Key Insights

The Automotive Cybersecurity Service market is projected for substantial growth, expected to reach $7.13 billion by 2025, driven by a CAGR of 11.2% from 2025 to 2033. This expansion is attributed to the increasing complexity of vehicle electronics, the widespread adoption of connected car technologies, and the escalating threat of cyberattacks on critical vehicle functions and sensitive data. As vehicles transform into sophisticated software-defined platforms, robust cybersecurity is essential. This necessitates integrated solutions for hardware, software, network security, and specialized services to foster a secure automotive ecosystem. Passenger cars dominate adoption, followed by commercial vehicles, due to their extensive feature sets and the need for operational continuity and fleet data protection.

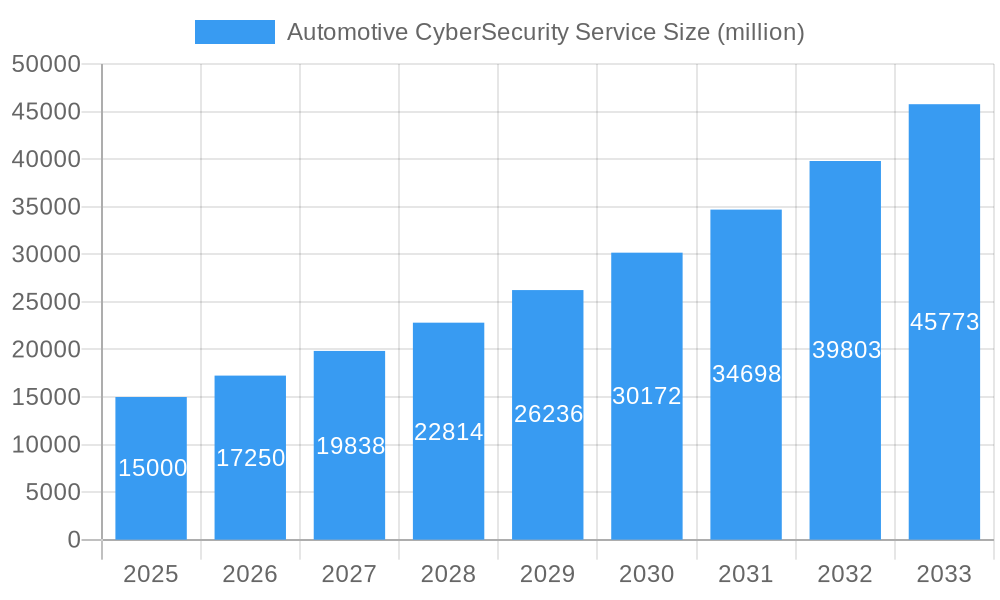

Automotive CyberSecurity Service Market Size (In Billion)

Key market drivers include the proliferation of Advanced Driver-Assistance Systems (ADAS), autonomous driving, and in-car infotainment systems, which expand the potential attack surface. Stringent government regulations and industry standards, such as ISO/SAE 21434, mandate significant investments in cybersecurity by automakers and suppliers. Emerging trends like over-the-air (OTA) updates, vehicle-to-everything (V2X) communication, and the integration of AI in vehicle security further accelerate market growth. Challenges include the high implementation cost of advanced security solutions, a shortage of skilled automotive cybersecurity professionals, and complexities within the diverse supply chain. Nevertheless, the paramount need to protect drivers, vehicles, and sensitive data ensures a dynamic and expanding market for automotive cybersecurity services.

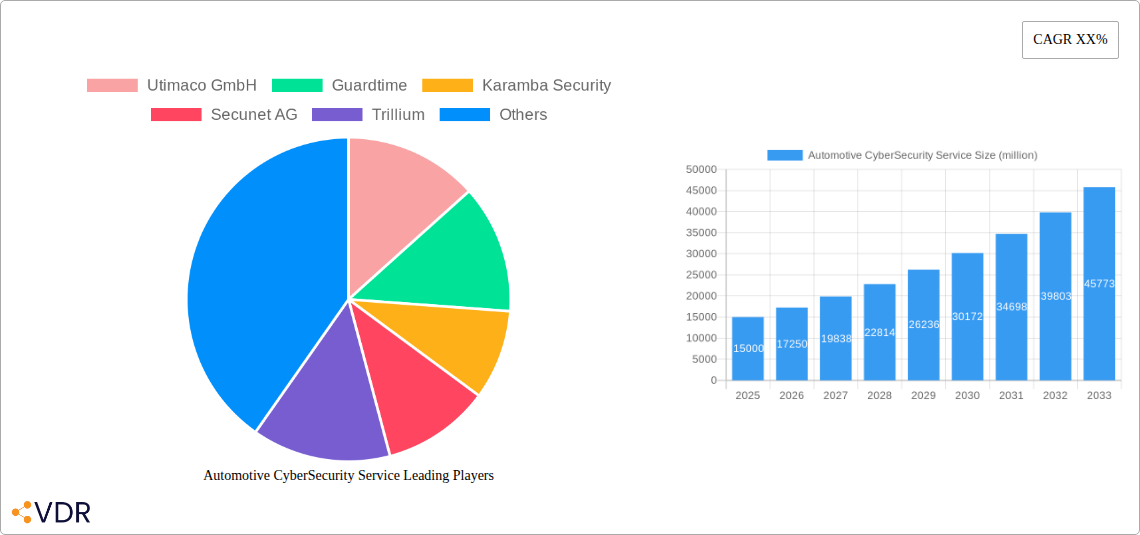

Automotive CyberSecurity Service Company Market Share

Automotive CyberSecurity Service Market Dynamics & Structure

The global automotive cybersecurity service market is characterized by a moderate to highly concentrated structure, with leading players like Intel Corporation, NXP Semiconductors, and BT Security holding significant market share. Technological innovation is a primary driver, fueled by the increasing connectivity and autonomous capabilities of vehicles, necessitating robust protection against sophisticated cyber threats. Regulatory frameworks, such as UN R155 and UNECE WP.29, are progressively mandating cybersecurity measures, further shaping market dynamics and encouraging investment. Competitive product substitutes are emerging, with a focus on integrated hardware and software solutions. End-user demographics are diverse, ranging from individual vehicle owners demanding data privacy to large fleet operators prioritizing operational integrity. Mergers and acquisitions (M&A) are prevalent as companies seek to consolidate expertise, expand product portfolios, and gain market access. For instance, M&A deal volumes in the automotive cybersecurity sector reached an estimated 15 deals in 2024, with an average deal value of over $100 million. Innovation barriers include the long development cycles for automotive components and the need for rigorous testing and validation to meet stringent safety standards.

- Market Concentration: Moderate to High, with key players dominating segments.

- Technological Innovation Drivers: Increasing vehicle connectivity, autonomous driving features, over-the-air (OTA) updates.

- Regulatory Frameworks: UN R155, UNECE WP.29 mandating cybersecurity by design.

- Competitive Product Substitutes: Integrated hardware-software solutions, end-to-end encryption services.

- End-User Demographics: Individual consumers, fleet operators, automotive manufacturers.

- M&A Trends: Consolidating expertise, expanding portfolios, strategic partnerships.

Automotive CyberSecurity Service Growth Trends & Insights

The automotive cybersecurity service market is poised for substantial expansion, driven by an escalating volume of connected vehicles and the inherent vulnerabilities they present. The market size is projected to grow from an estimated $15,000 million in 2024 to over $45,000 million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 13.5% during the forecast period (2025–2033). Adoption rates of advanced cybersecurity solutions are rapidly increasing as automotive manufacturers prioritize passenger safety, data privacy, and brand reputation. Technological disruptions, including the integration of AI and machine learning for threat detection and response, are fundamentally transforming the landscape. Consumer behavior is shifting towards greater awareness and expectation of robust cybersecurity features, influencing purchasing decisions. The increasing complexity of vehicle architectures, with numerous ECUs and interconnected systems, creates a larger attack surface, making comprehensive cybersecurity strategies indispensable.

The rise of software-defined vehicles and the proliferation of connected services such as telematics, infotainment, and autonomous driving functionalities are key contributors to this growth. Each new connected feature introduces potential entry points for malicious actors, necessitating continuous monitoring, threat intelligence, and robust defense mechanisms. The adoption of Hardware Security Modules (HSMs) and secure boot processes are becoming standard, alongside advanced intrusion detection and prevention systems (IDPS). Furthermore, the growing adoption of over-the-air (OTA) updates, while offering convenience and efficiency, also introduces risks associated with software integrity and secure deployment, thereby driving demand for specialized OTA security services. The market penetration of cybersecurity solutions, which stood at around 60% for new passenger vehicles in 2024, is expected to climb to over 90% by 2033. This upward trajectory is further bolstered by the increasing regulatory mandates that are transforming cybersecurity from a discretionary feature to a fundamental requirement. The evolving threat landscape, marked by increasingly sophisticated attacks targeting vehicle control systems, safety features, and personal data, compels the industry to invest proactively in advanced cybersecurity.

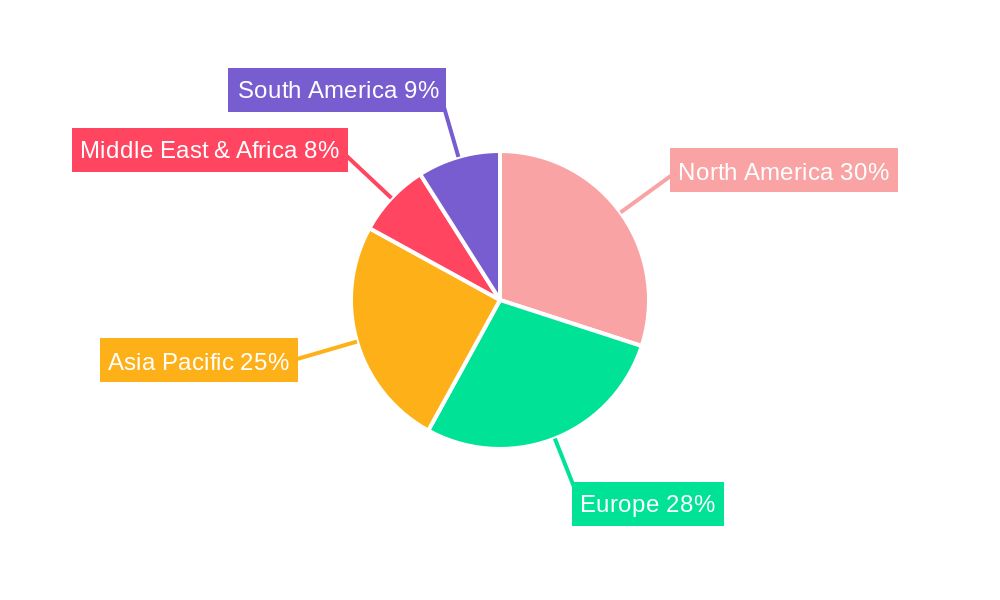

Dominant Regions, Countries, or Segments in Automotive CyberSecurity Service

North America, specifically the United States, currently leads the automotive cybersecurity service market. This dominance is attributed to a confluence of factors including a highly developed automotive industry, stringent data privacy regulations like CCPA, and a strong emphasis on technological innovation. The region's significant investment in autonomous vehicle research and development, coupled with a proactive stance on cybersecurity mandates, has positioned it as a frontrunner. The passenger car segment within the Application vertical is the largest contributor to market revenue, accounting for approximately 75% of the total market in 2024, driven by the sheer volume of vehicles produced and the increasing integration of advanced cyber-physical systems.

- Leading Region: North America (particularly the United States).

- Key Drivers: Advanced R&D in autonomous driving, robust regulatory landscape (CCPA), high adoption of connected car technologies, significant automotive manufacturing base.

- Market Share: Estimated 35% of global market in 2024.

- Growth Potential: High, driven by continued innovation and strict compliance requirements.

Within the Types segment, Software-based cybersecurity solutions are experiencing the most rapid growth, projected to capture over 50% of the market by 2033. This surge is fueled by the increasing complexity of in-vehicle software, the need for continuous updates, and the ability of software to adapt to evolving threats. Network & Cloud cybersecurity is also a rapidly expanding segment, as vehicles become increasingly reliant on cloud connectivity for services, data analytics, and remote diagnostics, requiring secure communication channels and data protection.

- Dominant Segment (Type): Software-based Cybersecurity Solutions.

- Market Share (2024): Approximately 45%.

- Growth Drivers: Over-the-air (OTA) updates, in-vehicle infotainment systems, connected car services, increasing software complexity.

- Future Outlook: Expected to be the fastest-growing segment.

Security Services & Frameworks also play a critical role, encompassing threat intelligence, risk assessment, and incident response, which are essential for maintaining the overall security posture of vehicles throughout their lifecycle. The market share for Security Services & Frameworks was approximately 20% in 2024, with strong growth anticipated due to the increasing need for managed security solutions.

Automotive CyberSecurity Service Product Landscape

The automotive cybersecurity service product landscape is characterized by a diverse range of solutions designed to protect vehicles from a wide array of cyber threats. Innovations include sophisticated intrusion detection and prevention systems (IDPS) capable of real-time monitoring of in-vehicle networks, secure communication protocols for vehicle-to-everything (V2X) communication, and robust authentication mechanisms for over-the-air (OTA) updates. Companies are also developing advanced encryption solutions and secure hardware modules (HSMs) to safeguard sensitive data and critical vehicle functions. The performance metrics for these products are evaluated based on their ability to detect and mitigate threats with minimal latency, their compatibility with existing automotive architectures, and their adherence to industry-specific security standards. Unique selling propositions often lie in the integrated nature of solutions, offering comprehensive protection across the vehicle's digital ecosystem.

Key Drivers, Barriers & Challenges in Automotive CyberSecurity Service

The automotive cybersecurity service market is propelled by several key drivers, including the escalating number of connected vehicles, the growing sophistication of cyber threats, and the increasing regulatory pressure for enhanced security. Technological advancements in areas like AI for threat detection and the demand for secure over-the-air (OTA) updates also fuel market expansion.

- Key Drivers:

- Increasing connectivity and autonomous features in vehicles.

- Rising sophistication of cyberattacks targeting vehicles.

- Stringent government regulations and industry standards (e.g., UN R155).

- Demand for secure data privacy and protection of sensitive information.

Conversely, significant barriers and challenges impede market growth. The sheer complexity of automotive electronic systems and the long product development cycles pose considerable obstacles. Supply chain vulnerabilities and the need for extensive integration and testing across diverse vehicle platforms present further hurdles. Furthermore, the high cost of implementing and maintaining advanced cybersecurity solutions can be a deterrent for some manufacturers and consumers.

- Key Barriers & Challenges:

- Complexity of automotive architectures and long development cycles.

- Supply chain integration and the need for interoperability.

- High implementation and maintenance costs.

- Talent shortage in specialized cybersecurity expertise.

Emerging Opportunities in Automotive CyberSecurity Service

Emerging opportunities in automotive cybersecurity lie in the development of predictive threat intelligence platforms leveraging AI and machine learning, offering proactive defense mechanisms. The growing demand for secure software-defined vehicle architectures presents significant potential for companies specializing in secure OTA update management and continuous security monitoring. Furthermore, the expansion of the connected services ecosystem, including mobility-as-a-service (MaaS) and vehicle-to-grid (V2G) technologies, creates new avenues for specialized cybersecurity solutions focused on securing these emerging platforms and ensuring the integrity of vast amounts of data being generated and transmitted. The evolving cybersecurity needs for commercial vehicles, particularly in logistics and transportation, also represent an untapped market segment.

Growth Accelerators in the Automotive CyberSecurity Service Industry

Long-term growth in the automotive cybersecurity service industry is being accelerated by significant technological breakthroughs in areas like post-quantum cryptography, which will be crucial for protecting future vehicles from advanced computational threats. Strategic partnerships between traditional automotive manufacturers, Tier-1 suppliers, and specialized cybersecurity firms are fostering innovation and creating comprehensive security ecosystems. The ongoing globalization of the automotive supply chain, coupled with varying regional regulations, is also driving market expansion as companies seek unified cybersecurity strategies that can be implemented globally. Furthermore, the increasing adoption of cybersecurity-as-a-service (CaaS) models is making advanced security solutions more accessible to a wider range of automotive players, thus democratizing cybersecurity and fostering widespread adoption.

Key Players Shaping the Automotive CyberSecurity Service Market

- Utimaco GmbH

- Guardtime

- Karamba Security

- Secunet AG

- Trillium

- NXP Semiconductors

- Intel Corporation

- BT Security

- Argus

- SBD Automotive & Ncc Group

- Harman (TowerSec)

- Arilou technologies

Notable Milestones in Automotive CyberSecurity Service Sector

- 2019: ISO/SAE 21434 standard for automotive cybersecurity published, providing a framework for security throughout the vehicle lifecycle.

- 2020: UN R155 regulation released, mandating cybersecurity management systems for vehicle type approval.

- 2021: Major automotive manufacturers begin integrating dedicated cybersecurity teams and investing heavily in threat intelligence platforms.

- 2022: Significant increase in reported vehicle hacking incidents, raising consumer and industry awareness.

- 2023: Emergence of specialized cybersecurity solutions for electric vehicles (EVs) and charging infrastructure.

- 2024: Increased adoption of AI-driven cybersecurity solutions for real-time threat detection and response.

In-Depth Automotive CyberSecurity Service Market Outlook

The automotive cybersecurity service market is projected for robust and sustained growth, driven by an inextricable link between vehicle innovation and security imperatives. The continuous evolution of autonomous driving technologies, the expansion of connected car services, and the increasing reliance on over-the-air updates will necessitate increasingly sophisticated and adaptable cybersecurity solutions. The market's trajectory indicates a shift from reactive security measures to proactive, AI-driven predictive defense systems. Strategic collaborations between automotive OEMs, technology providers, and cybersecurity experts will be pivotal in developing comprehensive, end-to-end security frameworks that can adapt to emerging threats. The growing global regulatory landscape, with more countries enacting stringent cybersecurity mandates, will act as a powerful catalyst, ensuring that cybersecurity remains a top priority throughout the entire automotive value chain, creating significant opportunities for market expansion and innovation.

Automotive CyberSecurity Service Segmentation

-

1. Application

- 1.1. Passenger Cars

- 1.2. Commercial Vehicles

-

2. Types

- 2.1. Software-based

- 2.2. Hardware-based

- 2.3. Network & Cloud

- 2.4. Security Services & Frameworks

Automotive CyberSecurity Service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive CyberSecurity Service Regional Market Share

Geographic Coverage of Automotive CyberSecurity Service

Automotive CyberSecurity Service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Cars

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Software-based

- 5.2.2. Hardware-based

- 5.2.3. Network & Cloud

- 5.2.4. Security Services & Frameworks

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Automotive CyberSecurity Service Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Cars

- 6.1.2. Commercial Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Software-based

- 6.2.2. Hardware-based

- 6.2.3. Network & Cloud

- 6.2.4. Security Services & Frameworks

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Automotive CyberSecurity Service Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Cars

- 7.1.2. Commercial Vehicles

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Software-based

- 7.2.2. Hardware-based

- 7.2.3. Network & Cloud

- 7.2.4. Security Services & Frameworks

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Automotive CyberSecurity Service Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Cars

- 8.1.2. Commercial Vehicles

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Software-based

- 8.2.2. Hardware-based

- 8.2.3. Network & Cloud

- 8.2.4. Security Services & Frameworks

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Automotive CyberSecurity Service Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Cars

- 9.1.2. Commercial Vehicles

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Software-based

- 9.2.2. Hardware-based

- 9.2.3. Network & Cloud

- 9.2.4. Security Services & Frameworks

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Automotive CyberSecurity Service Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Cars

- 10.1.2. Commercial Vehicles

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Software-based

- 10.2.2. Hardware-based

- 10.2.3. Network & Cloud

- 10.2.4. Security Services & Frameworks

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Automotive CyberSecurity Service Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Passenger Cars

- 11.1.2. Commercial Vehicles

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Software-based

- 11.2.2. Hardware-based

- 11.2.3. Network & Cloud

- 11.2.4. Security Services & Frameworks

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Utimaco GmbH

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Guardtime

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Karamba Security

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Secunet AG

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Trillium

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 NXP Semiconductors

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Intel Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 BT Security

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Argus

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 SBD Automotive & Ncc Group

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Harman (TowerSec)

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Arilou technologies

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Utimaco GmbH

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Automotive CyberSecurity Service Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Automotive CyberSecurity Service Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Automotive CyberSecurity Service Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive CyberSecurity Service Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Automotive CyberSecurity Service Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automotive CyberSecurity Service Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Automotive CyberSecurity Service Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive CyberSecurity Service Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Automotive CyberSecurity Service Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive CyberSecurity Service Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Automotive CyberSecurity Service Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automotive CyberSecurity Service Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Automotive CyberSecurity Service Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive CyberSecurity Service Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Automotive CyberSecurity Service Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive CyberSecurity Service Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Automotive CyberSecurity Service Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automotive CyberSecurity Service Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Automotive CyberSecurity Service Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive CyberSecurity Service Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive CyberSecurity Service Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive CyberSecurity Service Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automotive CyberSecurity Service Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automotive CyberSecurity Service Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive CyberSecurity Service Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive CyberSecurity Service Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive CyberSecurity Service Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive CyberSecurity Service Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Automotive CyberSecurity Service Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automotive CyberSecurity Service Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive CyberSecurity Service Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive CyberSecurity Service Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Automotive CyberSecurity Service Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Automotive CyberSecurity Service Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Automotive CyberSecurity Service Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Automotive CyberSecurity Service Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Automotive CyberSecurity Service Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive CyberSecurity Service Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Automotive CyberSecurity Service Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Automotive CyberSecurity Service Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive CyberSecurity Service Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Automotive CyberSecurity Service Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Automotive CyberSecurity Service Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive CyberSecurity Service Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Automotive CyberSecurity Service Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Automotive CyberSecurity Service Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive CyberSecurity Service Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Automotive CyberSecurity Service Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Automotive CyberSecurity Service Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive CyberSecurity Service Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive CyberSecurity Service?

The projected CAGR is approximately 11.2%.

2. Which companies are prominent players in the Automotive CyberSecurity Service?

Key companies in the market include Utimaco GmbH, Guardtime, Karamba Security, Secunet AG, Trillium, NXP Semiconductors, Intel Corporation, BT Security, Argus, SBD Automotive & Ncc Group, Harman (TowerSec), Arilou technologies.

3. What are the main segments of the Automotive CyberSecurity Service?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.13 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive CyberSecurity Service," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive CyberSecurity Service report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive CyberSecurity Service?

To stay informed about further developments, trends, and reports in the Automotive CyberSecurity Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence