Key Insights

The global distributed and edge computing market is projected to achieve significant expansion, reaching an estimated $168.4 billion by 2025, driven by a Compound Annual Growth Rate (CAGR) of 8.1% through 2033. This growth is fundamentally propelled by the increasing need for real-time data processing and analytics at the data source. Key catalysts include the expanding IoT device ecosystem, the widespread adoption of 5G networks enabling lower latency and higher bandwidth, and the critical requirement for robust cybersecurity at the network edge. The enterprise sector is expected to spearhead market growth, essential for operational optimization, enhanced customer experiences, and pioneering new business models in manufacturing, retail, and logistics. The healthcare sector is also a notable growth area, utilizing edge computing for remote patient monitoring and accelerated diagnostics.

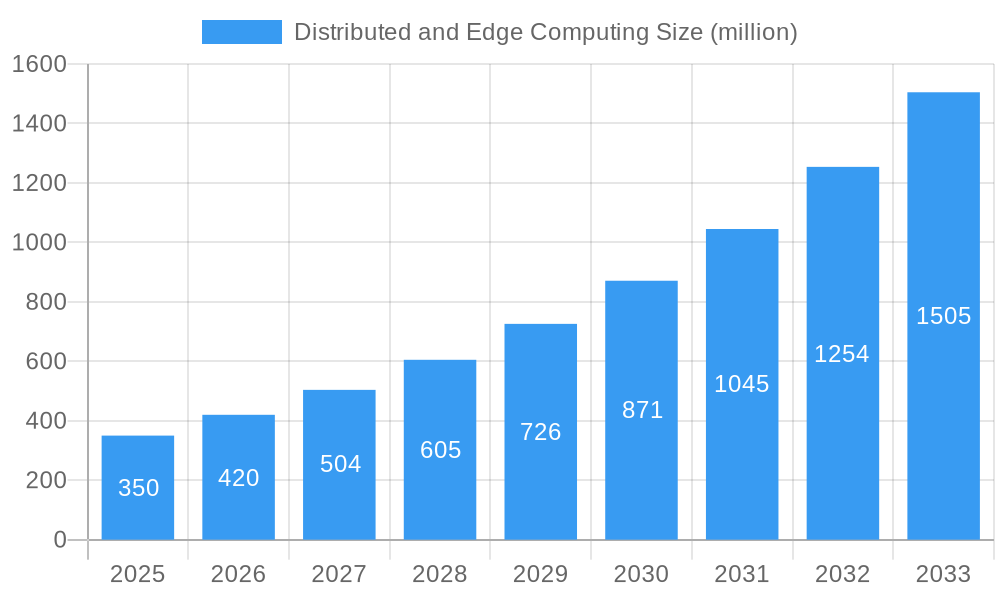

Distributed and Edge Computing Market Size (In Billion)

Evolving market trends include the synergy of AI and edge computing for intelligent edge decision-making and the emergence of edge-as-a-service models, enhancing business flexibility and scalability. Nevertheless, potential restraints to rapid adoption include data security and privacy challenges at the edge, the complexities of managing distributed infrastructure, and substantial initial deployment investments. Geographically, North America and Asia Pacific are anticipated to lead market dominance, supported by significant digital transformation investments, advanced technological infrastructure, and the strong presence of major players such as Amazon Web Services, Microsoft Azure, and Google Cloud. The competitive arena is vibrant, with established technology leaders and emerging startups competing through strategic alliances, mergers, and acquisitions, emphasizing integrated hardware and software solutions for diverse edge computing applications.

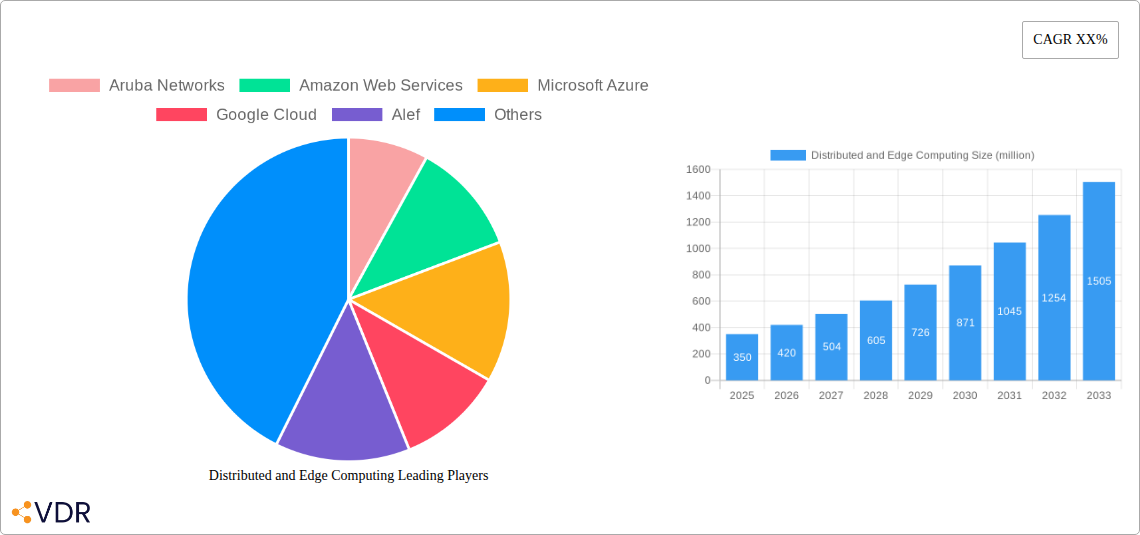

Distributed and Edge Computing Company Market Share

Discover key insights into the Distributed and Edge Computing market's size, growth trajectory, and future forecasts.

Distributed and Edge Computing Market Dynamics & Structure

The Distributed and Edge Computing market is characterized by dynamic forces shaping its rapid evolution. Market concentration is moderately fragmented, with major cloud providers like Amazon Web Services, Microsoft Azure, and Google Cloud holding significant sway, alongside specialized players such as Alef, ClearBlade, and Dell Technologies. Technological innovation is the primary driver, fueled by the increasing demand for real-time data processing, reduced latency, and enhanced cybersecurity at the network edge. Regulatory frameworks, though still developing, are beginning to address data sovereignty and privacy concerns, influencing deployment strategies. Competitive product substitutes include traditional centralized cloud solutions, but the unique advantages of edge computing in specific use cases are driving adoption. End-user demographics span across enterprise IT, telecommunications, manufacturing, and healthcare, with a growing personal segment utilizing IoT devices. Mergers and acquisitions (M&A) are a notable trend, with companies like EdgeConneX and Section actively consolidating infrastructure and solutions to capture market share. We anticipate approximately 15 M&A deals annually during the forecast period, with an average deal value of $50 million, indicating strategic consolidation and investment in this burgeoning sector. Barriers to innovation include the complexity of managing distributed infrastructure and the need for robust security protocols.

- Market Concentration: Moderately fragmented with a mix of hyperscale cloud providers and specialized edge solution vendors.

- Technological Innovation Drivers: Real-time processing, low latency, IoT expansion, AI/ML at the edge, 5G deployment.

- Regulatory Frameworks: Data privacy (GDPR, CCPA), data localization, and industry-specific compliance.

- Competitive Product Substitutes: Traditional centralized cloud services, on-premises data centers.

- End-User Demographics: Enterprise (IoT, industrial automation), Telecommunications (5G infrastructure), Healthcare (remote monitoring), Automotive (autonomous vehicles), Retail (smart stores).

- M&A Trends: Consolidation of edge infrastructure providers, integration of edge software and hardware solutions, acquisitions to enhance AI/ML capabilities at the edge.

Distributed and Edge Computing Growth Trends & Insights

The Distributed and Edge Computing market is poised for exponential growth, transitioning from a niche solution to a foundational component of modern digital infrastructure. The market size is projected to expand from an estimated $65,000 million in the base year of 2025 to a substantial $150,000 million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 11.5% during the forecast period. This robust growth is propelled by the relentless proliferation of data generated by an ever-increasing number of connected devices, demanding immediate processing and analysis closer to the source. Adoption rates are accelerating across various industries, driven by the need for enhanced performance, improved user experiences, and cost efficiencies. Technological disruptions, particularly the widespread rollout of 5G networks, are acting as significant catalysts, enabling low-latency, high-bandwidth applications that were previously unfeasible. Consumer behavior is also shifting, with a growing expectation for seamless, real-time interactions with digital services, from augmented reality experiences to responsive smart home devices. The historical period (2019-2024) saw initial development and pilot projects, with market penetration reaching around 15% by 2024. The base year of 2025 marks a critical inflection point where widespread commercial adoption is set to surge. Market penetration is estimated to reach 25% by 2025, indicating a significant leap in the integration of distributed and edge computing solutions across various sectors. The value chain is becoming increasingly complex, with collaboration between hardware manufacturers like Dell Technologies and Eurotech, software providers such as Microsoft Azure and ClearBlade, and network infrastructure specialists like Aruba Networks and EdgeConneX becoming crucial for delivering end-to-end solutions. The projected growth is not merely incremental but represents a fundamental shift in how data is processed and managed, moving computing power from centralized data centers to the periphery of networks where data is generated and consumed. This decentralized approach is unlocking new possibilities and driving innovation across the entire digital ecosystem.

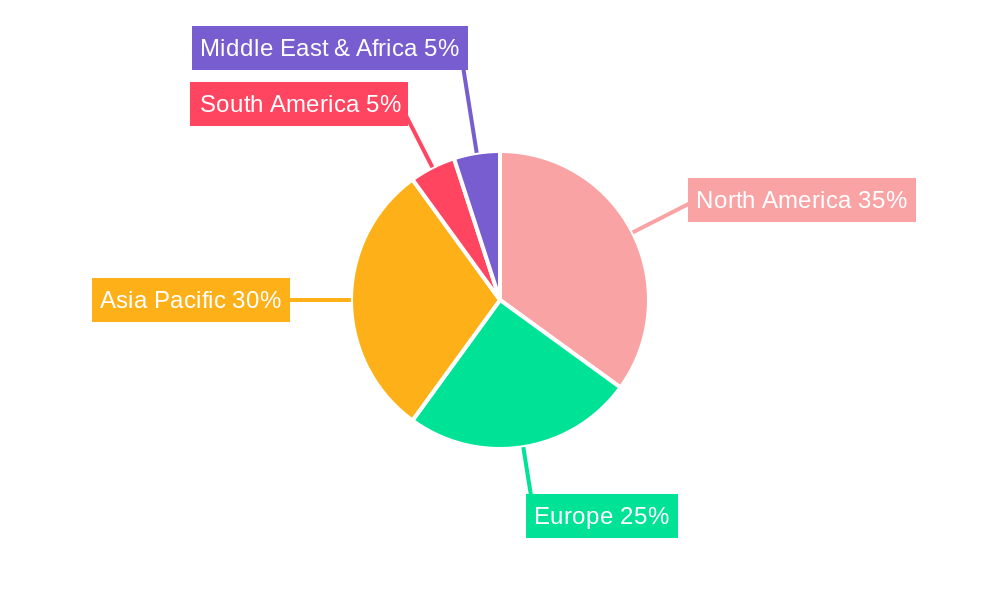

Dominant Regions, Countries, or Segments in Distributed and Edge Computing

North America currently dominates the Distributed and Edge Computing market, driven by a confluence of factors including a robust technological infrastructure, significant investments in 5G deployment, and a high concentration of enterprises actively pursuing digital transformation initiatives. The United States, in particular, is a powerhouse, home to leading technology companies such as Amazon Web Services, Microsoft Azure, and Google Cloud, which are investing heavily in developing and deploying edge computing solutions. Furthermore, the presence of a large industrial sector, a rapidly growing IoT ecosystem, and a strong research and development base contributes to North America's leadership.

The Enterprise segment is by far the most dominant application within the Distributed and Edge Computing market. Enterprises are leveraging edge solutions for a wide array of critical functions, including industrial automation, smart manufacturing, supply chain optimization, real-time analytics for operational efficiency, and enhanced customer experiences in retail environments. The sheer volume of data generated by industrial IoT devices, sensors, and machinery necessitates processing at the edge to enable immediate decision-making and prevent costly downtime. For instance, in manufacturing, edge computing facilitates predictive maintenance by analyzing sensor data locally, identifying potential equipment failures before they occur, thus significantly reducing operational disruptions and costs. In the retail sector, edge computing powers real-time inventory management, personalized customer interactions through localized analytics, and secure payment processing. The enterprise segment is projected to account for approximately 60% of the total market revenue during the forecast period, underscoring its pivotal role.

The Software type is also a key driver of market growth, enabling the intelligence and functionality of edge deployments. Companies like Microsoft Azure and ClearBlade are at the forefront of providing comprehensive software platforms that manage, orchestrate, and analyze data at the edge. This includes edge operating systems, containerization technologies, AI/ML inference engines, and data management tools. The ability to deploy intelligent applications at the edge, powered by sophisticated software, is crucial for unlocking the full potential of distributed computing. The software segment is expected to capture a significant market share, estimated at around 45% of the total market value, as it underpins the innovation and scalability of edge solutions.

- Dominant Region: North America

- Key Country: United States

- Drivers: High 5G deployment, presence of major tech giants, strong enterprise adoption, robust R&D ecosystem.

- Dominant Application Segment: Enterprise

- Key Verticals: Industrial Automation, Smart Manufacturing, Retail, Healthcare, Automotive.

- Growth Factors: IoT proliferation, need for real-time data processing, operational efficiency, cost reduction.

- Dominant Type Segment: Software

- Key Components: Edge OS, AI/ML inference engines, data management platforms, orchestration tools.

- Impact: Enables intelligent applications and efficient management of distributed infrastructure.

Distributed and Edge Computing Product Landscape

The product landscape in Distributed and Edge Computing is characterized by an expanding array of innovative solutions designed to meet diverse application needs. Hardware offerings range from ruggedized edge servers and gateways from companies like Dell Technologies and Eurotech, capable of withstanding harsh industrial environments, to specialized edge devices and accelerators for AI processing. Software solutions, provided by leaders such as Microsoft Azure and Google Cloud, encompass edge management platforms, container orchestration, data analytics, and machine learning inference engines. Innovations are focused on improving computational power at the edge, enhancing security, and simplifying deployment and management of distributed infrastructure. Performance metrics are constantly being pushed, with a focus on reducing latency to sub-millisecond levels, increasing data processing throughput, and optimizing power consumption for remote deployments. Unique selling propositions often revolve around industry-specific solutions, such as Alef's focus on mobile edge computing for telecommunications, and ClearBlade's robust industrial IoT platform.

Key Drivers, Barriers & Challenges in Distributed and Edge Computing

Key Drivers:

- Exponential Data Growth: The surge in data from IoT devices necessitates localized processing to reduce latency and bandwidth costs.

- 5G Network Expansion: Enables low-latency, high-bandwidth applications, making edge computing more viable and performant.

- AI/ML Advancements: The demand for real-time AI inferencing at the edge fuels the adoption of edge computing for intelligent applications.

- Industry Digitization: Enterprises across sectors are adopting digital transformation strategies, with edge computing being a critical enabler for efficiency and innovation.

Key Barriers & Challenges:

- Infrastructure Costs: Initial investment in edge hardware and deployment can be substantial.

- Security Complexities: Managing security across a vast and distributed network of edge devices presents significant challenges.

- Interoperability and Standardization: Lack of universal standards can lead to vendor lock-in and integration difficulties.

- Skilled Workforce Shortage: A demand for professionals with expertise in distributed systems, networking, and edge AI is growing, creating a talent gap.

- Supply Chain Disruptions: Global supply chain issues can impact the availability and cost of edge hardware components. For instance, the semiconductor shortage has impacted hardware availability, potentially delaying projects by an estimated 10-15%.

Emerging Opportunities in Distributed and Edge Computing

Emerging opportunities in Distributed and Edge Computing are vast, driven by evolving technological capabilities and increasing market maturity. The expansion of Industry 5.0 concepts, which emphasize human-robot collaboration and hyper-personalization, presents a significant avenue for edge computing to enable real-time coordination and data exchange. Augmented Reality (AR) and Virtual Reality (VR) applications in enterprise training, remote assistance, and entertainment are heavily reliant on low-latency edge processing. Furthermore, the growing need for edge-native AI models that can operate efficiently on resource-constrained devices is opening new avenues for specialized hardware and software solutions. The development of decentralized applications (dApps) leveraging blockchain technology at the edge for enhanced security and transparency is another promising area. Edge-as-a-Service (EaaS) models are also gaining traction, allowing businesses to access edge computing capabilities without significant upfront infrastructure investment.

Growth Accelerators in the Distributed and Edge Computing Industry

Several catalysts are accelerating the growth of the Distributed and Edge Computing industry. The ongoing deployment of 5G infrastructure globally is a primary accelerator, providing the necessary network capabilities for many edge applications to thrive. Strategic partnerships between hardware manufacturers (e.g., Hewlett Packard Enterprise), cloud providers (e.g., Amazon Web Services, Microsoft Azure), and telecommunications companies are crucial for developing integrated, end-to-end solutions. Advancements in AI and Machine Learning algorithms that can be optimized for edge devices are driving greater intelligence and autonomy at the periphery. Furthermore, the increasing focus on sustainability and energy efficiency is pushing the development of low-power edge computing solutions, making them more viable for widespread deployment. The growing maturity of edge orchestration and management platforms is also simplifying deployment and reducing operational overhead, thus encouraging broader adoption.

Key Players Shaping the Distributed and Edge Computing Market

- Aruba Networks

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- Alef

- IBM

- ClearBlade

- Dell Technologies

- EdgeConneX

- Section

- Eurotech

- Hewlett Packard Enterprise (HPE)

- Infiot ZETO

- Mutable

- Vapor IO

Notable Milestones in Distributed and Edge Computing Sector

- 2019: Widespread adoption of IoT devices begins to drive early edge computing deployments in industrial settings.

- 2020: Increased focus on remote work and collaboration fuels demand for edge solutions enabling secure and performant access to resources.

- 2021: Major cloud providers announce expanded edge computing portfolios, integrating hardware and software offerings.

- 2022: Telecommunications companies begin large-scale 5G network rollouts, creating a foundation for advanced edge services.

- 2023: Significant investments in edge AI hardware and software, with a focus on machine learning inference at the edge.

- 2024: Emergence of industry-specific edge solutions tailored for healthcare, retail, and smart cities.

In-Depth Distributed and Edge Computing Market Outlook

The future of Distributed and Edge Computing is exceptionally promising, with sustained high growth projected through 2033. Growth accelerators such as the ongoing build-out of 5G networks, the maturation of AI/ML capabilities for edge deployment, and increasing enterprise investment in digital transformation will continue to fuel market expansion. Strategic partnerships between leading technology providers will be pivotal in delivering comprehensive and scalable edge solutions. The outlook suggests a continued shift towards decentralized computing architectures, with edge playing a critical role in enabling real-time data processing, personalized user experiences, and operational efficiencies across all industries. Untapped markets in developing regions, coupled with innovative applications in areas like autonomous systems and smart infrastructure, present significant strategic opportunities for market participants. The market is expected to evolve towards more intelligent, secure, and autonomous edge environments, driving significant value creation.

Distributed and Edge Computing Segmentation

-

1. Application

- 1.1. Enterprise

- 1.2. Medical Insurance

- 1.3. Personal

- 1.4. Other

-

2. Types

- 2.1. Hardware

- 2.2. Software

Distributed and Edge Computing Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Distributed and Edge Computing Regional Market Share

Geographic Coverage of Distributed and Edge Computing

Distributed and Edge Computing REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Enterprise

- 5.1.2. Medical Insurance

- 5.1.3. Personal

- 5.1.4. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Hardware

- 5.2.2. Software

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Distributed and Edge Computing Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Enterprise

- 6.1.2. Medical Insurance

- 6.1.3. Personal

- 6.1.4. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Hardware

- 6.2.2. Software

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Distributed and Edge Computing Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Enterprise

- 7.1.2. Medical Insurance

- 7.1.3. Personal

- 7.1.4. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Hardware

- 7.2.2. Software

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Distributed and Edge Computing Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Enterprise

- 8.1.2. Medical Insurance

- 8.1.3. Personal

- 8.1.4. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Hardware

- 8.2.2. Software

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Distributed and Edge Computing Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Enterprise

- 9.1.2. Medical Insurance

- 9.1.3. Personal

- 9.1.4. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Hardware

- 9.2.2. Software

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Distributed and Edge Computing Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Enterprise

- 10.1.2. Medical Insurance

- 10.1.3. Personal

- 10.1.4. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Hardware

- 10.2.2. Software

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Distributed and Edge Computing Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Enterprise

- 11.1.2. Medical Insurance

- 11.1.3. Personal

- 11.1.4. Other

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Hardware

- 11.2.2. Software

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Aruba Networks

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Amazon Web Services

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Microsoft Azure

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Google Cloud

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Alef

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 IBM

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 ClearBlade

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Dell Technologies

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 EdgeConneX

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Section

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Eurotech

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Hewlett Packard Enterprise (HPE)

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Infiot ZETO

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Mutable

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Vapor IO

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Aruba Networks

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Distributed and Edge Computing Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Distributed and Edge Computing Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Distributed and Edge Computing Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Distributed and Edge Computing Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Distributed and Edge Computing Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Distributed and Edge Computing Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Distributed and Edge Computing Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Distributed and Edge Computing Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Distributed and Edge Computing Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Distributed and Edge Computing Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Distributed and Edge Computing Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Distributed and Edge Computing Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Distributed and Edge Computing Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Distributed and Edge Computing Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Distributed and Edge Computing Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Distributed and Edge Computing Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Distributed and Edge Computing Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Distributed and Edge Computing Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Distributed and Edge Computing Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Distributed and Edge Computing Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Distributed and Edge Computing Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Distributed and Edge Computing Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Distributed and Edge Computing Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Distributed and Edge Computing Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Distributed and Edge Computing Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Distributed and Edge Computing Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Distributed and Edge Computing Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Distributed and Edge Computing Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Distributed and Edge Computing Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Distributed and Edge Computing Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Distributed and Edge Computing Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Distributed and Edge Computing Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Distributed and Edge Computing Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Distributed and Edge Computing Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Distributed and Edge Computing Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Distributed and Edge Computing Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Distributed and Edge Computing Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Distributed and Edge Computing Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Distributed and Edge Computing Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Distributed and Edge Computing Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Distributed and Edge Computing Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Distributed and Edge Computing Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Distributed and Edge Computing Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Distributed and Edge Computing Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Distributed and Edge Computing Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Distributed and Edge Computing Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Distributed and Edge Computing Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Distributed and Edge Computing Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Distributed and Edge Computing Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Distributed and Edge Computing Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Distributed and Edge Computing?

The projected CAGR is approximately 8.1%.

2. Which companies are prominent players in the Distributed and Edge Computing?

Key companies in the market include Aruba Networks, Amazon Web Services, Microsoft Azure, Google Cloud, Alef, IBM, ClearBlade, Dell Technologies, EdgeConneX, Section, Eurotech, Hewlett Packard Enterprise (HPE), Infiot ZETO, Mutable, Vapor IO.

3. What are the main segments of the Distributed and Edge Computing?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 168.4 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Distributed and Edge Computing," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Distributed and Edge Computing report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Distributed and Edge Computing?

To stay informed about further developments, trends, and reports in the Distributed and Edge Computing, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence