Key Insights

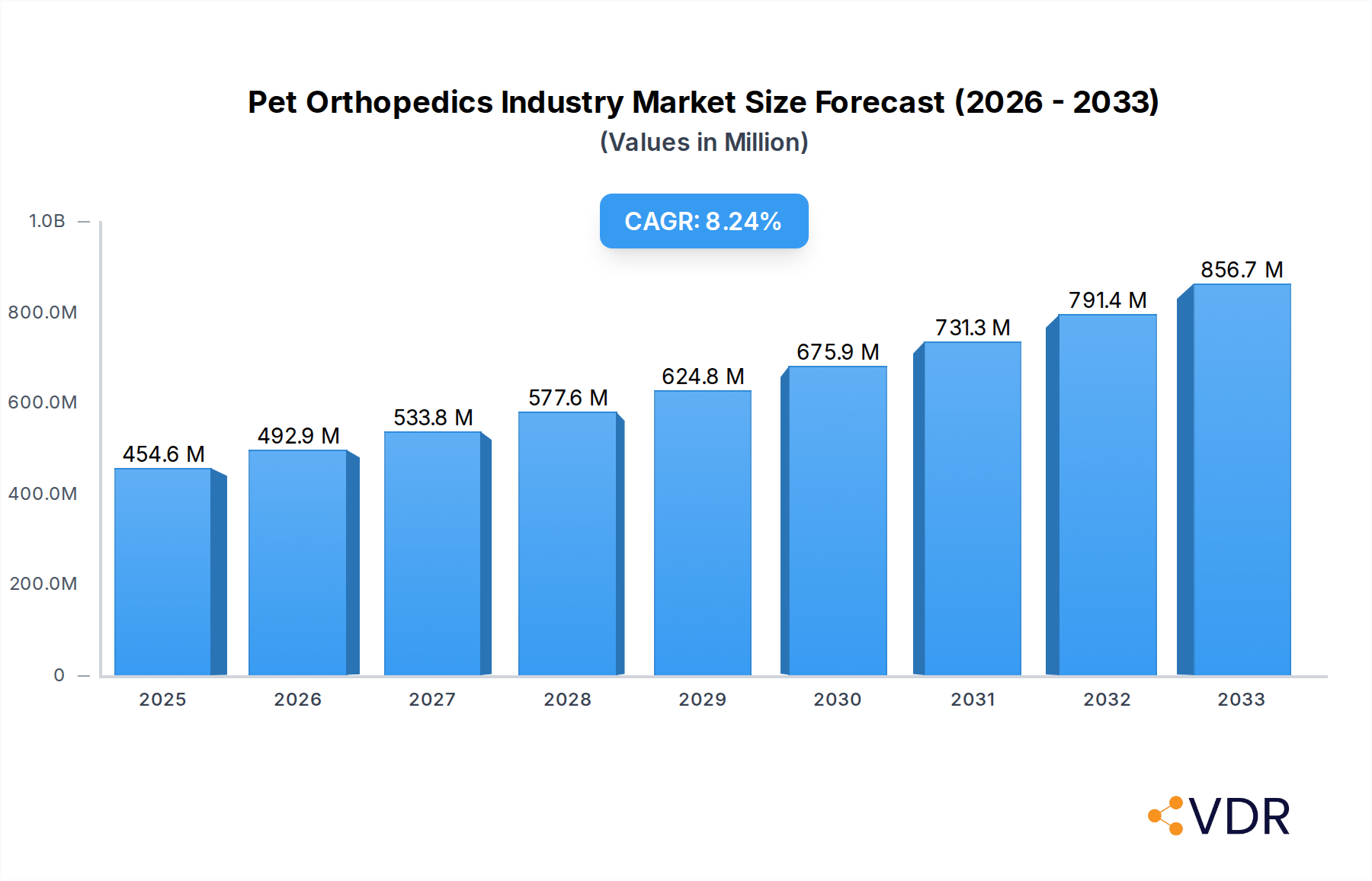

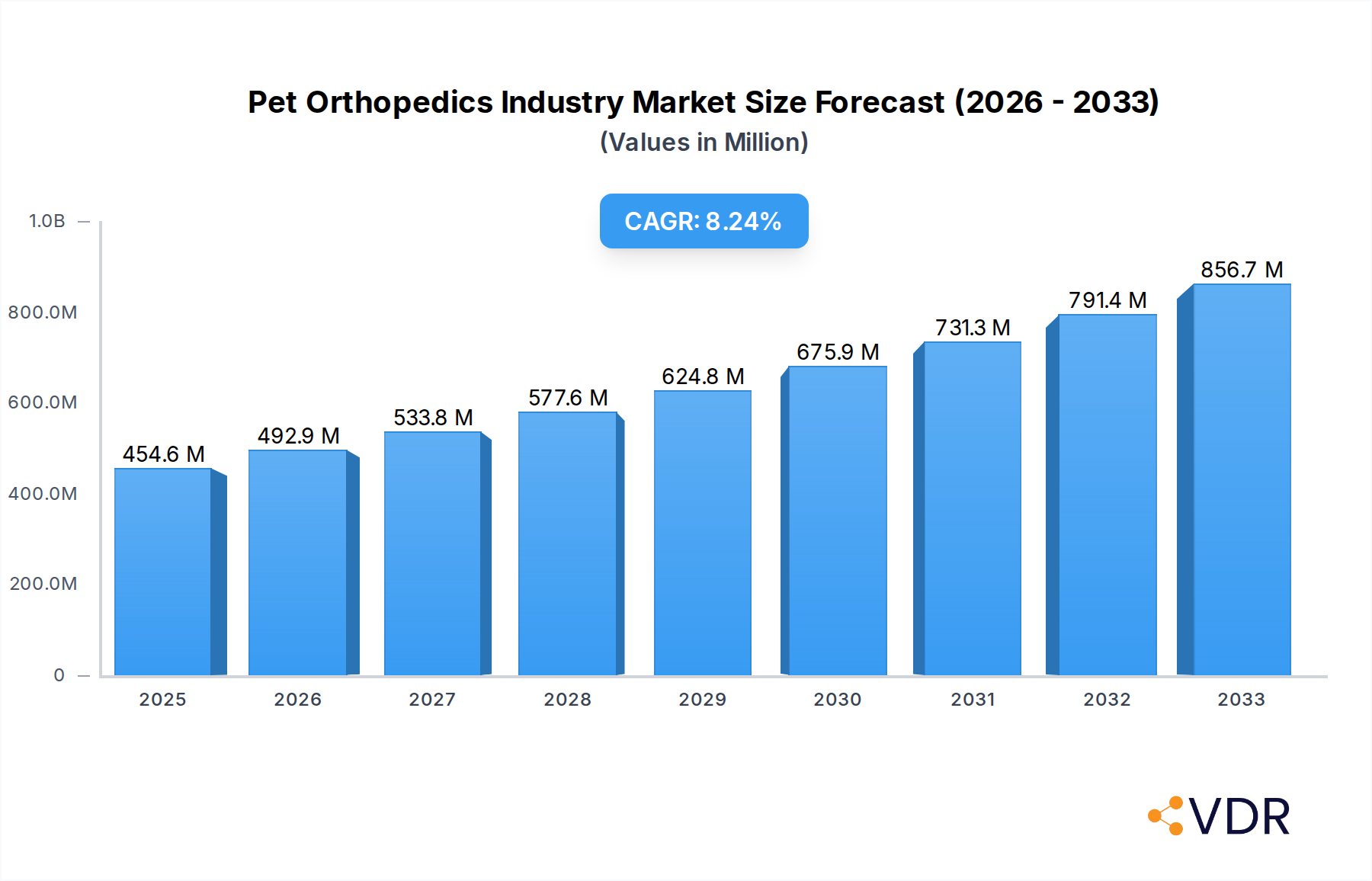

The global Pet Orthopedics Market is experiencing robust expansion, projected to reach an estimated $454.6 million in 2025 with a compound annual growth rate (CAGR) of 8.6% through 2033. This significant growth is propelled by an increasing pet humanization trend, where owners increasingly view their pets as family members and are willing to invest in advanced veterinary care. The rising incidence of orthopedic conditions such as arthritis, fractures, and developmental abnormalities in companion animals, coupled with the growing availability of sophisticated orthopedic implants and surgical instruments, further fuels market expansion. The market is segmented into key product types, including implants, instruments, screws, and others, catering to a wide range of applications such as total hip replacements, total knee replacements, trauma fixation, and other specialized procedures.

Pet Orthopedics Industry Market Size (In Million)

Several key drivers underpin the Pet Orthopedics Market's upward trajectory. The surge in pet ownership globally, particularly in developed nations, directly correlates with increased demand for veterinary orthopedic services. Advances in surgical techniques, the development of biocompatible materials for implants, and the proliferation of specialized veterinary orthopedic centers are critical growth enablers. Furthermore, growing awareness among pet owners and veterinary professionals about the benefits of orthopedic interventions for improving a pet's quality of life and mobility is a significant factor. Emerging trends include the adoption of minimally invasive surgical techniques, the use of advanced imaging technologies for diagnosis, and the development of innovative prosthetic and assistive devices. While the market exhibits strong growth, potential restraints include the high cost of advanced orthopedic procedures and implants, which can limit accessibility for some pet owners, and the need for specialized training for veterinary surgeons. Key players like Johnson & Johnson, B Braun Melsungen AG, and EVEROST INC are at the forefront of innovation, driving the market forward.

Pet Orthopedics Industry Company Market Share

Pet Orthopedics Industry Market Dynamics & Structure

The global Pet Orthopedics market exhibits a moderately concentrated structure, with key players investing heavily in research and development to drive innovation. Technological advancements, particularly in implant materials and surgical techniques, are significant drivers. Advancements in 3D printing for custom implants and minimally invasive surgical tools are reshaping treatment approaches. Regulatory frameworks, while evolving, are generally supportive of novel treatments aimed at improving animal welfare. Competitive product substitutes include advancements in regenerative medicine and non-surgical therapeutic options, though surgical interventions remain dominant for severe orthopedic conditions. End-user demographics are increasingly characterized by pet owners willing to invest more in their pets' health, viewing them as family members. This trend is fueled by rising disposable incomes and a growing awareness of advanced veterinary care. Mergers and acquisitions (M&A) trends are observed, as larger companies seek to expand their portfolios and market reach in this specialized veterinary segment. For instance, strategic acquisitions of innovative implant manufacturers by established veterinary product companies are common. The market concentration is influenced by the high cost of R&D and the specialized nature of veterinary orthopedic products. Barriers to innovation often include the lengthy approval processes for new medical devices and the need for extensive clinical validation in veterinary settings.

- Market Concentration: Moderately concentrated with a few leading global players.

- Technological Innovation Drivers: 3D printing for custom implants, advanced biomaterials, robotic-assisted surgery, and minimally invasive instruments.

- Regulatory Frameworks: Evolving to accommodate new veterinary medical devices and treatments, with a focus on safety and efficacy.

- Competitive Product Substitutes: Regenerative medicine (stem cell therapy, PRP), advanced pain management pharmaceuticals, and non-surgical physical therapy.

- End-User Demographics: Increasing pet humanization, willingness to spend on pet healthcare, and demand for specialized veterinary services.

- M&A Trends: Strategic acquisitions of innovative companies by larger veterinary corporations to enhance product offerings and market share.

- Innovation Barriers: High R&D costs, lengthy validation periods, and specialized market access.

Pet Orthopedics Industry Growth Trends & Insights

The Pet Orthopedics market is experiencing robust growth, driven by a confluence of escalating pet humanization trends, a surge in pet ownership, and a profound shift in veterinary healthcare paradigms. Pet owners are increasingly viewing their animal companions as integral family members, leading to a greater willingness to invest in advanced medical treatments, including orthopedic interventions. This heightened emotional bond translates directly into higher spending on diagnostics, surgical procedures, and post-operative care for orthopedic conditions. The market size is projected to expand significantly, driven by the increasing prevalence of age-related orthopedic issues in older pets, such as osteoarthritis and hip dysplasia, as well as an uptick in sports-related injuries in active animals.

Technological disruptions are a key catalyst for growth. Innovations in implant materials, such as the development of bio-compatible and biodegradable implants, alongside advancements in surgical instrumentation and imaging technologies, are enhancing surgical outcomes and patient recovery times. The adoption rates of these advanced solutions are steadily increasing as veterinary professionals become more familiar with and confident in their efficacy. Furthermore, the development of minimally invasive surgical techniques is making orthopedic procedures more accessible and less traumatic for pets, further boosting market penetration.

Consumer behavior is also playing a pivotal role. The proliferation of online veterinary resources and social media platforms has raised owner awareness about available orthopedic treatments, fostering demand for specialized care. This is complemented by the growing availability of veterinary financing options, which help pet owners manage the costs associated with complex procedures. The projected Compound Annual Growth Rate (CAGR) for the Pet Orthopedics industry is estimated to be robust, reflecting sustained investment in research and development, expanding indications, and increasing market penetration across various geographic regions. The market penetration is expected to deepen as more veterinary clinics acquire specialized equipment and training.

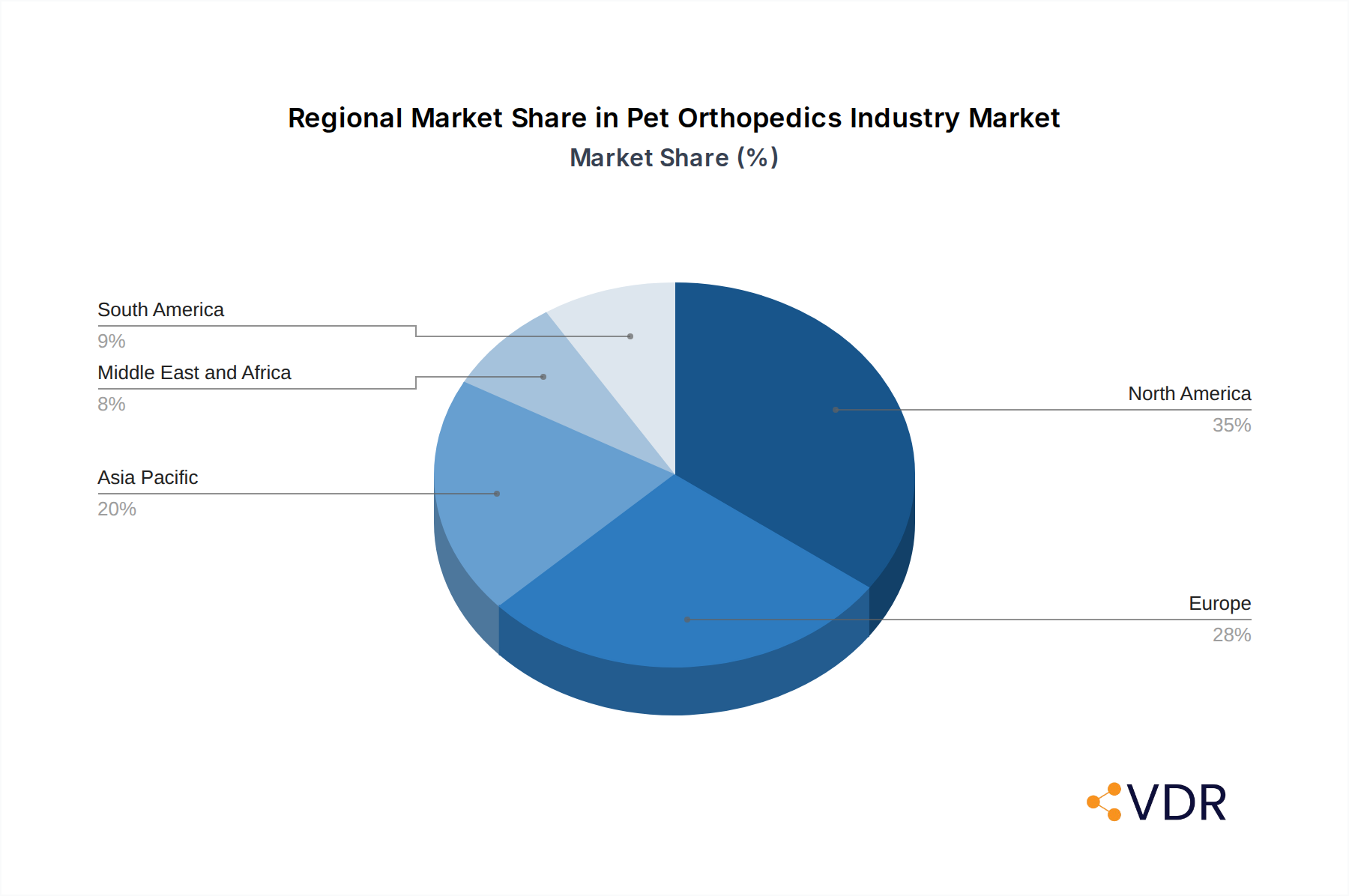

Dominant Regions, Countries, or Segments in Pet Orthopedics Industry

North America currently stands as the dominant region in the global Pet Orthopedics market, propelled by a combination of factors that foster high adoption rates and significant market investment. The region boasts a mature pet care industry, characterized by a high per-capita expenditure on companion animals and a deeply ingrained culture of advanced veterinary care. Pet owners in North America are highly educated about pet health issues and readily seek out specialized treatments to ensure the well-being of their animals.

The United States, in particular, is the leading country within this dominant region. Its extensive network of specialized veterinary orthopedic surgeons, state-of-the-art animal hospitals, and leading research institutions contribute to its market leadership. Economic policies that support small businesses, including veterinary practices, and strong intellectual property protection for medical devices further encourage innovation and investment. The infrastructure in the US is robust, with readily available access to advanced diagnostic equipment like MRI and CT scanners, which are crucial for accurate orthopedic diagnosis and surgical planning.

Within the segmentation by Type, Implants are a dominant segment, driving substantial revenue. This is directly linked to the high prevalence of conditions requiring total joint replacements and fracture fixation. The Application segment of Total hip replacement and Trauma fixation are also major contributors to market growth. The rising incidence of hip dysplasia in popular breeds and the increasing number of pet accidents requiring immediate surgical intervention underscore the importance of these applications. The market share for implants is significant, driven by the recurring need for replacement components and the continuous development of superior materials. The growth potential for these segments remains high due to ongoing research into more durable and biocompatible implant designs.

- Dominant Region: North America, primarily driven by the United States.

- Key Drivers in Dominant Region/Country: High pet expenditure, advanced veterinary infrastructure, well-established veterinary education system, and strong owner awareness.

- Dominant Segments:

- Type: Implants (e.g., hip prosthetics, knee prosthetics, bone plates).

- Application: Total hip replacement, Trauma fixation.

- Market Share & Growth Potential: Implants and applications like hip replacement and trauma fixation hold a substantial market share due to high demand and continued innovation.

Pet Orthopedics Industry Product Landscape

The product landscape within the Pet Orthopedics industry is characterized by continuous innovation focused on improving patient outcomes and surgical efficiency. Key product categories include a wide array of implants, such as custom-designed total hip and knee prosthetics, specialized bone plates, and screws tailored for various animal anatomies. Instruments are also crucial, with advancements in minimally invasive surgical tools, arthroscopic equipment, and robotic-assisted surgical systems enhancing precision and reducing patient trauma. The performance metrics of these products are evaluated based on longevity, biocompatibility, mechanical strength, and ease of surgical implantation. Unique selling propositions often lie in the development of novel biomaterials that promote faster healing and reduce implant rejection, alongside user-friendly designs for veterinary surgeons. Technological advancements are focused on creating lighter, stronger, and more adaptable implants that mimic natural bone structure and function.

Key Drivers, Barriers & Challenges in Pet Orthopedics Industry

The Pet Orthopedics industry is propelled by several key drivers, including the escalating trend of pet humanization, leading to increased willingness among owners to invest in advanced veterinary care. Technological advancements in implant design and surgical techniques, such as 3D printing for custom implants and minimally invasive procedures, are significant growth accelerators. The rising incidence of orthopedic conditions in aging pets and an increase in pet-related injuries also contribute to market expansion.

However, the industry faces notable barriers and challenges. High research and development costs for novel orthopedic devices, coupled with the rigorous and time-consuming regulatory approval processes for veterinary medical products, present significant hurdles. The limited availability of specialized veterinary orthopedic surgeons in certain regions can also restrain growth. Competitive pressures from emerging economies offering lower-cost alternatives, and the potential for supply chain disruptions for specialized materials, pose ongoing challenges. Furthermore, the economic sensitivity of pet owners, especially during economic downturns, can impact discretionary spending on advanced veterinary procedures.

Emerging Opportunities in Pet Orthopedics Industry

Emerging opportunities in the Pet Orthopedics industry are centered around untapped geographical markets, particularly in developing economies where pet ownership is growing rapidly and awareness of advanced veterinary care is increasing. The development of innovative, cost-effective implant solutions designed for a broader range of veterinary practices could significantly expand market reach. Furthermore, the application of regenerative medicine techniques in conjunction with traditional orthopedic surgery, such as using stem cells or platelet-rich plasma (PRP) to enhance healing, presents a promising area for growth. Evolving consumer preferences for less invasive and faster recovery procedures are also creating demand for advanced arthroscopic and endoscopic surgical instruments and techniques.

Growth Accelerators in the Pet Orthopedics Industry Industry

Several key catalysts are accelerating long-term growth in the Pet Orthopedics industry. Technological breakthroughs, particularly in biomaterials science and precision engineering, are leading to the development of more durable, biocompatible, and functional implants. Strategic partnerships between veterinary universities, research institutions, and medical device manufacturers are fostering collaborative innovation and speeding up the translation of research into practical clinical applications. Market expansion strategies, including educational initiatives for veterinarians and pet owners about the benefits of advanced orthopedic care, are crucial for driving adoption. The increasing investment by venture capital firms in veterinary technology startups further fuels the development of new products and services, contributing to sustained growth.

Key Players Shaping the Pet Orthopedics Industry Market

- GerMedUSA

- KYON PHARMA INC

- Johnson & Johnson

- EVEROST INC

- B Braun Melsungen AG

- BioMedtrix LLC

- Integra lifesciences

- Veterinary Orthopedic Implants

Notable Milestones in Pet Orthopedics Industry Sector

- 2019: Introduction of advanced ceramic-coated implants for enhanced biocompatibility and longevity.

- 2020: Increased adoption of 3D-printed patient-specific implants for complex fracture repairs.

- 2021: Development of new bioabsorbable fixation devices for soft tissue repair.

- 2022: Launch of robotic-assisted surgical systems specifically designed for veterinary orthopedic procedures.

- 2023: Significant advancements in regenerative therapies (e.g., advanced PRP formulations) integrated with orthopedic surgeries.

- 2024: Expansion of minimally invasive arthroscopic techniques for joint procedures, leading to quicker recovery times.

In-Depth Pet Orthopedics Industry Market Outlook

The Pet Orthopedics industry is poised for significant expansion, driven by persistent trends in pet humanization and a continuous influx of technological innovations. Growth accelerators such as the development of advanced biomaterials, the increasing integration of digital technologies like AI in surgical planning, and the expansion of specialized veterinary training programs will continue to fuel market potential. Strategic opportunities lie in addressing unmet needs in emerging markets, developing more cost-effective treatment options, and further advancing regenerative medicine applications. The focus on enhancing the quality of life for pets through sophisticated orthopedic solutions ensures a robust and promising future for this dynamic industry.

Pet Orthopedics Industry Segmentation

-

1. Type

- 1.1. Implants

- 1.2. Instruments

- 1.3. Screws

- 1.4. Others

-

2. Application

- 2.1. Total hip replacement

- 2.2. Total knee replacement

- 2.3. Total elbow replacement

- 2.4. Trauma fixation

- 2.5. Others

Pet Orthopedics Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Pet Orthopedics Industry Regional Market Share

Geographic Coverage of Pet Orthopedics Industry

Pet Orthopedics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Implants

- 5.1.2. Instruments

- 5.1.3. Screws

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Total hip replacement

- 5.2.2. Total knee replacement

- 5.2.3. Total elbow replacement

- 5.2.4. Trauma fixation

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Pet Orthopedics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Implants

- 6.1.2. Instruments

- 6.1.3. Screws

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Total hip replacement

- 6.2.2. Total knee replacement

- 6.2.3. Total elbow replacement

- 6.2.4. Trauma fixation

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Pet Orthopedics Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Implants

- 7.1.2. Instruments

- 7.1.3. Screws

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Total hip replacement

- 7.2.2. Total knee replacement

- 7.2.3. Total elbow replacement

- 7.2.4. Trauma fixation

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Pet Orthopedics Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Implants

- 8.1.2. Instruments

- 8.1.3. Screws

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Total hip replacement

- 8.2.2. Total knee replacement

- 8.2.3. Total elbow replacement

- 8.2.4. Trauma fixation

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Pet Orthopedics Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Implants

- 9.1.2. Instruments

- 9.1.3. Screws

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Total hip replacement

- 9.2.2. Total knee replacement

- 9.2.3. Total elbow replacement

- 9.2.4. Trauma fixation

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East and Africa Pet Orthopedics Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Implants

- 10.1.2. Instruments

- 10.1.3. Screws

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Total hip replacement

- 10.2.2. Total knee replacement

- 10.2.3. Total elbow replacement

- 10.2.4. Trauma fixation

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. South America Pet Orthopedics Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Implants

- 11.1.2. Instruments

- 11.1.3. Screws

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Total hip replacement

- 11.2.2. Total knee replacement

- 11.2.3. Total elbow replacement

- 11.2.4. Trauma fixation

- 11.2.5. Others

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 GerMedUSA

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 KYON PHARMA INC

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Johnson & Johnson*List Not Exhaustive

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 EVEROST INC

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 B Braun Melsungen AG

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 BioMedtrix LLC

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Integra lifesciences

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Veterinary Orthopedic Implants

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.1 GerMedUSA

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Pet Orthopedics Industry Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Pet Orthopedics Industry Revenue (undefined), by Type 2025 & 2033

- Figure 3: North America Pet Orthopedics Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Pet Orthopedics Industry Revenue (undefined), by Application 2025 & 2033

- Figure 5: North America Pet Orthopedics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Pet Orthopedics Industry Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Pet Orthopedics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Pet Orthopedics Industry Revenue (undefined), by Type 2025 & 2033

- Figure 9: Europe Pet Orthopedics Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: Europe Pet Orthopedics Industry Revenue (undefined), by Application 2025 & 2033

- Figure 11: Europe Pet Orthopedics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: Europe Pet Orthopedics Industry Revenue (undefined), by Country 2025 & 2033

- Figure 13: Europe Pet Orthopedics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Pet Orthopedics Industry Revenue (undefined), by Type 2025 & 2033

- Figure 15: Asia Pacific Pet Orthopedics Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Asia Pacific Pet Orthopedics Industry Revenue (undefined), by Application 2025 & 2033

- Figure 17: Asia Pacific Pet Orthopedics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 18: Asia Pacific Pet Orthopedics Industry Revenue (undefined), by Country 2025 & 2033

- Figure 19: Asia Pacific Pet Orthopedics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East and Africa Pet Orthopedics Industry Revenue (undefined), by Type 2025 & 2033

- Figure 21: Middle East and Africa Pet Orthopedics Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Middle East and Africa Pet Orthopedics Industry Revenue (undefined), by Application 2025 & 2033

- Figure 23: Middle East and Africa Pet Orthopedics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: Middle East and Africa Pet Orthopedics Industry Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East and Africa Pet Orthopedics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Pet Orthopedics Industry Revenue (undefined), by Type 2025 & 2033

- Figure 27: South America Pet Orthopedics Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: South America Pet Orthopedics Industry Revenue (undefined), by Application 2025 & 2033

- Figure 29: South America Pet Orthopedics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: South America Pet Orthopedics Industry Revenue (undefined), by Country 2025 & 2033

- Figure 31: South America Pet Orthopedics Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Pet Orthopedics Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 2: Global Pet Orthopedics Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 3: Global Pet Orthopedics Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Pet Orthopedics Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 5: Global Pet Orthopedics Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 6: Global Pet Orthopedics Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Pet Orthopedics Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 11: Global Pet Orthopedics Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 12: Global Pet Orthopedics Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Germany Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: France Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Italy Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 17: Spain Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 19: Global Pet Orthopedics Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 20: Global Pet Orthopedics Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 21: Global Pet Orthopedics Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 22: China Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Japan Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: India Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Australia Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: South Korea Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Pet Orthopedics Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 29: Global Pet Orthopedics Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 30: Global Pet Orthopedics Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: GCC Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: South Africa Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: Rest of Middle East and Africa Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: Global Pet Orthopedics Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 35: Global Pet Orthopedics Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 36: Global Pet Orthopedics Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 37: Brazil Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: Argentina Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 39: Rest of South America Pet Orthopedics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Pet Orthopedics Industry?

The projected CAGR is approximately 8.6%.

2. Which companies are prominent players in the Pet Orthopedics Industry?

Key companies in the market include GerMedUSA, KYON PHARMA INC, Johnson & Johnson*List Not Exhaustive, EVEROST INC, B Braun Melsungen AG, BioMedtrix LLC, Integra lifesciences, Veterinary Orthopedic Implants.

3. What are the main segments of the Pet Orthopedics Industry?

The market segments include Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

; Rising Number of Pet Owners & Veterinary Practitioners; Growing Number of Government Initiatives; Increasing Incidence of Obesity.

6. What are the notable trends driving market growth?

Implants segment in Veterinary Orthopedics market is Estimated to Witness a Healthy Growth in Future..

7. Are there any restraints impacting market growth?

; High Surgery and Pet Care Cost.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Pet Orthopedics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Pet Orthopedics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Pet Orthopedics Industry?

To stay informed about further developments, trends, and reports in the Pet Orthopedics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence