Key Insights

The global RNA interference (RNAi) based biopesticides market is experiencing robust growth, projected to reach an estimated USD 9.5 billion in 2024. This expansion is fueled by a significant Compound Annual Growth Rate (CAGR) of 12.7% from 2025 to 2033, indicating a strong upward trajectory for this innovative segment of crop protection. The primary drivers behind this impressive growth include increasing global demand for sustainable agricultural practices, growing consumer preference for organic and residue-free produce, and rising concerns about the environmental and health impacts of conventional chemical pesticides. Regulatory support for biopesticides and advancements in RNAi technology, leading to more effective and targeted pest control solutions, are also crucial accelerators. The market is witnessing a surge in research and development, with key players investing in novel formulations and delivery mechanisms to enhance the efficacy and commercial viability of RNAi biopesticides.

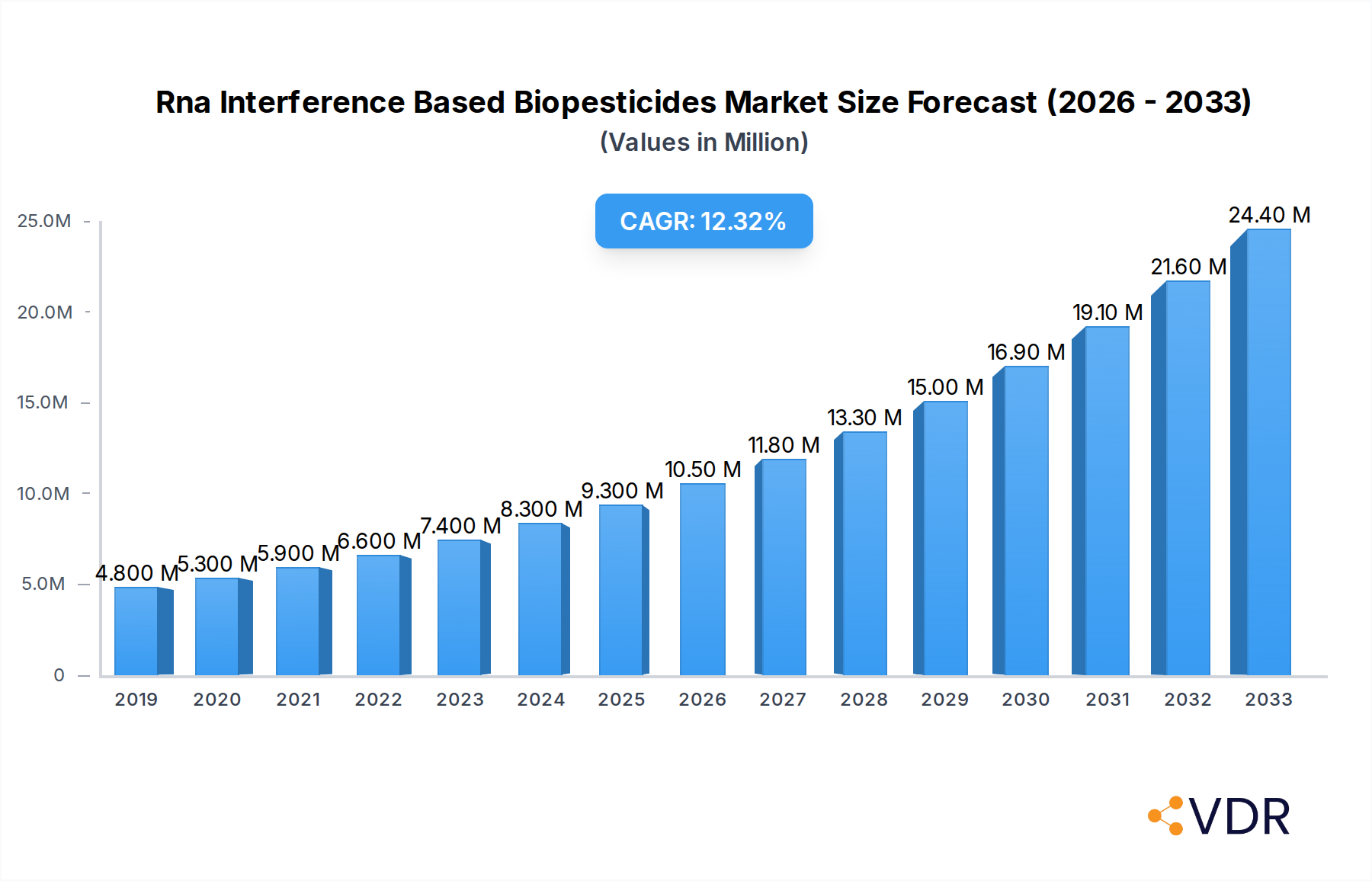

Rna Interference Based Biopesticides Market Size (In Million)

The market is segmented by application, with Farmland dominating due to the extensive acreage requiring pest management, followed by Orchards. In terms of type, Plant-Incorporated Protectants (PIP) are gaining traction for their targeted action and reduced environmental dispersal, although Non-PIP formulations continue to hold a significant share. Leading companies such as Bayer, Syngenta, and BASF are actively involved in this space, alongside specialized RNAi biopesticide developers like Greenlight Biosciences and RNAissance Ag, pushing the boundaries of innovation. North America and Europe are currently the leading regions, driven by stringent regulations on chemical pesticides and a well-established sustainable agriculture framework. However, the Asia Pacific region is poised for substantial growth due to its large agricultural base and increasing adoption of advanced farming techniques. Emerging restraints, such as the higher initial cost of some RNAi products and the need for broader farmer education and adoption, are being addressed through technological advancements and strategic market penetration efforts.

Rna Interference Based Biopesticides Company Market Share

Unlocking the Future of Sustainable Agriculture: RNA Interference (RNAi) Based Biopesticides Market Report

This comprehensive market research report delves deep into the burgeoning RNA interference (RNAi) based biopesticides market, a revolutionary segment poised to transform global crop protection. As the agricultural industry grapples with the need for eco-friendly pest management solutions, RNAi technology emerges as a powerful, precise, and sustainable alternative to conventional chemical pesticides. This report offers an in-depth analysis of market dynamics, growth trajectories, key players, and future opportunities, providing invaluable insights for stakeholders.

Study Period: 2019–2033 Base Year: 2025 Estimated Year: 2025 Forecast Period: 2025–2033 Historical Period: 2019–2024

Rna Interference Based Biopesticides Market Dynamics & Structure

The RNAi biopesticides market is characterized by a dynamic interplay of technological innovation, evolving regulatory landscapes, and increasing demand for sustainable agricultural practices. Market concentration is gradually shifting as established agrochemical giants like Bayer, Syngenta, BASF, and Corteva invest heavily in acquiring or developing RNAi-based solutions, alongside agile innovators such as Greenlight Biosciences, RNAissance Ag, Pebble Labs, Renaissance BioScience, and AgroSpheres. Technological innovation remains the primary driver, with continuous advancements in RNA delivery mechanisms, target specificity, and formulation stability. The regulatory framework, while still maturing, is increasingly favoring environmentally benign biopesticides, creating a more favorable environment for RNAi adoption. Competitive product substitutes include traditional chemical pesticides, other biopesticides (e.g., microbial, botanical), and integrated pest management (IPM) strategies. End-user demographics are expanding from large-scale commercial farms to smaller, organic producers seeking advanced pest control. Mergers and acquisitions (M&A) are a significant trend, with larger companies strategically acquiring promising RNAi startups to bolster their portfolios and accelerate market entry. For instance, a projected xx billion unit M&A volume is expected within the forecast period as companies consolidate expertise. Barriers to entry include the high cost of R&D, lengthy regulatory approval processes, and the need for extensive field trials to demonstrate efficacy and safety.

- Market Concentration: Emerging, with increasing involvement of major agrochemical players alongside specialized biotech firms.

- Technological Innovation Drivers: Precision pest targeting, reduced environmental impact, resistance management.

- Regulatory Frameworks: Evolving, with a trend towards greater acceptance of biopesticides.

- Competitive Product Substitutes: Conventional chemical pesticides, other biopesticides, IPM.

- End-User Demographics: Diversifying from large-scale commercial farms to organic and specialty crop growers.

- M&A Trends: Active, with strategic acquisitions to gain access to novel technologies and market share.

Rna Interference Based Biopesticides Growth Trends & Insights

The RNAi biopesticides market is on an upward trajectory, driven by a confluence of factors propelling its growth from an estimated xx billion units in 2025 to a projected xx billion units by 2033, exhibiting a robust CAGR of xx%. This significant expansion is fueled by increasing global awareness of the detrimental effects of synthetic pesticides on ecosystems and human health, alongside growing consumer preference for sustainably grown produce. The adoption rates of RNAi-based solutions are steadily climbing as farmers witness their efficacy and favorable environmental profiles. Technological disruptions, such as advancements in gene synthesis, RNA delivery systems, and the development of novel RNA sequences targeting a wider spectrum of pests, are continuously enhancing the performance and applicability of these biopesticides. Consumer behavior shifts towards organic and residue-free food products are directly influencing demand for effective and safe pest management tools like RNAi biopesticides. Market penetration is expected to rise from xx% in 2025 to xx% by 2033, indicating a significant shift in the global pest control paradigm. The development of RNAi biopesticides targeting specific insect species with high precision minimizes off-target effects, a critical advantage over broad-spectrum chemical pesticides. Furthermore, the potential for RNAi to overcome pest resistance issues that plague conventional pesticides adds another layer of growth potential. The market is also benefiting from government initiatives promoting sustainable agriculture and the development of bio-based solutions. The increasing investment in research and development by both established corporations and innovative startups is crucial in overcoming technical hurdles and bringing new products to market. The base year value of xx billion units highlights the foundational strength from which this sector is expanding. The estimated value of xx billion units in 2025 signifies the immediate market potential and the anticipated acceleration of adoption in the coming years. The forecast period of 2025-2033 is critical for solidifying market leadership and driving widespread integration into agricultural practices globally. The historical period of 2019-2024 has laid the groundwork, witnessing initial product development and early adoption trials, setting the stage for this remarkable growth. The market size evolution is a testament to the increasing recognition of RNAi's role in future-proof agriculture.

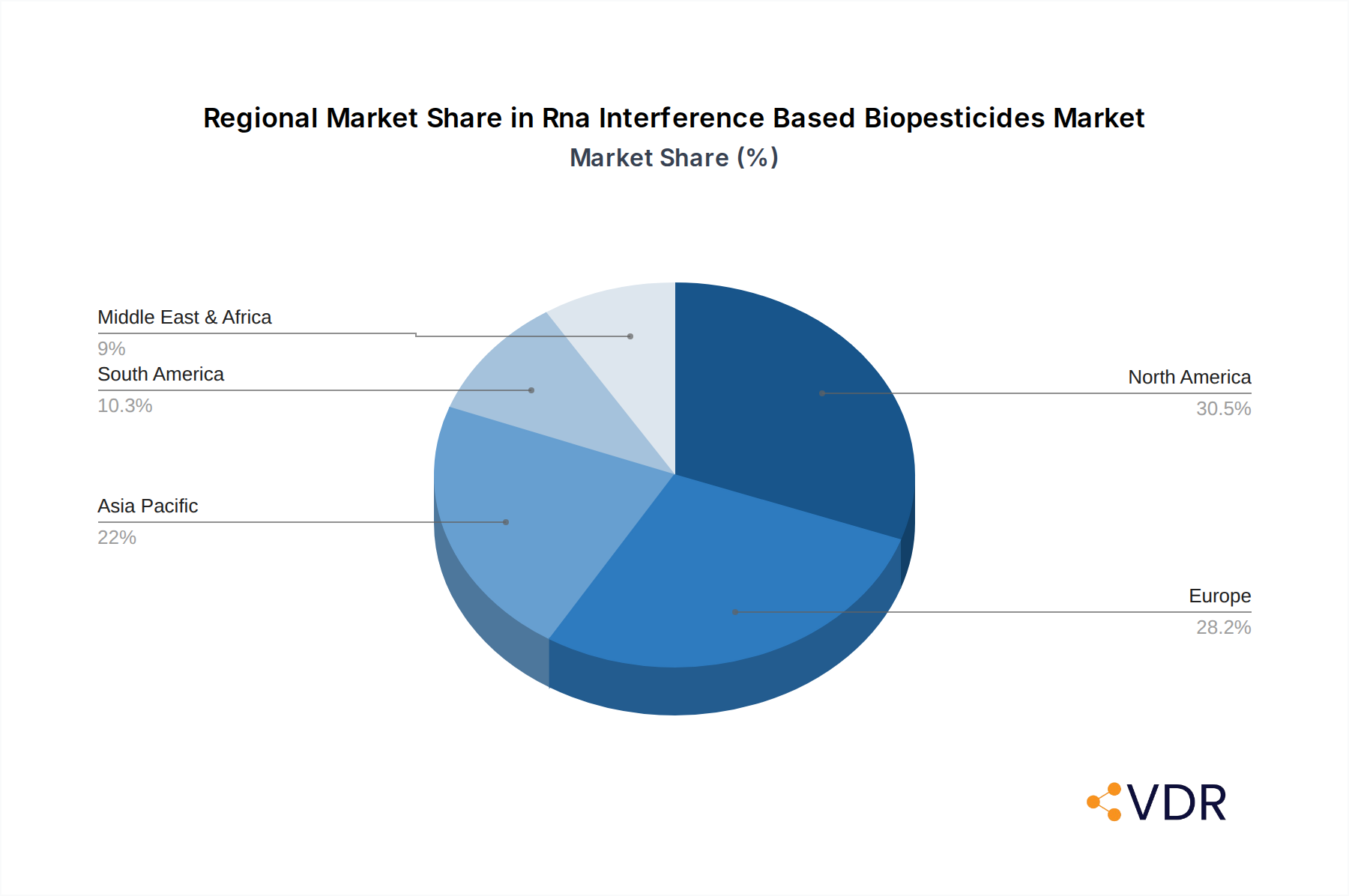

Dominant Regions, Countries, or Segments in Rna Interference Based Biopesticides

The RNAi biopesticides market is witnessing accelerated growth driven by specific regions and segments that are at the forefront of adopting sustainable agriculture. The Farmland application segment, encompassing broad-acre crops, is projected to dominate the market due to the sheer scale of agricultural production and the pressing need for effective pest control across vast cultivated areas. This segment is expected to contribute approximately xx% to the overall market revenue by 2033. Within this segment, countries with advanced agricultural infrastructures and strong regulatory support for biopesticides are leading the charge.

North America, particularly the United States, is identified as a dominant region. The presence of leading agrochemical companies, a strong research and development ecosystem, and proactive government policies supporting sustainable farming practices are key drivers. The region's extensive agricultural land, coupled with a high adoption rate of new technologies, further solidifies its leading position. The market share of North America in the global RNAi biopesticides market is estimated to be around xx% in 2025, projected to grow to xx% by 2033.

In terms of product type, the Non-PIP (Non-Plant-Incorporated Protectant) segment is anticipated to experience more rapid growth in the near to mid-term. This is attributed to the simpler regulatory pathways and faster time-to-market compared to Plant-Incorporated Protectants (PIPs). Non-PIP formulations can be applied exogenously, offering flexibility and immediate pest control. The market share of the Non-PIP segment is expected to rise from xx% in 2025 to xx% by 2033. However, PIPs hold significant long-term potential as they offer inherent protection within the plant, reducing the need for external applications and potentially leading to more cost-effective solutions over time.

Key drivers for dominance in these segments include:

- Economic Policies: Government subsidies, tax incentives, and grants for sustainable agriculture and biopesticide development.

- Infrastructure: Robust agricultural supply chains, research institutions, and distribution networks.

- Regulatory Landscape: Favorable regulatory approvals and streamlined processes for biopesticide registration.

- Technological Adoption: High willingness and capacity of farmers to adopt innovative pest management solutions.

- Environmental Awareness: Growing public and governmental pressure to reduce the environmental footprint of agriculture.

The Orchard segment, while smaller in scale compared to Farmland, presents substantial growth potential due to the high-value nature of orchard crops and the stringent residue requirements for fruits and nuts. The "Others" application segment, encompassing greenhouses, turf, and ornamental plants, also offers niche growth opportunities.

Rna Interference Based Biopesticides Product Landscape

The RNAi biopesticides product landscape is characterized by a wave of innovative formulations designed for enhanced efficacy, specificity, and environmental compatibility. Companies are focusing on developing RNAi products that precisely target critical genes in pest species, disrupting vital biological processes like development, reproduction, or nutrient absorption, leading to mortality or reduced infestation. These products often boast unique selling propositions such as high potency against target pests, minimal impact on beneficial insects and non-target organisms, and rapid biodegradation in the environment, leaving no harmful residues. Technological advancements include the development of novel delivery systems that protect RNA molecules from degradation and facilitate their uptake by pests, alongside the continuous exploration of new target genes for a broader pest spectrum.

Key Drivers, Barriers & Challenges in Rna Interference Based Biopesticides

Key Drivers: The RNAi biopesticides market is propelled by several key factors. The escalating demand for sustainable and environmentally friendly agricultural practices is a primary driver, fueled by growing concerns over the ecological and health impacts of conventional chemical pesticides. Technological advancements in RNA synthesis and delivery systems are making these biopesticides more effective and cost-efficient. Furthermore, the ability of RNAi to overcome pest resistance issues that plague traditional pesticides provides a significant competitive advantage. Regulatory bodies worldwide are increasingly supportive of biopesticide development, creating a more conducive environment for market entry.

Barriers & Challenges: Despite the promising outlook, the market faces significant challenges. The high cost of research and development, coupled with lengthy and complex regulatory approval processes, presents a substantial barrier to entry. Ensuring the stability and shelf-life of RNAi formulations in diverse environmental conditions remains a technical hurdle. Public perception and education regarding the safety and efficacy of novel biopesticides also require attention. Supply chain complexities in manufacturing and distributing specialized biological products can lead to logistical challenges. Moreover, competition from established chemical pesticides, which often have lower upfront costs and familiar application methods, continues to be a restraint, with an estimated xx billion unit market share held by conventional pesticides that needs to be addressed.

Emerging Opportunities in Rna Interference Based Biopesticides

Emerging opportunities in the RNAi biopesticides market are abundant and diverse. The untapped potential in developing countries, where sustainable agricultural practices are gaining traction, presents significant growth avenues. Innovative applications are emerging, such as the development of RNAi formulations for seed treatments, offering early-stage protection against soil-borne pests. Evolving consumer preferences for organic and pesticide-free produce are creating a strong demand for residue-free pest control solutions. The development of multi-target RNAi products that can combat a broader range of pests or address resistance in a single application is another promising area. Furthermore, the integration of RNAi technology with digital agriculture platforms for precision application and monitoring can unlock new levels of efficiency.

Growth Accelerators in the Rna Interference Based Biopesticides Industry

Several growth accelerators are poised to significantly boost the long-term expansion of the RNAi biopesticides industry. Technological breakthroughs in areas like synthetic biology, artificial intelligence for target gene discovery, and advanced formulation science will continuously enhance product efficacy and reduce production costs. Strategic partnerships and collaborations between research institutions, biotech startups, and major agrochemical companies are crucial for accelerating R&D, navigating regulatory pathways, and scaling up production. Market expansion strategies, including penetrating new geographical regions and diversifying product portfolios to address a wider range of crops and pests, will be vital. The increasing focus on integrated pest management (IPM) programs, where RNAi biopesticides can play a synergistic role, will also drive adoption.

Key Players Shaping the Rna Interference Based Biopesticides Market

- Bayer

- Syngenta

- BASF

- Corteva

- Greenlight Biosciences

- RNAissance Ag

- Pebble Labs

- Renaissance BioScience

- AgroSpheres

Notable Milestones in Rna Interference Based Biopesticides Sector

- 2021: Greenlight Biosciences secures Series C funding to advance its RNAi platform for agriculture.

- 2022: RNAissance Ag announces successful field trials for its novel RNAi biopesticide targeting specific lepidopteran pests.

- 2023: Pebble Labs receives regulatory approval for its first RNAi-based solution in a key agricultural market.

- 2023: Renaissance BioScience enters into a strategic partnership with a major agricultural distributor to expand market reach.

- 2024: AgroSpheres showcases its proprietary delivery system for enhanced RNAi efficacy at a leading agricultural technology conference.

In-Depth Rna Interference Based Biopesticides Market Outlook

The future market outlook for RNAi biopesticides is exceptionally strong, driven by a confluence of accelerating factors. The persistent global drive towards sustainable agriculture, coupled with increasing regulatory favorability towards biopesticides, will continue to fuel demand. Technological innovation, particularly in precision targeting and cost-effective production, is expected to overcome existing market barriers. Strategic alliances and acquisitions will consolidate market leadership and accelerate product development cycles. The expanding consumer demand for residue-free food products provides a powerful impetus for the adoption of RNAi solutions. The market is poised for significant growth, estimated to reach xx billion units by 2033, presenting substantial opportunities for innovation and investment in this transformative sector of crop protection.

Rna Interference Based Biopesticides Segmentation

-

1. Application

- 1.1. Farmland

- 1.2. Orchard

- 1.3. Others

-

2. Type

- 2.1. Plant-Incorporated Protectant (PIP)

- 2.2. Non-PIP (Non-Plant-Incorporated Protectant)

Rna Interference Based Biopesticides Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Rna Interference Based Biopesticides Regional Market Share

Geographic Coverage of Rna Interference Based Biopesticides

Rna Interference Based Biopesticides REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Rna Interference Based Biopesticides Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Farmland

- 5.1.2. Orchard

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Plant-Incorporated Protectant (PIP)

- 5.2.2. Non-PIP (Non-Plant-Incorporated Protectant)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Rna Interference Based Biopesticides Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Farmland

- 6.1.2. Orchard

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Plant-Incorporated Protectant (PIP)

- 6.2.2. Non-PIP (Non-Plant-Incorporated Protectant)

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Rna Interference Based Biopesticides Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Farmland

- 7.1.2. Orchard

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Plant-Incorporated Protectant (PIP)

- 7.2.2. Non-PIP (Non-Plant-Incorporated Protectant)

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Rna Interference Based Biopesticides Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Farmland

- 8.1.2. Orchard

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Plant-Incorporated Protectant (PIP)

- 8.2.2. Non-PIP (Non-Plant-Incorporated Protectant)

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Rna Interference Based Biopesticides Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Farmland

- 9.1.2. Orchard

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Plant-Incorporated Protectant (PIP)

- 9.2.2. Non-PIP (Non-Plant-Incorporated Protectant)

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Rna Interference Based Biopesticides Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Farmland

- 10.1.2. Orchard

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Plant-Incorporated Protectant (PIP)

- 10.2.2. Non-PIP (Non-Plant-Incorporated Protectant)

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Bayer

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Syngenta

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 BASF

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Corteva

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Greenlight Biosciences

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 RNAissance Ag

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Pebble Labs

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Renaissance BioScience

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 AgroSpheres

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 Bayer

List of Figures

- Figure 1: Global Rna Interference Based Biopesticides Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Rna Interference Based Biopesticides Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Rna Interference Based Biopesticides Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Rna Interference Based Biopesticides Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Rna Interference Based Biopesticides Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Rna Interference Based Biopesticides Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Rna Interference Based Biopesticides Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Rna Interference Based Biopesticides Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Rna Interference Based Biopesticides Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Rna Interference Based Biopesticides Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Rna Interference Based Biopesticides Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Rna Interference Based Biopesticides Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Rna Interference Based Biopesticides Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Rna Interference Based Biopesticides Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Rna Interference Based Biopesticides Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Rna Interference Based Biopesticides Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Rna Interference Based Biopesticides Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Rna Interference Based Biopesticides Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Rna Interference Based Biopesticides Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Rna Interference Based Biopesticides Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Rna Interference Based Biopesticides Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Rna Interference Based Biopesticides Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Rna Interference Based Biopesticides Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Rna Interference Based Biopesticides Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Rna Interference Based Biopesticides Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Rna Interference Based Biopesticides Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Rna Interference Based Biopesticides Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Rna Interference Based Biopesticides Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Rna Interference Based Biopesticides Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Rna Interference Based Biopesticides Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Rna Interference Based Biopesticides Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Rna Interference Based Biopesticides Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Rna Interference Based Biopesticides Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Rna Interference Based Biopesticides Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Rna Interference Based Biopesticides Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Rna Interference Based Biopesticides Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Rna Interference Based Biopesticides Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Rna Interference Based Biopesticides Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Rna Interference Based Biopesticides Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Rna Interference Based Biopesticides Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Rna Interference Based Biopesticides Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Rna Interference Based Biopesticides Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Rna Interference Based Biopesticides Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Rna Interference Based Biopesticides Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Rna Interference Based Biopesticides Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Rna Interference Based Biopesticides Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Rna Interference Based Biopesticides Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Rna Interference Based Biopesticides Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Rna Interference Based Biopesticides Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Rna Interference Based Biopesticides Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Rna Interference Based Biopesticides?

The projected CAGR is approximately 12.7%.

2. Which companies are prominent players in the Rna Interference Based Biopesticides?

Key companies in the market include Bayer, Syngenta, BASF, Corteva, Greenlight Biosciences, RNAissance Ag, Pebble Labs, Renaissance BioScience, AgroSpheres.

3. What are the main segments of the Rna Interference Based Biopesticides?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Rna Interference Based Biopesticides," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Rna Interference Based Biopesticides report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Rna Interference Based Biopesticides?

To stay informed about further developments, trends, and reports in the Rna Interference Based Biopesticides, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence