Key Insights

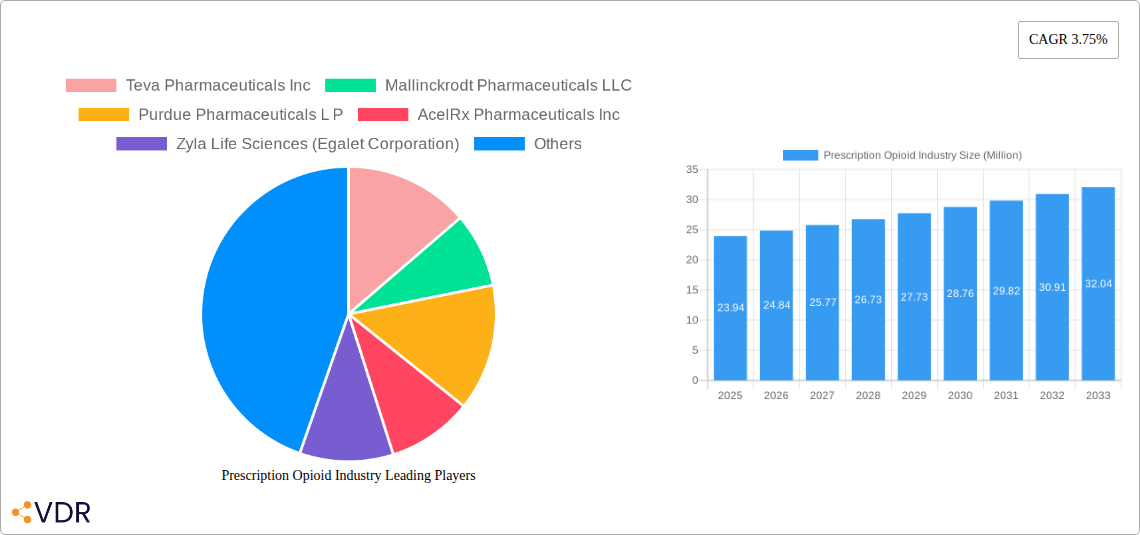

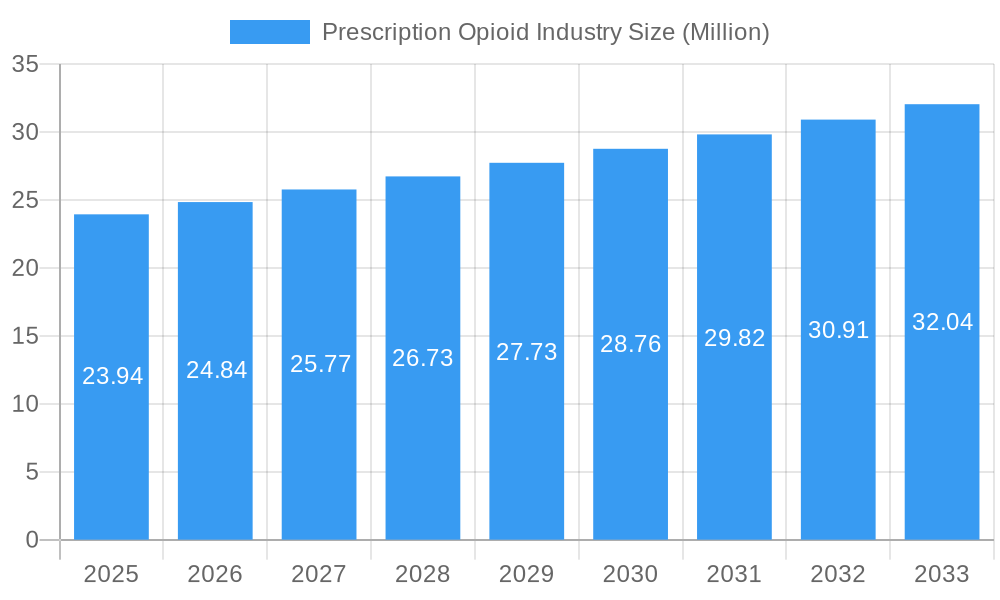

The global Prescription Opioid market is poised for steady growth, projected to reach approximately USD 23.94 million by 2025, with a Compound Annual Growth Rate (CAGR) of 3.75% anticipated from 2025 to 2033. This expansion is primarily driven by the escalating prevalence of chronic pain conditions, including neuropathic pain and osteoarthritis, which necessitates effective pain management solutions. Furthermore, the increasing incidence of post-operative pain and the limited availability of alternative pain relief options are contributing significantly to the market's upward trajectory. The expanding geriatric population, often experiencing a higher burden of chronic diseases, also represents a key demographic fueling demand for prescription opioids. While concerns surrounding opioid addiction and regulatory scrutiny persist, ongoing research and development efforts are focused on creating safer formulations and exploring novel delivery mechanisms to mitigate these risks.

Prescription Opioid Industry Market Size (In Million)

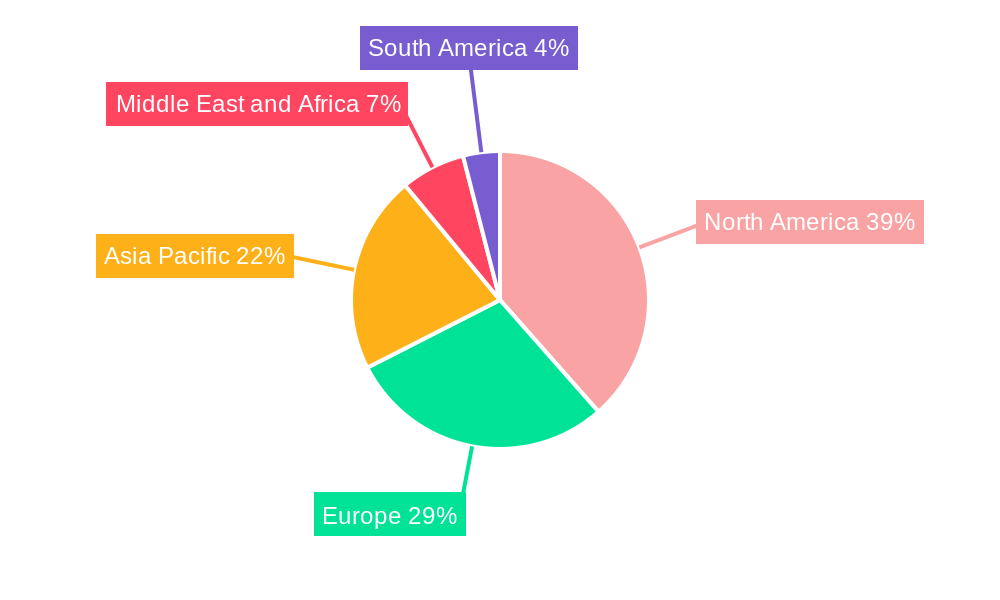

The market is segmented across various product types, with Codeine, Fentanyl, and Morphine emerging as leading segments due to their established efficacy in managing moderate to severe pain. Strong agonists, in particular, dominate the receptor binding landscape. Beyond pain management, prescription opioids find applications in treating coughs, diarrhea, and other conditions, albeit to a lesser extent. Geographically, North America currently holds a significant market share, driven by a high prevalence of chronic pain and advanced healthcare infrastructure. However, the Asia Pacific region is expected to witness the fastest growth, propelled by improving healthcare access, rising disposable incomes, and an increasing awareness of pain management treatments. Key players such as Teva Pharmaceuticals, Mallinckrodt Pharmaceuticals, and Purdue Pharmaceuticals are actively involved in research, development, and strategic collaborations to maintain their market positions and innovate within this complex therapeutic area.

Prescription Opioid Industry Company Market Share

Comprehensive Report on the Prescription Opioid Industry: Market Dynamics, Growth Trends, and Future Outlook (2019–2033)

This in-depth report provides a thorough analysis of the global Prescription Opioid Industry, offering critical insights into market dynamics, growth trajectories, and competitive landscapes. Covering the period from 2019 to 2033, with a base and estimated year of 2025, this research is indispensable for pharmaceutical manufacturers, healthcare providers, regulatory bodies, and investors seeking to understand the evolving market for potent analgesics and related therapeutic applications. We delve into parent and child markets, presenting data in million units for clarity and strategic decision-making.

Prescription Opioid Industry Market Dynamics & Structure

The Prescription Opioid Industry is characterized by a complex interplay of market concentration, intense technological innovation, and a dynamic regulatory environment. Leading pharmaceutical giants like Johnson and Johnson, Pfizer Inc, and AbbVie Inc (Allergan PLC) often dominate market share through extensive R&D and established distribution networks. However, the market also sees significant activity from specialized players such as Mallinckrodt Pharmaceuticals LLC, Purdue Pharmaceuticals L P, and Amneal Pharmaceuticals Inc, particularly in niche product categories or generic formulations. Technological innovation is a critical driver, focusing on developing safer opioid formulations with reduced abuse potential and exploring novel delivery systems to enhance patient outcomes. Regulatory frameworks, particularly those addressing opioid prescribing guidelines and abuse deterrence, significantly shape market entry and product development strategies. Competitive product substitutes, including non-opioid analgesics and alternative pain management therapies, exert pressure on market growth. End-user demographics, primarily aging populations and individuals suffering from chronic or severe acute pain, continue to fuel demand. Mergers and acquisitions (M&A) activity, while potentially consolidating market power, also signifies strategic moves to acquire innovative pipelines or expand product portfolios. The market faces innovation barriers such as lengthy clinical trial processes, stringent regulatory approvals, and public perception challenges related to opioid use.

- Market Concentration: Dominated by a few large pharmaceutical companies with significant R&D and manufacturing capabilities.

- Technological Innovation Drivers: Focus on abuse-deterrent formulations, novel delivery systems, and non-addictive pain management alternatives.

- Regulatory Frameworks: Strict regulations concerning prescribing, dispensing, and manufacturing impact market access and product lifecycle.

- Competitive Product Substitutes: Increasing availability and adoption of non-opioid analgesics and interventional pain management techniques.

- End-User Demographics: Growing demand driven by an aging global population and the increasing prevalence of chronic pain conditions.

- M&A Trends: Strategic acquisitions aimed at strengthening R&D pipelines and expanding market reach in pain management.

Prescription Opioid Industry Growth Trends & Insights

The Prescription Opioid Industry is poised for significant growth, driven by an increasing global demand for effective pain management solutions, particularly for severe and chronic conditions. The market size evolution is projected to showcase a steady upward trajectory, influenced by advancements in drug formulation and an expanding patient base. Adoption rates for novel opioid analgesics, especially those with enhanced safety profiles or targeted delivery mechanisms, are expected to climb as healthcare providers and patients seek more reliable and less risky treatment options. Technological disruptions are at the forefront, with a notable emphasis on developing opioid formulations that are more resistant to diversion and abuse, thereby addressing public health concerns while still providing essential pain relief. Consumer behavior shifts are also playing a crucial role; there's a growing awareness among patients regarding the risks associated with opioids, leading to a more informed demand for carefully managed prescriptions and a greater openness to alternative therapies when appropriate.

The CAGR of the Prescription Opioid Industry is estimated to be influenced by a confluence of factors, including the aging global population, the rising incidence of chronic diseases, and the ongoing research into more effective and safer pain management strategies. Market penetration for specific opioid classes, such as potent synthetic opioids like Fentanyl, will continue to be a significant metric, balanced against regulatory scrutiny and the development of non-opioid alternatives. The historical period (2019–2024) has seen fluctuations due to evolving regulations and public discourse, but the forecast period (2025–2033) anticipates a more stable growth pattern driven by unmet medical needs and therapeutic innovation. The strategic development of drugs like Trevena, Inc.'s OLINVYK and Esteve Pharmaceuticals' SEGLENTIS underscores the industry's commitment to innovation within the opioid analgesic space, focusing on controlled pain management for severe conditions.

Dominant Regions, Countries, or Segments in Prescription Opioid Industry

The dominance within the Prescription Opioid Industry is multifaceted, with Pain Management emerging as the most significant application segment driving market growth. Within this broad application, Cancer Pain and Neuropathic Pain are particularly influential, demanding potent analgesics where opioids remain a cornerstone of treatment. The Strong Agonist receptor binding category, encompassing powerful opioids like Fentanyl and Morphine, commands a substantial market share due to its efficacy in managing severe and intractable pain, especially in oncology and palliative care settings.

Geographically, North America, particularly the United States, historically represents a dominant region due to high healthcare expenditure, advanced pharmaceutical research and development infrastructure, and a significant patient population suffering from chronic pain conditions. However, the Asia-Pacific region is exhibiting rapid growth potential, fueled by improving healthcare access, a growing prevalence of chronic diseases, and increasing investments in pharmaceutical manufacturing. The Product Type segment is led by Fentanyl and Morphine, owing to their established efficacy in managing severe pain and their widespread use in both hospital and outpatient settings. Codeine also maintains a significant presence, primarily for milder pain and cough suppression.

Key drivers contributing to the dominance of these segments include:

- Economic Policies: Government initiatives promoting pain management research and development, as well as healthcare access, play a crucial role.

- Infrastructure: Advanced healthcare infrastructure in developed regions supports the widespread availability and administration of prescription opioids.

- Disease Prevalence: The increasing incidence of chronic pain conditions, cancer, and post-surgical pain globally directly fuels demand for effective analgesics.

- Technological Advancements: Innovations in drug delivery systems and abuse-deterrent formulations are enhancing the safety and efficacy profiles of prescription opioids, leading to increased adoption.

- Regulatory Landscape: While stringent, regulations often aim to ensure the appropriate use of these powerful medications, thereby sustaining demand from legitimate medical needs.

The market share for strong agonists in severe pain management remains high, despite ongoing efforts to develop and promote non-opioid alternatives. The robust demand for effective pain relief in critical care and end-of-life scenarios solidifies the position of Fentanyl and Morphine.

Prescription Opioid Industry Product Landscape

The prescription opioid product landscape is characterized by ongoing innovation focused on improving efficacy, safety, and patient convenience. Key product innovations include the development of abuse-deterrent formulations (ADFs) designed to resist crushing, chewing, or dissolving, thereby mitigating diversion and misuse. Novel delivery systems, such as transdermal patches, extended-release formulations, and intravenous administrations, are also enhancing patient adherence and therapeutic outcomes. Performance metrics such as onset of action, duration of effect, and side effect profiles are critical for differentiation. Unique selling propositions often revolve around faster pain relief, prolonged analgesia with fewer doses, and reduced risks of respiratory depression or addiction. Technological advancements are also exploring combination therapies and personalized medicine approaches to optimize pain management for individual patient needs.

Key Drivers, Barriers & Challenges in Prescription Opioid Industry

Key Drivers:

- Rising Global Pain Burden: The increasing prevalence of chronic and acute pain conditions, driven by aging populations and lifestyle factors, is a primary growth accelerator.

- Medical Advancements in Pain Management: Continuous R&D efforts leading to safer, more effective opioid formulations and alternative pain management strategies.

- Expanding Healthcare Access: Growing access to healthcare services in emerging economies translates to increased demand for prescription medications, including opioids for severe pain.

- Technological Innovations: Development of abuse-deterrent formulations and novel drug delivery systems is enhancing product appeal and addressing safety concerns.

Barriers & Challenges:

- Regulatory Scrutiny and Opioid Crisis Concerns: Stringent regulations, prescribing limitations, and public perception due to the opioid crisis create significant hurdles for market growth and product development.

- Development of Non-Opioid Alternatives: Increasing availability and adoption of non-opioid analgesics and interventional pain management techniques pose a competitive threat.

- High R&D Costs and Long Approval Times: The pharmaceutical industry faces substantial investment requirements and lengthy approval processes for new opioid-based medications.

- Supply Chain Disruptions: Geopolitical factors and manufacturing complexities can lead to challenges in ensuring a consistent and reliable supply of essential opioid medications.

- Physician and Patient Education: Ensuring appropriate prescribing practices and patient education on safe opioid use remains a continuous challenge.

Emerging Opportunities in Prescription Opioid Industry

Emerging opportunities in the Prescription Opioid Industry lie in the development of next-generation analgesics with significantly reduced abuse liability and improved safety profiles. The untapped market for personalized pain management solutions, leveraging genetic profiling and advanced diagnostics, presents a significant growth avenue. Evolving consumer preferences are driving demand for integrated pain management strategies that combine pharmacotherapy with non-pharmacological interventions, creating opportunities for synergistic product development and service offerings. Furthermore, the expansion of healthcare infrastructure and access in developing regions offers a substantial opportunity for market penetration of essential opioid analgesics for severe pain.

Growth Accelerators in the Prescription Opioid Industry Industry

The long-term growth of the Prescription Opioid Industry is being significantly accelerated by groundbreaking technological advancements, particularly in the realm of abuse-deterrent formulations and novel drug delivery systems that enhance safety and efficacy. Strategic partnerships between pharmaceutical manufacturers and academic research institutions are fostering a more robust pipeline of innovative pain management solutions. Furthermore, market expansion strategies, including targeting underserved patient populations and expanding into emerging geographical markets with a growing need for pain management, are key catalysts for sustained growth. The increasing understanding of pain mechanisms at a molecular level also promises to unlock new therapeutic targets and drug development opportunities.

Key Players Shaping the Prescription Opioid Industry Market

- Teva Pharmaceuticals Inc

- Mallinckrodt Pharmaceuticals LLC

- Purdue Pharmaceuticals L P

- AcelRx Pharmaceuticals Inc

- Zyla Life Sciences (Egalet Corporation)

- Alcaliber SA

- Hikma Pharmaceuticals PLC

- Johnson and Johnson

- Amneal Pharmaceuticals Inc

- Vertice Pharma LLC

- AbbVie Inc (Allergan PLC)

- Endo Pharmaceuticals Inc

- Sun Pharmaceutical Industries Ltd

- Pfizer Inc

Notable Milestones in Prescription Opioid Industry Sector

- January 2022: Trevena, Inc. announced that China's National Medical Products Administration (NMPA) has accepted the submission of a New Drug Application (NDA) for OLINVYK (oliceridine) injection, a novel IV analgesic that has been approved in the United States by the Food and Drug Administration (FDA) for use in adults for the management of acute pain severe enough to require an intravenous opioid analgesic.

- October 2021: Esteve Pharmaceuticals received approval from the United States Food and Drug Administration (FDA) for SEGLENTIS (celecoxib and tramadol hydrochloride) for the management of acute pain in adults that is severe enough to require an opioid analgesic.

In-Depth Prescription Opioid Industry Market Outlook

The Prescription Opioid Industry is projected to witness substantial future market potential, driven by an unabating need for effective pain management solutions across the globe. Growth accelerators, including advancements in abuse-deterrent technologies and the increasing demand for specialized analgesics in oncology and chronic pain, are expected to shape the market positively. Strategic opportunities lie in the development of non-addictive pain relief alternatives and integrated pain management platforms that combine pharmacological and non-pharmacological approaches. The industry's ability to navigate the evolving regulatory landscape while prioritizing patient safety and therapeutic efficacy will be crucial in unlocking its full potential.

Prescription Opioid Industry Segmentation

-

1. Product Type

- 1.1. Codeine

- 1.2. Fentanyl

- 1.3. Morphine

- 1.4. Meperidine

- 1.5. Methadone

- 1.6. Other Product Types

-

2. Receptor Binding

- 2.1. Strong Agonist

- 2.2. Mild to Moderate Agonist

-

3. Application

-

3.1. Pain Management

- 3.1.1. Cancer Pain

- 3.1.2. Neuropathic Pain

- 3.1.3. Osteoarthritis Pain

- 3.1.4. Other Pain Managements

- 3.2. Cold and Cough

- 3.3. Diarrhoea

- 3.4. Other Applications

-

3.1. Pain Management

Prescription Opioid Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Prescription Opioid Industry Regional Market Share

Geographic Coverage of Prescription Opioid Industry

Prescription Opioid Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.75% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Codeine

- 5.1.2. Fentanyl

- 5.1.3. Morphine

- 5.1.4. Meperidine

- 5.1.5. Methadone

- 5.1.6. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by Receptor Binding

- 5.2.1. Strong Agonist

- 5.2.2. Mild to Moderate Agonist

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Pain Management

- 5.3.1.1. Cancer Pain

- 5.3.1.2. Neuropathic Pain

- 5.3.1.3. Osteoarthritis Pain

- 5.3.1.4. Other Pain Managements

- 5.3.2. Cold and Cough

- 5.3.3. Diarrhoea

- 5.3.4. Other Applications

- 5.3.1. Pain Management

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Prescription Opioid Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Codeine

- 6.1.2. Fentanyl

- 6.1.3. Morphine

- 6.1.4. Meperidine

- 6.1.5. Methadone

- 6.1.6. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by Receptor Binding

- 6.2.1. Strong Agonist

- 6.2.2. Mild to Moderate Agonist

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Pain Management

- 6.3.1.1. Cancer Pain

- 6.3.1.2. Neuropathic Pain

- 6.3.1.3. Osteoarthritis Pain

- 6.3.1.4. Other Pain Managements

- 6.3.2. Cold and Cough

- 6.3.3. Diarrhoea

- 6.3.4. Other Applications

- 6.3.1. Pain Management

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. North America Prescription Opioid Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Codeine

- 7.1.2. Fentanyl

- 7.1.3. Morphine

- 7.1.4. Meperidine

- 7.1.5. Methadone

- 7.1.6. Other Product Types

- 7.2. Market Analysis, Insights and Forecast - by Receptor Binding

- 7.2.1. Strong Agonist

- 7.2.2. Mild to Moderate Agonist

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Pain Management

- 7.3.1.1. Cancer Pain

- 7.3.1.2. Neuropathic Pain

- 7.3.1.3. Osteoarthritis Pain

- 7.3.1.4. Other Pain Managements

- 7.3.2. Cold and Cough

- 7.3.3. Diarrhoea

- 7.3.4. Other Applications

- 7.3.1. Pain Management

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Europe Prescription Opioid Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Codeine

- 8.1.2. Fentanyl

- 8.1.3. Morphine

- 8.1.4. Meperidine

- 8.1.5. Methadone

- 8.1.6. Other Product Types

- 8.2. Market Analysis, Insights and Forecast - by Receptor Binding

- 8.2.1. Strong Agonist

- 8.2.2. Mild to Moderate Agonist

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Pain Management

- 8.3.1.1. Cancer Pain

- 8.3.1.2. Neuropathic Pain

- 8.3.1.3. Osteoarthritis Pain

- 8.3.1.4. Other Pain Managements

- 8.3.2. Cold and Cough

- 8.3.3. Diarrhoea

- 8.3.4. Other Applications

- 8.3.1. Pain Management

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Asia Pacific Prescription Opioid Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Codeine

- 9.1.2. Fentanyl

- 9.1.3. Morphine

- 9.1.4. Meperidine

- 9.1.5. Methadone

- 9.1.6. Other Product Types

- 9.2. Market Analysis, Insights and Forecast - by Receptor Binding

- 9.2.1. Strong Agonist

- 9.2.2. Mild to Moderate Agonist

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Pain Management

- 9.3.1.1. Cancer Pain

- 9.3.1.2. Neuropathic Pain

- 9.3.1.3. Osteoarthritis Pain

- 9.3.1.4. Other Pain Managements

- 9.3.2. Cold and Cough

- 9.3.3. Diarrhoea

- 9.3.4. Other Applications

- 9.3.1. Pain Management

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Middle East and Africa Prescription Opioid Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Codeine

- 10.1.2. Fentanyl

- 10.1.3. Morphine

- 10.1.4. Meperidine

- 10.1.5. Methadone

- 10.1.6. Other Product Types

- 10.2. Market Analysis, Insights and Forecast - by Receptor Binding

- 10.2.1. Strong Agonist

- 10.2.2. Mild to Moderate Agonist

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Pain Management

- 10.3.1.1. Cancer Pain

- 10.3.1.2. Neuropathic Pain

- 10.3.1.3. Osteoarthritis Pain

- 10.3.1.4. Other Pain Managements

- 10.3.2. Cold and Cough

- 10.3.3. Diarrhoea

- 10.3.4. Other Applications

- 10.3.1. Pain Management

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. South America Prescription Opioid Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Codeine

- 11.1.2. Fentanyl

- 11.1.3. Morphine

- 11.1.4. Meperidine

- 11.1.5. Methadone

- 11.1.6. Other Product Types

- 11.2. Market Analysis, Insights and Forecast - by Receptor Binding

- 11.2.1. Strong Agonist

- 11.2.2. Mild to Moderate Agonist

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Pain Management

- 11.3.1.1. Cancer Pain

- 11.3.1.2. Neuropathic Pain

- 11.3.1.3. Osteoarthritis Pain

- 11.3.1.4. Other Pain Managements

- 11.3.2. Cold and Cough

- 11.3.3. Diarrhoea

- 11.3.4. Other Applications

- 11.3.1. Pain Management

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Teva Pharmaceuticals Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Mallinckrodt Pharmaceuticals LLC

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Purdue Pharmaceuticals L P

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 AcelRx Pharmaceuticals Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Zyla Life Sciences (Egalet Corporation)

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Alcaliber SA

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Hikma Pharmaceuticals PLC

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Johnson and Johnson

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Amneal Pharmaceuticals Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Vertice Pharma LLC

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 AbbVie Inc (Allergan PLC)

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Endo Pharmaceuticals Inc

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Sun Pharmaceutical Industries Ltd

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Pfizer Inc

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Teva Pharmaceuticals Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Prescription Opioid Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Prescription Opioid Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Prescription Opioid Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 4: North America Prescription Opioid Industry Volume (K Unit), by Product Type 2025 & 2033

- Figure 5: North America Prescription Opioid Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: North America Prescription Opioid Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 7: North America Prescription Opioid Industry Revenue (Million), by Receptor Binding 2025 & 2033

- Figure 8: North America Prescription Opioid Industry Volume (K Unit), by Receptor Binding 2025 & 2033

- Figure 9: North America Prescription Opioid Industry Revenue Share (%), by Receptor Binding 2025 & 2033

- Figure 10: North America Prescription Opioid Industry Volume Share (%), by Receptor Binding 2025 & 2033

- Figure 11: North America Prescription Opioid Industry Revenue (Million), by Application 2025 & 2033

- Figure 12: North America Prescription Opioid Industry Volume (K Unit), by Application 2025 & 2033

- Figure 13: North America Prescription Opioid Industry Revenue Share (%), by Application 2025 & 2033

- Figure 14: North America Prescription Opioid Industry Volume Share (%), by Application 2025 & 2033

- Figure 15: North America Prescription Opioid Industry Revenue (Million), by Country 2025 & 2033

- Figure 16: North America Prescription Opioid Industry Volume (K Unit), by Country 2025 & 2033

- Figure 17: North America Prescription Opioid Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: North America Prescription Opioid Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Europe Prescription Opioid Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 20: Europe Prescription Opioid Industry Volume (K Unit), by Product Type 2025 & 2033

- Figure 21: Europe Prescription Opioid Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 22: Europe Prescription Opioid Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 23: Europe Prescription Opioid Industry Revenue (Million), by Receptor Binding 2025 & 2033

- Figure 24: Europe Prescription Opioid Industry Volume (K Unit), by Receptor Binding 2025 & 2033

- Figure 25: Europe Prescription Opioid Industry Revenue Share (%), by Receptor Binding 2025 & 2033

- Figure 26: Europe Prescription Opioid Industry Volume Share (%), by Receptor Binding 2025 & 2033

- Figure 27: Europe Prescription Opioid Industry Revenue (Million), by Application 2025 & 2033

- Figure 28: Europe Prescription Opioid Industry Volume (K Unit), by Application 2025 & 2033

- Figure 29: Europe Prescription Opioid Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Prescription Opioid Industry Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Prescription Opioid Industry Revenue (Million), by Country 2025 & 2033

- Figure 32: Europe Prescription Opioid Industry Volume (K Unit), by Country 2025 & 2033

- Figure 33: Europe Prescription Opioid Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Europe Prescription Opioid Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Asia Pacific Prescription Opioid Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 36: Asia Pacific Prescription Opioid Industry Volume (K Unit), by Product Type 2025 & 2033

- Figure 37: Asia Pacific Prescription Opioid Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 38: Asia Pacific Prescription Opioid Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 39: Asia Pacific Prescription Opioid Industry Revenue (Million), by Receptor Binding 2025 & 2033

- Figure 40: Asia Pacific Prescription Opioid Industry Volume (K Unit), by Receptor Binding 2025 & 2033

- Figure 41: Asia Pacific Prescription Opioid Industry Revenue Share (%), by Receptor Binding 2025 & 2033

- Figure 42: Asia Pacific Prescription Opioid Industry Volume Share (%), by Receptor Binding 2025 & 2033

- Figure 43: Asia Pacific Prescription Opioid Industry Revenue (Million), by Application 2025 & 2033

- Figure 44: Asia Pacific Prescription Opioid Industry Volume (K Unit), by Application 2025 & 2033

- Figure 45: Asia Pacific Prescription Opioid Industry Revenue Share (%), by Application 2025 & 2033

- Figure 46: Asia Pacific Prescription Opioid Industry Volume Share (%), by Application 2025 & 2033

- Figure 47: Asia Pacific Prescription Opioid Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Asia Pacific Prescription Opioid Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Asia Pacific Prescription Opioid Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Prescription Opioid Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Prescription Opioid Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 52: Middle East and Africa Prescription Opioid Industry Volume (K Unit), by Product Type 2025 & 2033

- Figure 53: Middle East and Africa Prescription Opioid Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 54: Middle East and Africa Prescription Opioid Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 55: Middle East and Africa Prescription Opioid Industry Revenue (Million), by Receptor Binding 2025 & 2033

- Figure 56: Middle East and Africa Prescription Opioid Industry Volume (K Unit), by Receptor Binding 2025 & 2033

- Figure 57: Middle East and Africa Prescription Opioid Industry Revenue Share (%), by Receptor Binding 2025 & 2033

- Figure 58: Middle East and Africa Prescription Opioid Industry Volume Share (%), by Receptor Binding 2025 & 2033

- Figure 59: Middle East and Africa Prescription Opioid Industry Revenue (Million), by Application 2025 & 2033

- Figure 60: Middle East and Africa Prescription Opioid Industry Volume (K Unit), by Application 2025 & 2033

- Figure 61: Middle East and Africa Prescription Opioid Industry Revenue Share (%), by Application 2025 & 2033

- Figure 62: Middle East and Africa Prescription Opioid Industry Volume Share (%), by Application 2025 & 2033

- Figure 63: Middle East and Africa Prescription Opioid Industry Revenue (Million), by Country 2025 & 2033

- Figure 64: Middle East and Africa Prescription Opioid Industry Volume (K Unit), by Country 2025 & 2033

- Figure 65: Middle East and Africa Prescription Opioid Industry Revenue Share (%), by Country 2025 & 2033

- Figure 66: Middle East and Africa Prescription Opioid Industry Volume Share (%), by Country 2025 & 2033

- Figure 67: South America Prescription Opioid Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 68: South America Prescription Opioid Industry Volume (K Unit), by Product Type 2025 & 2033

- Figure 69: South America Prescription Opioid Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 70: South America Prescription Opioid Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 71: South America Prescription Opioid Industry Revenue (Million), by Receptor Binding 2025 & 2033

- Figure 72: South America Prescription Opioid Industry Volume (K Unit), by Receptor Binding 2025 & 2033

- Figure 73: South America Prescription Opioid Industry Revenue Share (%), by Receptor Binding 2025 & 2033

- Figure 74: South America Prescription Opioid Industry Volume Share (%), by Receptor Binding 2025 & 2033

- Figure 75: South America Prescription Opioid Industry Revenue (Million), by Application 2025 & 2033

- Figure 76: South America Prescription Opioid Industry Volume (K Unit), by Application 2025 & 2033

- Figure 77: South America Prescription Opioid Industry Revenue Share (%), by Application 2025 & 2033

- Figure 78: South America Prescription Opioid Industry Volume Share (%), by Application 2025 & 2033

- Figure 79: South America Prescription Opioid Industry Revenue (Million), by Country 2025 & 2033

- Figure 80: South America Prescription Opioid Industry Volume (K Unit), by Country 2025 & 2033

- Figure 81: South America Prescription Opioid Industry Revenue Share (%), by Country 2025 & 2033

- Figure 82: South America Prescription Opioid Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Prescription Opioid Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: Global Prescription Opioid Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 3: Global Prescription Opioid Industry Revenue Million Forecast, by Receptor Binding 2020 & 2033

- Table 4: Global Prescription Opioid Industry Volume K Unit Forecast, by Receptor Binding 2020 & 2033

- Table 5: Global Prescription Opioid Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 6: Global Prescription Opioid Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 7: Global Prescription Opioid Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Global Prescription Opioid Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Global Prescription Opioid Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 10: Global Prescription Opioid Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 11: Global Prescription Opioid Industry Revenue Million Forecast, by Receptor Binding 2020 & 2033

- Table 12: Global Prescription Opioid Industry Volume K Unit Forecast, by Receptor Binding 2020 & 2033

- Table 13: Global Prescription Opioid Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 14: Global Prescription Opioid Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 15: Global Prescription Opioid Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Prescription Opioid Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: United States Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: United States Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Canada Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Canada Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: Mexico Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Mexico Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Global Prescription Opioid Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 24: Global Prescription Opioid Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 25: Global Prescription Opioid Industry Revenue Million Forecast, by Receptor Binding 2020 & 2033

- Table 26: Global Prescription Opioid Industry Volume K Unit Forecast, by Receptor Binding 2020 & 2033

- Table 27: Global Prescription Opioid Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 28: Global Prescription Opioid Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 29: Global Prescription Opioid Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 30: Global Prescription Opioid Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Germany Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Germany Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: United Kingdom Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: United Kingdom Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: France Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: France Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Italy Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Italy Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: Spain Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Spain Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: Rest of Europe Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Rest of Europe Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: Global Prescription Opioid Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 44: Global Prescription Opioid Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 45: Global Prescription Opioid Industry Revenue Million Forecast, by Receptor Binding 2020 & 2033

- Table 46: Global Prescription Opioid Industry Volume K Unit Forecast, by Receptor Binding 2020 & 2033

- Table 47: Global Prescription Opioid Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 48: Global Prescription Opioid Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 49: Global Prescription Opioid Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 50: Global Prescription Opioid Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 51: China Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: China Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Japan Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 54: Japan Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: India Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 56: India Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 57: Australia Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 58: Australia Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 59: South Korea Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 60: South Korea Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 61: Rest of Asia Pacific Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: Rest of Asia Pacific Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Global Prescription Opioid Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 64: Global Prescription Opioid Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 65: Global Prescription Opioid Industry Revenue Million Forecast, by Receptor Binding 2020 & 2033

- Table 66: Global Prescription Opioid Industry Volume K Unit Forecast, by Receptor Binding 2020 & 2033

- Table 67: Global Prescription Opioid Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 68: Global Prescription Opioid Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 69: Global Prescription Opioid Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 70: Global Prescription Opioid Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 71: GCC Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 72: GCC Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 73: South Africa Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 74: South Africa Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: Rest of Middle East and Africa Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 76: Rest of Middle East and Africa Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: Global Prescription Opioid Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 78: Global Prescription Opioid Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 79: Global Prescription Opioid Industry Revenue Million Forecast, by Receptor Binding 2020 & 2033

- Table 80: Global Prescription Opioid Industry Volume K Unit Forecast, by Receptor Binding 2020 & 2033

- Table 81: Global Prescription Opioid Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 82: Global Prescription Opioid Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 83: Global Prescription Opioid Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 84: Global Prescription Opioid Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 85: Brazil Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 86: Brazil Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 87: Argentina Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 88: Argentina Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 89: Rest of South America Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 90: Rest of South America Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Prescription Opioid Industry?

The projected CAGR is approximately 3.75%.

2. Which companies are prominent players in the Prescription Opioid Industry?

Key companies in the market include Teva Pharmaceuticals Inc, Mallinckrodt Pharmaceuticals LLC, Purdue Pharmaceuticals L P, AcelRx Pharmaceuticals Inc, Zyla Life Sciences (Egalet Corporation), Alcaliber SA, Hikma Pharmaceuticals PLC, Johnson and Johnson, Amneal Pharmaceuticals Inc, Vertice Pharma LLC, AbbVie Inc (Allergan PLC), Endo Pharmaceuticals Inc, Sun Pharmaceutical Industries Ltd, Pfizer Inc.

3. What are the main segments of the Prescription Opioid Industry?

The market segments include Product Type, Receptor Binding, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 23.94 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Prevalence of Orthopedic Diseases and Chronic Pain; Inclination toward Extended Release Formulations from Immediate Release of Opioids; Rising Focus on Abuse-deterrent Formulation (ADF) by Generic Manufacturers.

6. What are the notable trends driving market growth?

Strong Agonists are Expected to Hold Significant Market Share in the Receptor Binding Segment.

7. Are there any restraints impacting market growth?

Advent and Legalization of Cannabis as an Alternative to Opioids; Prescription Drug Abuse.

8. Can you provide examples of recent developments in the market?

In January 2022, Trevena, Inc. announced that China's National Medical Products Administration (NMPA) has accepted the submission of a New Drug Application (NDA) for OLINVYK (oliceridine) injection, a novel IV analgesic that has been approved in the United States by the Food and Drug Administration (FDA) for use in adults for the management of acute pain severe enough to require an intravenous opioid analgesic

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Prescription Opioid Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Prescription Opioid Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Prescription Opioid Industry?

To stay informed about further developments, trends, and reports in the Prescription Opioid Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence