IP Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Interface IP Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Interface IP Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Interface IP Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Interface IP Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Interface IP Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Interface IP Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Interface IP Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Interface IP Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Interface IP Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Interface IP Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Interface IP Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Interface IP Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Interface IP?

The projected CAGR is approximately 7.53%.

2. Which companies are prominent players in the Interface IP?

Key companies in the market include Synopsys, ARM, CEVA, Cadence, Rambus, Actt.

3. What are the main segments of the Interface IP?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Interface IP," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Interface IP report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Interface IP?

To stay informed about further developments, trends, and reports in the Interface IP, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence