Key Insights

The India connected vehicles market is experiencing robust growth, driven by increasing smartphone penetration, improving infrastructure for data connectivity (5G rollout), and government initiatives promoting digitalization. A Compound Annual Growth Rate (CAGR) exceeding 20% from 2019-2033 signifies a significant expansion, particularly within passenger cars where features like driver-assistance systems, infotainment, and telematics are becoming increasingly standard. The market segmentation reveals a strong demand for V2V (Vehicle-to-Vehicle) and V2I (Vehicle-to-Infrastructure) connectivity solutions, reflecting the push for enhanced road safety and intelligent transportation systems. While the market is currently dominated by passenger cars, the commercial vehicle segment is poised for substantial growth fueled by fleet management solutions and advancements in logistics optimization. Regional variations exist, with potentially higher growth in metropolitan areas of North and South India due to higher vehicle density and technological adoption. The presence of major automotive players like Maruti Suzuki, Hyundai, and Toyota underscores the market's maturity and competitive landscape. However, challenges remain, including addressing data security concerns and ensuring seamless connectivity across various platforms and regions. Overcoming these hurdles will be crucial for sustainable growth in this dynamic market.

The forecast period (2025-2033) anticipates continued expansion, driven by technological advancements in areas like Artificial Intelligence (AI) and the Internet of Things (IoT), enhancing the capabilities of connected vehicles. The integration of connected car technology with smart cities initiatives is another significant driver, creating opportunities for improved traffic management and urban planning. As consumer preferences shift towards safer and more technologically advanced vehicles, the demand for connected features will continue to rise. This will spur further investments in research and development, leading to the emergence of innovative solutions and services in the connected vehicle ecosystem. The Indian market's unique demographic and economic landscape present both challenges and opportunities for stakeholders. A strategic focus on affordability, accessibility, and addressing regional disparities will be critical for maximizing the market's potential.

India Connected Vehicles Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the burgeoning India connected vehicles market, projecting robust growth from 2025 to 2033. It covers market dynamics, growth trends, regional dominance, product landscapes, key players, and future outlook, offering invaluable insights for industry professionals, investors, and strategic decision-makers. The report leverages extensive data analysis, covering the historical period (2019-2024), base year (2025), and forecast period (2025-2033), with estimated market values in million units.

India Connected Vehicles Industry Market Dynamics & Structure

The Indian connected vehicles market is characterized by increasing market concentration among major players, driven by technological innovations in V2X (Vehicle-to-Everything) communication, advanced driver-assistance systems (ADAS), and in-vehicle infotainment systems. Stringent regulatory frameworks regarding data privacy and cybersecurity are shaping the market landscape. The market witnesses significant competition from established automotive manufacturers and emerging technology providers. Consumer demand is largely influenced by rising disposable incomes, increased smartphone penetration, and a growing preference for advanced vehicle features.

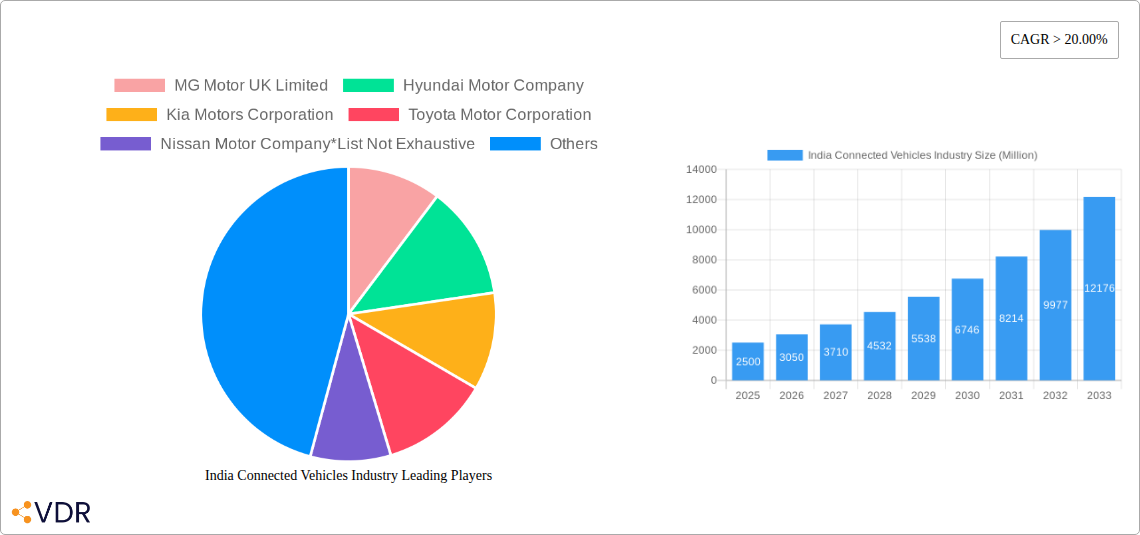

- Market Concentration: The top 5 players (MG Motor UK Limited, Hyundai Motor Company, Kia Motors Corporation, Toyota Motor Corporation, and Maruti Suzuki India Limited) hold an estimated xx% market share in 2025.

- Technological Innovation: Focus on 5G connectivity, AI-powered features, and improved data analytics is driving growth.

- Regulatory Landscape: Government initiatives promoting digitalization and smart infrastructure are fostering market expansion, while data privacy regulations are presenting challenges.

- Competitive Landscape: Intense competition exists among OEMs and Tier-1 suppliers, leading to strategic partnerships and mergers & acquisitions. xx M&A deals were recorded in the 2019-2024 period.

- End-User Demographics: The primary target market comprises affluent urban consumers and businesses seeking enhanced safety, efficiency, and connectivity solutions.

India Connected Vehicles Industry Growth Trends & Insights

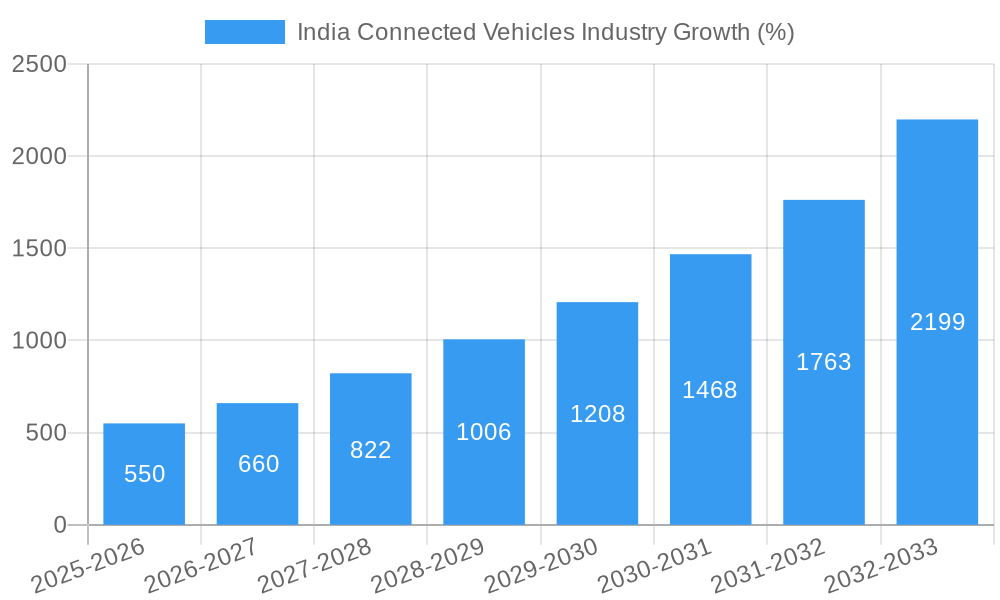

The Indian connected vehicles market is experiencing exponential growth, fueled by rising vehicle sales, increasing smartphone penetration, and improving digital infrastructure. The market size is projected to reach xx million units by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of xx% during the forecast period. Increased adoption of connected car features, particularly in the passenger car segment, is a key driver. Technological disruptions like the integration of 5G and AI are reshaping consumer preferences, leading to demand for advanced safety and infotainment features. Consumer behavior is shifting towards subscription-based services and data-driven experiences.

Dominant Regions, Countries, or Segments in India Connected Vehicles Industry

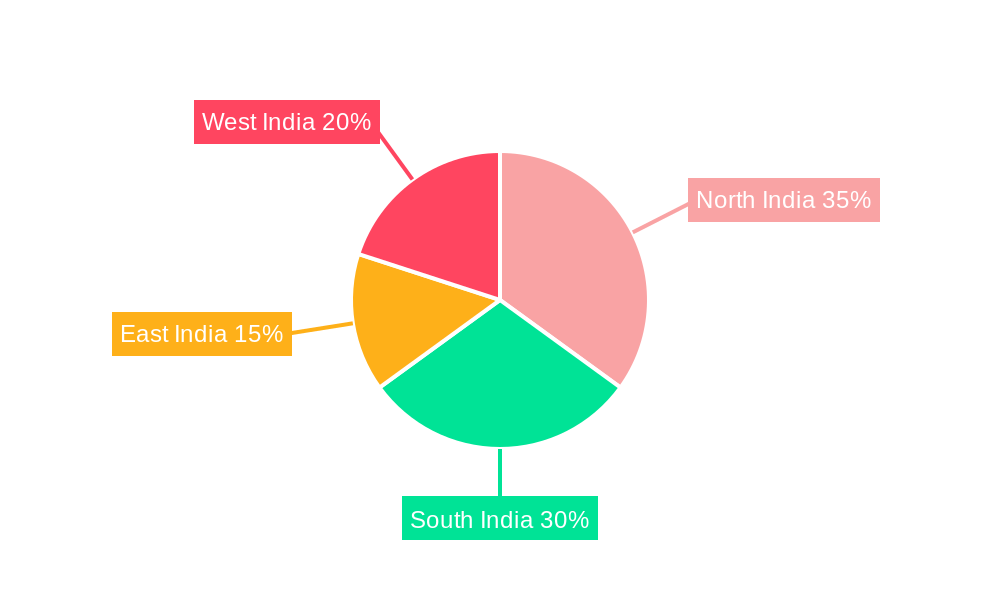

The passenger car segment dominates the Indian connected vehicles market, accounting for xx% of the total market share in 2025. The growth is primarily driven by strong demand in urban areas like Mumbai, Delhi, Bengaluru, and Chennai. The driver assistance systems segment shows the fastest growth rate due to increasing consumer focus on safety features. V2Vehicle connectivity is also a rapidly expanding segment, followed by V2Infrastructure.

- Leading Segment: Passenger Cars (by vehicle type); Driver Assistance (by application type); V2Vehicle (by connectivity type).

- Key Growth Drivers: Government initiatives promoting vehicle safety and digital infrastructure development; rising disposable incomes; and improved road infrastructure in major cities.

- Regional Dominance: Urban areas show higher market penetration due to higher vehicle ownership and better digital infrastructure.

India Connected Vehicles Industry Product Landscape

The Indian connected vehicle market showcases a diverse range of products, encompassing advanced driver-assistance systems (ADAS) like lane departure warning and adaptive cruise control, sophisticated telematics solutions for fleet management and vehicle diagnostics, and engaging infotainment systems with integrated navigation and connectivity features. These products are differentiated by features like AI-powered voice assistants, over-the-air updates, and seamless integration with mobile devices. Continuous innovation focuses on enhancing safety, efficiency, and user experience.

Key Drivers, Barriers & Challenges in India Connected Vehicles Industry

Key Drivers: Government regulations mandating safety features; increasing demand for advanced driver-assistance systems; and the growing adoption of telematics for fleet management. The expansion of 5G networks is a significant catalyst.

Key Barriers & Challenges: High initial investment costs for connected vehicle technologies; concerns about data privacy and cybersecurity; and the lack of robust digital infrastructure in certain regions. Supply chain disruptions also impact production and market growth. Furthermore, regulatory uncertainty related to data usage and security standards poses a challenge.

Emerging Opportunities in India Connected Vehicles Industry

Untapped opportunities lie in the expansion of connected vehicle services into rural areas, the development of niche applications targeting specific industries (e.g., logistics, agriculture), and the integration of connected vehicle data into smart city initiatives. The increasing adoption of electric vehicles presents opportunities for specialized connected car solutions. The rise of shared mobility services also creates new opportunities for optimized fleet management and passenger experience enhancements.

Growth Accelerators in the India Connected Vehicles Industry

Technological breakthroughs in AI, 5G, and IoT are significantly accelerating market growth. Strategic partnerships between automotive manufacturers, technology providers, and telecommunication companies are fostering innovation and market expansion. Government support for digital infrastructure development and favorable regulatory policies are creating a conducive environment for the growth of the connected vehicle ecosystem.

Key Players Shaping the India Connected Vehicles Industry Market

- MG Motor UK Limited

- Hyundai Motor Company

- Kia Motors Corporation

- Toyota Motor Corporation

- Nissan Motor Company

- Maruti Suzuki India Limited

Notable Milestones in India Connected Vehicles Industry Sector

- 2020: Introduction of mandatory safety features in new vehicles.

- 2021: Launch of 5G trials by major telecom operators.

- 2022: Several major partnerships between automakers and technology firms for connected car solutions.

- 2023: Significant increase in adoption of telematics solutions in commercial vehicle fleets.

In-Depth India Connected Vehicles Industry Market Outlook

The Indian connected vehicles market is poised for substantial growth, driven by technological advancements, favorable government policies, and increasing consumer demand. Strategic investments in R&D, expansion into untapped markets, and strategic partnerships will be crucial for success. The market presents significant opportunities for both established players and new entrants, fostering innovation and driving the evolution of the automotive industry in India.

India Connected Vehicles Industry Segmentation

-

1. Application Type

- 1.1. Driver Assistance

- 1.2. Telematics

- 1.3. Infotainment

- 1.4. Other Application Types

-

2. Connectivity Type

- 2.1. Integrated

- 2.2. Embedded

- 2.3. Tethered

-

3. Vehicle Connectivity

- 3.1. Vehicle-to-Vehicle (V2V)

- 3.2. Vehicle-to-Infrastructure (V2I)

- 3.3. Vehicle-to-Pedestrain (V2P)

-

4. Vehicle Type

- 4.1. Passenger Cars

- 4.2. Commercial Vehicle

India Connected Vehicles Industry Segmentation By Geography

- 1. India

India Connected Vehicles Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 20.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing disposable income and Low-interest rates from lenders increase the market demand

- 3.3. Market Restrains

- 3.3.1. High initial costs may obstruct the growth

- 3.4. Market Trends

- 3.4.1. EVs will Boost the Market's Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. India Connected Vehicles Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application Type

- 5.1.1. Driver Assistance

- 5.1.2. Telematics

- 5.1.3. Infotainment

- 5.1.4. Other Application Types

- 5.2. Market Analysis, Insights and Forecast - by Connectivity Type

- 5.2.1. Integrated

- 5.2.2. Embedded

- 5.2.3. Tethered

- 5.3. Market Analysis, Insights and Forecast - by Vehicle Connectivity

- 5.3.1. Vehicle-to-Vehicle (V2V)

- 5.3.2. Vehicle-to-Infrastructure (V2I)

- 5.3.3. Vehicle-to-Pedestrain (V2P)

- 5.4. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.4.1. Passenger Cars

- 5.4.2. Commercial Vehicle

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. India

- 5.1. Market Analysis, Insights and Forecast - by Application Type

- 6. North India India Connected Vehicles Industry Analysis, Insights and Forecast, 2019-2031

- 7. South India India Connected Vehicles Industry Analysis, Insights and Forecast, 2019-2031

- 8. East India India Connected Vehicles Industry Analysis, Insights and Forecast, 2019-2031

- 9. West India India Connected Vehicles Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 MG Motor UK Limited

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Hyundai Motor Company

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Kia Motors Corporation

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Toyota Motor Corporation

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Nissan Motor Company*List Not Exhaustive

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Maruti Suzuki India Limited

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.1 MG Motor UK Limited

List of Figures

- Figure 1: India Connected Vehicles Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: India Connected Vehicles Industry Share (%) by Company 2024

List of Tables

- Table 1: India Connected Vehicles Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: India Connected Vehicles Industry Revenue Million Forecast, by Application Type 2019 & 2032

- Table 3: India Connected Vehicles Industry Revenue Million Forecast, by Connectivity Type 2019 & 2032

- Table 4: India Connected Vehicles Industry Revenue Million Forecast, by Vehicle Connectivity 2019 & 2032

- Table 5: India Connected Vehicles Industry Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 6: India Connected Vehicles Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 7: India Connected Vehicles Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: North India India Connected Vehicles Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: South India India Connected Vehicles Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: East India India Connected Vehicles Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: West India India Connected Vehicles Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: India Connected Vehicles Industry Revenue Million Forecast, by Application Type 2019 & 2032

- Table 13: India Connected Vehicles Industry Revenue Million Forecast, by Connectivity Type 2019 & 2032

- Table 14: India Connected Vehicles Industry Revenue Million Forecast, by Vehicle Connectivity 2019 & 2032

- Table 15: India Connected Vehicles Industry Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 16: India Connected Vehicles Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Connected Vehicles Industry?

The projected CAGR is approximately > 20.00%.

2. Which companies are prominent players in the India Connected Vehicles Industry?

Key companies in the market include MG Motor UK Limited, Hyundai Motor Company, Kia Motors Corporation, Toyota Motor Corporation, Nissan Motor Company*List Not Exhaustive, Maruti Suzuki India Limited.

3. What are the main segments of the India Connected Vehicles Industry?

The market segments include Application Type, Connectivity Type, Vehicle Connectivity, Vehicle Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing disposable income and Low-interest rates from lenders increase the market demand.

6. What are the notable trends driving market growth?

EVs will Boost the Market's Growth.

7. Are there any restraints impacting market growth?

High initial costs may obstruct the growth.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Connected Vehicles Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Connected Vehicles Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Connected Vehicles Industry?

To stay informed about further developments, trends, and reports in the India Connected Vehicles Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence