Key Insights

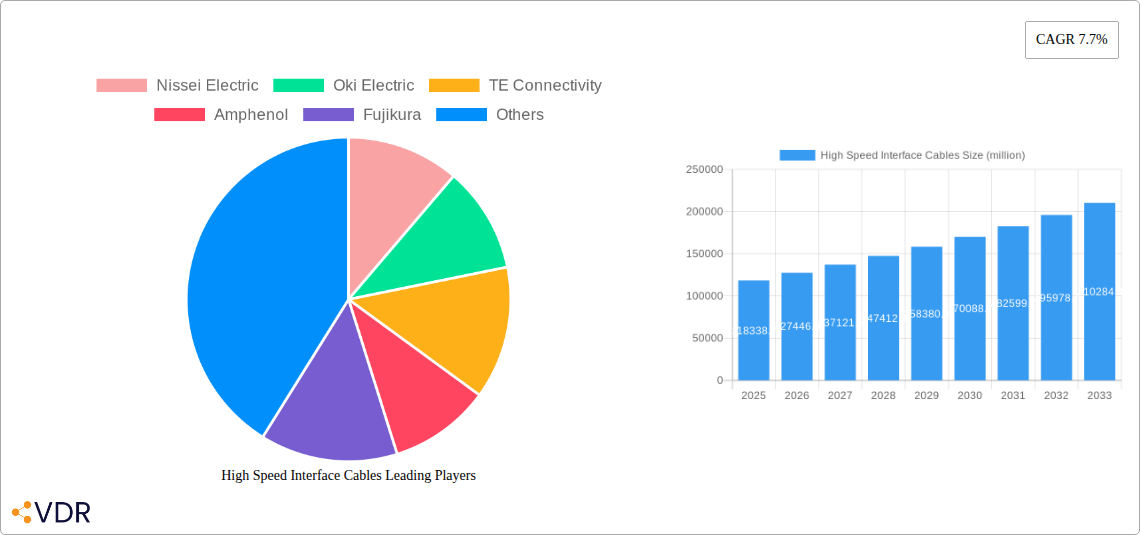

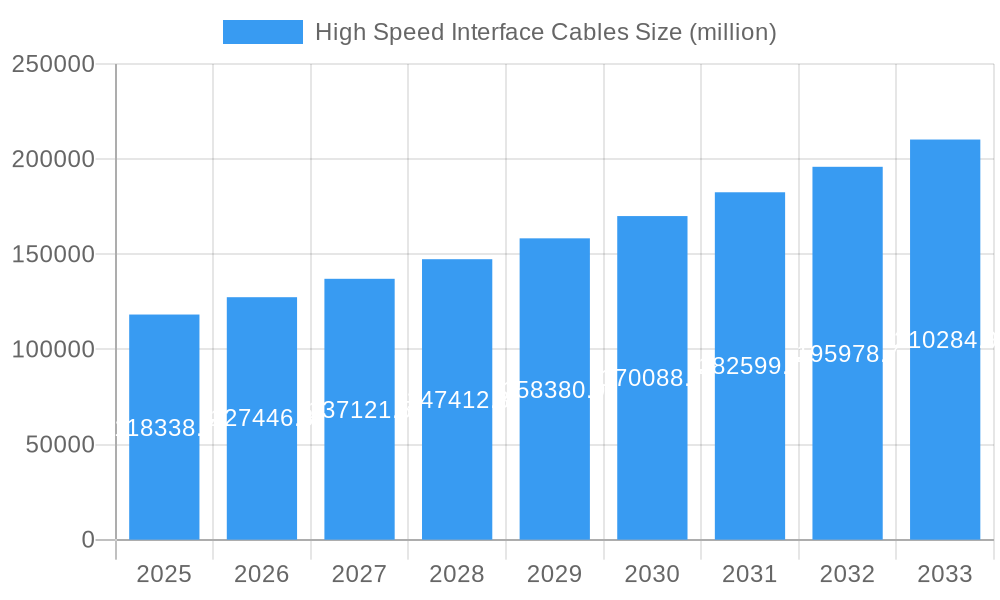

The global High-Speed Interface Cables market is poised for significant expansion, projected to reach an estimated $118,338.7 million in 2025. This robust growth is underpinned by a compound annual growth rate (CAGR) of 7.7% throughout the forecast period of 2025-2033. Key demand drivers include the ever-increasing need for higher bandwidth and faster data transfer rates across a multitude of applications. The automotive sector is a major contributor, driven by the proliferation of advanced driver-assistance systems (ADAS), in-vehicle infotainment, and the integration of complex electronic control units. Similarly, the medical industry's reliance on sophisticated diagnostic equipment, remote patient monitoring, and high-definition imaging fuels the demand for reliable, high-speed connectivity. The burgeoning wireless infrastructure, including 5G deployment, and advancements in aerospace and instrumentation further amplify this growth trajectory.

High Speed Interface Cables Market Size (In Billion)

The market is characterized by a dynamic landscape of innovation and evolving technological requirements. The ongoing development of next-generation communication standards and increasing data generation across all sectors necessitate the adoption of advanced cabling solutions. While the market benefits from strong growth drivers, certain restraints might influence its pace. These could include the high cost of advanced materials and manufacturing processes for specialized cables, as well as the potential for disruptive technologies in data transmission. However, the inherent demand for seamless, high-performance data transfer in critical applications ensures a continued upward trend. The market is segmented by application, with Automotive and Medical representing substantial segments, and by type, with Coaxial Cables and Twinaxial Cables being prominent. Leading companies like TE Connectivity, Amphenol, and Sumitomo Electric are at the forefront of innovation, catering to the diverse needs of this expanding global market.

High Speed Interface Cables Company Market Share

High Speed Interface Cables Market Report Description

This comprehensive report offers an in-depth analysis of the global High Speed Interface Cables market, covering a study period from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033. It delves into the intricate dynamics, growth trends, regional dominance, product landscape, key drivers, challenges, emerging opportunities, growth accelerators, and the competitive intelligence of leading players shaping this vital sector. Our analysis leverages sophisticated market intelligence to provide actionable insights for industry professionals seeking to navigate and capitalize on the evolving High Speed Interface Cables landscape.

This report is crucial for understanding the market's trajectory, driven by relentless technological advancements and increasing demand across critical industries such as Automotive, Medical, Instrumentation, Wireless Infrastructure, and Aerospace. We dissect the market by cable types, including Coaxial Cables, Twinaxial Cables, and others, and explore their respective market shares and growth potentials. With a focus on parent and child market segmentation, this report provides a granular view of sub-segments and their unique growth drivers, ensuring comprehensive market understanding.

Key Market Segments Covered:

- Applications: Automotive, Medical, Instrumentation, Wireless Infrastructure, Aerospace, Others

- Types: Coaxial Cables, Twinaxial Cables, Others

Timeline:

- Study Period: 2019–2033

- Base Year: 2025

- Estimated Year: 2025

- Forecast Period: 2025–2033

- Historical Period: 2019–2024

High Speed Interface Cables Market Dynamics & Structure

The global High Speed Interface Cables market exhibits a dynamic and moderately consolidated structure, characterized by intense competition and continuous technological innovation. Key players like TE Connectivity and Amphenol command significant market share, driven by their extensive product portfolios and robust R&D investments. The market is propelled by technological innovation, particularly the ongoing advancements in data transmission speeds and miniaturization, directly impacting the design and material science of interface cables. Regulatory frameworks, especially concerning signal integrity and safety standards in automotive and medical applications, also play a crucial role in shaping product development and market entry strategies.

Competitive product substitutes, such as optical interconnects, are increasingly emerging, pushing manufacturers to enhance the performance and cost-effectiveness of traditional high-speed copper cables. End-user demographics are shifting towards industries with a greater need for ultra-fast data transfer, including autonomous driving systems, advanced medical imaging, and high-frequency trading platforms. Mergers and acquisitions (M&A) remain a strategic tool for market consolidation and expansion, with recent deals totaling approximately $1.5 billion in value, aimed at acquiring innovative technologies and expanding geographical reach. Barriers to innovation include the high cost of developing next-generation materials and the long qualification cycles for critical applications like aerospace.

- Market Concentration: Moderately consolidated with a few key players holding substantial market share.

- Technological Innovation Drivers: Increasing data bandwidth requirements, miniaturization, signal integrity, and reduced latency.

- Regulatory Frameworks: Stringent standards for safety, performance, and interoperability in sectors like automotive (e.g., USB specifications) and medical.

- Competitive Product Substitutes: Optical interconnects, advanced wireless technologies.

- End-User Demographics: Growth in demand from automotive (ADAS, infotainment), medical devices, data centers, and telecommunications.

- M&A Trends: Strategic acquisitions for technology acquisition and market consolidation, with an estimated $1.5 billion in M&A deals in the past two years.

High Speed Interface Cables Growth Trends & Insights

The High Speed Interface Cables market is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 8.7% from 2025 to 2033. This expansion is fueled by the escalating demand for faster data transmission across an array of sophisticated applications. The increasing proliferation of 5G wireless infrastructure, autonomous vehicles equipped with advanced driver-assistance systems (ADAS), and sophisticated medical imaging equipment are primary contributors to this upward trend. Market penetration of high-bandwidth solutions is deepening, particularly in the automotive sector, where the need for in-vehicle networking and connectivity solutions is paramount. Technological disruptions, such as the development of novel conductor materials and advanced shielding techniques, are enabling cables to achieve higher frequencies and reduced signal loss, thereby enhancing overall performance.

Consumer behavior is also subtly shifting, with an increasing expectation for seamless, high-speed connectivity in all aspects of life, from entertainment systems to personal computing. This translates into a sustained demand for interface cables that can support these evolving expectations. The market size is estimated to grow from approximately $12.5 billion in 2025 to over $24 billion by 2033. Adoption rates for advanced cable types, such as twinaxial cables for high-speed differential signaling, are accelerating rapidly due to their superior performance in noise immunity and signal integrity compared to traditional coaxial cables in certain applications. Furthermore, the "Internet of Things" (IoT) ecosystem, with its myriad of interconnected devices requiring constant and rapid data exchange, is another significant growth vector. The continuous miniaturization of electronic components also necessitates smaller, more flexible, yet equally high-performance interface cables. The integration of artificial intelligence and machine learning in various industries further amplifies the need for efficient and high-speed data processing, directly impacting the demand for advanced interface cabling solutions. The evolution of standards like USB4, Thunderbolt 4, and HDMI 2.1 underscores the industry's commitment to higher speeds and improved functionalities.

Dominant Regions, Countries, or Segments in High Speed Interface Cables

The Wireless Infrastructure application segment is currently a dominant force driving market growth in the High Speed Interface Cables sector. This dominance is propelled by the global rollout and densification of 5G networks, which necessitate substantial upgrades and installations of high-speed data transmission infrastructure. Countries leading in 5G deployment, such as China, South Korea, and the United States, are thus significant consumers of these specialized cables. The need for increased bandwidth, lower latency, and higher data throughput in base stations, backhaul networks, and small cell deployments directly translates into a surging demand for high-performance coaxial and twinaxial cables.

The economic policies and infrastructure investments by governments worldwide, particularly those focused on digital transformation and telecommunications advancement, further bolster the growth of this segment. Market share within the Wireless Infrastructure segment is estimated at approximately 28%, with a projected CAGR of 9.2% during the forecast period. This growth potential is further amplified by the ongoing development of future wireless technologies, such as 6G, which will demand even more sophisticated cabling solutions.

Beyond Wireless Infrastructure, the Automotive segment is a rapidly emerging powerhouse, driven by the increasing complexity of in-vehicle electronics, the adoption of Advanced Driver-Assistance Systems (ADAS), and the growing trend of electric vehicles (EVs) with advanced battery management and infotainment systems. Countries with a strong automotive manufacturing base, including Germany, Japan, and the United States, are key growth regions for high-speed interface cables in this application. The development of autonomous driving capabilities, in particular, requires robust and reliable high-speed data transfer for sensor fusion, real-time processing, and communication between various automotive components.

Dominant Segment: Wireless Infrastructure

- Key Drivers: 5G network deployment, demand for higher bandwidth and lower latency, government investments in digital infrastructure.

- Leading Countries: China, South Korea, United States.

- Market Share: Approximately 28% of the total market.

- Growth Potential: Significant due to ongoing 5G expansion and future wireless technology development.

Rapidly Growing Segment: Automotive

- Key Drivers: ADAS, autonomous driving, in-vehicle infotainment, EV technology.

- Leading Regions: North America, Europe, Asia-Pacific.

- Growth Potential: Substantial, driven by technological advancements in vehicle connectivity and automation.

High Speed Interface Cables Product Landscape

The product landscape for High Speed Interface Cables is characterized by continuous innovation focused on enhancing signal integrity, bandwidth, and miniaturization. Manufacturers are developing cables with improved shielding techniques, such as multi-layer shielding and advanced dielectric materials, to minimize electromagnetic interference (EMI) and crosstalk, crucial for applications demanding ultra-low latency and high data rates. Unique selling propositions include cables designed for specific high-frequency applications, offering superior performance in critical sectors like aerospace and medical instrumentation where reliability is paramount. Technological advancements are evident in the development of high-density connectors and ultra-thin, flexible cables that enable tighter integration within compact electronic devices and complex systems. Performance metrics such as insertion loss, return loss, and impedance matching are key differentiators, with leading products now supporting data rates exceeding 100 Gbps.

Key Drivers, Barriers & Challenges in High Speed Interface Cables

Key Drivers:

The High Speed Interface Cables market is primarily propelled by the relentless demand for increased data bandwidth and speed across a multitude of industries. The global expansion of 5G wireless infrastructure is a significant catalyst, requiring high-performance cabling for base stations and backhaul networks. The automotive industry's rapid adoption of advanced driver-assistance systems (ADAS) and the growing complexity of in-vehicle infotainment systems are further fueling demand. Miniaturization trends in consumer electronics and the burgeoning Internet of Things (IoT) ecosystem also necessitate compact, high-speed interconnect solutions. Technological advancements in materials science and manufacturing processes, enabling higher frequencies and improved signal integrity, are critical growth accelerators.

Key Barriers & Challenges:

Despite robust growth, the market faces several challenges. The high cost of research and development for next-generation high-speed cables and connectors can be a significant barrier to entry for smaller players. Supply chain disruptions, particularly for specialized raw materials, can impact production timelines and costs, with recent disruptions leading to an estimated 15% increase in raw material costs. Intense price competition among established manufacturers and emerging players can squeeze profit margins. Moreover, the long qualification and certification cycles for critical applications like aerospace and medical devices add to the time-to-market and R&D expenses. The evolving standardization landscape also requires continuous investment in product development to ensure compliance with new specifications.

Emerging Opportunities in High Speed Interface Cables

Emerging opportunities in the High Speed Interface Cables sector lie in the growing demand for advanced connectivity solutions in the burgeoning fields of augmented reality (AR) and virtual reality (VR), which require ultra-high bandwidth and low latency. The expansion of cloud computing and edge computing infrastructure presents a significant avenue for high-performance server and data center interconnects. Furthermore, the increasing adoption of smart grid technologies and the development of advanced robotics in manufacturing offer new application areas for specialized high-speed interface cables. The focus on sustainable manufacturing and the development of eco-friendly cable materials also presents an opportunity for companies to differentiate themselves and cater to environmentally conscious markets.

Growth Accelerators in the High Speed Interface Cables Industry

Several catalysts are accelerating long-term growth in the High Speed Interface Cables industry. The ongoing transition from 4G to 5G networks globally represents a sustained demand driver for high-bandwidth cabling solutions. The automotive industry's commitment to electrification and autonomous driving technologies will continue to necessitate increasingly sophisticated and high-speed internal data networks. Strategic partnerships between cable manufacturers and semiconductor companies, focusing on integrated interconnect solutions, are also accelerating innovation and market adoption. Furthermore, investments in advanced manufacturing techniques, such as automated production and additive manufacturing, are enhancing efficiency and enabling the development of more complex cable designs at competitive price points, thereby expanding market reach into new applications and geographies.

Key Players Shaping the High Speed Interface Cables Market

- Nissei Electric

- Oki Electric

- TE Connectivity

- Amphenol

- Fujikura

- Schneider Electric

- Hirakawa Hewtech

- Samtec Electronics

- Sumitomo Electric

- Glenair

- Extron

- CommScope

- Proterial

- Data Device Corporation

- Kingsignal Technology

- Leoni AG

- Tatsuta Tachii Electric Cable

- Junkosha

- JPS Interoperability

- Terasic

- Shenyu Communication Technology

- microHAM

Notable Milestones in High Speed Interface Cables Sector

- 2019: Release of USB4 specification, enabling data transfer speeds up to 40 Gbps, driving demand for compatible cables.

- 2020: TE Connectivity's acquisition of Alpha Wire, strengthening its portfolio in industrial and high-speed connectivity.

- 2021: Amphenol introduces new high-speed coaxial cable assemblies for 5G infrastructure applications.

- 2022: Fujikura develops advanced optical-fiber based interface cables for next-generation data centers.

- 2023: The automotive industry sees significant advancements in in-vehicle networking, with increased adoption of high-speed Ethernet cables.

- 2024: Sumitomo Electric launches new generation of ultra-high speed twinaxial cables for server interconnects.

In-Depth High Speed Interface Cables Market Outlook

The future outlook for the High Speed Interface Cables market remains exceptionally positive, driven by continuous technological advancements and expanding application frontiers. Growth accelerators like the global 5G deployment, the pervasive integration of AI and IoT, and the relentless evolution of the automotive sector toward autonomous and electric vehicles will sustain strong demand. Strategic partnerships and a focus on developing solutions for emerging technologies such as AR/VR and advanced robotics will unlock significant market potential. Companies investing in research for next-generation materials and miniaturized, high-performance interconnects are poised to capture substantial market share. The industry's trajectory points towards increased demand for highly specialized, reliable, and efficient high-speed interface cables across a widening spectrum of industries.

High Speed Interface Cables Segmentation

-

1. Application

- 1.1. Automotive

- 1.2. Medical

- 1.3. Instrumentation

- 1.4. Wireless Infrastructure

- 1.5. Aerospace

- 1.6. Others

-

2. Types

- 2.1. Coaxial Cables

- 2.2. Twinaxial Cables

- 2.3. Others

High Speed Interface Cables Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

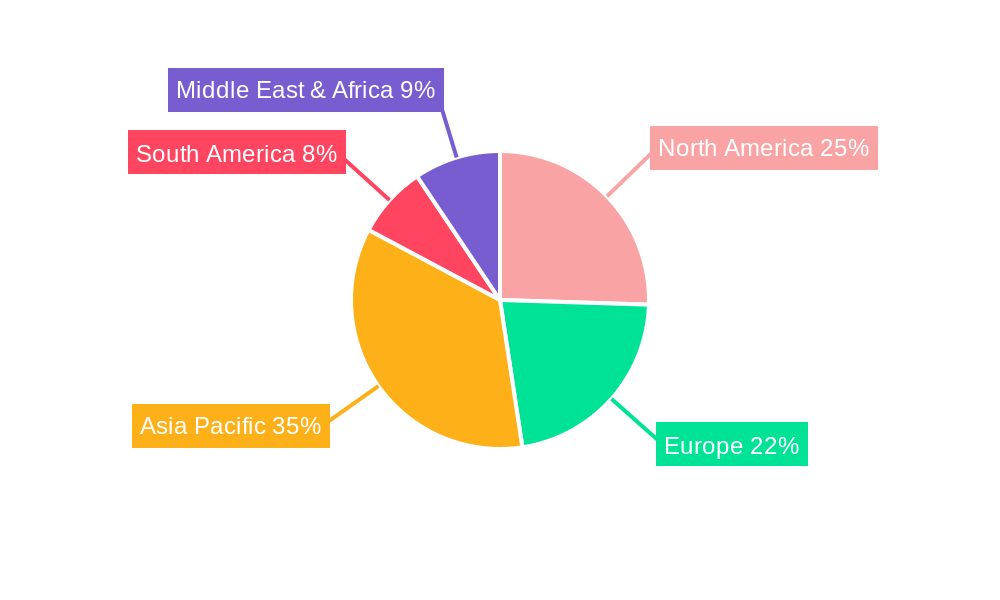

High Speed Interface Cables Regional Market Share

Geographic Coverage of High Speed Interface Cables

High Speed Interface Cables REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Automotive

- 5.1.2. Medical

- 5.1.3. Instrumentation

- 5.1.4. Wireless Infrastructure

- 5.1.5. Aerospace

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Coaxial Cables

- 5.2.2. Twinaxial Cables

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global High Speed Interface Cables Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Automotive

- 6.1.2. Medical

- 6.1.3. Instrumentation

- 6.1.4. Wireless Infrastructure

- 6.1.5. Aerospace

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Coaxial Cables

- 6.2.2. Twinaxial Cables

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America High Speed Interface Cables Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Automotive

- 7.1.2. Medical

- 7.1.3. Instrumentation

- 7.1.4. Wireless Infrastructure

- 7.1.5. Aerospace

- 7.1.6. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Coaxial Cables

- 7.2.2. Twinaxial Cables

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America High Speed Interface Cables Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Automotive

- 8.1.2. Medical

- 8.1.3. Instrumentation

- 8.1.4. Wireless Infrastructure

- 8.1.5. Aerospace

- 8.1.6. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Coaxial Cables

- 8.2.2. Twinaxial Cables

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe High Speed Interface Cables Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Automotive

- 9.1.2. Medical

- 9.1.3. Instrumentation

- 9.1.4. Wireless Infrastructure

- 9.1.5. Aerospace

- 9.1.6. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Coaxial Cables

- 9.2.2. Twinaxial Cables

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa High Speed Interface Cables Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Automotive

- 10.1.2. Medical

- 10.1.3. Instrumentation

- 10.1.4. Wireless Infrastructure

- 10.1.5. Aerospace

- 10.1.6. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Coaxial Cables

- 10.2.2. Twinaxial Cables

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific High Speed Interface Cables Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Automotive

- 11.1.2. Medical

- 11.1.3. Instrumentation

- 11.1.4. Wireless Infrastructure

- 11.1.5. Aerospace

- 11.1.6. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Coaxial Cables

- 11.2.2. Twinaxial Cables

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Nissei Electric

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Oki Electric

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 TE Connectivity

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Amphenol

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Fujikura

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Schneider Electric

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Hirakawa Hewtech

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Samtec Electronics

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Sumitomo Electric

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Glenair

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Extron

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 CommScope

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Proterial

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Data Device Corporation

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Kingsignal Technology

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Leoni AG

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Tatsuta Tachii Electric Cable

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Junkosha

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 JPS Interoperability

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 Terasic

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 Shenyu Communication Technology

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.22 microHAM

- 12.1.22.1. Company Overview

- 12.1.22.2. Products

- 12.1.22.3. Company Financials

- 12.1.22.4. SWOT Analysis

- 12.1.1 Nissei Electric

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global High Speed Interface Cables Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America High Speed Interface Cables Revenue (million), by Application 2025 & 2033

- Figure 3: North America High Speed Interface Cables Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America High Speed Interface Cables Revenue (million), by Types 2025 & 2033

- Figure 5: North America High Speed Interface Cables Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America High Speed Interface Cables Revenue (million), by Country 2025 & 2033

- Figure 7: North America High Speed Interface Cables Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America High Speed Interface Cables Revenue (million), by Application 2025 & 2033

- Figure 9: South America High Speed Interface Cables Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America High Speed Interface Cables Revenue (million), by Types 2025 & 2033

- Figure 11: South America High Speed Interface Cables Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America High Speed Interface Cables Revenue (million), by Country 2025 & 2033

- Figure 13: South America High Speed Interface Cables Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe High Speed Interface Cables Revenue (million), by Application 2025 & 2033

- Figure 15: Europe High Speed Interface Cables Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe High Speed Interface Cables Revenue (million), by Types 2025 & 2033

- Figure 17: Europe High Speed Interface Cables Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe High Speed Interface Cables Revenue (million), by Country 2025 & 2033

- Figure 19: Europe High Speed Interface Cables Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa High Speed Interface Cables Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa High Speed Interface Cables Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa High Speed Interface Cables Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa High Speed Interface Cables Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa High Speed Interface Cables Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa High Speed Interface Cables Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific High Speed Interface Cables Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific High Speed Interface Cables Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific High Speed Interface Cables Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific High Speed Interface Cables Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific High Speed Interface Cables Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific High Speed Interface Cables Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global High Speed Interface Cables Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global High Speed Interface Cables Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global High Speed Interface Cables Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global High Speed Interface Cables Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global High Speed Interface Cables Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global High Speed Interface Cables Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global High Speed Interface Cables Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global High Speed Interface Cables Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global High Speed Interface Cables Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global High Speed Interface Cables Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global High Speed Interface Cables Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global High Speed Interface Cables Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global High Speed Interface Cables Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global High Speed Interface Cables Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global High Speed Interface Cables Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global High Speed Interface Cables Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global High Speed Interface Cables Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global High Speed Interface Cables Revenue million Forecast, by Country 2020 & 2033

- Table 40: China High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific High Speed Interface Cables Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the High Speed Interface Cables?

The projected CAGR is approximately 7.7%.

2. Which companies are prominent players in the High Speed Interface Cables?

Key companies in the market include Nissei Electric, Oki Electric, TE Connectivity, Amphenol, Fujikura, Schneider Electric, Hirakawa Hewtech, Samtec Electronics, Sumitomo Electric, Glenair, Extron, CommScope, Proterial, Data Device Corporation, Kingsignal Technology, Leoni AG, Tatsuta Tachii Electric Cable, Junkosha, JPS Interoperability, Terasic, Shenyu Communication Technology, microHAM.

3. What are the main segments of the High Speed Interface Cables?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 118338.7 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "High Speed Interface Cables," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the High Speed Interface Cables report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the High Speed Interface Cables?

To stay informed about further developments, trends, and reports in the High Speed Interface Cables, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence