Key Insights

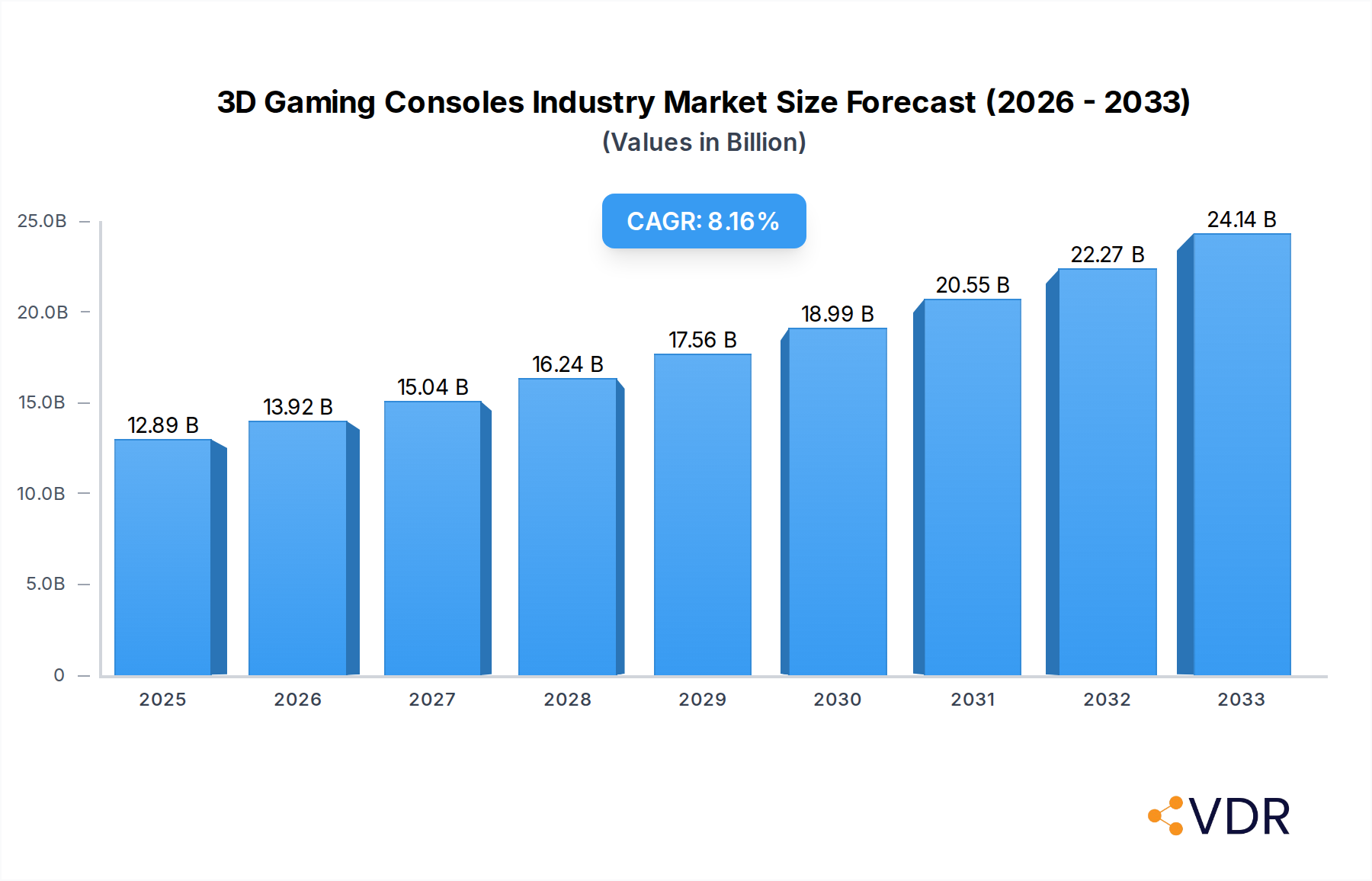

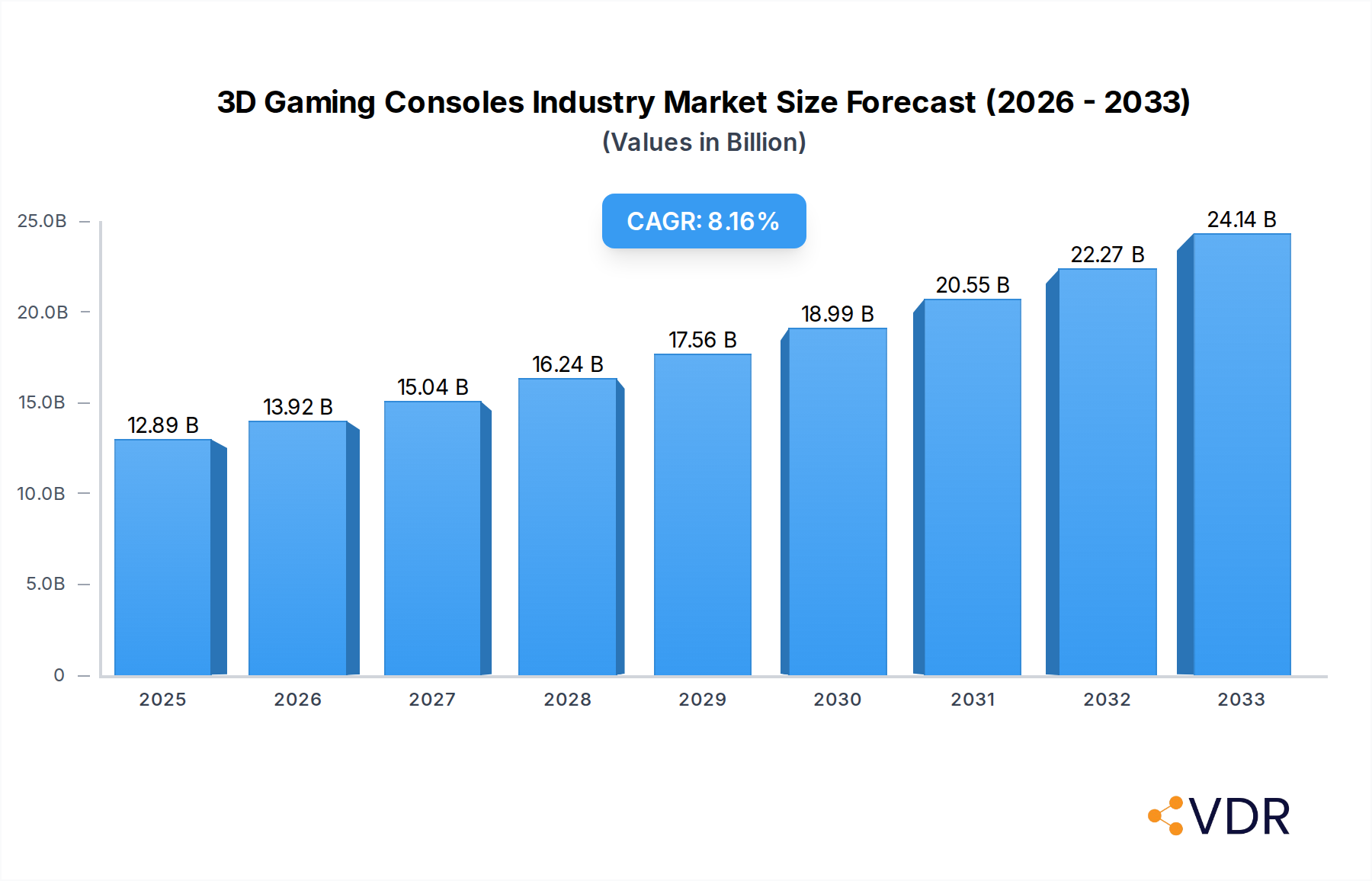

The 3D Gaming Consoles industry is poised for significant expansion, projecting a robust market size of $12.888 billion in 2025, driven by an anticipated Compound Annual Growth Rate (CAGR) of 8.21%. This impressive growth is fueled by an evolving entertainment landscape and advancements in immersive technologies. Key drivers include the increasing adoption of virtual reality (VR) and augmented reality (AR) technologies, which are transforming the gaming experience and opening up new avenues for console manufacturers. Furthermore, the persistent demand for high-fidelity graphics and more interactive gameplay continues to push innovation in hardware and software development. The market is experiencing a surge in demand for more powerful and versatile consoles capable of rendering complex 3D environments, offering players unparalleled levels of realism and engagement. This technological evolution is supported by a growing global gaming community with increasing disposable income dedicated to entertainment.

3D Gaming Consoles Industry Market Size (In Billion)

The industry's trajectory is further shaped by key trends such as the growing popularity of cloud gaming, which allows for access to high-end gaming experiences on less powerful hardware, thereby broadening the potential consumer base. The expansion of online multiplayer capabilities and the development of innovative peripherals like motion controllers and advanced haptic feedback systems are also contributing to market dynamism. While the market is robust, potential restraints include the high cost of entry for cutting-edge 3D gaming hardware and the ongoing challenge of developing compelling content that fully leverages the capabilities of new console generations. However, the strong consumer appetite for advanced gaming experiences, coupled with ongoing technological advancements and strategic market expansions by major players like Sony, Microsoft, and Nintendo, suggests a highly promising future for the 3D Gaming Consoles industry. The diverse segmentation, encompassing both hardware and software components across various console types and platforms, indicates a broad market appeal and multiple avenues for revenue generation.

3D Gaming Consoles Industry Company Market Share

Unveiling the Future of Immersive Entertainment: 3D Gaming Consoles Industry Report

Dive deep into the dynamic 3D Gaming Consoles Industry with our comprehensive report, engineered to empower industry professionals, investors, and tech enthusiasts with actionable insights. Explore the evolving landscape of gaming hardware and software, from cutting-edge home consoles to portable powerhouses, and understand the pivotal role of key players in shaping this multi-billion dollar market. Our analysis spans the crucial Study Period of 2019–2033, with a Base Year of 2025, and offers a granular Forecast Period of 2025–2033, building upon a robust Historical Period from 2019–2024.

This report is meticulously optimized with high-traffic keywords such as "gaming consoles," "3D gaming," "next-gen consoles," "virtual reality gaming," "console market share," "gaming hardware," "gaming software," "handheld consoles," "home consoles," "Microsoft Xbox," "Sony PlayStation," "Nintendo Wii," and "blockchain gaming consoles," ensuring maximum search engine visibility. Discover detailed market segmentation, regional dominance, and key growth drivers within the parent and child market structures, providing a 360-degree view of this exhilarating industry.

3D Gaming Consoles Industry Market Dynamics & Structure

The 3D Gaming Consoles Industry is characterized by intense competition and rapid technological advancement, driving significant market concentration among established giants while creating space for innovative newcomers. Microsoft Corporation, Sony Corporation, and Nintendo Co Ltd continue to dominate the hardware space, their strategic investments in R&D and exclusive content fueling consumer demand. Technological innovation is primarily driven by advancements in graphics processing, virtual reality (VR) integration, and cloud gaming capabilities, pushing the boundaries of immersive experiences. Regulatory frameworks, while generally supportive of innovation, often focus on content rating, data privacy, and consumer protection. Competitive product substitutes are emerging from PC gaming, mobile gaming, and increasing adoption of AR/VR technologies that blur the lines of traditional console gaming. End-user demographics are broadening, with a significant increase in casual gamers and a growing appeal to older age groups. Mergers and acquisitions (M&A) trends, though less frequent in the core console manufacturing, are prevalent in the software and peripheral sectors, with companies like Activision Publishing Inc. and Electronic Arts Inc. constantly evaluating strategic alliances and acquisitions to bolster their content portfolios.

- Market Concentration: Dominated by the "big three" (Sony, Microsoft, Nintendo), with a significant portion of market share held by these entities.

- Technological Innovation Drivers: Advancements in GPU and CPU technology, AI integration for enhanced gameplay, VR/AR headset compatibility, and low-latency cloud streaming services.

- Regulatory Frameworks: Focus on age ratings (ESRB, PEGI), data security, and antitrust regulations impacting market consolidation.

- Competitive Product Substitutes: High-end gaming PCs, advanced mobile gaming devices, and standalone VR/AR headsets.

- End-User Demographics: A diverse base ranging from young adults to older demographics, with a growing interest in family-friendly and educational gaming experiences.

- M&A Trends: Strategic acquisitions of game development studios and integration of emerging technologies like AI and blockchain.

3D Gaming Consoles Industry Growth Trends & Insights

The global 3D Gaming Consoles Industry is poised for substantial growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 10-12% over the forecast period. This impressive trajectory is fueled by a confluence of factors, including escalating consumer disposable income, increasing internet penetration, and a burgeoning appetite for high-fidelity, immersive gaming experiences. The adoption rates of next-generation consoles, featuring advanced 3D graphics capabilities and ray tracing technology, have been robust, signaling a strong consumer willingness to invest in premium gaming hardware. Technological disruptions, particularly the seamless integration of virtual and augmented reality into mainstream gaming, are creating entirely new avenues for engagement and revenue generation. Consumer behavior is shifting dramatically, with a greater emphasis on online multiplayer experiences, the integration of social features within gaming platforms, and a growing demand for subscription-based gaming services offering access to vast game libraries. The parent market, encompassing all video gaming, provides a stable foundation, while the child market of specialized 3D gaming consoles experiences accelerated growth due to its niche but highly engaged audience. The market penetration of dedicated 3D gaming hardware is steadily increasing, moving beyond early adopters to a more mainstream consumer base.

- Market Size Evolution: The global market is expected to reach over $150 billion by 2033, from an estimated $75 billion in 2025.

- Adoption Rates: Next-generation console adoption is projected to exceed 70% of console-owning households by 2028.

- Technological Disruptions: The widespread adoption of VR/AR accessories and cloud gaming services is revolutionizing gameplay accessibility and immersion.

- Consumer Behavior Shifts: Increased spending on in-game content and digital game downloads, alongside a growing preference for subscription models.

- CAGR: Projected at 10-12% from 2025 to 2033.

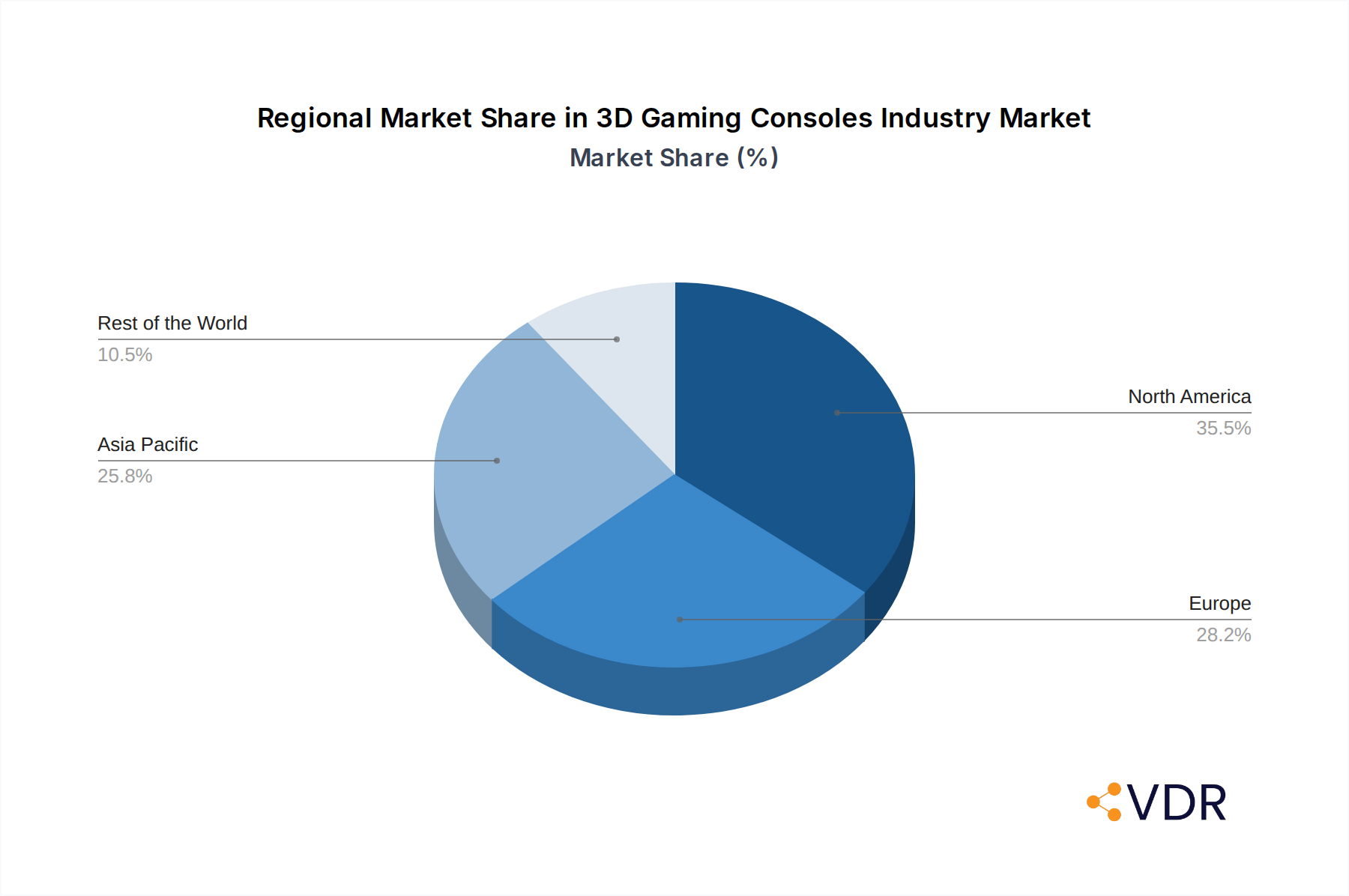

Dominant Regions, Countries, or Segments in 3D Gaming Consoles Industry

North America, particularly the United States, currently stands as the dominant region in the 3D Gaming Consoles Industry, driven by a combination of high disposable incomes, a technologically savvy population, and a deeply ingrained gaming culture. The segment of Home Consoles is the primary revenue generator, with the latest iterations from Sony PlayStation and Microsoft Xbox captivating a vast consumer base. Key drivers for this dominance include robust economic policies supporting consumer spending on entertainment, well-developed digital infrastructure facilitating online gaming and content delivery, and a mature market for AAA game titles. The Hardware segment, encompassing the consoles themselves and their peripherals like controllers and VR headsets, is the bedrock of this market. Sony Corporation and Microsoft Corporation, with their extensive brand recognition and established ecosystems, command significant market share.

However, significant growth potential is also observed in the Handheld Consoles segment, particularly in regions like Asia, where mobile gaming has a strong foothold and the appeal of portable, high-quality gaming experiences is immense. Nintendo Co Ltd has historically shown strong performance in this segment. The Software segment, while crucial globally, sees its value amplified by the hardware sales in dominant regions. Countries like Japan, while a smaller overall market, are critical innovation hubs, especially for Nintendo. The increasing accessibility and affordability of Micro Consoles and dedicated gaming devices are also beginning to carve out niches, appealing to budget-conscious consumers or those seeking specific entertainment solutions. The "Other Platforms" category, while diverse, includes emerging technologies and specialized devices that contribute to the overall market dynamism.

- Dominant Region: North America, with the United States as the leading country.

- Dominant Segment (Primary): Home Consoles (Hardware and Software).

- Key Drivers in North America: High disposable income, strong consumer demand for advanced technology, extensive digital infrastructure.

- Market Share Leadership: Sony PlayStation and Microsoft Xbox leading the Home Console segment.

- Emerging Growth Segment: Handheld Consoles, with strong potential in Asia.

- Key Countries for Innovation: Japan (Nintendo), USA (Microsoft, Sony).

- Contributing Segments: Micro Consoles and Dedicated Consoles are expanding their market presence.

3D Gaming Consoles Industry Product Landscape

The 3D Gaming Consoles Industry product landscape is defined by continuous innovation aimed at delivering unparalleled visual fidelity and immersive gameplay. Next-generation consoles like the PlayStation 5 and Xbox Series X/S are at the forefront, boasting powerful custom GPUs capable of real-time ray tracing, 4K resolution at high frame rates, and ultra-fast SSDs for significantly reduced load times. Virtual Reality integration is a key differentiator, with headsets like Oculus VR offering expansive 3D gaming worlds. Logitech Inc. and Guillemot Corporation SA (Thrustmaster) are instrumental in providing advanced peripherals, from ergonomic controllers to realistic racing wheels, enhancing the tactile experience. Sony’s recent launch of the Gray Camouflage Collection, featuring coordinated accessories, exemplifies a focus on aesthetic appeal alongside performance.

Key Drivers, Barriers & Challenges in 3D Gaming Consoles Industry

Key Drivers:

- Technological Advancements: Continuous innovation in GPU and CPU power, VR/AR integration, and AI-driven gameplay experiences.

- Growing Demand for Immersive Entertainment: Consumers increasingly seek high-fidelity, interactive experiences that transcend traditional media.

- Expansion of Online Multiplayer and Cloud Gaming: Facilitates wider accessibility and social interaction within gaming.

- Content Ecosystem Growth: Exclusive titles and a diverse range of third-party games fuel console sales and hardware upgrades.

- Increasing Disposable Income: Particularly in emerging markets, enabling greater consumer spending on premium gaming products.

Barriers & Challenges:

- High Development Costs: Creating cutting-edge 3D games and hardware requires substantial R&D investment.

- Supply Chain Disruptions: Geopolitical factors and component shortages can impact production and availability, as seen in recent years.

- Console Obsolescence: Rapid technological evolution can lead to shorter hardware lifecycles and significant upfront costs for consumers.

- Market Saturation and Competition: Intense competition from PC and mobile gaming platforms requires continuous differentiation.

- Regulatory Hurdles: Evolving regulations regarding data privacy, content moderation, and potential antitrust scrutiny.

- Cybersecurity Threats: Protecting user data and preventing online cheating are ongoing challenges.

Emerging Opportunities in 3D Gaming Consoles Industry

Emerging opportunities within the 3D Gaming Consoles Industry are abundant, driven by technological convergence and evolving consumer preferences. The integration of blockchain technology into gaming consoles, as exemplified by Zilliqa Blockchain's Web3 gaming console initiative, presents a significant frontier for digital ownership and decentralized gaming economies. The continued refinement and broader adoption of VR and AR technologies promise more deeply immersive and interactive gaming experiences, potentially merging physical and virtual worlds. Furthermore, the growth of cloud gaming services is democratizing access to high-end gaming, reducing the reliance on expensive hardware and expanding the potential consumer base. The development of more sophisticated AI for game development and in-game experiences offers opportunities for richer narratives and more dynamic gameplay.

Growth Accelerators in the 3D Gaming Consoles Industry Industry

The long-term growth of the 3D Gaming Consoles Industry is significantly accelerated by strategic technological breakthroughs and evolving market strategies. The relentless pursuit of higher graphical fidelity, including advancements in real-time ray tracing and photorealistic rendering, continues to captivate consumers. Strategic partnerships between console manufacturers and major game developers, ensuring exclusive content and leveraging established IP, are critical for driving hardware sales and maintaining ecosystem loyalty. Furthermore, the expansion of cloud gaming infrastructure and services, enabling seamless cross-platform play and instant access to game libraries, is a major catalyst for market growth. The increasing integration of AI not only enhances gameplay but also streamlines game development processes, leading to a more robust and diverse content pipeline.

Key Players Shaping the 3D Gaming Consoles Industry Market

- Guillemot Corporation SA (Thrustmaster)

- Logitech Inc

- Microsoft Corporation

- Activision Publishing Inc

- Kaneva LLC

- Nintendo Co Ltd

- Electronic Arts Inc

- Sony Corporation

- A4Tech Co Ltd

- Oculus VR

Notable Milestones in 3D Gaming Consoles Industry Sector

- September 2022: Zilliqa Blockchain launched the world's first Web3 games console. With the gaming industry proving itself time and time again as a productive medium for leveraging blockchain technology, Layer-1 blockchain Zilliqa revealed its plans to introduce the world's first Web3 hardware console and gaming hub.

- September 2022: Sony Interactive Entertainment announced the launch of the Gray Camouflage Collection. The Gray Camouflage Collection features a matching set of accessories with the DualSense wireless controller, PS5 console covers for the PS5 with the Ultra HD Blu-ray disc drive, Pulse 3D wireless headset, and the PS5 Digital Edition. The PlayStation design team reimagined the camouflage pattern to reflect a fresher and more contemporary feel.

In-Depth 3D Gaming Consoles Industry Market Outlook

The future outlook for the 3D Gaming Consoles Industry is exceptionally bright, with sustained growth fueled by ongoing technological innovation and an expanding global consumer base. The strategic expansion of cloud gaming infrastructure and the increasing adoption of advanced VR/AR technologies are set to redefine interactive entertainment, offering more accessible and immersive experiences. The development of AI-powered gameplay and content creation tools will lead to richer, more dynamic game worlds. Furthermore, the exploration and integration of blockchain technology promise new models for digital asset ownership and player engagement, creating novel revenue streams and fostering decentralized gaming ecosystems. Console manufacturers will continue to invest heavily in exclusive content and robust online services, solidifying their ecosystems and driving hardware upgrades, positioning the industry for continued dominance in the entertainment sector.

3D Gaming Consoles Industry Segmentation

-

1. Component

- 1.1. Hardware

- 1.2. Software

-

2. Console

- 2.1. Home Consoles

- 2.2. Handheld Consoles

- 2.3. Micro Consoles

- 2.4. Dedicated Consoles

-

3. Platform

- 3.1. Microsoft Xbox

- 3.2. Sony PlayStation

- 3.3. Nintendo Wii

- 3.4. Other Platforms

3D Gaming Consoles Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Rest of Asia Pacific

- 4. Rest of the World

3D Gaming Consoles Industry Regional Market Share

Geographic Coverage of 3D Gaming Consoles Industry

3D Gaming Consoles Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.21% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Hardware

- 5.1.2. Software

- 5.2. Market Analysis, Insights and Forecast - by Console

- 5.2.1. Home Consoles

- 5.2.2. Handheld Consoles

- 5.2.3. Micro Consoles

- 5.2.4. Dedicated Consoles

- 5.3. Market Analysis, Insights and Forecast - by Platform

- 5.3.1. Microsoft Xbox

- 5.3.2. Sony PlayStation

- 5.3.3. Nintendo Wii

- 5.3.4. Other Platforms

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Global 3D Gaming Consoles Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Hardware

- 6.1.2. Software

- 6.2. Market Analysis, Insights and Forecast - by Console

- 6.2.1. Home Consoles

- 6.2.2. Handheld Consoles

- 6.2.3. Micro Consoles

- 6.2.4. Dedicated Consoles

- 6.3. Market Analysis, Insights and Forecast - by Platform

- 6.3.1. Microsoft Xbox

- 6.3.2. Sony PlayStation

- 6.3.3. Nintendo Wii

- 6.3.4. Other Platforms

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. North America 3D Gaming Consoles Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Component

- 7.1.1. Hardware

- 7.1.2. Software

- 7.2. Market Analysis, Insights and Forecast - by Console

- 7.2.1. Home Consoles

- 7.2.2. Handheld Consoles

- 7.2.3. Micro Consoles

- 7.2.4. Dedicated Consoles

- 7.3. Market Analysis, Insights and Forecast - by Platform

- 7.3.1. Microsoft Xbox

- 7.3.2. Sony PlayStation

- 7.3.3. Nintendo Wii

- 7.3.4. Other Platforms

- 7.1. Market Analysis, Insights and Forecast - by Component

- 8. Europe 3D Gaming Consoles Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Component

- 8.1.1. Hardware

- 8.1.2. Software

- 8.2. Market Analysis, Insights and Forecast - by Console

- 8.2.1. Home Consoles

- 8.2.2. Handheld Consoles

- 8.2.3. Micro Consoles

- 8.2.4. Dedicated Consoles

- 8.3. Market Analysis, Insights and Forecast - by Platform

- 8.3.1. Microsoft Xbox

- 8.3.2. Sony PlayStation

- 8.3.3. Nintendo Wii

- 8.3.4. Other Platforms

- 8.1. Market Analysis, Insights and Forecast - by Component

- 9. Asia Pacific 3D Gaming Consoles Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Component

- 9.1.1. Hardware

- 9.1.2. Software

- 9.2. Market Analysis, Insights and Forecast - by Console

- 9.2.1. Home Consoles

- 9.2.2. Handheld Consoles

- 9.2.3. Micro Consoles

- 9.2.4. Dedicated Consoles

- 9.3. Market Analysis, Insights and Forecast - by Platform

- 9.3.1. Microsoft Xbox

- 9.3.2. Sony PlayStation

- 9.3.3. Nintendo Wii

- 9.3.4. Other Platforms

- 9.1. Market Analysis, Insights and Forecast - by Component

- 10. Rest of the World 3D Gaming Consoles Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Component

- 10.1.1. Hardware

- 10.1.2. Software

- 10.2. Market Analysis, Insights and Forecast - by Console

- 10.2.1. Home Consoles

- 10.2.2. Handheld Consoles

- 10.2.3. Micro Consoles

- 10.2.4. Dedicated Consoles

- 10.3. Market Analysis, Insights and Forecast - by Platform

- 10.3.1. Microsoft Xbox

- 10.3.2. Sony PlayStation

- 10.3.3. Nintendo Wii

- 10.3.4. Other Platforms

- 10.1. Market Analysis, Insights and Forecast - by Component

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Guillemot Corporation SA (Thrustmaster)

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Logitech Inc

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Microsoft Corporation

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Activision Publishing Inc

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Kaneva LLC

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Nintendo Co Ltd

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Electronic Art Inc

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Sony Corporatio

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 A4Tech Co Ltd

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Oculus VR

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 Guillemot Corporation SA (Thrustmaster)

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global 3D Gaming Consoles Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America 3D Gaming Consoles Industry Revenue (billion), by Component 2025 & 2033

- Figure 3: North America 3D Gaming Consoles Industry Revenue Share (%), by Component 2025 & 2033

- Figure 4: North America 3D Gaming Consoles Industry Revenue (billion), by Console 2025 & 2033

- Figure 5: North America 3D Gaming Consoles Industry Revenue Share (%), by Console 2025 & 2033

- Figure 6: North America 3D Gaming Consoles Industry Revenue (billion), by Platform 2025 & 2033

- Figure 7: North America 3D Gaming Consoles Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 8: North America 3D Gaming Consoles Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: North America 3D Gaming Consoles Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe 3D Gaming Consoles Industry Revenue (billion), by Component 2025 & 2033

- Figure 11: Europe 3D Gaming Consoles Industry Revenue Share (%), by Component 2025 & 2033

- Figure 12: Europe 3D Gaming Consoles Industry Revenue (billion), by Console 2025 & 2033

- Figure 13: Europe 3D Gaming Consoles Industry Revenue Share (%), by Console 2025 & 2033

- Figure 14: Europe 3D Gaming Consoles Industry Revenue (billion), by Platform 2025 & 2033

- Figure 15: Europe 3D Gaming Consoles Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 16: Europe 3D Gaming Consoles Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Europe 3D Gaming Consoles Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific 3D Gaming Consoles Industry Revenue (billion), by Component 2025 & 2033

- Figure 19: Asia Pacific 3D Gaming Consoles Industry Revenue Share (%), by Component 2025 & 2033

- Figure 20: Asia Pacific 3D Gaming Consoles Industry Revenue (billion), by Console 2025 & 2033

- Figure 21: Asia Pacific 3D Gaming Consoles Industry Revenue Share (%), by Console 2025 & 2033

- Figure 22: Asia Pacific 3D Gaming Consoles Industry Revenue (billion), by Platform 2025 & 2033

- Figure 23: Asia Pacific 3D Gaming Consoles Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 24: Asia Pacific 3D Gaming Consoles Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Pacific 3D Gaming Consoles Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Rest of the World 3D Gaming Consoles Industry Revenue (billion), by Component 2025 & 2033

- Figure 27: Rest of the World 3D Gaming Consoles Industry Revenue Share (%), by Component 2025 & 2033

- Figure 28: Rest of the World 3D Gaming Consoles Industry Revenue (billion), by Console 2025 & 2033

- Figure 29: Rest of the World 3D Gaming Consoles Industry Revenue Share (%), by Console 2025 & 2033

- Figure 30: Rest of the World 3D Gaming Consoles Industry Revenue (billion), by Platform 2025 & 2033

- Figure 31: Rest of the World 3D Gaming Consoles Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 32: Rest of the World 3D Gaming Consoles Industry Revenue (billion), by Country 2025 & 2033

- Figure 33: Rest of the World 3D Gaming Consoles Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global 3D Gaming Consoles Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 2: Global 3D Gaming Consoles Industry Revenue billion Forecast, by Console 2020 & 2033

- Table 3: Global 3D Gaming Consoles Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 4: Global 3D Gaming Consoles Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global 3D Gaming Consoles Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 6: Global 3D Gaming Consoles Industry Revenue billion Forecast, by Console 2020 & 2033

- Table 7: Global 3D Gaming Consoles Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 8: Global 3D Gaming Consoles Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States 3D Gaming Consoles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada 3D Gaming Consoles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Global 3D Gaming Consoles Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 12: Global 3D Gaming Consoles Industry Revenue billion Forecast, by Console 2020 & 2033

- Table 13: Global 3D Gaming Consoles Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 14: Global 3D Gaming Consoles Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United Kingdom 3D Gaming Consoles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Germany 3D Gaming Consoles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: France 3D Gaming Consoles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe 3D Gaming Consoles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Global 3D Gaming Consoles Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 20: Global 3D Gaming Consoles Industry Revenue billion Forecast, by Console 2020 & 2033

- Table 21: Global 3D Gaming Consoles Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 22: Global 3D Gaming Consoles Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 23: China 3D Gaming Consoles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Japan 3D Gaming Consoles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: India 3D Gaming Consoles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Rest of Asia Pacific 3D Gaming Consoles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Global 3D Gaming Consoles Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 28: Global 3D Gaming Consoles Industry Revenue billion Forecast, by Console 2020 & 2033

- Table 29: Global 3D Gaming Consoles Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 30: Global 3D Gaming Consoles Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the 3D Gaming Consoles Industry?

The projected CAGR is approximately 8.21%.

2. Which companies are prominent players in the 3D Gaming Consoles Industry?

Key companies in the market include Guillemot Corporation SA (Thrustmaster), Logitech Inc, Microsoft Corporation, Activision Publishing Inc, Kaneva LLC, Nintendo Co Ltd, Electronic Art Inc, Sony Corporatio, A4Tech Co Ltd, Oculus VR.

3. What are the main segments of the 3D Gaming Consoles Industry?

The market segments include Component, Console, Platform.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.888 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Popularity of 3D Devices; Development of Autostereoscopic Technology.

6. What are the notable trends driving market growth?

Home Consoles to Dominate the 3D Gaming Consoles Market.

7. Are there any restraints impacting market growth?

Strong Competition form PCs; Higher Game Development Costs.

8. Can you provide examples of recent developments in the market?

September 2022: Zilliqa Blockchain launched the world's first Web3 games console. With the gaming industry proving itself time and time again as a productive medium for leveraging blockchain technology, Layer-1 blockchain Zilliqa revealed its plans to introduce the world's first Web3 hardware console and gaming hub.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "3D Gaming Consoles Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the 3D Gaming Consoles Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the 3D Gaming Consoles Industry?

To stay informed about further developments, trends, and reports in the 3D Gaming Consoles Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence