Key Insights

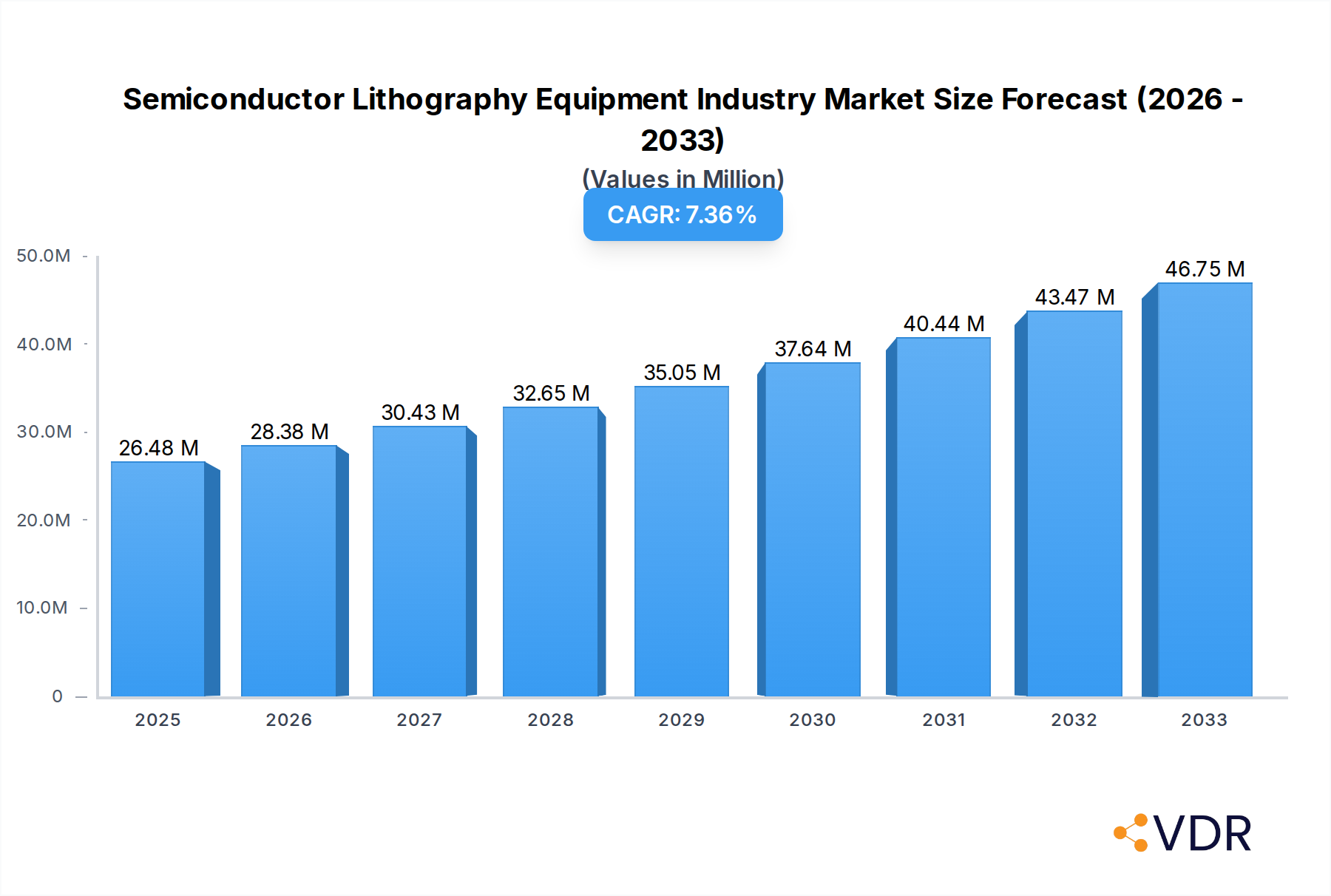

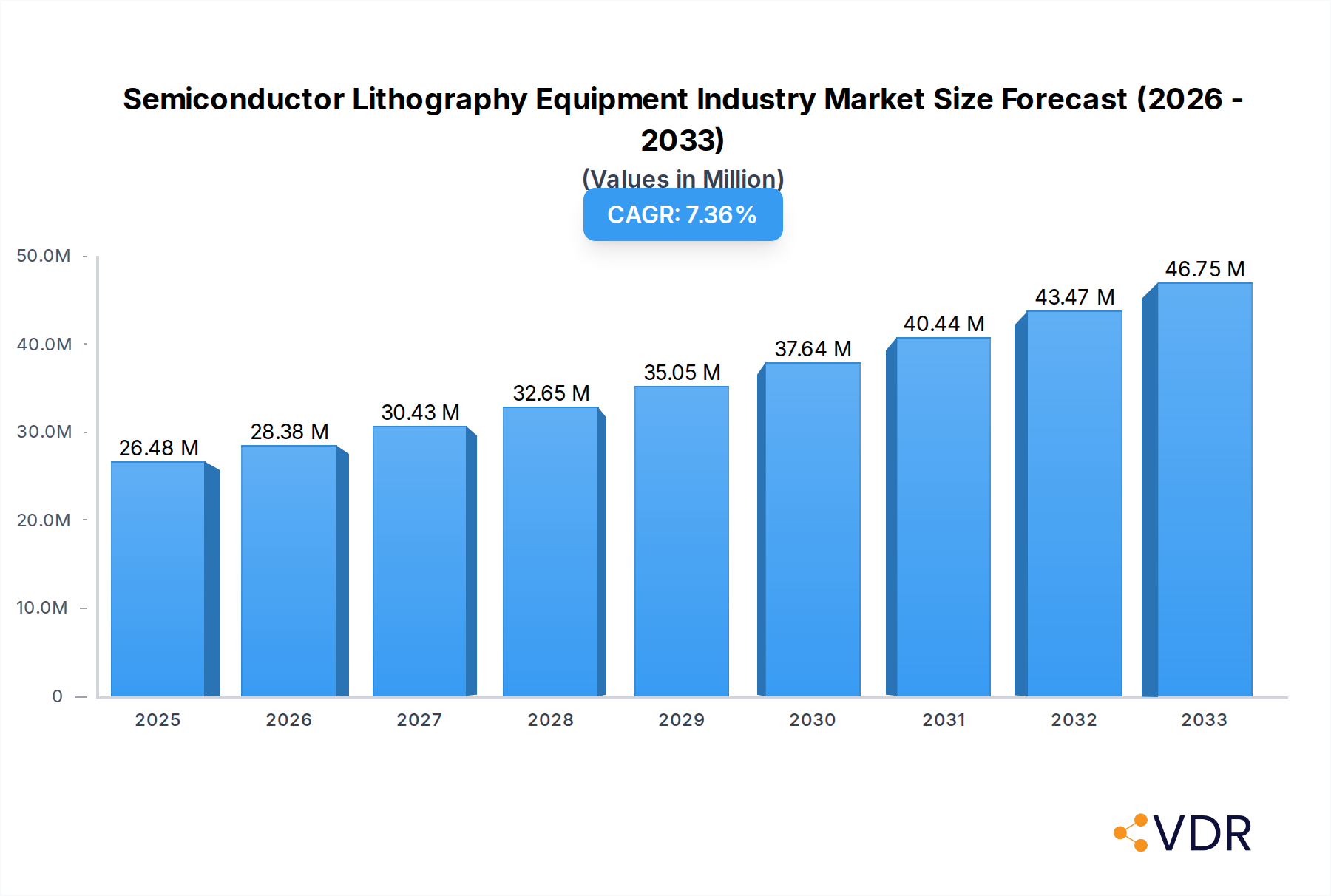

The global Semiconductor Lithography Equipment market is poised for significant expansion, projected to reach $26.48 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 7.38% throughout the forecast period of 2025-2033. This growth is underpinned by the escalating demand for advanced microprocessors and an increasing reliance on sophisticated electronic devices across diverse sectors. Key drivers include the relentless pursuit of miniaturization in semiconductor manufacturing, leading to higher transistor densities and enhanced device performance. The burgeoning Internet of Things (IoT) ecosystem, the proliferation of artificial intelligence (AI) applications, and the continuous evolution of consumer electronics are fueling the need for cutting-edge lithography solutions. Furthermore, advancements in areas such as autonomous vehicles and high-performance computing are creating substantial opportunities for market players.

Semiconductor Lithography Equipment Industry Market Size (In Million)

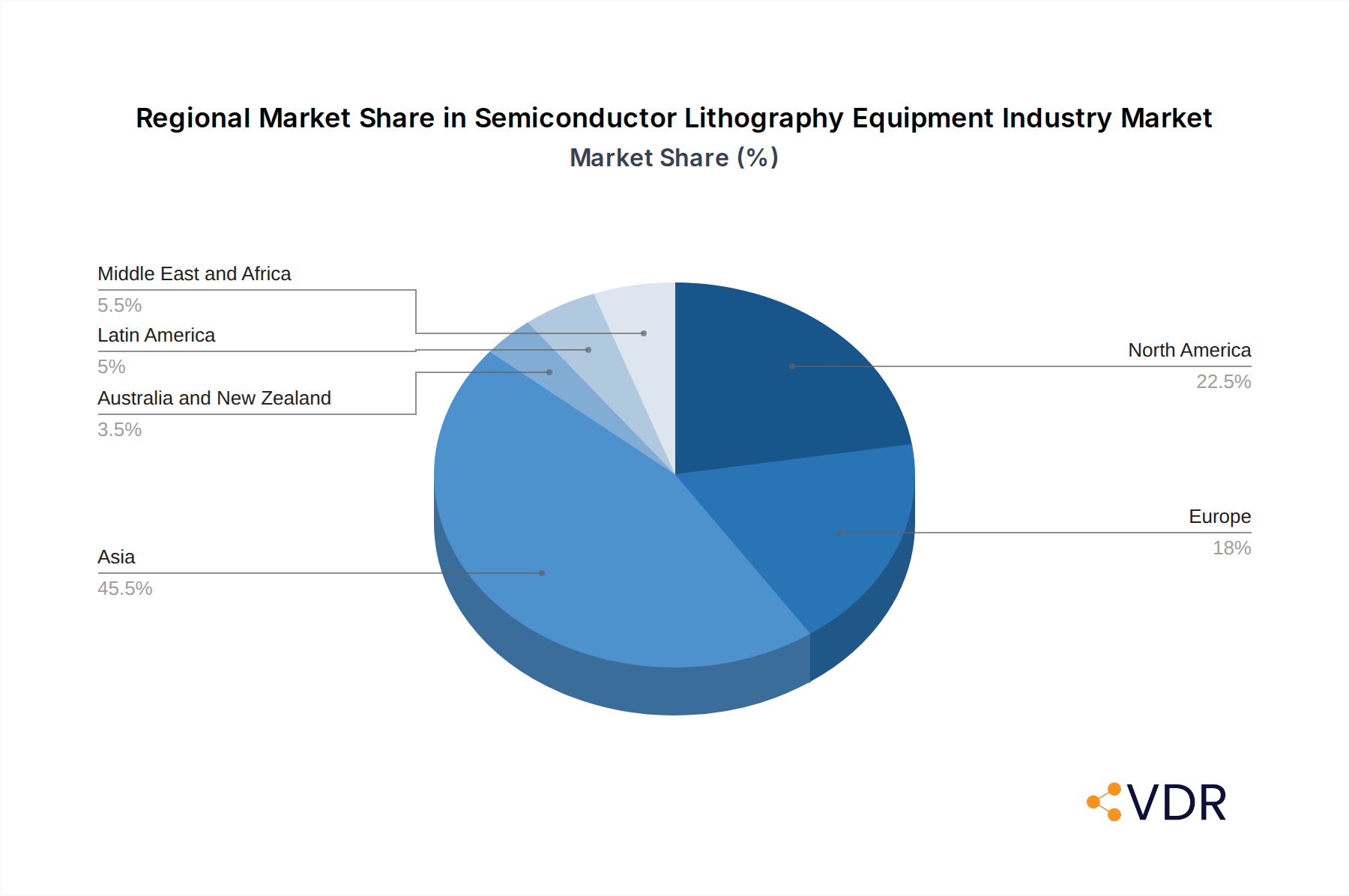

The market is segmented by technology into Deep Ultraviolet Lithography (DUV) and Extreme Ultraviolet Lithography (EUV), with EUV expected to gain prominence due to its capability to enable the production of sub-10nm nodes. Applications span Advanced Packaging, MEMS Devices, and LED Devices, each contributing to the overall market dynamism. Emerging trends indicate a focus on developing more cost-effective and efficient lithography techniques, alongside innovations in materials and processes to support next-generation chip manufacturing. While the market is driven by strong demand, it faces potential restraints such as the high capital expenditure required for advanced lithography tools and the complexity of integrating new technologies into existing fabrication processes. The competitive landscape is characterized by the presence of major industry giants like ASML Holding NV, Nikon Corporation, and Canon Inc., with SÜSS MicroTec SE and Veeco Instruments Inc. also holding significant positions. Regional analysis suggests North America and Asia will be key growth hubs, driven by substantial semiconductor manufacturing presence and R&D investments.

Semiconductor Lithography Equipment Industry Company Market Share

In-Depth Semiconductor Lithography Equipment Market Outlook 2023-2033

Unlock critical insights into the global Semiconductor Lithography Equipment market with this comprehensive report. Covering Deep Ultraviolet Lithography (DUV) and Extreme Ultraviolet Lithography (EUV) systems, this analysis delves into applications for Advanced Packaging, MEMS Devices, and LED Devices. Explore market dynamics, growth trends, regional dominance, product landscape, key drivers, barriers, challenges, emerging opportunities, and growth accelerators. Featuring vendor market share analysis, this report provides a future-proof roadmap for stakeholders navigating the evolving semiconductor manufacturing landscape. All values are presented in Million units.

Semiconductor Lithography Equipment Industry Market Dynamics & Structure

The semiconductor lithography equipment market is characterized by a highly consolidated structure, primarily dominated by a few key players holding significant market share. This concentration is a testament to the immense capital investment, advanced R&D, and intricate intellectual property required to develop and manufacture these sophisticated machines. Technological innovation serves as the primary engine driving market growth, with relentless advancements in resolution, throughput, and efficiency being paramount. The constant pursuit of smaller feature sizes and more complex chip designs fuels innovation in areas like EUV lithography. Regulatory frameworks, particularly concerning trade and intellectual property, can influence market access and investment. Competitive product substitutes, while limited at the leading edge, exist in the form of older lithography technologies for less demanding applications. End-user demographics are shifting towards advanced packaging solutions and the burgeoning MEMS and LED device markets, demanding specialized lithography capabilities. Mergers and acquisitions (M&A) trends, though infrequent due to high valuations and technological barriers, are observed as companies seek to consolidate expertise, expand product portfolios, or gain access to critical technologies. For instance, the acquisition of Rudolph Technologies Inc. by Onto Innovation highlights a strategic move to bolster integrated solutions. The market size for lithography equipment was approximately USD 15,250.73 Million units in 2025, with significant investments in R&D projected to maintain this growth trajectory. Innovation barriers are substantial, including the extremely high cost of EUV development and manufacturing, as well as the long lead times for technology maturation.

Semiconductor Lithography Equipment Industry Growth Trends & Insights

The semiconductor lithography equipment industry is poised for substantial growth, driven by the insatiable demand for advanced computing power across various sectors, including artificial intelligence, 5G, and the Internet of Things (IoT). The market size, projected to reach approximately USD 21,900.50 Million units by 2033, is expected to witness a Compound Annual Growth Rate (CAGR) of approximately 4.5% during the forecast period of 2025–2033. This upward trajectory is fueled by the continuous need for smaller, more powerful, and energy-efficient semiconductor devices. The adoption rates for advanced lithography techniques, particularly EUV, are steadily increasing as foundries invest in next-generation manufacturing nodes to achieve unprecedented miniaturization and performance gains. Technological disruptions, such as advancements in directed self-assembly (DSA) and multi-beam lithography, are emerging as potential game-changers, offering alternative pathways to achieve sub-10nm features. Consumer behavior shifts, characterized by an increasing reliance on data-intensive applications and connected devices, directly translate into higher demand for sophisticated semiconductors, thereby stimulating the lithography equipment market. The market penetration of lithography equipment is intrinsically linked to the expansion of global semiconductor manufacturing capacity and the ongoing technological race among leading chip manufacturers. As chip complexity escalates, the demand for high-resolution and high-throughput lithography solutions will only intensify. The market is projected to experience a significant surge in demand for advanced packaging solutions, driving the need for specialized lithography equipment capable of handling complex interconnects and multi-chip modules.

Dominant Regions, Countries, or Segments in Semiconductor Lithography Equipment Industry

The semiconductor lithography equipment industry's dominance is primarily dictated by the geographical concentration of advanced semiconductor manufacturing facilities and the strategic importance of technological innovation within specific regions. Asia-Pacific, particularly Taiwan and South Korea, stands out as the leading region driving market growth, owing to the presence of world-leading foundries and a robust ecosystem for semiconductor production. This dominance is underpinned by significant government investments in the semiconductor sector, favorable economic policies, and extensive infrastructure development tailored to support high-tech manufacturing. The strong presence of advanced packaging facilities in these regions further accentuates the demand for sophisticated lithography solutions. Consequently, the Advanced Packaging segment, crucial for enabling next-generation chip architectures like chiplets, is a key growth driver within the overall market. Market share for lithography equipment in this segment is substantial and rapidly expanding, reflecting the industry's shift towards heterogeneous integration. The market size for lithography equipment used in advanced packaging alone was approximately USD 6,500.25 Million units in 2025 and is projected to grow at a CAGR of 5.2% through 2033.

Another significant driver is the Deep Ultraviolet Lithography (DUV) segment, which continues to be the workhorse for a vast majority of semiconductor manufacturing processes. While EUV is capturing headlines for leading-edge nodes, DUV lithography remains critical for mature nodes and specific applications, maintaining a substantial market share. The market size for DUV lithography equipment was approximately USD 8,750.40 Million units in 2025.

In terms of specific countries, Taiwan's dominance is driven by TSMC's unparalleled manufacturing prowess, while South Korea benefits from the significant investments by Samsung Electronics and SK Hynix in cutting-edge memory and logic production. The United States, with its strong R&D capabilities and growing fab investments, also plays a crucial role. China is rapidly expanding its domestic semiconductor manufacturing capacity, presenting a substantial growth opportunity for lithography equipment suppliers. The growth potential in Asia-Pacific is immense, fueled by ongoing capacity expansions and the relentless pursuit of technological leadership in semiconductor fabrication.

Semiconductor Lithography Equipment Industry Product Landscape

The product landscape of the semiconductor lithography equipment industry is defined by continuous innovation aimed at achieving higher resolution, increased throughput, and enhanced precision. Leading the charge are advanced systems like Extreme Ultraviolet (EUV) lithography, essential for fabricating chips at the 7nm node and below, enabling unprecedented miniaturization and performance. Deep Ultraviolet (DUV) lithography, particularly ArF immersion scanners, remains a cornerstone for a wide range of semiconductor manufacturing processes, offering a balance of resolution and cost-effectiveness. Beyond these primary types, specialized lithography solutions are emerging for specific applications. For advanced packaging, i-line lithography steppers, such as Canon Inc.'s FPA-5520iV LF2, are optimized for back-end processing, offering 0.8-micron resolution for applications like chiplets. For MEMS device fabrication, advanced optical and nano-imprint lithography techniques are crucial for creating intricate microstructures. EV Group's EVG 150 automated resist processing system, a next-generation 200-mm version, highlights advancements in supporting lithography workflows for MEMS and nanotech applications. These product innovations are critical for enabling the next generation of electronic devices, from high-performance CPUs and GPUs to advanced sensors and displays.

Key Drivers, Barriers & Challenges in Semiconductor Lithography Equipment Industry

Key Drivers:

- Exponential growth in data consumption and AI/ML adoption: Fuels demand for increasingly powerful and complex semiconductors.

- Advancements in nanotechnology and materials science: Enables development of new lithography techniques and applications.

- Government initiatives and investments in semiconductor self-sufficiency: Promotes domestic manufacturing and R&D.

- Evolution of IoT and connected devices: Creates demand for specialized sensors and processing units.

- Technological race for smaller process nodes: Drives continuous investment in cutting-edge lithography equipment.

Barriers & Challenges:

- Extremely high capital expenditure: The cost of developing and acquiring leading-edge lithography equipment, especially EUV systems, is immense, limiting market entry for new players.

- Complex supply chains and geopolitical risks: Dependence on specialized components and the potential for trade restrictions pose significant challenges.

- Long technology development cycles and high R&D costs: Bringing new lithography technologies to market requires substantial time and investment.

- Skilled labor shortage: The industry faces a deficit of highly trained engineers and technicians needed for advanced manufacturing and equipment maintenance.

- Environmental regulations and sustainability concerns: Increasing scrutiny on manufacturing processes and the use of hazardous materials can impact operations and development. The global supply chain for critical lithography components, such as pellicles and specialized optics, is highly constrained, with lead times extending to over 12 months.

Emerging Opportunities in Semiconductor Lithography Equipment Industry

Emerging opportunities in the semiconductor lithography equipment industry are largely driven by the relentless demand for miniaturization and performance enhancements in electronic devices. The expanding applications of Advanced Packaging techniques, such as 3D stacking and chiplets, present a significant avenue for growth, requiring specialized lithography for intricate interconnections and heterogeneous integration. The burgeoning MEMS Devices market, encompassing sensors, actuators, and microfluidic systems for automotive, healthcare, and consumer electronics, necessitates advanced lithography for creating micro-scale structures with high precision. Furthermore, the growth in LED Devices, particularly for high-brightness and energy-efficient lighting and displays, relies on lithography for efficient micro-patterning. The development of novel lithography approaches, including directed self-assembly (DSA) and multi-beam e-beam lithography, holds the promise of achieving sub-10nm features cost-effectively, opening new frontiers in semiconductor manufacturing.

Growth Accelerators in the Semiconductor Lithography Equipment Industry Industry

The semiconductor lithography equipment industry is propelled by several key growth accelerators. Foremost among these is the relentless technological breakthrough in areas like EUV technology, which continues to push the boundaries of semiconductor miniaturization. Strategic partnerships and collaborations between equipment manufacturers, chip designers, and foundries are crucial for co-developing and optimizing next-generation lithography solutions. Market expansion strategies, including the increasing adoption of advanced lithography in emerging economies and the diversification of applications beyond traditional computing, are also significant growth catalysts. The growing demand for high-performance computing in data centers, AI, and autonomous driving is a primary market driver, compelling continuous investment in advanced lithography capabilities. Furthermore, the trend towards heterogeneous integration in advanced packaging is creating a new wave of demand for specialized lithography equipment.

Key Players Shaping the Semiconductor Lithography Equipment Industry Market

- ASML Holding NV

- Canon Inc.

- Nikon Corporation

- JEOL Ltd

- Shanghai Micro Electronics Equipment (Group) Co Ltd

- Veeco Instruments Inc

- SÜSS MicroTec SE

- EV Group (EVG)

- Onto Innovation (Rudolph Technologies Inc )

- Neutronix Quintel Inc (NXQ)

Notable Milestones in Semiconductor Lithography Equipment Industry Sector

- December 2022: Canon Inc. launched an i-line lithography stepper (FPA-5520iV LF2) optimized for 3D advanced packaging, supporting chiplets with 0.8-micron resolution and a 52 mm by 68 mm single-exposure field.

- November 2022: EV Group (EVG) strengthened its optical lithography solutions by launching the next-generation 200-mm version of its EVG 150 automated resist processing system, enhancing offerings for MEMS, nanotechnology, and semiconductor markets.

In-Depth Semiconductor Lithography Equipment Industry Market Outlook

The semiconductor lithography equipment industry is set for robust growth, driven by foundational pillars of technological innovation and burgeoning market demands. The continuous evolution of EUV and DUV technologies, coupled with emerging techniques, will facilitate the creation of increasingly sophisticated semiconductors essential for AI, 5G, and IoT applications. The expansion of advanced packaging and the growing MEMS and LED device markets represent significant growth opportunities, requiring specialized and high-precision lithography solutions. Strategic investments by governments and industry leaders in R&D and manufacturing capacity will further accelerate market expansion. Collaboration and partnerships will be key to navigating the complex technological landscape and ensuring the efficient deployment of advanced lithography. The market outlook remains highly positive, with sustained demand for cutting-edge lithography equipment poised to drive significant advancements in the semiconductor ecosystem.

Semiconductor Lithography Equipment Industry Segmentation

-

1. Type

- 1.1. Deep Ultraviolet Lithography (DUV)

- 1.2. Extreme Ultraviolet Lithography (EUV)

-

2. Application

- 2.1. Advanced Packaging

- 2.2. MEMS Devices

- 2.3. LED Devices

Semiconductor Lithography Equipment Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Semiconductor Lithography Equipment Industry Regional Market Share

Geographic Coverage of Semiconductor Lithography Equipment Industry

Semiconductor Lithography Equipment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.38% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Deep Ultraviolet Lithography (DUV)

- 5.1.2. Extreme Ultraviolet Lithography (EUV)

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Advanced Packaging

- 5.2.2. MEMS Devices

- 5.2.3. LED Devices

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia

- 5.3.4. Australia and New Zealand

- 5.3.5. Latin America

- 5.3.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Semiconductor Lithography Equipment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Deep Ultraviolet Lithography (DUV)

- 6.1.2. Extreme Ultraviolet Lithography (EUV)

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Advanced Packaging

- 6.2.2. MEMS Devices

- 6.2.3. LED Devices

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Semiconductor Lithography Equipment Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Deep Ultraviolet Lithography (DUV)

- 7.1.2. Extreme Ultraviolet Lithography (EUV)

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Advanced Packaging

- 7.2.2. MEMS Devices

- 7.2.3. LED Devices

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Semiconductor Lithography Equipment Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Deep Ultraviolet Lithography (DUV)

- 8.1.2. Extreme Ultraviolet Lithography (EUV)

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Advanced Packaging

- 8.2.2. MEMS Devices

- 8.2.3. LED Devices

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Semiconductor Lithography Equipment Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Deep Ultraviolet Lithography (DUV)

- 9.1.2. Extreme Ultraviolet Lithography (EUV)

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Advanced Packaging

- 9.2.2. MEMS Devices

- 9.2.3. LED Devices

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Australia and New Zealand Semiconductor Lithography Equipment Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Deep Ultraviolet Lithography (DUV)

- 10.1.2. Extreme Ultraviolet Lithography (EUV)

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Advanced Packaging

- 10.2.2. MEMS Devices

- 10.2.3. LED Devices

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Latin America Semiconductor Lithography Equipment Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Deep Ultraviolet Lithography (DUV)

- 11.1.2. Extreme Ultraviolet Lithography (EUV)

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Advanced Packaging

- 11.2.2. MEMS Devices

- 11.2.3. LED Devices

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Middle East and Africa Semiconductor Lithography Equipment Industry Analysis, Insights and Forecast, 2021-2033

- 12.1. Market Analysis, Insights and Forecast - by Type

- 12.1.1. Deep Ultraviolet Lithography (DUV)

- 12.1.2. Extreme Ultraviolet Lithography (EUV)

- 12.2. Market Analysis, Insights and Forecast - by Application

- 12.2.1. Advanced Packaging

- 12.2.2. MEMS Devices

- 12.2.3. LED Devices

- 12.1. Market Analysis, Insights and Forecast - by Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 SÜSS MicroTec SE

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Veeco Instruments Inc

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Canon Inc

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Shanghai Micro Electronics Equipment (Group) Co Ltd

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Nikon Corporation

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 JEOL Ltd

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Neutronix Quintel Inc (NXQ)7 2 Vendor Market Share Analysi

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Onto Innovation (Rudolph Technologies Inc )

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 ASML Holding NV

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 EV Group (EVG)

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.1 SÜSS MicroTec SE

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Semiconductor Lithography Equipment Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Semiconductor Lithography Equipment Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Semiconductor Lithography Equipment Industry Revenue (Million), by Type 2025 & 2033

- Figure 4: North America Semiconductor Lithography Equipment Industry Volume (K Unit), by Type 2025 & 2033

- Figure 5: North America Semiconductor Lithography Equipment Industry Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Semiconductor Lithography Equipment Industry Volume Share (%), by Type 2025 & 2033

- Figure 7: North America Semiconductor Lithography Equipment Industry Revenue (Million), by Application 2025 & 2033

- Figure 8: North America Semiconductor Lithography Equipment Industry Volume (K Unit), by Application 2025 & 2033

- Figure 9: North America Semiconductor Lithography Equipment Industry Revenue Share (%), by Application 2025 & 2033

- Figure 10: North America Semiconductor Lithography Equipment Industry Volume Share (%), by Application 2025 & 2033

- Figure 11: North America Semiconductor Lithography Equipment Industry Revenue (Million), by Country 2025 & 2033

- Figure 12: North America Semiconductor Lithography Equipment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 13: North America Semiconductor Lithography Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Semiconductor Lithography Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: Europe Semiconductor Lithography Equipment Industry Revenue (Million), by Type 2025 & 2033

- Figure 16: Europe Semiconductor Lithography Equipment Industry Volume (K Unit), by Type 2025 & 2033

- Figure 17: Europe Semiconductor Lithography Equipment Industry Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Semiconductor Lithography Equipment Industry Volume Share (%), by Type 2025 & 2033

- Figure 19: Europe Semiconductor Lithography Equipment Industry Revenue (Million), by Application 2025 & 2033

- Figure 20: Europe Semiconductor Lithography Equipment Industry Volume (K Unit), by Application 2025 & 2033

- Figure 21: Europe Semiconductor Lithography Equipment Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: Europe Semiconductor Lithography Equipment Industry Volume Share (%), by Application 2025 & 2033

- Figure 23: Europe Semiconductor Lithography Equipment Industry Revenue (Million), by Country 2025 & 2033

- Figure 24: Europe Semiconductor Lithography Equipment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 25: Europe Semiconductor Lithography Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Semiconductor Lithography Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Asia Semiconductor Lithography Equipment Industry Revenue (Million), by Type 2025 & 2033

- Figure 28: Asia Semiconductor Lithography Equipment Industry Volume (K Unit), by Type 2025 & 2033

- Figure 29: Asia Semiconductor Lithography Equipment Industry Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Semiconductor Lithography Equipment Industry Volume Share (%), by Type 2025 & 2033

- Figure 31: Asia Semiconductor Lithography Equipment Industry Revenue (Million), by Application 2025 & 2033

- Figure 32: Asia Semiconductor Lithography Equipment Industry Volume (K Unit), by Application 2025 & 2033

- Figure 33: Asia Semiconductor Lithography Equipment Industry Revenue Share (%), by Application 2025 & 2033

- Figure 34: Asia Semiconductor Lithography Equipment Industry Volume Share (%), by Application 2025 & 2033

- Figure 35: Asia Semiconductor Lithography Equipment Industry Revenue (Million), by Country 2025 & 2033

- Figure 36: Asia Semiconductor Lithography Equipment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 37: Asia Semiconductor Lithography Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Asia Semiconductor Lithography Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Australia and New Zealand Semiconductor Lithography Equipment Industry Revenue (Million), by Type 2025 & 2033

- Figure 40: Australia and New Zealand Semiconductor Lithography Equipment Industry Volume (K Unit), by Type 2025 & 2033

- Figure 41: Australia and New Zealand Semiconductor Lithography Equipment Industry Revenue Share (%), by Type 2025 & 2033

- Figure 42: Australia and New Zealand Semiconductor Lithography Equipment Industry Volume Share (%), by Type 2025 & 2033

- Figure 43: Australia and New Zealand Semiconductor Lithography Equipment Industry Revenue (Million), by Application 2025 & 2033

- Figure 44: Australia and New Zealand Semiconductor Lithography Equipment Industry Volume (K Unit), by Application 2025 & 2033

- Figure 45: Australia and New Zealand Semiconductor Lithography Equipment Industry Revenue Share (%), by Application 2025 & 2033

- Figure 46: Australia and New Zealand Semiconductor Lithography Equipment Industry Volume Share (%), by Application 2025 & 2033

- Figure 47: Australia and New Zealand Semiconductor Lithography Equipment Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Australia and New Zealand Semiconductor Lithography Equipment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Australia and New Zealand Semiconductor Lithography Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Australia and New Zealand Semiconductor Lithography Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Latin America Semiconductor Lithography Equipment Industry Revenue (Million), by Type 2025 & 2033

- Figure 52: Latin America Semiconductor Lithography Equipment Industry Volume (K Unit), by Type 2025 & 2033

- Figure 53: Latin America Semiconductor Lithography Equipment Industry Revenue Share (%), by Type 2025 & 2033

- Figure 54: Latin America Semiconductor Lithography Equipment Industry Volume Share (%), by Type 2025 & 2033

- Figure 55: Latin America Semiconductor Lithography Equipment Industry Revenue (Million), by Application 2025 & 2033

- Figure 56: Latin America Semiconductor Lithography Equipment Industry Volume (K Unit), by Application 2025 & 2033

- Figure 57: Latin America Semiconductor Lithography Equipment Industry Revenue Share (%), by Application 2025 & 2033

- Figure 58: Latin America Semiconductor Lithography Equipment Industry Volume Share (%), by Application 2025 & 2033

- Figure 59: Latin America Semiconductor Lithography Equipment Industry Revenue (Million), by Country 2025 & 2033

- Figure 60: Latin America Semiconductor Lithography Equipment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 61: Latin America Semiconductor Lithography Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: Latin America Semiconductor Lithography Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 63: Middle East and Africa Semiconductor Lithography Equipment Industry Revenue (Million), by Type 2025 & 2033

- Figure 64: Middle East and Africa Semiconductor Lithography Equipment Industry Volume (K Unit), by Type 2025 & 2033

- Figure 65: Middle East and Africa Semiconductor Lithography Equipment Industry Revenue Share (%), by Type 2025 & 2033

- Figure 66: Middle East and Africa Semiconductor Lithography Equipment Industry Volume Share (%), by Type 2025 & 2033

- Figure 67: Middle East and Africa Semiconductor Lithography Equipment Industry Revenue (Million), by Application 2025 & 2033

- Figure 68: Middle East and Africa Semiconductor Lithography Equipment Industry Volume (K Unit), by Application 2025 & 2033

- Figure 69: Middle East and Africa Semiconductor Lithography Equipment Industry Revenue Share (%), by Application 2025 & 2033

- Figure 70: Middle East and Africa Semiconductor Lithography Equipment Industry Volume Share (%), by Application 2025 & 2033

- Figure 71: Middle East and Africa Semiconductor Lithography Equipment Industry Revenue (Million), by Country 2025 & 2033

- Figure 72: Middle East and Africa Semiconductor Lithography Equipment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 73: Middle East and Africa Semiconductor Lithography Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 74: Middle East and Africa Semiconductor Lithography Equipment Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 3: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 5: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 8: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 9: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 10: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 11: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 14: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 15: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 16: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 17: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 18: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 19: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 20: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 21: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 22: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 23: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 26: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 27: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 28: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 29: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 30: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 32: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 33: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 34: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 35: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 36: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 37: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 38: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 39: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 40: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 41: Global Semiconductor Lithography Equipment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 42: Global Semiconductor Lithography Equipment Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Lithography Equipment Industry?

The projected CAGR is approximately 7.38%.

2. Which companies are prominent players in the Semiconductor Lithography Equipment Industry?

Key companies in the market include SÜSS MicroTec SE, Veeco Instruments Inc, Canon Inc, Shanghai Micro Electronics Equipment (Group) Co Ltd, Nikon Corporation, JEOL Ltd, Neutronix Quintel Inc (NXQ)7 2 Vendor Market Share Analysi, Onto Innovation (Rudolph Technologies Inc ), ASML Holding NV, EV Group (EVG).

3. What are the main segments of the Semiconductor Lithography Equipment Industry?

The market segments include Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 26.48 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Miniaturization and Extra Functionality by Electric Vehicles and Advanced Mobile Devices; Growing Innovation by Specialist Equipment Vendors offering Brand New Lithography Tools.

6. What are the notable trends driving market growth?

Deep Ultraviolet Lithography (DUV) to Hold Major Market Share.

7. Are there any restraints impacting market growth?

Challenges Regarding Complexity of Pattern in Manufacturing Process.

8. Can you provide examples of recent developments in the market?

December 2022 - Canon Inc. launched an i-line lithography stepper for 3D advanced packaging, such as those used with chiplets mounted on an interposer. The FPA-5520iV LF2, based on 365nm wavelength light, is optimized for back-end processing and delivers 0.8-micron resolution across a 52 mm by 68 mm single-exposure field. A four-shot mode extends the area to 100 mm by 100 mm.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Semiconductor Lithography Equipment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Semiconductor Lithography Equipment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Semiconductor Lithography Equipment Industry?

To stay informed about further developments, trends, and reports in the Semiconductor Lithography Equipment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence