Key Insights

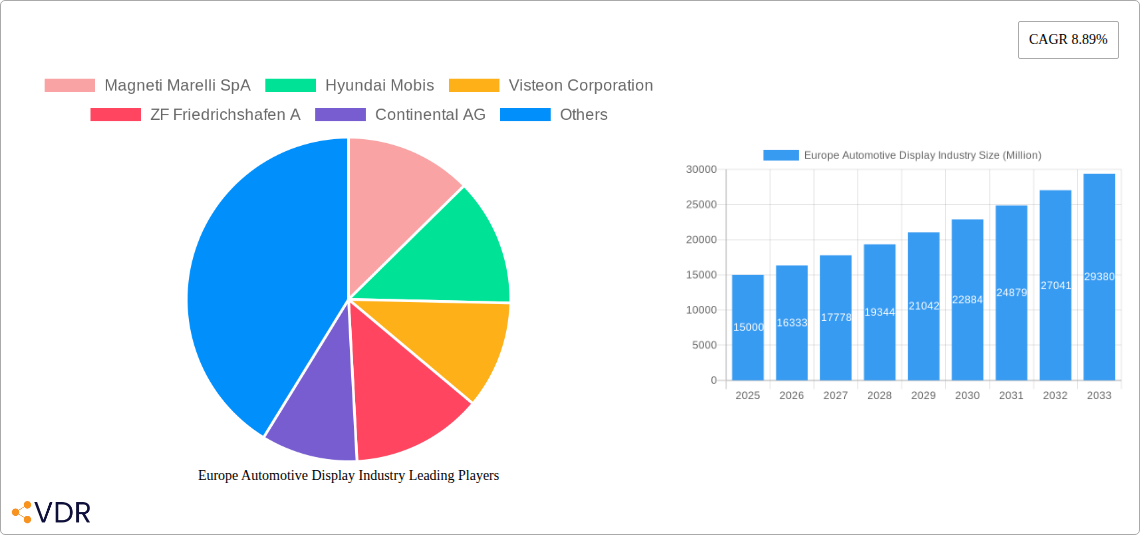

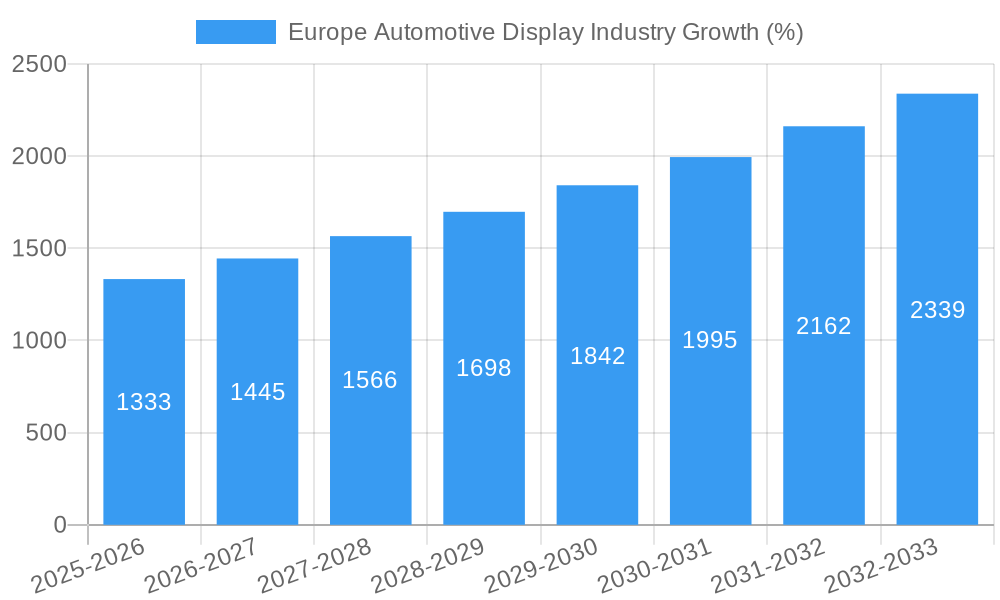

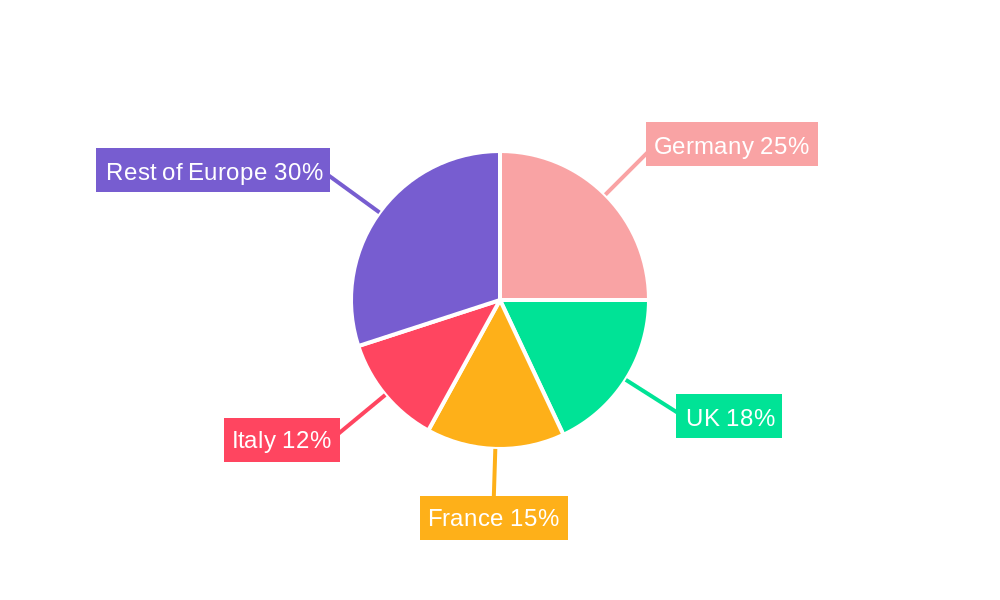

The European automotive display market is experiencing robust growth, driven by increasing demand for advanced driver-assistance systems (ADAS), infotainment features, and enhanced user experience in vehicles. The market, estimated at €XX million in 2025, is projected to exhibit a compound annual growth rate (CAGR) of 8.89% from 2025 to 2033, reaching a significant market value by the end of the forecast period. This growth is fueled by several key factors. The rising adoption of LCD and OLED technologies, offering higher resolution, better color accuracy, and improved energy efficiency, is a primary driver. Furthermore, the increasing integration of larger center stack displays, instrument cluster displays, and heads-up displays (HUDs) enhances the in-car experience, boosting consumer demand. The shift towards electric vehicles (EVs) also contributes positively, as these vehicles often feature more sophisticated and larger displays. Segmentation analysis reveals a strong presence across various vehicle types, with passenger cars contributing a larger share, followed by commercial vehicles. OEM sales currently dominate the market, though the aftermarket segment holds potential for future expansion as drivers seek upgrades and enhanced functionalities. Germany, the UK, France, and Italy are key markets within Europe, reflecting high vehicle production and a strong consumer preference for technologically advanced vehicles.

The competitive landscape is highly consolidated, with major players like Magneti Marelli, Hyundai Mobis, Visteon, ZF Friedrichshafen, Continental, Robert Bosch, MTA, JDI Europe, Denso, and LG Electronics vying for market share. These companies are investing heavily in R&D to develop innovative display technologies and meet the evolving needs of the automotive industry. While the market faces challenges such as supply chain disruptions and fluctuating raw material costs, the overall positive growth trajectory is expected to continue, driven by the overarching trends of technological advancement and increased consumer demand for sophisticated automotive displays. The increasing focus on safety features and autonomous driving functionalities will further solidify the demand for advanced display solutions in the coming years. Therefore, the European automotive display market presents a lucrative opportunity for established players and new entrants alike.

Europe Automotive Display Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Europe Automotive Display industry, covering market dynamics, growth trends, dominant segments, and key players. The study period spans from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033. The report leverages extensive primary and secondary research to deliver actionable insights for industry professionals, investors, and strategic decision-makers. The total market size is predicted to reach xx Million units by 2033.

Europe Automotive Display Industry Market Dynamics & Structure

The European automotive display market is characterized by intense competition, rapid technological advancements, and evolving regulatory landscapes. Market concentration is moderate, with several key players holding significant market share, while smaller, specialized firms focus on niche segments. Technological innovation, driven by the demand for enhanced driver assistance systems (ADAS) and infotainment features, is a key driver. Stringent safety and emission regulations within the EU are shaping the adoption of advanced display technologies. The increasing prevalence of electric and autonomous vehicles fuels the growth of larger, higher-resolution displays. Significant M&A activity has been observed in recent years, with larger players acquiring smaller companies to expand their product portfolios and technological capabilities.

- Market Concentration: Moderate, with top 5 players holding approximately xx% market share in 2025.

- Technological Innovation: Focus on OLED, mini-LED, and micro-LED technologies, along with augmented reality (AR) and head-up display (HUD) integration.

- Regulatory Framework: Stringent EU regulations on vehicle safety and emissions are driving demand for advanced driver-assistance systems (ADAS).

- Competitive Substitutes: Limited direct substitutes, but alternative infotainment solutions may impact market growth.

- End-User Demographics: Growing demand from premium vehicle segments and increasing adoption in commercial vehicles.

- M&A Trends: Consolidation expected to continue, driven by the need for scale and technological expertise. xx M&A deals recorded between 2019 and 2024.

Europe Automotive Display Industry Growth Trends & Insights

The European automotive display market exhibits a robust growth trajectory, driven by increasing vehicle production, rising consumer demand for advanced features, and the proliferation of connected car technologies. The market size experienced substantial growth during the historical period (2019-2024), and this upward trend is projected to continue throughout the forecast period (2025-2033). The adoption rate of advanced display technologies like OLED and HUD is steadily increasing, fueled by technological advancements and falling prices. Consumer preferences are shifting towards larger, higher-resolution displays with enhanced functionalities. The market is expected to achieve a Compound Annual Growth Rate (CAGR) of xx% during the forecast period.

Dominant Regions, Countries, or Segments in Europe Automotive Display Industry

Germany holds the largest market share in the European automotive display industry, followed by the United Kingdom and France. This dominance is attributable to the strong presence of major automotive manufacturers and a well-established automotive supply chain. The passenger car segment dominates the overall market due to higher vehicle production volumes compared to commercial vehicles. Within technology types, LCD displays currently hold a significant market share, but OLED is rapidly gaining traction, especially in premium vehicle segments. The center stack display is the leading product type, followed by instrument cluster displays. The OEM sales channel is the primary driver of market growth, with a significantly larger market share compared to the aftermarket.

- Leading Region: Germany

- Key Drivers in Germany: Strong automotive manufacturing base, presence of key display suppliers, and supportive government policies.

- Passenger Car Segment: Largest segment, driven by high vehicle production and increasing demand for advanced features.

- LCD Technology: Currently dominant, but OLED is witnessing rapid growth.

- Center Stack Display: Largest product type segment, due to increasing complexity of in-car infotainment systems.

- OEM Sales: Primary sales channel, due to its role in new vehicle production.

Europe Automotive Display Industry Product Landscape

The automotive display market showcases continuous product innovation, focusing on improved image quality, enhanced brightness, wider viewing angles, and increased durability. Advancements in display technology are leading to larger screen sizes, higher resolutions, and the integration of advanced features such as touchscreens, haptic feedback, and curved displays. Unique selling propositions include superior color reproduction, faster response times, and reduced power consumption. The incorporation of AR and HUD technology is transforming the driver experience, providing enhanced safety and convenience. Mini-LED and Micro-LED technologies are emerging as key contenders, promising significant improvements in brightness, contrast, and energy efficiency.

Key Drivers, Barriers & Challenges in Europe Automotive Display Industry

Key Drivers:

- The rising demand for advanced driver-assistance systems (ADAS) and infotainment features is a major driver of market growth.

- The increasing adoption of electric and autonomous vehicles is fueling the demand for larger and more sophisticated displays.

- Favorable government policies and initiatives promoting technological advancement in the automotive sector are also contributing to market growth.

Challenges:

- The increasing complexity of automotive displays increases manufacturing costs and poses technical challenges.

- Supply chain disruptions and raw material shortages can impact production volumes.

- Intense competition among display manufacturers puts pressure on prices and profit margins.

Emerging Opportunities in Europe Automotive Display Industry

- Growing demand for customized displays tailored to specific vehicle models and consumer preferences.

- Expanding applications of automotive displays beyond infotainment and driver assistance systems into other areas such as passenger entertainment and vehicle-to-infrastructure communication.

- Emerging markets for transparent OLED displays and flexible displays offer significant growth potential.

Growth Accelerators in the Europe Automotive Display Industry Industry

Technological breakthroughs in display technologies, such as mini-LED and Micro-LED, are key catalysts driving long-term growth. Strategic partnerships between display manufacturers and automotive OEMs foster innovation and accelerate product development. Expansion into new geographic markets and the development of innovative display applications are also fueling market growth.

Key Players Shaping the Europe Automotive Display Industry Market

- Magneti Marelli SpA

- Hyundai Mobis

- Visteon Corporation

- ZF Friedrichshafen A

- Continental AG

- Robert Bosch GmbH

- MTA SpA

- JDI Europe GmbH

- DENSO Corporation

- LG Electronics

Notable Milestones in Europe Automotive Display Industry Sector

- 2020: Launch of several new vehicle models featuring advanced display technologies, particularly HUD and curved displays.

- 2021: Significant investments by major players in the development of OLED and mini-LED display technologies.

- 2022: Several mergers and acquisitions in the automotive display supply chain.

- 2023: Introduction of new regulatory standards for automotive display safety and performance.

In-Depth Europe Automotive Display Industry Market Outlook

The European automotive display market is poised for continued robust growth, driven by technological innovations, increasing vehicle production, and the growing demand for advanced features. Strategic partnerships and market expansion strategies are likely to enhance the growth potential further. The emergence of new display technologies such as Micro-LED and the growing importance of software and services will significantly influence the market landscape. The market offers lucrative opportunities for companies that can innovate, adapt to the changing regulatory environment, and offer value-added solutions to the automotive OEMs.

Europe Automotive Display Industry Segmentation

-

1. Vehicle Type

- 1.1. Passenger Cars

- 1.2. Commercial Vehicles

-

2. Technology Type

- 2.1. LCD

- 2.2. OLED

-

3. Product Type

- 3.1. Center Stack Display

- 3.2. Instrument Cluster Display

- 3.3. Heads-up Display

- 3.4. Other Product Types

-

4. Sales Type

- 4.1. OEM

- 4.2. Aftermarket

Europe Automotive Display Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Automotive Display Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 8.89% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increase in Sales of Passenger Cars

- 3.3. Market Restrains

- 3.3.1. Failure in Garage Equipment may Result in Downtime of the Repair Work

- 3.4. Market Trends

- 3.4.1. Autonomous and Electric Vehicles Driving the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Automotive Display Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Passenger Cars

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Technology Type

- 5.2.1. LCD

- 5.2.2. OLED

- 5.3. Market Analysis, Insights and Forecast - by Product Type

- 5.3.1. Center Stack Display

- 5.3.2. Instrument Cluster Display

- 5.3.3. Heads-up Display

- 5.3.4. Other Product Types

- 5.4. Market Analysis, Insights and Forecast - by Sales Type

- 5.4.1. OEM

- 5.4.2. Aftermarket

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. Germany Europe Automotive Display Industry Analysis, Insights and Forecast, 2019-2031

- 7. France Europe Automotive Display Industry Analysis, Insights and Forecast, 2019-2031

- 8. Italy Europe Automotive Display Industry Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Europe Automotive Display Industry Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Europe Automotive Display Industry Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Europe Automotive Display Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Europe Automotive Display Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Magneti Marelli SpA

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Hyundai Mobis

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Visteon Corporation

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 ZF Friedrichshafen A

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Continental AG

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Robert Bosch GmbH

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 MTA SpA

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 JDI Europe GmbH

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 DENSO Corporation

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 LG Electronics

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.1 Magneti Marelli SpA

List of Figures

- Figure 1: Europe Automotive Display Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Automotive Display Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe Automotive Display Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Automotive Display Industry Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 3: Europe Automotive Display Industry Revenue Million Forecast, by Technology Type 2019 & 2032

- Table 4: Europe Automotive Display Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 5: Europe Automotive Display Industry Revenue Million Forecast, by Sales Type 2019 & 2032

- Table 6: Europe Automotive Display Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 7: Europe Automotive Display Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: Germany Europe Automotive Display Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: France Europe Automotive Display Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Italy Europe Automotive Display Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: United Kingdom Europe Automotive Display Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Netherlands Europe Automotive Display Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Sweden Europe Automotive Display Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Rest of Europe Europe Automotive Display Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Europe Automotive Display Industry Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 16: Europe Automotive Display Industry Revenue Million Forecast, by Technology Type 2019 & 2032

- Table 17: Europe Automotive Display Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 18: Europe Automotive Display Industry Revenue Million Forecast, by Sales Type 2019 & 2032

- Table 19: Europe Automotive Display Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Europe Automotive Display Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Germany Europe Automotive Display Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: France Europe Automotive Display Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Italy Europe Automotive Display Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Spain Europe Automotive Display Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Netherlands Europe Automotive Display Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Belgium Europe Automotive Display Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Sweden Europe Automotive Display Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Norway Europe Automotive Display Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Poland Europe Automotive Display Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Denmark Europe Automotive Display Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Automotive Display Industry?

The projected CAGR is approximately 8.89%.

2. Which companies are prominent players in the Europe Automotive Display Industry?

Key companies in the market include Magneti Marelli SpA, Hyundai Mobis, Visteon Corporation, ZF Friedrichshafen A, Continental AG, Robert Bosch GmbH, MTA SpA, JDI Europe GmbH, DENSO Corporation, LG Electronics.

3. What are the main segments of the Europe Automotive Display Industry?

The market segments include Vehicle Type, Technology Type, Product Type, Sales Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increase in Sales of Passenger Cars.

6. What are the notable trends driving market growth?

Autonomous and Electric Vehicles Driving the Market.

7. Are there any restraints impacting market growth?

Failure in Garage Equipment may Result in Downtime of the Repair Work.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Automotive Display Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Automotive Display Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Automotive Display Industry?

To stay informed about further developments, trends, and reports in the Europe Automotive Display Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence