Key Insights

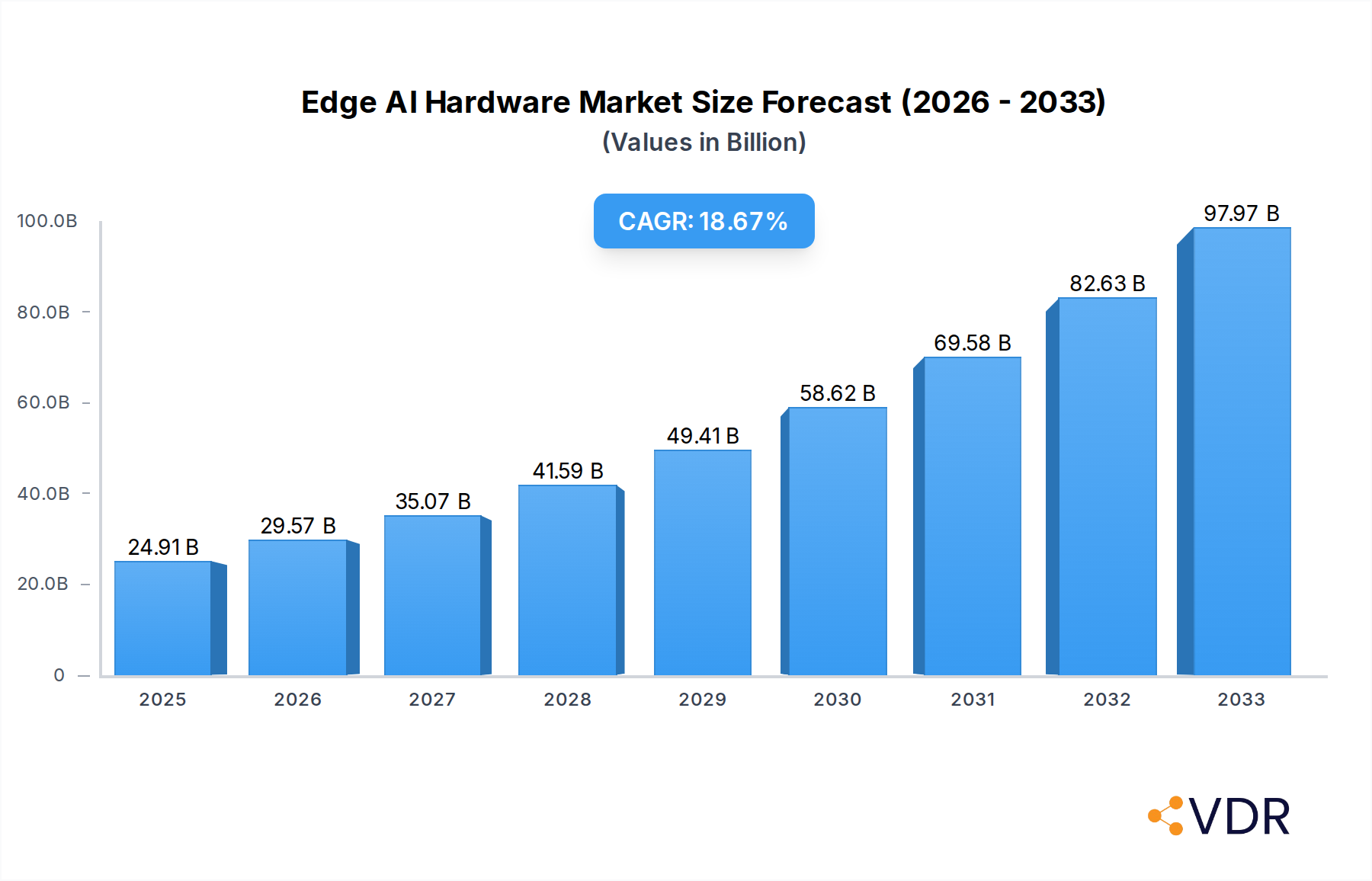

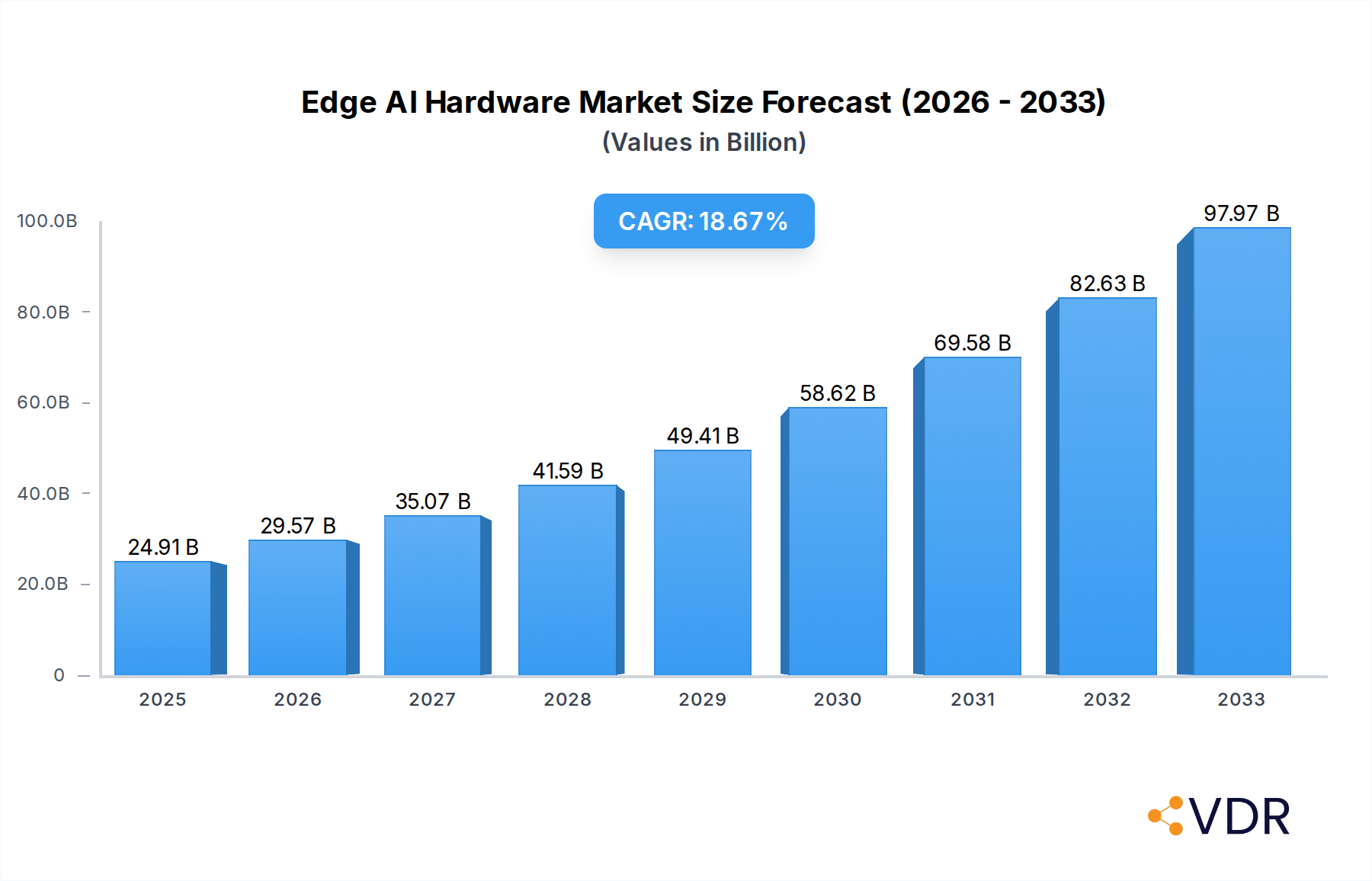

The Edge AI Hardware Market is poised for remarkable expansion, projecting a market size of $24.91 billion in 2025 and demonstrating a robust Compound Annual Growth Rate (CAGR) of 21.7% throughout the forecast period (2025-2033). This explosive growth is primarily fueled by the escalating demand for real-time data processing and intelligent decision-making capabilities directly at the source, eliminating latency and enhancing privacy. Key drivers include the proliferation of connected devices, the increasing adoption of Artificial Intelligence (AI) across diverse industries, and the need for localized processing power to handle massive data volumes generated by IoT ecosystems. The market is experiencing a significant shift towards more efficient and specialized hardware solutions capable of supporting complex AI algorithms at the edge, ranging from sophisticated processors like GPUs and FPGAs to custom ASICs.

Edge AI Hardware Market Market Size (In Billion)

The competitive landscape is characterized by intense innovation and strategic alliances as major technology players vie for market dominance. Consumer electronics, automotive, and manufacturing sectors are leading the charge in adopting edge AI hardware, leveraging its capabilities for applications such as autonomous driving, smart manufacturing, advanced surveillance, and personalized user experiences. While the market benefits from advancements in AI algorithms and the decreasing cost of hardware, challenges such as power consumption, thermal management, and the development of standardized edge AI architectures need to be addressed. Nevertheless, the inherent advantages of edge AI, including improved security, reduced bandwidth requirements, and enhanced operational efficiency, ensure its continued and accelerated integration into virtually every aspect of modern technology.

Edge AI Hardware Market Company Market Share

Edge AI Hardware Market: Unlocking Decentralized Intelligence

This comprehensive report, Edge AI Hardware Market, provides an in-depth analysis of the global market for hardware designed to enable artificial intelligence processing at the network edge. Explore the burgeoning demand for low-latency, high-performance AI solutions across diverse industries, driven by the exponential growth of connected devices and the need for real-time data analysis. The study meticulously examines the market's evolution from its historical roots (2019-2024) through to a detailed forecast period (2025-2033), with 2025 serving as the base and estimated year. Discover critical insights into market dynamics, growth trends, regional dominance, product landscapes, key players, and emerging opportunities that are shaping the future of decentralized AI.

Edge AI Hardware Market Market Dynamics & Structure

The Edge AI hardware market is characterized by a dynamic and rapidly evolving structure, driven by intense technological innovation and increasing adoption across a multitude of end-user industries. Market concentration is moderate, with a significant presence of established semiconductor giants alongside nimble startups focusing on specialized AI accelerators. The primary driver of innovation stems from the relentless pursuit of enhanced performance, reduced power consumption, and miniaturization of AI processing capabilities for edge devices. Regulatory frameworks are gradually taking shape, focusing on data privacy and security standards for AI deployments. Competitive product substitutes are emerging, particularly in the form of highly specialized ASICs designed for specific AI inference tasks, challenging the dominance of more general-purpose processors like GPUs and CPUs. End-user demographics are broadening, with a significant surge in demand from the automotive, manufacturing, and consumer electronics sectors. Mergers and acquisitions (M&A) trends are prevalent as larger companies seek to acquire cutting-edge AI hardware technologies and talent, thereby consolidating market share and expanding their portfolios.

- Market Concentration: Moderate, with a mix of large integrated device manufacturers and specialized AI chip designers.

- Technological Innovation Drivers: Demand for real-time data processing, low latency, power efficiency, and AI inference acceleration.

- Regulatory Frameworks: Emerging focus on data privacy, AI ethics, and cybersecurity standards.

- Competitive Product Substitutes: Increasing prevalence of ASICs tailored for specific AI workloads, alongside ongoing advancements in FPGAs.

- End-User Demographics: Diversifying rapidly, with strong growth in automotive, industrial IoT, and smart devices.

- M&A Trends: Active consolidation to acquire intellectual property and market presence, with approximately 15-20 significant M&A deals projected annually from 2025 onwards.

Edge AI Hardware Market Growth Trends & Insights

The Edge AI hardware market is on a trajectory of robust growth, propelled by the fundamental shift towards decentralized intelligence. This market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 25.7% between 2025 and 2033, a testament to the accelerating adoption of AI capabilities at the network edge. The market size, estimated at USD 15.2 billion in 2025, is expected to surge to USD 78.5 billion by 2033. This expansion is fueled by the increasing need for real-time data analysis in applications ranging from autonomous vehicles to smart cities and sophisticated industrial automation. Technological disruptions, such as the development of neuromorphic computing and highly efficient AI accelerators, are playing a pivotal role in making edge AI more accessible and powerful. Consumer behavior is also shifting, with a growing expectation for intelligent, responsive devices that offer personalized experiences and enhanced functionalities without constant cloud connectivity. This paradigm shift necessitates more powerful and specialized hardware integrated directly into end-user devices.

The adoption rates for edge AI hardware are experiencing a significant uplift, particularly in sectors demanding immediate decision-making and reduced reliance on network bandwidth. For instance, the automotive sector's integration of advanced driver-assistance systems (ADAS) and the increasing complexity of autonomous driving algorithms are major contributors to this trend. Similarly, the manufacturing industry is leveraging edge AI for predictive maintenance, quality control, and optimizing production lines, leading to substantial operational efficiencies. The consumer electronics segment is also a key growth engine, with smart home devices, wearables, and advanced mobile computing increasingly incorporating edge AI capabilities for features like on-device voice recognition, intelligent image processing, and personalized user experiences. The development of specialized processors, including AI-specific ASICs and more efficient GPUs and FPGAs, is directly supporting this demand by offering tailored solutions for various AI workloads.

Furthermore, the growth in the edge AI hardware market is intrinsically linked to the proliferation of the Internet of Things (IoT). As the number of connected devices continues to explode, the volume of data generated at the edge also escalates, making cloud-based processing increasingly impractical and expensive. Edge AI hardware provides the necessary computational power to process this data locally, enabling faster insights, reduced latency, and enhanced privacy. The evolution of AI algorithms themselves, becoming more sophisticated and capable of running on less powerful hardware, further democratizes edge AI adoption. This symbiotic relationship between hardware innovation and algorithmic advancements is creating a virtuous cycle of growth for the entire edge AI ecosystem. The increasing maturity of edge computing infrastructure, including specialized data centers and network capabilities, also underpins this growth by providing the necessary support for distributed AI deployments.

Dominant Regions, Countries, or Segments in Edge AI Hardware Market

The Edge AI hardware market is experiencing robust growth across various segments, with the Automotive end-user industry emerging as a dominant driver, significantly influencing regional and segment-specific market expansion. Within the processor segment, ASICs are poised for substantial growth due to their specialized, high-performance capabilities tailored for AI inference tasks, directly benefiting applications like autonomous driving. The Automotive sector's insatiable demand for AI-powered features, including advanced driver-assistance systems (ADAS), in-cabin intelligent systems, and eventually fully autonomous driving, is a primary catalyst. This necessitates on-device processing for critical safety and navigation functions, where latency is paramount and cloud dependency is a significant risk.

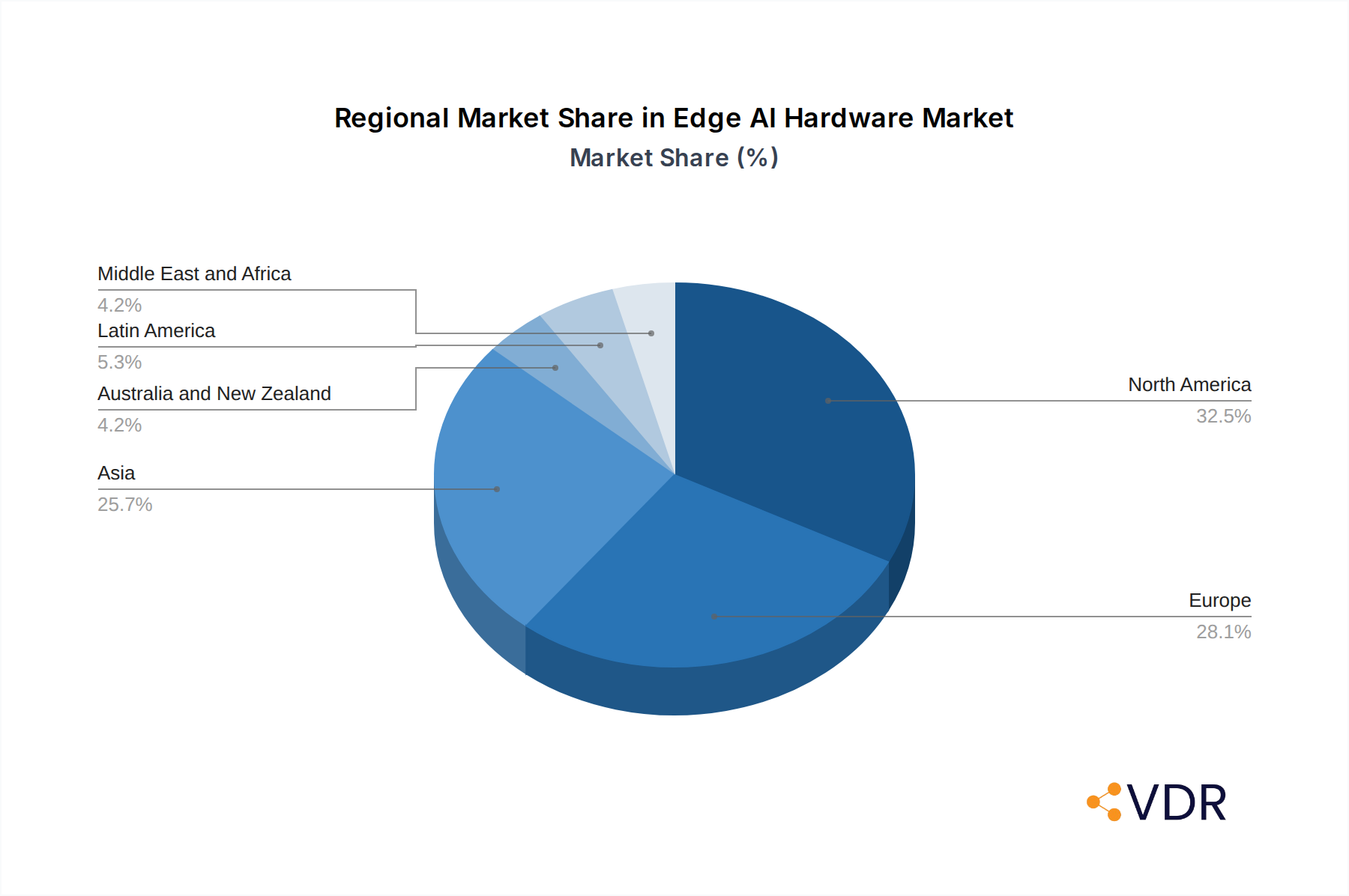

North America, particularly the United States, stands as a leading region, driven by significant investments in AI research and development, a strong presence of major technology companies, and a high adoption rate of advanced technologies across various sectors. The robust automotive industry in the US, coupled with the nation's leadership in AI innovation, positions it as a key market. Economic policies that encourage technological advancement and robust venture capital funding for AI startups further bolster this dominance. Infrastructure development for 5G connectivity is also playing a crucial role in enabling more sophisticated edge AI deployments, particularly in the automotive and industrial sectors.

In terms of device segments, Cameras and Robots are witnessing accelerated adoption of edge AI hardware. Smart cameras equipped with AI capabilities are transforming surveillance, retail analytics, and industrial quality control by enabling real-time object detection, facial recognition, and anomaly identification. Similarly, the increasing automation in manufacturing, logistics, and healthcare is driving demand for AI-enabled robots capable of complex decision-making and task execution at the edge. The market share for ASICs within the processor segment is projected to grow considerably, driven by their ability to offer optimized power and performance for specific AI workloads, a critical requirement for edge devices with limited power budgets. The development of advanced AI algorithms and the need for efficient deployment are pushing manufacturers towards custom silicon solutions, further solidifying the dominance of ASICs in high-demand applications.

The growth potential within the automotive segment is immense, with ongoing advancements in autonomous driving technology requiring increasingly sophisticated edge AI hardware. This includes powerful processors capable of processing massive amounts of sensor data in real-time, low-power AI chips for efficient operation, and robust security features to protect sensitive data. Government initiatives promoting the adoption of electric and autonomous vehicles also indirectly fuel the demand for edge AI hardware. The convergence of automotive, transportation, and the broader industrial automation sectors presents a significant opportunity for edge AI hardware manufacturers to deliver integrated and scalable solutions.

Edge AI Hardware Market Product Landscape

The Edge AI hardware market is characterized by a diverse and rapidly evolving product landscape, driven by relentless innovation aimed at optimizing performance, power efficiency, and cost-effectiveness for edge deployments. Key product innovations include the development of specialized AI accelerators such as Neural Processing Units (NPUs) and Tensor Processing Units (TPUs) designed for efficient inference. These processors often leverage advanced architectures like convolutional neural networks (CNNs) and recurrent neural networks (RNNs) to accelerate AI computations. Field-Programmable Gate Arrays (FPGAs) are gaining traction due to their flexibility and reconfigurability, allowing for adaptation to evolving AI algorithms. Furthermore, advancements in miniaturization and low-power design are enabling the integration of powerful AI capabilities into increasingly smaller and more power-constrained devices.

Key Drivers, Barriers & Challenges in Edge AI Hardware Market

The Edge AI hardware market is propelled by several key drivers, including the escalating demand for real-time data processing and low-latency decision-making across industries like automotive and manufacturing. The proliferation of IoT devices generates vast amounts of data, making edge processing essential for efficiency and cost-effectiveness. Technological advancements in AI algorithms and specialized hardware, such as ASICs and NPUs, are enabling more powerful and efficient AI deployments at the edge. Government initiatives and investments in smart city projects and digital transformation further accelerate market growth.

However, the market faces significant barriers and challenges. The high cost of developing and manufacturing advanced AI chips can be a restraint, especially for smaller companies. Supply chain complexities and the availability of raw materials, particularly for advanced semiconductor manufacturing, pose ongoing concerns. Regulatory hurdles related to data privacy and security standards can also impact adoption rates. Intense competition from established players and emerging startups creates pressure on pricing and margins. Furthermore, the need for specialized expertise in AI hardware design and integration can be a challenge for some end-user industries.

Emerging Opportunities in Edge AI Hardware Market

Emerging opportunities in the Edge AI hardware market are abundant and span across various innovative applications and untapped sectors. The increasing demand for AI-powered solutions in healthcare, particularly for remote patient monitoring, diagnostics, and personalized treatment, presents a significant growth avenue. The expansion of smart agriculture, leveraging AI for crop monitoring, yield optimization, and resource management, is another burgeoning area. Furthermore, the development of edge AI for augmented reality (AR) and virtual reality (VR) applications, enabling more immersive and interactive experiences without relying on cloud processing, holds immense potential. The growing focus on sustainability and energy efficiency is also driving demand for low-power edge AI hardware solutions.

Growth Accelerators in the Edge AI Hardware Market Industry

Several factors are acting as significant growth accelerators for the Edge AI hardware market. Continuous technological breakthroughs in semiconductor manufacturing, including advancements in FinFET technology and new materials, are enabling the creation of more powerful and energy-efficient AI chips. Strategic partnerships between hardware manufacturers, AI software developers, and end-user industry leaders are crucial for co-developing optimized solutions and fostering wider adoption. Market expansion strategies, such as entering emerging economies with rapidly digitizing infrastructures, are also key to driving long-term growth. The increasing availability of open-source AI frameworks and development tools further lowers the barrier to entry for developing edge AI applications.

Key Players Shaping the Edge AI Hardware Market Market

- Baidu Inc

- Samsung Group

- Denso Corporation

- Xilinx Inc

- Alibaba Group Holding Limited

- Alphabet Inc

- Continental AG

- Qualcomm Incorporated

- Advanced Micro Devices Inc

- Amazon com Inc

- Robert Bosch GmbH

- KALRAY Corporation

- Huawei Technologies Co Ltd

- MediaTek Inc

- Nvidia Corporation

- Apple Inc

- Intel Corporation

Notable Milestones in Edge AI Hardware Market Sector

- November 2022: Network solutions provider Lumen Technologies began expanding its portfolio of Edge Computing Solutions into the Asia-Pacific Region, including its Edge Bare Metal pay-as-you-go hardware solution for servers, taking advantage of sites in Singapore and Japan. This expansion aims to bring enhanced connectivity and localized processing power closer to end-users in a key growth region.

- October 2022: Kneron bagged USD 50 million in funding for next-gen AI hardware solutions. The company plans to use the funds to accelerate its research and development to produce next-gen AI inference modules. Kneron anticipates increased adoption of on-device edge AI technology in the future. This involves placing AI computing power onto devices that include hardware rather than within cloud software, signaling a strong trend towards dedicated edge AI processors.

- August 2022: Stanford University engineers created a more efficient and flexible AI chip suited to power AI in tiny edge devices. The engineers' chip, called NeuRRAM, is a novel resistive random-access memory (RRAM) chip that innovates how current chips process and store data. This breakthrough highlights the ongoing pursuit of novel architectures for ultra-low-power and highly integrated edge AI solutions.

In-Depth Edge AI Hardware Market Market Outlook

The future outlook for the Edge AI hardware market is exceptionally bright, fueled by the relentless drive towards decentralization and intelligence at the network's edge. Growth accelerators such as continued advancements in AI algorithms, the exponential rise of IoT devices, and the critical need for real-time data processing are creating a sustained demand for specialized hardware. The increasing adoption of 5G technology further empowers edge AI by providing the necessary bandwidth and low latency for more sophisticated deployments. Strategic partnerships between technology giants and specialized chip manufacturers will continue to drive innovation and market penetration. As industries across the spectrum, from automotive and healthcare to manufacturing and consumer electronics, increasingly integrate AI into their operations and products, the demand for powerful, efficient, and cost-effective edge AI hardware solutions is set to witness unprecedented growth, solidifying its position as a cornerstone of the future digital economy.

Edge AI Hardware Market Segmentation

-

1. Processor

- 1.1. CPU

- 1.2. GPU

- 1.3. FPGA

- 1.4. ASICs

-

2. Device

- 2.1. Smartphones

- 2.2. Cameras

- 2.3. Robots

- 2.4. Wearables

- 2.5. Smart Speaker

- 2.6. Other Devices

-

3. End-User Industry

- 3.1. Government

- 3.2. Real Estate

- 3.3. Consumer Electronics

- 3.4. Automotive

- 3.5. Transportation

- 3.6. Healthcare

- 3.7. Manufacturing

- 3.8. Others

Edge AI Hardware Market Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Edge AI Hardware Market Regional Market Share

Geographic Coverage of Edge AI Hardware Market

Edge AI Hardware Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 21.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Processor

- 5.1.1. CPU

- 5.1.2. GPU

- 5.1.3. FPGA

- 5.1.4. ASICs

- 5.2. Market Analysis, Insights and Forecast - by Device

- 5.2.1. Smartphones

- 5.2.2. Cameras

- 5.2.3. Robots

- 5.2.4. Wearables

- 5.2.5. Smart Speaker

- 5.2.6. Other Devices

- 5.3. Market Analysis, Insights and Forecast - by End-User Industry

- 5.3.1. Government

- 5.3.2. Real Estate

- 5.3.3. Consumer Electronics

- 5.3.4. Automotive

- 5.3.5. Transportation

- 5.3.6. Healthcare

- 5.3.7. Manufacturing

- 5.3.8. Others

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia

- 5.4.4. Australia and New Zealand

- 5.4.5. Latin America

- 5.4.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Processor

- 6. Global Edge AI Hardware Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Processor

- 6.1.1. CPU

- 6.1.2. GPU

- 6.1.3. FPGA

- 6.1.4. ASICs

- 6.2. Market Analysis, Insights and Forecast - by Device

- 6.2.1. Smartphones

- 6.2.2. Cameras

- 6.2.3. Robots

- 6.2.4. Wearables

- 6.2.5. Smart Speaker

- 6.2.6. Other Devices

- 6.3. Market Analysis, Insights and Forecast - by End-User Industry

- 6.3.1. Government

- 6.3.2. Real Estate

- 6.3.3. Consumer Electronics

- 6.3.4. Automotive

- 6.3.5. Transportation

- 6.3.6. Healthcare

- 6.3.7. Manufacturing

- 6.3.8. Others

- 6.1. Market Analysis, Insights and Forecast - by Processor

- 7. North America Edge AI Hardware Market Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Processor

- 7.1.1. CPU

- 7.1.2. GPU

- 7.1.3. FPGA

- 7.1.4. ASICs

- 7.2. Market Analysis, Insights and Forecast - by Device

- 7.2.1. Smartphones

- 7.2.2. Cameras

- 7.2.3. Robots

- 7.2.4. Wearables

- 7.2.5. Smart Speaker

- 7.2.6. Other Devices

- 7.3. Market Analysis, Insights and Forecast - by End-User Industry

- 7.3.1. Government

- 7.3.2. Real Estate

- 7.3.3. Consumer Electronics

- 7.3.4. Automotive

- 7.3.5. Transportation

- 7.3.6. Healthcare

- 7.3.7. Manufacturing

- 7.3.8. Others

- 7.1. Market Analysis, Insights and Forecast - by Processor

- 8. Europe Edge AI Hardware Market Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Processor

- 8.1.1. CPU

- 8.1.2. GPU

- 8.1.3. FPGA

- 8.1.4. ASICs

- 8.2. Market Analysis, Insights and Forecast - by Device

- 8.2.1. Smartphones

- 8.2.2. Cameras

- 8.2.3. Robots

- 8.2.4. Wearables

- 8.2.5. Smart Speaker

- 8.2.6. Other Devices

- 8.3. Market Analysis, Insights and Forecast - by End-User Industry

- 8.3.1. Government

- 8.3.2. Real Estate

- 8.3.3. Consumer Electronics

- 8.3.4. Automotive

- 8.3.5. Transportation

- 8.3.6. Healthcare

- 8.3.7. Manufacturing

- 8.3.8. Others

- 8.1. Market Analysis, Insights and Forecast - by Processor

- 9. Asia Edge AI Hardware Market Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Processor

- 9.1.1. CPU

- 9.1.2. GPU

- 9.1.3. FPGA

- 9.1.4. ASICs

- 9.2. Market Analysis, Insights and Forecast - by Device

- 9.2.1. Smartphones

- 9.2.2. Cameras

- 9.2.3. Robots

- 9.2.4. Wearables

- 9.2.5. Smart Speaker

- 9.2.6. Other Devices

- 9.3. Market Analysis, Insights and Forecast - by End-User Industry

- 9.3.1. Government

- 9.3.2. Real Estate

- 9.3.3. Consumer Electronics

- 9.3.4. Automotive

- 9.3.5. Transportation

- 9.3.6. Healthcare

- 9.3.7. Manufacturing

- 9.3.8. Others

- 9.1. Market Analysis, Insights and Forecast - by Processor

- 10. Australia and New Zealand Edge AI Hardware Market Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Processor

- 10.1.1. CPU

- 10.1.2. GPU

- 10.1.3. FPGA

- 10.1.4. ASICs

- 10.2. Market Analysis, Insights and Forecast - by Device

- 10.2.1. Smartphones

- 10.2.2. Cameras

- 10.2.3. Robots

- 10.2.4. Wearables

- 10.2.5. Smart Speaker

- 10.2.6. Other Devices

- 10.3. Market Analysis, Insights and Forecast - by End-User Industry

- 10.3.1. Government

- 10.3.2. Real Estate

- 10.3.3. Consumer Electronics

- 10.3.4. Automotive

- 10.3.5. Transportation

- 10.3.6. Healthcare

- 10.3.7. Manufacturing

- 10.3.8. Others

- 10.1. Market Analysis, Insights and Forecast - by Processor

- 11. Latin America Edge AI Hardware Market Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Processor

- 11.1.1. CPU

- 11.1.2. GPU

- 11.1.3. FPGA

- 11.1.4. ASICs

- 11.2. Market Analysis, Insights and Forecast - by Device

- 11.2.1. Smartphones

- 11.2.2. Cameras

- 11.2.3. Robots

- 11.2.4. Wearables

- 11.2.5. Smart Speaker

- 11.2.6. Other Devices

- 11.3. Market Analysis, Insights and Forecast - by End-User Industry

- 11.3.1. Government

- 11.3.2. Real Estate

- 11.3.3. Consumer Electronics

- 11.3.4. Automotive

- 11.3.5. Transportation

- 11.3.6. Healthcare

- 11.3.7. Manufacturing

- 11.3.8. Others

- 11.1. Market Analysis, Insights and Forecast - by Processor

- 12. Middle East and Africa Edge AI Hardware Market Analysis, Insights and Forecast, 2021-2033

- 12.1. Market Analysis, Insights and Forecast - by Processor

- 12.1.1. CPU

- 12.1.2. GPU

- 12.1.3. FPGA

- 12.1.4. ASICs

- 12.2. Market Analysis, Insights and Forecast - by Device

- 12.2.1. Smartphones

- 12.2.2. Cameras

- 12.2.3. Robots

- 12.2.4. Wearables

- 12.2.5. Smart Speaker

- 12.2.6. Other Devices

- 12.3. Market Analysis, Insights and Forecast - by End-User Industry

- 12.3.1. Government

- 12.3.2. Real Estate

- 12.3.3. Consumer Electronics

- 12.3.4. Automotive

- 12.3.5. Transportation

- 12.3.6. Healthcare

- 12.3.7. Manufacturing

- 12.3.8. Others

- 12.1. Market Analysis, Insights and Forecast - by Processor

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Baidu Inc

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Samsung Group

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Denso Corporation

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Xilinx Inc *List Not Exhaustive

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Alibaba Group Holding Limited

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Alphabet Inc

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Continental AG

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Qualcomm Incorporated

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Advanced Micro Devices Inc

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Amazon com Inc

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Robert Bosch GmbH

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 KALRAY Corporation

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.13 Huawei Technologies Co Ltd

- 13.1.13.1. Company Overview

- 13.1.13.2. Products

- 13.1.13.3. Company Financials

- 13.1.13.4. SWOT Analysis

- 13.1.14 MediaTek Inc

- 13.1.14.1. Company Overview

- 13.1.14.2. Products

- 13.1.14.3. Company Financials

- 13.1.14.4. SWOT Analysis

- 13.1.15 Nvidia Corporation

- 13.1.15.1. Company Overview

- 13.1.15.2. Products

- 13.1.15.3. Company Financials

- 13.1.15.4. SWOT Analysis

- 13.1.16 Apple Inc

- 13.1.16.1. Company Overview

- 13.1.16.2. Products

- 13.1.16.3. Company Financials

- 13.1.16.4. SWOT Analysis

- 13.1.17 Intel Corporation

- 13.1.17.1. Company Overview

- 13.1.17.2. Products

- 13.1.17.3. Company Financials

- 13.1.17.4. SWOT Analysis

- 13.1.1 Baidu Inc

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Edge AI Hardware Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Edge AI Hardware Market Revenue (billion), by Processor 2025 & 2033

- Figure 3: North America Edge AI Hardware Market Revenue Share (%), by Processor 2025 & 2033

- Figure 4: North America Edge AI Hardware Market Revenue (billion), by Device 2025 & 2033

- Figure 5: North America Edge AI Hardware Market Revenue Share (%), by Device 2025 & 2033

- Figure 6: North America Edge AI Hardware Market Revenue (billion), by End-User Industry 2025 & 2033

- Figure 7: North America Edge AI Hardware Market Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 8: North America Edge AI Hardware Market Revenue (billion), by Country 2025 & 2033

- Figure 9: North America Edge AI Hardware Market Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Edge AI Hardware Market Revenue (billion), by Processor 2025 & 2033

- Figure 11: Europe Edge AI Hardware Market Revenue Share (%), by Processor 2025 & 2033

- Figure 12: Europe Edge AI Hardware Market Revenue (billion), by Device 2025 & 2033

- Figure 13: Europe Edge AI Hardware Market Revenue Share (%), by Device 2025 & 2033

- Figure 14: Europe Edge AI Hardware Market Revenue (billion), by End-User Industry 2025 & 2033

- Figure 15: Europe Edge AI Hardware Market Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 16: Europe Edge AI Hardware Market Revenue (billion), by Country 2025 & 2033

- Figure 17: Europe Edge AI Hardware Market Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Edge AI Hardware Market Revenue (billion), by Processor 2025 & 2033

- Figure 19: Asia Edge AI Hardware Market Revenue Share (%), by Processor 2025 & 2033

- Figure 20: Asia Edge AI Hardware Market Revenue (billion), by Device 2025 & 2033

- Figure 21: Asia Edge AI Hardware Market Revenue Share (%), by Device 2025 & 2033

- Figure 22: Asia Edge AI Hardware Market Revenue (billion), by End-User Industry 2025 & 2033

- Figure 23: Asia Edge AI Hardware Market Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 24: Asia Edge AI Hardware Market Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Edge AI Hardware Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Australia and New Zealand Edge AI Hardware Market Revenue (billion), by Processor 2025 & 2033

- Figure 27: Australia and New Zealand Edge AI Hardware Market Revenue Share (%), by Processor 2025 & 2033

- Figure 28: Australia and New Zealand Edge AI Hardware Market Revenue (billion), by Device 2025 & 2033

- Figure 29: Australia and New Zealand Edge AI Hardware Market Revenue Share (%), by Device 2025 & 2033

- Figure 30: Australia and New Zealand Edge AI Hardware Market Revenue (billion), by End-User Industry 2025 & 2033

- Figure 31: Australia and New Zealand Edge AI Hardware Market Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 32: Australia and New Zealand Edge AI Hardware Market Revenue (billion), by Country 2025 & 2033

- Figure 33: Australia and New Zealand Edge AI Hardware Market Revenue Share (%), by Country 2025 & 2033

- Figure 34: Latin America Edge AI Hardware Market Revenue (billion), by Processor 2025 & 2033

- Figure 35: Latin America Edge AI Hardware Market Revenue Share (%), by Processor 2025 & 2033

- Figure 36: Latin America Edge AI Hardware Market Revenue (billion), by Device 2025 & 2033

- Figure 37: Latin America Edge AI Hardware Market Revenue Share (%), by Device 2025 & 2033

- Figure 38: Latin America Edge AI Hardware Market Revenue (billion), by End-User Industry 2025 & 2033

- Figure 39: Latin America Edge AI Hardware Market Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 40: Latin America Edge AI Hardware Market Revenue (billion), by Country 2025 & 2033

- Figure 41: Latin America Edge AI Hardware Market Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa Edge AI Hardware Market Revenue (billion), by Processor 2025 & 2033

- Figure 43: Middle East and Africa Edge AI Hardware Market Revenue Share (%), by Processor 2025 & 2033

- Figure 44: Middle East and Africa Edge AI Hardware Market Revenue (billion), by Device 2025 & 2033

- Figure 45: Middle East and Africa Edge AI Hardware Market Revenue Share (%), by Device 2025 & 2033

- Figure 46: Middle East and Africa Edge AI Hardware Market Revenue (billion), by End-User Industry 2025 & 2033

- Figure 47: Middle East and Africa Edge AI Hardware Market Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 48: Middle East and Africa Edge AI Hardware Market Revenue (billion), by Country 2025 & 2033

- Figure 49: Middle East and Africa Edge AI Hardware Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Edge AI Hardware Market Revenue billion Forecast, by Processor 2020 & 2033

- Table 2: Global Edge AI Hardware Market Revenue billion Forecast, by Device 2020 & 2033

- Table 3: Global Edge AI Hardware Market Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 4: Global Edge AI Hardware Market Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global Edge AI Hardware Market Revenue billion Forecast, by Processor 2020 & 2033

- Table 6: Global Edge AI Hardware Market Revenue billion Forecast, by Device 2020 & 2033

- Table 7: Global Edge AI Hardware Market Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 8: Global Edge AI Hardware Market Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Global Edge AI Hardware Market Revenue billion Forecast, by Processor 2020 & 2033

- Table 10: Global Edge AI Hardware Market Revenue billion Forecast, by Device 2020 & 2033

- Table 11: Global Edge AI Hardware Market Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 12: Global Edge AI Hardware Market Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Edge AI Hardware Market Revenue billion Forecast, by Processor 2020 & 2033

- Table 14: Global Edge AI Hardware Market Revenue billion Forecast, by Device 2020 & 2033

- Table 15: Global Edge AI Hardware Market Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 16: Global Edge AI Hardware Market Revenue billion Forecast, by Country 2020 & 2033

- Table 17: Global Edge AI Hardware Market Revenue billion Forecast, by Processor 2020 & 2033

- Table 18: Global Edge AI Hardware Market Revenue billion Forecast, by Device 2020 & 2033

- Table 19: Global Edge AI Hardware Market Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 20: Global Edge AI Hardware Market Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Global Edge AI Hardware Market Revenue billion Forecast, by Processor 2020 & 2033

- Table 22: Global Edge AI Hardware Market Revenue billion Forecast, by Device 2020 & 2033

- Table 23: Global Edge AI Hardware Market Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 24: Global Edge AI Hardware Market Revenue billion Forecast, by Country 2020 & 2033

- Table 25: Global Edge AI Hardware Market Revenue billion Forecast, by Processor 2020 & 2033

- Table 26: Global Edge AI Hardware Market Revenue billion Forecast, by Device 2020 & 2033

- Table 27: Global Edge AI Hardware Market Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 28: Global Edge AI Hardware Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Edge AI Hardware Market?

The projected CAGR is approximately 21.7%.

2. Which companies are prominent players in the Edge AI Hardware Market?

Key companies in the market include Baidu Inc, Samsung Group, Denso Corporation, Xilinx Inc *List Not Exhaustive, Alibaba Group Holding Limited, Alphabet Inc, Continental AG, Qualcomm Incorporated, Advanced Micro Devices Inc, Amazon com Inc, Robert Bosch GmbH, KALRAY Corporation, Huawei Technologies Co Ltd, MediaTek Inc, Nvidia Corporation, Apple Inc, Intel Corporation.

3. What are the main segments of the Edge AI Hardware Market?

The market segments include Processor, Device, End-User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 24.91 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Penetration of AI in Edge Devices; Increasing Demand for Smart Homes and Smart Cities.

6. What are the notable trends driving market growth?

Increase Demand for Smart Homes and Smart Cities is Expected to Drive the Market Growth.

7. Are there any restraints impacting market growth?

Security Concerns Related to Edge AI Devices.

8. Can you provide examples of recent developments in the market?

November 2022 - Network solutions provider Lumen Technologies began expanding its portfolio of Edge Computing Solutions into the Asia-Pacific Region, including its Edge Bare Metal pay-as-you-go hardware solution for servers, taking advantage of sites in Singapore and Japan.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Edge AI Hardware Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Edge AI Hardware Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Edge AI Hardware Market?

To stay informed about further developments, trends, and reports in the Edge AI Hardware Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence