Key Insights

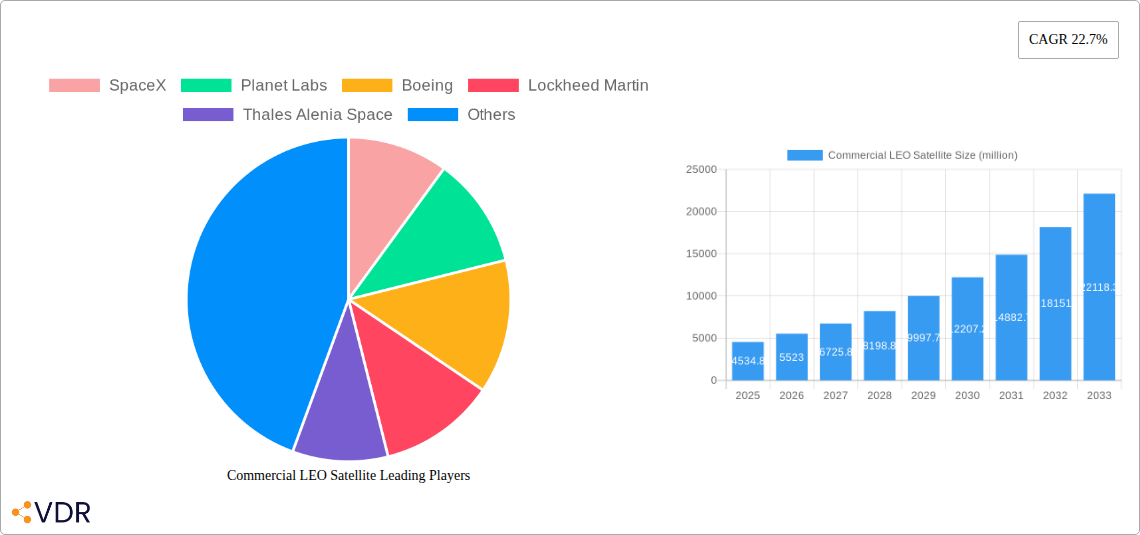

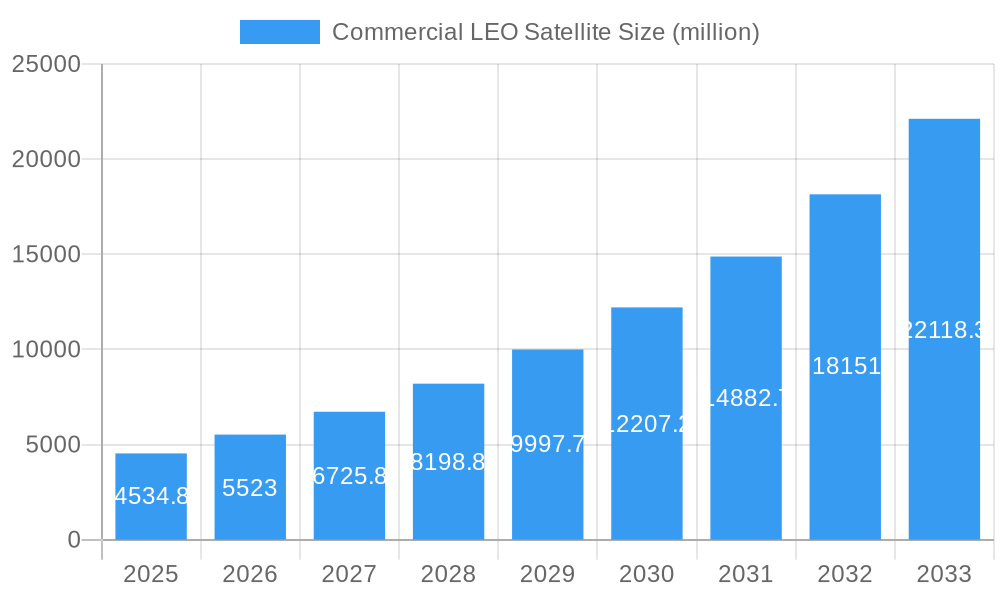

The global Commercial Low Earth Orbit (LEO) Satellite market is experiencing phenomenal growth, projected to reach an impressive $4534.8 million by 2025. This rapid expansion is fueled by a remarkable Compound Annual Growth Rate (CAGR) of 22.7% during the forecast period of 2019-2033. The burgeoning demand for ubiquitous, high-speed internet access in remote and underserved regions stands as a primary driver, alongside the increasing utilization of LEO satellites for robust marine operations and reliable onboard WiFi solutions. Furthermore, the critical role LEO satellites play in disaster recovery efforts, offering resilient communication networks when terrestrial infrastructure fails, is a significant contributor to market momentum. Emerging trends such as the proliferation of small satellite constellations and advancements in satellite technology are further accelerating adoption and innovation.

Commercial LEO Satellite Market Size (In Billion)

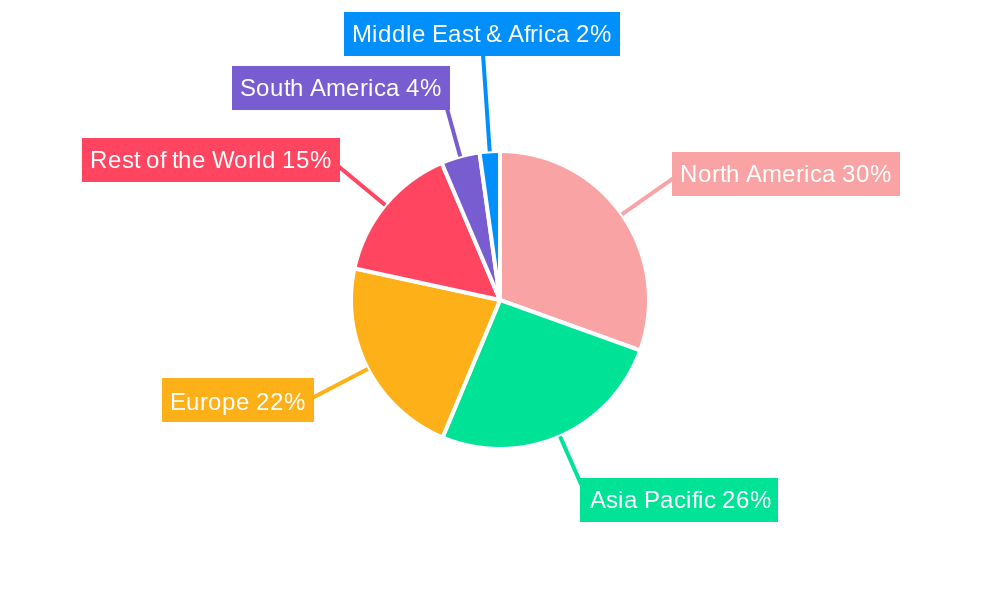

The market is segmented by application into Remote Area Satellite Network, Marine Operations, Onboard WiFi, and Network Disaster Recovery, each showcasing substantial growth potential. By type, segments include Below 50 Kg, 50-500 Kg, and Above 500 Kg, reflecting the diverse range of satellite solutions being deployed. Key players like SpaceX, Planet Labs, Boeing, and OneWeb Satellites are at the forefront, investing heavily in R&D and constellation deployment to capture market share. Geographically, North America, with its advanced technological infrastructure and strong demand for connectivity, is expected to lead, followed closely by the rapidly developing Asia Pacific region. Europe also presents significant opportunities, driven by governmental initiatives and commercial demand. While the market is experiencing robust growth, potential restraints such as the high initial investment costs for satellite deployment and the increasing risk of orbital debris require careful consideration and proactive management to ensure sustained progress.

Commercial LEO Satellite Company Market Share

Here is a compelling, SEO-optimized report description for the Commercial LEO Satellite market, integrating high-traffic keywords and structured as requested.

Commercial LEO Satellite Market Dynamics & Structure

The global commercial LEO satellite market is characterized by a dynamic and evolving structure, driven by rapid technological advancements and increasing demand across diverse applications. Market concentration is moderately high, with key players like SpaceX and OneWeb Satellites leading innovation and deployment. However, a growing number of specialized companies and new entrants are contributing to a more competitive landscape. Technological innovation serves as the primary driver, fueled by miniaturization, improved launch capabilities, and the development of advanced communication payloads. Regulatory frameworks, while evolving, are crucial for enabling orbital access and spectrum allocation, influencing market entry and expansion. Competitive product substitutes, such as terrestrial broadband and geostationary satellites, are present but are increasingly being outpaced by the cost-effectiveness and low latency offered by LEO constellations. End-user demographics are broadening, extending beyond traditional telecommunications to include enterprise, government, and consumer sectors seeking ubiquitous connectivity. Merger and acquisition (M&A) trends are evident, with larger players consolidating capabilities or acquiring innovative technologies to secure market position. For instance, the historical period has seen key M&A activities amounting to approximately $1,200 million in deal volumes, indicating strategic consolidation.

- Market Concentration: Moderate to high, with a few dominant players and a growing base of agile competitors.

- Technological Innovation: Driven by satellite miniaturization, advanced propulsion, and on-orbit servicing capabilities.

- Regulatory Frameworks: Evolving policies impacting spectrum allocation, orbital debris mitigation, and international cooperation.

- Competitive Substitutes: Terrestrial fiber optics, 5G networks, and geostationary satellite services.

- End-User Demographics: Expanding to include maritime, aviation, remote enterprises, and IoT applications.

- M&A Trends: Strategic acquisitions and partnerships aimed at enhancing capabilities and market reach.

Commercial LEO Satellite Growth Trends & Insights

The Commercial LEO Satellite market is poised for explosive growth, projected to expand significantly from its $28,500 million valuation in the Base Year of 2025 to an estimated $120,000 million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 19.5% during the Forecast Period of 2025–2033. This robust expansion is underpinned by a confluence of factors including rapidly decreasing launch costs, advancements in satellite technology, and a burgeoning demand for high-speed, low-latency broadband connectivity across underserved regions. The historical period, from 2019 to 2024, witnessed foundational investments and initial constellation deployments, laying the groundwork for the current accelerated adoption phase.

Technological disruptions are at the forefront of this growth trajectory. The development of smaller, more affordable satellites (Below 50 Kg segment) manufactured in large constellations is enabling unprecedented scalability and service coverage. This trend directly impacts adoption rates, making satellite internet a viable and competitive alternative to terrestrial solutions in many areas. Consumer behavior is shifting towards an expectation of constant connectivity, irrespective of location, a demand that LEO constellations are uniquely positioned to fulfill. The increasing reliance on cloud-based services, the Internet of Things (IoT), and the proliferation of mobile devices further amplify the need for reliable and pervasive network infrastructure. Market penetration is steadily increasing, particularly in regions with limited terrestrial broadband infrastructure, such as rural and remote areas, as well as in specialized sectors like aviation and maritime operations. The parent market for satellite services, which encompasses all satellite-based communication solutions, is itself experiencing significant growth, with LEO satellites carving out an increasingly dominant share of this expanding pie. The child market, focusing specifically on LEO satellite-based services, is demonstrating even more accelerated growth rates, driven by innovative business models and expanded application portfolios. Key industry developments include the ongoing deployment of mega-constellations by major players, the introduction of advanced in-orbit computing capabilities, and the increasing focus on satellite servicing and debris removal technologies, all of which are contributing to a more sustainable and efficient LEO ecosystem. The market penetration for LEO satellite services, which stood at an estimated 15% of the total addressable market in 2024, is projected to reach over 50% by 2033, underscoring the transformative impact of this technology.

Dominant Regions, Countries, or Segments in Commercial LEO Satellite

The Commercial LEO Satellite market's dominance is increasingly being shaped by specific regions, countries, and application segments that are capitalizing on the technology's transformative potential. North America, particularly the United States, stands out as a dominant region, driven by significant private investment, pioneering companies like SpaceX and Planet Labs, and a robust demand for advanced connectivity. The U.S. government's focus on next-generation communication infrastructure and its significant R&D investments in space technologies further solidify its leading position.

Within the Application segment, Remote Area Satellite Network is a primary growth driver. This segment is experiencing a substantial uplift due to the critical need for reliable internet access in rural, underserved, and developing regions worldwide. The ability of LEO satellites to provide high-speed, low-latency internet where terrestrial infrastructure is economically unviable makes this application paramount. Close behind is Marine Operations, a rapidly expanding sector that leverages LEO connectivity for enhanced navigation, real-time data transmission, crew welfare, and operational efficiency for shipping fleets and offshore platforms. Network Disaster Recovery is also gaining significant traction, offering a resilient backup communication solution that can be rapidly deployed during natural disasters or network outages, ensuring business continuity. Onboard WiFi for aviation and other mobile platforms is another key growth area, enhancing passenger and crew experience.

In terms of Types, the 50-500 Kg segment is currently the most dominant in terms of market share and deployment volume. This size category offers a compelling balance between payload capacity, launch cost, and constellation manageability, making it ideal for many commercial communication and earth observation missions. However, the Below 50 Kg segment is experiencing the fastest growth rate, driven by the proliferation of smaller, standardized satellites that allow for mass production and rapid deployment of large constellations, significantly lowering the barrier to entry and enabling new innovative applications. The Above 500 Kg segment, while less numerous, often caters to specialized, high-capacity applications and government contracts.

- Dominant Region: North America (primarily the United States) due to substantial private investment and technological leadership.

- Key Application Driver: Remote Area Satellite Network, addressing the global digital divide and connectivity gaps.

- Emerging Application Focus: Marine Operations and Network Disaster Recovery, showcasing critical use cases for resilient and widespread connectivity.

- Dominant Satellite Type: 50-500 Kg, offering a balanced approach to cost, capacity, and deployment for a wide range of applications.

- Fastest Growing Satellite Type: Below 50 Kg, enabling the mass deployment of advanced LEO constellations.

- Market Share (Approximate, 2025):

- Remote Area Satellite Network: 40%

- Marine Operations: 25%

- Network Disaster Recovery: 15%

- Onboard WiFi: 10%

- Other Applications: 10%

- Growth Potential: The "Remote Area Satellite Network" and "Marine Operations" segments are projected to exhibit the highest CAGRs during the forecast period.

Commercial LEO Satellite Product Landscape

The commercial LEO satellite product landscape is characterized by rapid innovation, focusing on miniaturization, modularity, and enhanced capabilities. Companies are developing satellites ranging from ultra-small satellites (CubeSats) to larger, more sophisticated platforms, catering to diverse mission requirements. Key product advancements include improved on-board processing, high-throughput antennas, advanced propulsion systems for orbit maintenance and de-orbiting, and enhanced power generation. Applications are expanding beyond traditional broadband to include sophisticated earth observation, IoT connectivity, and secure communications. For instance, Planet Labs' Earth observation satellites provide daily global imagery, while OneWeb Satellites is focused on providing high-speed, low-latency internet for governments, businesses, and communities worldwide. SpaceX's Starlink constellation, comprised of thousands of satellites, exemplifies the trend towards mega-constellations designed for mass-market broadband. The emphasis is on cost-effective manufacturing, rapid deployment cycles, and robust, reliable performance in the harsh space environment.

Key Drivers, Barriers & Challenges in Commercial LEO Satellite

Key Drivers: The Commercial LEO Satellite market is propelled by several significant drivers. The escalating demand for ubiquitous, high-speed, low-latency internet connectivity, particularly in underserved regions, is a primary catalyst. Falling launch costs, thanks to reusable rocket technology championed by companies like SpaceX, have made LEO constellation deployment economically viable. Technological advancements in satellite design, including miniaturization and modularity, enable more affordable and scalable deployments. Growing adoption across industries such as maritime, aviation, and IoT further fuels market expansion. Government initiatives supporting space infrastructure development and the increasing need for resilient communication networks during disasters also act as crucial growth accelerators.

Barriers & Challenges: Despite the immense potential, the LEO satellite market faces considerable barriers and challenges. The immense capital investment required for establishing and maintaining large constellations remains a significant hurdle. Regulatory complexities, including orbital slot allocation, spectrum licensing, and space debris mitigation policies, can slow down deployment and create international coordination issues. Intense competition among constellation operators can lead to price wars and market saturation. Supply chain disruptions, particularly for specialized satellite components, can impact production timelines. Furthermore, the operational challenges of managing thousands of satellites in orbit, including collision avoidance and maintenance, are substantial. The cybersecurity of satellite networks and the data they transmit is also a growing concern. The estimated cost to mitigate space debris, a critical challenge, is projected to exceed $5,000 million annually by 2030.

Emerging Opportunities in Commercial LEO Satellite

Emerging opportunities in the Commercial LEO Satellite sector are diverse and promising. The burgeoning demand for global IoT connectivity is creating a significant market for LEO satellites to support a vast array of sensors and devices in remote or mobile environments. The development of on-orbit servicing, assembly, and manufacturing (OSAM) presents a paradigm shift, enabling satellite repair, refueling, and in-space assembly, extending satellite lifespans and enabling more complex missions. The integration of LEO satellite networks with terrestrial 5G and future wireless technologies, often referred to as "space-terrestrial convergence," promises to deliver seamless global connectivity. Furthermore, the increasing focus on space sustainability and responsible space utilization is opening avenues for companies offering advanced debris removal and space traffic management solutions. The potential for LEO satellites to support high-frequency trading and other time-sensitive financial applications due to their low latency is also a growing area of interest.

Growth Accelerators in the Commercial LEO Satellite Industry

Several key factors are acting as growth accelerators for the Commercial LEO Satellite industry. Continuous advancements in launch vehicle technology, leading to reduced launch costs and increased launch frequency, are critical. Innovations in satellite component miniaturization and mass production techniques significantly lower the per-unit cost of satellites, enabling the deployment of larger constellations. The increasing integration of artificial intelligence (AI) and machine learning (ML) for satellite operations, data analysis, and network management is enhancing efficiency and enabling new service offerings. Strategic partnerships and collaborations between satellite operators, ground infrastructure providers, and application developers are expanding market reach and accelerating service adoption. Government support through research grants, favorable regulations, and direct procurement of satellite services also plays a crucial role in accelerating industry growth. The ongoing development of inter-satellite links (ISLs) is further enhancing network performance and reducing reliance on ground stations, thereby accelerating global coverage.

Key Players Shaping the Commercial LEO Satellite Market

- SpaceX

- Planet Labs

- Boeing

- Lockheed Martin

- Thales Alenia Space

- OneWeb Satellites

- SSL (Space Systems Loral)

- Northrop Grumman

- ISS-Reshetnev

- Kepler Communications

Notable Milestones in Commercial LEO Satellite Sector

- 2019: SpaceX successfully launches its first batch of Starlink satellites, marking a significant step towards its mega-constellation.

- 2020: OneWeb Satellites secures new funding and continues its satellite deployment efforts, focusing on global broadband.

- 2021: Planet Labs announces significant advancements in its Earth observation satellite technology, increasing revisit rates and data resolution.

- 2022: Thales Alenia Space and Northrop Grumman announce collaborations on next-generation LEO satellite platforms and components.

- 2023: SpaceX surpasses 4,000 Starlink satellites in orbit, demonstrating rapid constellation scaling.

- Early 2024: Kepler Communications launches its next-generation satellites, enhancing its data relay and IoT capabilities.

- Mid 2024: Boeing announces plans for new LEO satellite designs optimized for enterprise and government applications.

- Late 2024: ISS-Reshetnev delivers advanced communication payloads for upcoming LEO constellations.

In-Depth Commercial LEO Satellite Market Outlook

The outlook for the Commercial LEO Satellite market is exceptionally robust, driven by sustained technological innovation and expanding global connectivity demands. Growth accelerators such as ongoing reductions in launch costs, advancements in satellite manufacturing, and the increasing sophistication of AI-driven satellite operations will continue to fuel market expansion. Strategic partnerships and the development of space-terrestrial integrated networks are set to unlock unprecedented levels of service accessibility and performance. The market's potential is further amplified by the rise of emerging opportunities like global IoT enablement and on-orbit servicing, which promise to revolutionize how we interact with space. As regulatory frameworks mature and address concerns like space debris, the LEO satellite ecosystem is poised for a period of sustained, high-impact growth, solidifying its role as a cornerstone of future global communication infrastructure. The projected market size of over $120,000 million by 2033 underscores the transformative economic and societal impact anticipated from this dynamic sector.

Commercial LEO Satellite Segmentation

-

1. Application

- 1.1. Remote Area Satellite Network

- 1.2. Marine Operations

- 1.3. Onboard WiFi

- 1.4. Network Disaster Recovery

-

2. Types

- 2.1. Below 50 Kg

- 2.2. 50-500 Kg

- 2.3. Above 500 Kg

Commercial LEO Satellite Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Commercial LEO Satellite Regional Market Share

Geographic Coverage of Commercial LEO Satellite

Commercial LEO Satellite REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Remote Area Satellite Network

- 5.1.2. Marine Operations

- 5.1.3. Onboard WiFi

- 5.1.4. Network Disaster Recovery

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Below 50 Kg

- 5.2.2. 50-500 Kg

- 5.2.3. Above 500 Kg

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Commercial LEO Satellite Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Remote Area Satellite Network

- 6.1.2. Marine Operations

- 6.1.3. Onboard WiFi

- 6.1.4. Network Disaster Recovery

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Below 50 Kg

- 6.2.2. 50-500 Kg

- 6.2.3. Above 500 Kg

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Commercial LEO Satellite Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Remote Area Satellite Network

- 7.1.2. Marine Operations

- 7.1.3. Onboard WiFi

- 7.1.4. Network Disaster Recovery

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Below 50 Kg

- 7.2.2. 50-500 Kg

- 7.2.3. Above 500 Kg

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Commercial LEO Satellite Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Remote Area Satellite Network

- 8.1.2. Marine Operations

- 8.1.3. Onboard WiFi

- 8.1.4. Network Disaster Recovery

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Below 50 Kg

- 8.2.2. 50-500 Kg

- 8.2.3. Above 500 Kg

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Commercial LEO Satellite Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Remote Area Satellite Network

- 9.1.2. Marine Operations

- 9.1.3. Onboard WiFi

- 9.1.4. Network Disaster Recovery

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Below 50 Kg

- 9.2.2. 50-500 Kg

- 9.2.3. Above 500 Kg

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Commercial LEO Satellite Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Remote Area Satellite Network

- 10.1.2. Marine Operations

- 10.1.3. Onboard WiFi

- 10.1.4. Network Disaster Recovery

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Below 50 Kg

- 10.2.2. 50-500 Kg

- 10.2.3. Above 500 Kg

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Commercial LEO Satellite Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Remote Area Satellite Network

- 11.1.2. Marine Operations

- 11.1.3. Onboard WiFi

- 11.1.4. Network Disaster Recovery

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Below 50 Kg

- 11.2.2. 50-500 Kg

- 11.2.3. Above 500 Kg

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 SpaceX

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Planet Labs

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Boeing

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Lockheed Martin

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Thales Alenia Space

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 OneWeb Satellites

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 SSL (Space Systems Loral)

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Northrop Grumman

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 ISS-Reshetnev

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Kepler Communications

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 SpaceX

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Commercial LEO Satellite Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Commercial LEO Satellite Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Commercial LEO Satellite Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Commercial LEO Satellite Volume (K), by Application 2025 & 2033

- Figure 5: North America Commercial LEO Satellite Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Commercial LEO Satellite Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Commercial LEO Satellite Revenue (undefined), by Types 2025 & 2033

- Figure 8: North America Commercial LEO Satellite Volume (K), by Types 2025 & 2033

- Figure 9: North America Commercial LEO Satellite Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Commercial LEO Satellite Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Commercial LEO Satellite Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Commercial LEO Satellite Volume (K), by Country 2025 & 2033

- Figure 13: North America Commercial LEO Satellite Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Commercial LEO Satellite Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Commercial LEO Satellite Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Commercial LEO Satellite Volume (K), by Application 2025 & 2033

- Figure 17: South America Commercial LEO Satellite Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Commercial LEO Satellite Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Commercial LEO Satellite Revenue (undefined), by Types 2025 & 2033

- Figure 20: South America Commercial LEO Satellite Volume (K), by Types 2025 & 2033

- Figure 21: South America Commercial LEO Satellite Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Commercial LEO Satellite Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Commercial LEO Satellite Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Commercial LEO Satellite Volume (K), by Country 2025 & 2033

- Figure 25: South America Commercial LEO Satellite Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Commercial LEO Satellite Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Commercial LEO Satellite Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Commercial LEO Satellite Volume (K), by Application 2025 & 2033

- Figure 29: Europe Commercial LEO Satellite Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Commercial LEO Satellite Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Commercial LEO Satellite Revenue (undefined), by Types 2025 & 2033

- Figure 32: Europe Commercial LEO Satellite Volume (K), by Types 2025 & 2033

- Figure 33: Europe Commercial LEO Satellite Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Commercial LEO Satellite Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Commercial LEO Satellite Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Commercial LEO Satellite Volume (K), by Country 2025 & 2033

- Figure 37: Europe Commercial LEO Satellite Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Commercial LEO Satellite Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Commercial LEO Satellite Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Commercial LEO Satellite Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Commercial LEO Satellite Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Commercial LEO Satellite Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Commercial LEO Satellite Revenue (undefined), by Types 2025 & 2033

- Figure 44: Middle East & Africa Commercial LEO Satellite Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Commercial LEO Satellite Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Commercial LEO Satellite Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Commercial LEO Satellite Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Commercial LEO Satellite Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Commercial LEO Satellite Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Commercial LEO Satellite Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Commercial LEO Satellite Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Commercial LEO Satellite Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Commercial LEO Satellite Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Commercial LEO Satellite Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Commercial LEO Satellite Revenue (undefined), by Types 2025 & 2033

- Figure 56: Asia Pacific Commercial LEO Satellite Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Commercial LEO Satellite Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Commercial LEO Satellite Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Commercial LEO Satellite Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Commercial LEO Satellite Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Commercial LEO Satellite Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Commercial LEO Satellite Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Commercial LEO Satellite Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Commercial LEO Satellite Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Commercial LEO Satellite Revenue undefined Forecast, by Types 2020 & 2033

- Table 4: Global Commercial LEO Satellite Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Commercial LEO Satellite Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Commercial LEO Satellite Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Commercial LEO Satellite Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Commercial LEO Satellite Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Commercial LEO Satellite Revenue undefined Forecast, by Types 2020 & 2033

- Table 10: Global Commercial LEO Satellite Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Commercial LEO Satellite Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Commercial LEO Satellite Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Commercial LEO Satellite Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Commercial LEO Satellite Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Commercial LEO Satellite Revenue undefined Forecast, by Types 2020 & 2033

- Table 22: Global Commercial LEO Satellite Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Commercial LEO Satellite Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Commercial LEO Satellite Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Commercial LEO Satellite Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Commercial LEO Satellite Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Commercial LEO Satellite Revenue undefined Forecast, by Types 2020 & 2033

- Table 34: Global Commercial LEO Satellite Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Commercial LEO Satellite Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Commercial LEO Satellite Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Commercial LEO Satellite Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Commercial LEO Satellite Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Commercial LEO Satellite Revenue undefined Forecast, by Types 2020 & 2033

- Table 58: Global Commercial LEO Satellite Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Commercial LEO Satellite Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Commercial LEO Satellite Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Commercial LEO Satellite Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Commercial LEO Satellite Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Commercial LEO Satellite Revenue undefined Forecast, by Types 2020 & 2033

- Table 76: Global Commercial LEO Satellite Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Commercial LEO Satellite Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Commercial LEO Satellite Volume K Forecast, by Country 2020 & 2033

- Table 79: China Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Commercial LEO Satellite Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Commercial LEO Satellite Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Commercial LEO Satellite?

The projected CAGR is approximately 11.9%.

2. Which companies are prominent players in the Commercial LEO Satellite?

Key companies in the market include SpaceX, Planet Labs, Boeing, Lockheed Martin, Thales Alenia Space, OneWeb Satellites, SSL (Space Systems Loral), Northrop Grumman, ISS-Reshetnev, Kepler Communications.

3. What are the main segments of the Commercial LEO Satellite?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Commercial LEO Satellite," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Commercial LEO Satellite report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Commercial LEO Satellite?

To stay informed about further developments, trends, and reports in the Commercial LEO Satellite, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence