Key Insights

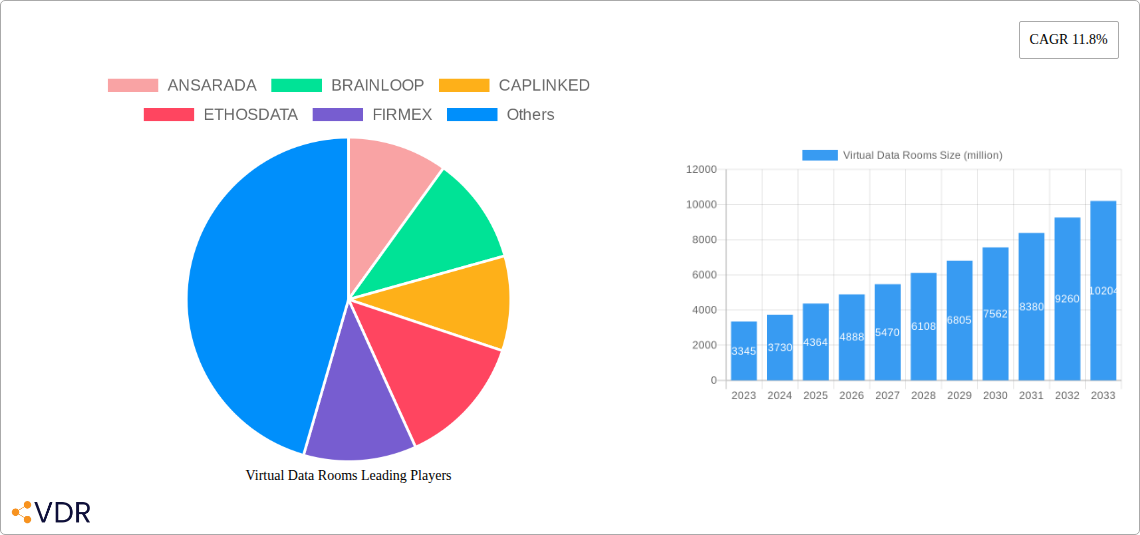

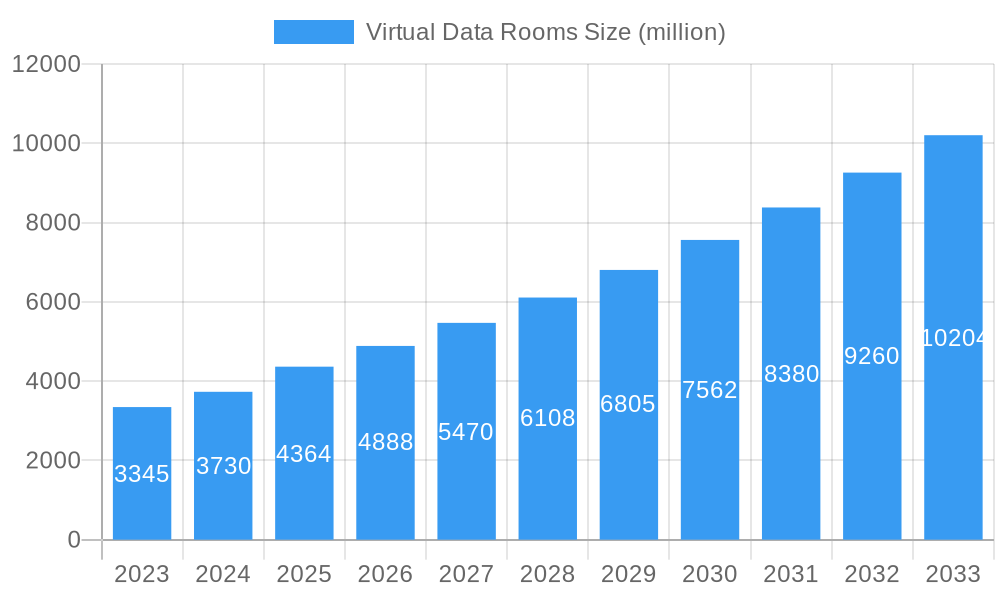

The global Virtual Data Room (VDR) market is experiencing robust expansion, projected to reach a substantial USD 4,364 million by 2025. This growth is fueled by a compelling Compound Annual Growth Rate (CAGR) of 11.8% between 2019 and 2033, indicating a dynamic and rapidly evolving industry. A primary driver for this surge is the increasing adoption of VDRs across diverse sectors, notably financial services and electronic commerce. These industries rely heavily on secure and efficient platforms for managing sensitive documents during critical transactions like mergers, acquisitions, and due diligence processes. The escalating need for enhanced data security, streamlined collaboration, and regulatory compliance further propels the demand for sophisticated VDR solutions. Furthermore, the widespread integration of cloud computing is a significant enabler, offering scalability, accessibility, and cost-effectiveness that traditional methods cannot match.

Virtual Data Rooms Market Size (In Billion)

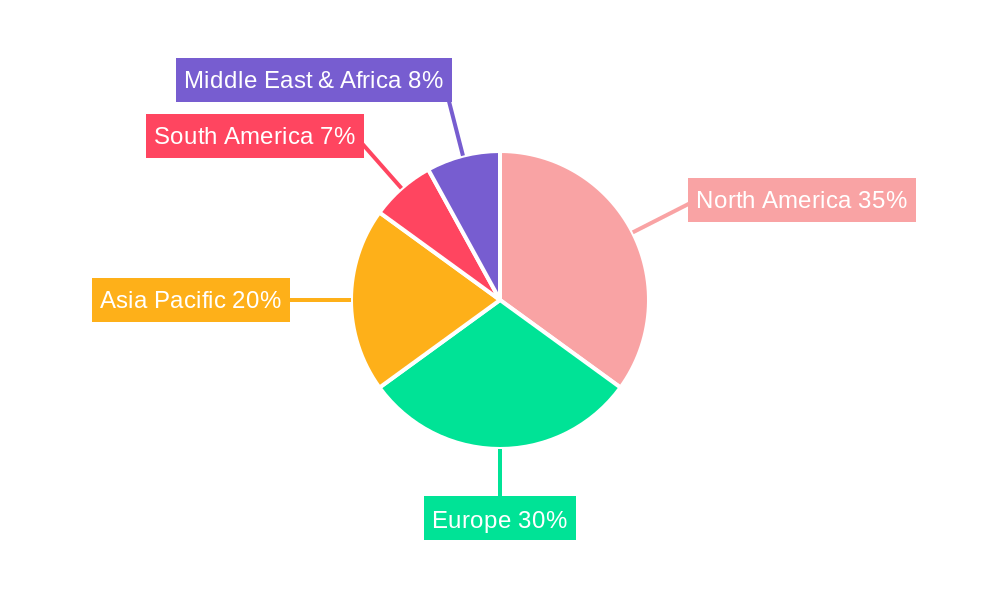

The market landscape for VDRs is characterized by a blend of innovative software systems and integrated hardware devices, catering to a broad spectrum of user needs. Key players like Intralinks, RR Donnelley Sons, and TransPerfect Deal Interactive are actively shaping the market through continuous technological advancements and strategic partnerships. Geographically, North America and Europe currently dominate the VDR market share, owing to the presence of a mature corporate landscape and early adoption of digital solutions. However, the Asia Pacific region is poised for significant growth, driven by rapid economic development, increasing foreign investment, and a burgeoning awareness of data security best practices. Emerging economies in South America and the Middle East & Africa are also showing promising adoption trends, presenting lucrative opportunities for VDR providers in the coming years.

Virtual Data Rooms Company Market Share

Virtual Data Rooms Market: Comprehensive Analysis and Future Outlook (2019-2033)

Unlock critical insights into the global Virtual Data Rooms (VDR) market with this definitive report. Spanning the historical period of 2019-2024, base year 2025, and an extensive forecast period of 2025-2033, this research delivers an in-depth analysis of market dynamics, growth trends, regional dominance, product innovations, key drivers, barriers, emerging opportunities, and strategic outlook.

This report is meticulously crafted for industry professionals, M&A strategists, legal experts, IT decision-makers, and investors seeking to understand the evolving VDR landscape, identify lucrative investment avenues, and formulate robust business strategies in this rapidly expanding sector.

Virtual Data Rooms Market Dynamics & Structure

The Virtual Data Rooms (VDR) market exhibits a moderately concentrated structure, with a few dominant players holding significant market share, yet a growing number of niche providers catering to specialized needs. Technological innovation serves as a primary driver, fueled by the relentless demand for secure and efficient data management, particularly in complex transactions. Robust regulatory frameworks, such as GDPR and CCPA, further necessitate the adoption of advanced VDR solutions to ensure data privacy and compliance, indirectly stimulating market growth. Competitive product substitutes, including traditional physical data rooms and generic cloud storage solutions, are progressively losing ground due to inherent limitations in security, accessibility, and auditability compared to dedicated VDR platforms. End-user demographics are broadening, moving beyond traditional financial services to encompass life sciences, real estate, legal, and technology sectors, each with unique data handling requirements. Mergers and acquisitions (M&A) trends are a constant feature, with larger VDR providers acquiring smaller innovators to expand their feature sets, geographical reach, and customer base. For instance, the past five years have seen approximately 15 M&A deals in the VDR space, totaling an estimated $550 million in transaction value, signaling a consolidation phase driven by a pursuit of market leadership and enhanced service offerings. Innovation barriers, such as the high cost of developing and maintaining advanced security protocols and the complexity of integrating with diverse existing IT infrastructures, remain significant, but are being overcome through strategic investments in R&D and partnerships.

- Market Concentration: Moderately concentrated with key players and a growing number of specialized providers.

- Technological Innovation Drivers: Demand for enhanced security, streamlined collaboration, and efficient due diligence processes.

- Regulatory Frameworks: GDPR, CCPA, and other data privacy regulations are significant market enablers.

- Competitive Product Substitutes: Traditional physical data rooms and generic cloud storage are facing declining relevance.

- End-User Demographics: Expanding beyond finance to include life sciences, real estate, legal, and technology.

- M&A Trends: Active consolidation with an estimated $550 million in deal value over the last five years.

- Innovation Barriers: High development costs for advanced security and integration complexity.

Virtual Data Rooms Growth Trends & Insights

The global Virtual Data Rooms market is poised for robust expansion, projected to grow from an estimated $1.8 billion in 2025 to a significant $4.5 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 12.5% during the forecast period. This substantial growth is underpinned by several interconnected trends. The increasing volume and complexity of M&A activities worldwide continue to be a primary catalyst, with VDRs offering an indispensable platform for secure document sharing, due diligence, and collaboration among diverse stakeholders. The rise of digital transformation initiatives across industries, coupled with the growing acceptance of cloud-based solutions, has significantly boosted VDR adoption rates. Businesses are increasingly recognizing the inherent inefficiencies and security risks associated with traditional data management methods, leading to a decisive shift towards more secure, accessible, and auditable VDR solutions.

Technological disruptions are playing a pivotal role in shaping market evolution. Advancements in artificial intelligence (AI) and machine learning (ML) are being integrated into VDR platforms to offer features such as intelligent document analysis, automated data room setup, and enhanced security threat detection. Blockchain technology is also emerging as a potential disruptor, promising immutable audit trails and heightened data integrity. Consumer behavior shifts are further contributing to market growth. Users now expect intuitive interfaces, seamless mobile access, and advanced collaboration tools, pushing VDR providers to continuously innovate and enhance their user experience. The demand for real-time collaboration and communication features within the VDR environment is also on the rise, especially as remote and hybrid work models become more prevalent. Market penetration is expected to deepen across all sectors, with specialized VDR solutions catering to the unique compliance and security needs of industries like pharmaceuticals, energy, and government. The increasing prevalence of cross-border transactions and the need for robust governance and compliance frameworks are further accelerating the adoption of VDRs globally, making them an integral part of modern business operations. The overall market penetration is expected to rise from an estimated 35% in 2025 to over 60% by 2033, indicating a substantial untapped market potential.

Dominant Regions, Countries, or Segments in Virtual Data Rooms

The Financial Services sector, encompassing investment banking, private equity, venture capital, and corporate finance, is currently the dominant application segment driving the global Virtual Data Rooms (VDR) market. This dominance is projected to continue throughout the forecast period, contributing an estimated 45% of the total market revenue in 2025, valued at approximately $810 million. The inherent nature of financial transactions, involving high-stakes negotiations, extensive due diligence, and the handling of sensitive financial information, necessitates the robust security, auditability, and control offered by VDRs. Regulatory compliance requirements within this sector are particularly stringent, further mandating the use of specialized platforms like VDRs to safeguard sensitive data and ensure transparent transaction processes.

North America, particularly the United States, stands out as the dominant geographical region, accounting for an estimated 40% of the global VDR market share in 2025, generating approximately $720 million in revenue. This leadership is attributed to the region's highly developed financial markets, a robust ecosystem of venture capital and private equity firms, and a strong emphasis on corporate governance and regulatory compliance. The presence of major financial institutions and a high concentration of publicly traded companies fuel a continuous demand for VDR solutions for M&A, IPOs, and other significant financial transactions.

Within the Type segmentation, Software Systems represent the leading category, projected to capture 90% of the market revenue in 2025, valued at an estimated $1.62 billion. This segment's dominance is driven by the software-centric nature of modern VDR solutions, offering scalability, advanced features, and accessibility through cloud infrastructure. Hardware devices, while contributing to the overall ecosystem, play a supporting role and constitute a smaller fraction of the market. The increasing reliance on Software-as-a-Service (SaaS) models further solidifies the dominance of software systems, providing flexibility and cost-effectiveness for businesses of all sizes.

Key drivers contributing to the dominance of these segments include:

- Financial Services:

- High volume and value of M&A and capital raising activities.

- Stringent regulatory compliance mandates (e.g., SEC regulations).

- Need for secure and auditable handling of sensitive financial data.

- Global interconnectedness of financial markets.

- North America (USA):

- Leading global hub for M&A, IPOs, and venture capital funding.

- Strong regulatory environment promoting secure data handling.

- High adoption rate of advanced technologies.

- Presence of major financial institutions and corporations.

- Software Systems (Type):

- Scalability and flexibility offered by cloud-based SaaS models.

- Continuous innovation in features like AI-powered analytics and enhanced security.

- Cost-effectiveness and ease of deployment compared to hardware solutions.

- Accessibility and integration capabilities with existing IT infrastructure.

The Cloud Computing segment as an application is also showing rapid growth, driven by the overall shift towards cloud-based infrastructure and services, and is expected to contribute $270 million in 2025.

Virtual Data Rooms Product Landscape

The Virtual Data Rooms (VDR) product landscape is characterized by continuous innovation focused on enhancing security, user experience, and efficiency for complex transactions. Leading VDR solutions now offer sophisticated features such as granular access controls, advanced encryption (both in transit and at rest), multi-factor authentication, and robust audit trails that meticulously record every user interaction. Product differentiation is increasingly seen in AI-powered functionalities, including intelligent document indexing, automated data room setup, and predictive analytics that can identify potential risks or bottlenecks in due diligence processes. Mobile-first design principles ensure seamless access and collaboration across various devices, catering to the modern workforce. Furthermore, many VDR providers are integrating features like real-time Q&A modules, collaborative annotation tools, and secure messaging to streamline communication and decision-making during critical deal phases. Performance metrics are paramount, with providers emphasizing high uptime, rapid document upload/download speeds, and intuitive navigation to minimize user friction. Unique selling propositions often lie in specialized industry-specific functionalities, such as compliance tools for life sciences or IP management features for technology firms, alongside exceptional customer support and dedicated account management.

Key Drivers, Barriers & Challenges in Virtual Data Rooms

The Virtual Data Rooms (VDR) market is propelled by several key drivers. The relentless growth in M&A activities globally necessitates secure and efficient platforms for due diligence. Increasing regulatory compliance demands, particularly concerning data privacy and security (e.g., GDPR, CCPA), compel organizations to adopt robust VDR solutions. Digital transformation initiatives across industries are accelerating the shift from physical to virtual data management. Technological advancements, such as AI and blockchain, are enhancing VDR capabilities, offering more sophisticated analytics and security.

However, the market also faces significant barriers and challenges. High initial investment costs for advanced VDR solutions and their implementation can be a deterrent for smaller businesses. Integration complexities with existing IT infrastructure can hinder seamless adoption. User adoption and training are critical, as unfamiliarity with VDR functionalities can lead to inefficiencies. Data security concerns and the threat of cyberattacks, despite stringent measures, remain a persistent challenge, requiring constant vigilance and investment in cutting-edge security protocols. The highly competitive landscape also presents a challenge, with a multitude of providers vying for market share, leading to price pressures.

Emerging Opportunities in Virtual Data Rooms

Emerging opportunities in the Virtual Data Rooms (VDR) sector are abundant, driven by evolving business needs and technological advancements. The expansion of VDR usage into post-merger integration (PMI) phases, offering a secure environment for the seamless transition and consolidation of data and operations, represents a significant untapped market. Furthermore, the increasing adoption of VDRs for intellectual property (IP) management and litigation support, where secure and granular access to sensitive legal documents is paramount, presents substantial growth potential. The development of industry-specific VDR solutions tailored to the unique compliance and workflow requirements of sectors like renewable energy, advanced manufacturing, and cybersecurity offers niche market penetration opportunities. Moreover, the integration of advanced AI-driven analytics and automated workflows within VDRs is creating opportunities for predictive insights, risk assessment, and streamlined due diligence, enhancing their value proposition beyond mere storage and sharing.

Growth Accelerators in the Virtual Data Rooms Industry

Several catalysts are accelerating long-term growth in the Virtual Data Rooms (VDR) industry. Continuous technological innovation, particularly in artificial intelligence for data analysis and security, and the exploration of blockchain for enhanced audit trails, are key accelerators. Strategic partnerships between VDR providers and complementary technology firms (e.g., cybersecurity, legal tech, cloud service providers) are expanding service offerings and market reach. Market expansion into emerging economies and underserved industries, driven by globalization and increasing awareness of data security benefits, presents substantial growth opportunities. The growing trend of remote and hybrid work models inherently increases the reliance on secure, accessible, and collaborative platforms like VDRs for seamless operations and deal execution.

Key Players Shaping the Virtual Data Rooms Market

- ANSARADA

- BRAINLOOP

- CAPLINKED

- ETHOSDATA

- FIRMEX

- GLOBAL CAP

- HIGHQ DATA ROOM

- IDEALS SOLUTIONS

- INTRALINKS

- MERRIL DATA SITE

- RR DONNELLEY SONS

- SECCUREDOOCS

- SHAREVAULT

- TRANSPERFECT DEAL INTERACTIVE

Notable Milestones in Virtual Data Rooms Sector

- 2019 - Q3: Increased adoption of AI-powered features for enhanced document analysis and security by leading providers.

- 2020 - Q1: Surge in VDR usage for remote due diligence due to global pandemic restrictions.

- 2020 - Q4: Enhanced mobile accessibility and collaboration tools become a standard offering.

- 2021 - Q2: Greater integration of VDRs with other enterprise software solutions.

- 2022 - Q1: Emergence of specialized VDR solutions for life sciences and healthcare sectors.

- 2022 - Q3: Focus on advanced security protocols, including zero-trust architecture.

- 2023 - Q1: Increased investment in cloud-native VDR platforms for scalability and resilience.

- 2023 - Q4: Introduction of blockchain-inspired features for immutable audit trails.

- 2024 - Q2: Growing demand for VDRs in renewable energy and ESG-related transactions.

In-Depth Virtual Data Rooms Market Outlook

The future outlook for the Virtual Data Rooms (VDR) market is exceptionally bright, characterized by sustained growth driven by the indispensable role VDRs play in secure digital transactions and data management. The ongoing digital transformation across industries, coupled with the increasing complexity and volume of global M&A activities, will continue to fuel demand. Technological advancements, particularly in AI for intelligent automation and predictive analytics, will further enhance VDR functionality, driving user adoption and creating new service opportunities. Strategic partnerships and market expansion into nascent sectors and regions will broaden the VDR ecosystem. The inherent need for robust data security and regulatory compliance in an increasingly data-sensitive world ensures that VDRs will remain a critical technology investment for organizations of all sizes, solidifying their position as an essential tool for modern business operations and strategic decision-making.

Virtual Data Rooms Segmentation

-

1. Application

- 1.1. Financial Services

- 1.2. Electronic Commerce

- 1.3. Cloud Computing

- 1.4. Other

-

2. Type

- 2.1. Software System

- 2.2. Hardware Devices

Virtual Data Rooms Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Virtual Data Rooms Regional Market Share

Geographic Coverage of Virtual Data Rooms

Virtual Data Rooms REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.11% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Virtual Data Rooms Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Financial Services

- 5.1.2. Electronic Commerce

- 5.1.3. Cloud Computing

- 5.1.4. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Software System

- 5.2.2. Hardware Devices

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Virtual Data Rooms Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Financial Services

- 6.1.2. Electronic Commerce

- 6.1.3. Cloud Computing

- 6.1.4. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Software System

- 6.2.2. Hardware Devices

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Virtual Data Rooms Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Financial Services

- 7.1.2. Electronic Commerce

- 7.1.3. Cloud Computing

- 7.1.4. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Software System

- 7.2.2. Hardware Devices

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Virtual Data Rooms Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Financial Services

- 8.1.2. Electronic Commerce

- 8.1.3. Cloud Computing

- 8.1.4. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Software System

- 8.2.2. Hardware Devices

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Virtual Data Rooms Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Financial Services

- 9.1.2. Electronic Commerce

- 9.1.3. Cloud Computing

- 9.1.4. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Software System

- 9.2.2. Hardware Devices

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Virtual Data Rooms Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Financial Services

- 10.1.2. Electronic Commerce

- 10.1.3. Cloud Computing

- 10.1.4. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Software System

- 10.2.2. Hardware Devices

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 ANSARADA

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 BRAINLOOP

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 CAPLINKED

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 ETHOSDATA

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 FIRMEX

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 GLOBAL CAP

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 HIGHQ DATA ROOM

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 IDEALS SOLUTIONS

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 INTRALINKS

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 MERRIL DATA SITE

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 RR DONNELLEY SONS

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 SECCUREDOCS

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 SHAREVAULT

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 TRANSPERFECT DEAL INTERACTIVE

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 ANSARADA

List of Figures

- Figure 1: Global Virtual Data Rooms Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Virtual Data Rooms Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Virtual Data Rooms Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Virtual Data Rooms Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Virtual Data Rooms Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Virtual Data Rooms Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Virtual Data Rooms Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Virtual Data Rooms Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Virtual Data Rooms Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Virtual Data Rooms Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Virtual Data Rooms Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Virtual Data Rooms Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Virtual Data Rooms Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Virtual Data Rooms Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Virtual Data Rooms Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Virtual Data Rooms Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Virtual Data Rooms Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Virtual Data Rooms Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Virtual Data Rooms Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Virtual Data Rooms Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Virtual Data Rooms Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Virtual Data Rooms Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Virtual Data Rooms Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Virtual Data Rooms Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Virtual Data Rooms Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Virtual Data Rooms Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Virtual Data Rooms Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Virtual Data Rooms Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Virtual Data Rooms Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Virtual Data Rooms Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Virtual Data Rooms Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Virtual Data Rooms Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Virtual Data Rooms Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Virtual Data Rooms Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Virtual Data Rooms Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Virtual Data Rooms Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Virtual Data Rooms Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Virtual Data Rooms Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Virtual Data Rooms Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Virtual Data Rooms Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Virtual Data Rooms Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Virtual Data Rooms Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Virtual Data Rooms Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Virtual Data Rooms Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Virtual Data Rooms Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Virtual Data Rooms Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Virtual Data Rooms Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Virtual Data Rooms Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Virtual Data Rooms Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Virtual Data Rooms Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Virtual Data Rooms?

The projected CAGR is approximately 15.11%.

2. Which companies are prominent players in the Virtual Data Rooms?

Key companies in the market include ANSARADA, BRAINLOOP, CAPLINKED, ETHOSDATA, FIRMEX, GLOBAL CAP, HIGHQ DATA ROOM, IDEALS SOLUTIONS, INTRALINKS, MERRIL DATA SITE, RR DONNELLEY SONS, SECCUREDOCS, SHAREVAULT, TRANSPERFECT DEAL INTERACTIVE.

3. What are the main segments of the Virtual Data Rooms?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Virtual Data Rooms," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Virtual Data Rooms report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Virtual Data Rooms?

To stay informed about further developments, trends, and reports in the Virtual Data Rooms, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence