Key Insights

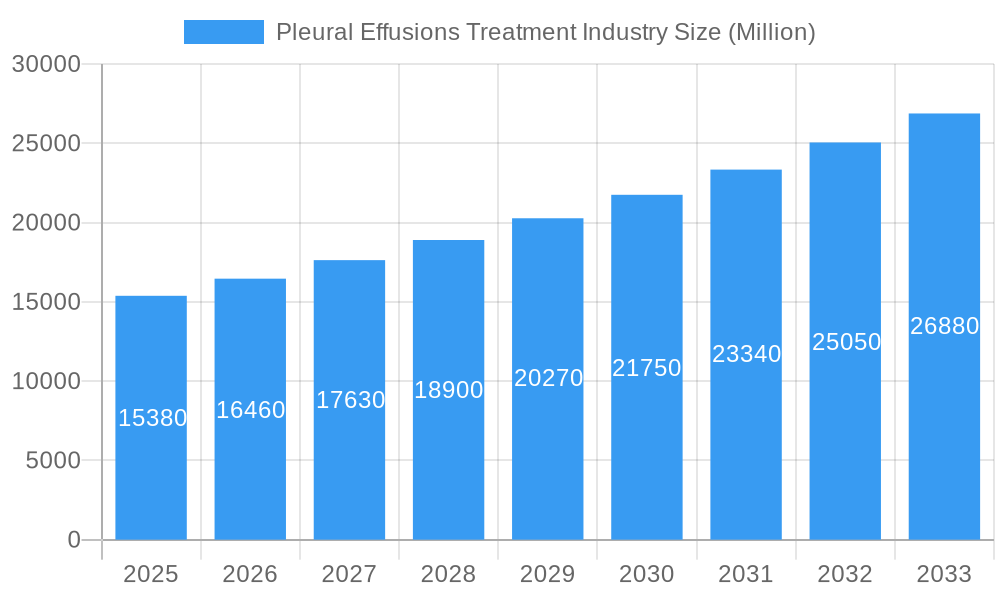

The Pleural Effusions Treatment Market is poised for robust expansion, projected to reach a significant USD 15.38 billion by 2025, demonstrating a compelling compound annual growth rate (CAGR) of 7.23% throughout the forecast period of 2025-2033. This growth is underpinned by several critical drivers, including the increasing prevalence of underlying conditions leading to pleural effusions, such as heart failure, pneumonia, and cancer. Advances in diagnostic technologies and minimally invasive treatment modalities are also playing a pivotal role in driving market adoption and improving patient outcomes. The market is segmented by disease type into Transudative and Exudative effusions, with Exudative effusions, often associated with more complex conditions like malignancy or infection, likely representing a larger share due to requiring more intensive treatment interventions. By end-user, hospitals are expected to dominate the market due to the severity of cases and the need for specialized equipment and personnel, followed by ambulatory clinics for less complex drainage procedures and follow-up care, and other end-users encompassing research institutions and home healthcare settings.

Pleural Effusions Treatment Industry Market Size (In Billion)

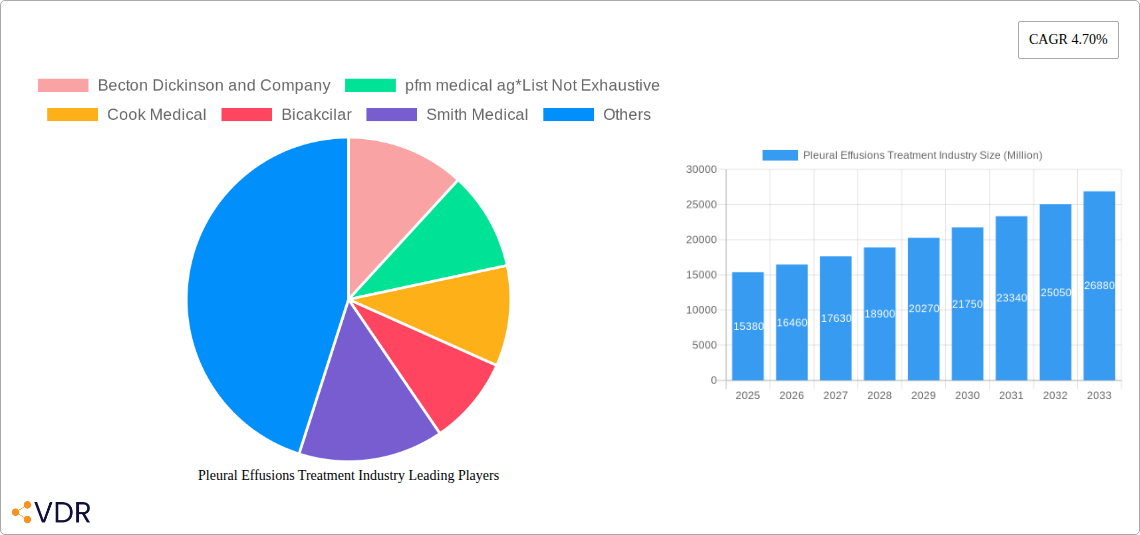

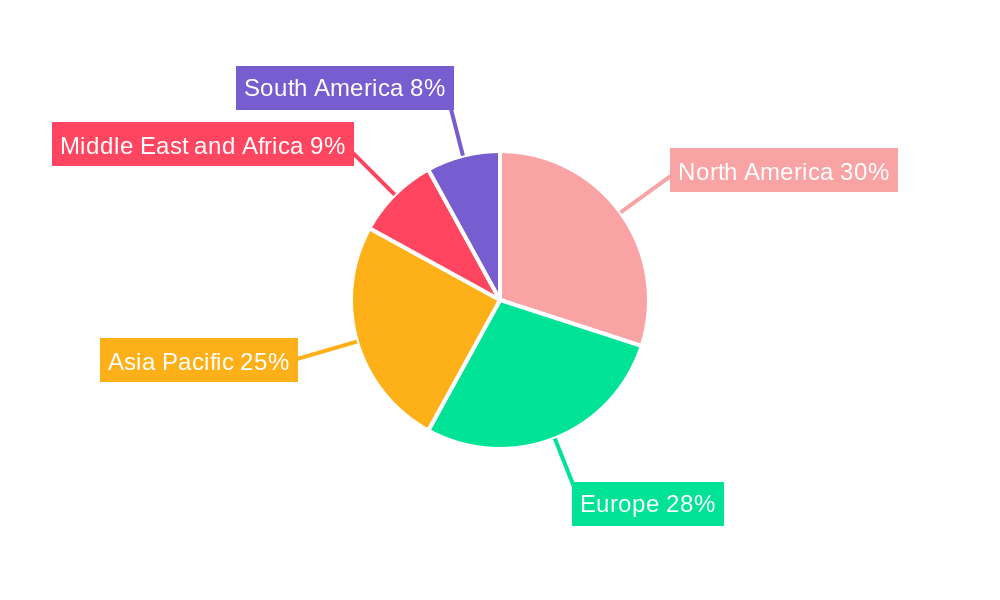

Emerging trends in the Pleural Effusions Treatment Market include the development of novel biomaterials for pleural space management, enhanced thoracentesis techniques, and the growing adoption of indwelling pleural catheters (IPCs) for managing recurrent effusions, offering patients improved quality of life and reduced hospitalizations. Personalized medicine approaches are also gaining traction, with treatments being tailored based on the underlying cause and characteristics of the effusion. However, the market faces certain restraints, such as the high cost of advanced treatment devices and procedures, reimbursement challenges in certain regions, and the need for skilled healthcare professionals to perform these interventions. Geographically, North America and Europe currently hold significant market shares due to advanced healthcare infrastructure and high disease prevalence. The Asia Pacific region is anticipated to witness the fastest growth, driven by increasing healthcare expenditure, a rising burden of chronic diseases, and expanding access to medical facilities. Key players such as Becton Dickinson and Company, Cook Medical, and B. Braun SE are actively involved in research and development, product innovation, and strategic collaborations to capitalize on the market's growth potential.

Pleural Effusions Treatment Industry Company Market Share

Comprehensive Report: Pleural Effusions Treatment Industry - Market Dynamics, Growth, and Future Outlook (2019-2033)

This in-depth report provides a strategic analysis of the global Pleural Effusions Treatment market, offering critical insights into its current landscape and future trajectory. Leveraging a robust study period from 2019 to 2033, with a base and estimated year of 2025, this report is essential for stakeholders seeking to understand market dynamics, growth trends, regional dominance, product innovations, key challenges, and emerging opportunities within this vital healthcare sector. We delve into the parent and child market structures, utilizing high-traffic keywords to maximize SEO visibility and engagement for industry professionals.

Pleural Effusions Treatment Industry Market Dynamics & Structure

The Pleural Effusions Treatment market is characterized by a moderate to high level of concentration, with key players investing heavily in research and development to introduce novel therapeutic approaches. Technological innovation, particularly in minimally invasive diagnostic and drainage techniques, is a significant driver. Regulatory frameworks, primarily driven by patient safety and efficacy standards from bodies like the FDA and EMA, influence product development and market entry. Competitive product substitutes include traditional thoracentesis, indwelling pleural catheters, and advanced pharmacological interventions. End-user demographics are predominantly influenced by the increasing prevalence of underlying conditions such as heart failure, pneumonia, and cancers that lead to pleural effusions. Mergers and acquisitions (M&A) trends are observed, as larger companies seek to expand their portfolios and gain access to innovative technologies and patient populations. Barriers to innovation include the lengthy and costly clinical trial processes, stringent regulatory approvals, and the need for specialized medical infrastructure.

- Market Concentration: Dominated by a mix of large medical device manufacturers and specialized pharmaceutical companies.

- Technological Innovation Drivers: Advancements in imaging guidance for procedures, development of more effective sclerosing agents, and targeted drug therapies for underlying causes.

- Regulatory Frameworks: Strict compliance with global health authorities for device safety and drug efficacy.

- Competitive Product Substitutes: Shifting towards less invasive and more effective treatment modalities.

- End-User Demographics: Ageing populations and rising incidence of chronic diseases are key influencers.

- M&A Trends: Strategic acquisitions to enhance product pipelines and market reach.

Pleural Effusions Treatment Industry Growth Trends & Insights

The Pleural Effusions Treatment market is poised for robust growth, projected to expand significantly from its 2025 valuation of approximately \$X.XX billion. This growth is fueled by an increasing global incidence of cardiovascular diseases, respiratory infections, and a rising cancer burden, all of which contribute to the development of pleural effusions. Adoption rates for advanced diagnostic and therapeutic devices are escalating, driven by their superior efficacy, reduced invasiveness, and improved patient outcomes compared to traditional methods. Technological disruptions, such as the development of bio-absorbable materials for chest tube drainage and novel drug delivery systems, are reshaping treatment paradigms. Consumer behavior is shifting towards seeking minimally invasive procedures with faster recovery times, further propelling the demand for innovative pleural effusion management solutions. The market penetration of advanced pleural effusion treatments is expected to deepen as healthcare providers become more aware of and invest in these technologies.

- Market Size Evolution: Projected to reach \$Y.YY billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of Z.ZZ% during the forecast period.

- Adoption Rates: Increasing adoption of minimally invasive techniques and advanced catheter systems.

- Technological Disruptions: Innovations in drug delivery, biomaterials, and diagnostic imaging are transforming treatment protocols.

- Consumer Behavior Shifts: Growing patient preference for less invasive procedures and quicker recovery periods.

Dominant Regions, Countries, or Segments in Pleural Effusions Treatment Industry

North America currently stands as the dominant region in the Pleural Effusions Treatment market, driven by a confluence of advanced healthcare infrastructure, high disposable incomes, and a substantial patient population suffering from underlying conditions like heart failure and lung cancer. The United States, in particular, contributes significantly due to extensive research and development activities, early adoption of innovative medical technologies, and a well-established reimbursement framework for medical procedures. The Exudative segment within the Disease Type classification is a primary growth engine, owing to its stronger association with malignant causes and inflammatory conditions requiring more intensive treatment. Within the End User segment, Hospitals represent the largest market share, acting as primary centers for diagnosis and complex treatment interventions. Ambulatory Clinics are also witnessing steady growth, especially for less complex procedures and follow-up care.

- Leading Region: North America, with the United States as a key contributor.

- Dominant Disease Type Segment: Exudative pleural effusions, due to their link to serious underlying pathologies.

- Key End User Segment: Hospitals, owing to their comprehensive treatment capabilities.

- Drivers of Dominance in North America:

- Advanced healthcare infrastructure and technology adoption.

- High prevalence of chronic diseases leading to pleural effusions.

- Robust reimbursement policies supporting advanced treatments.

- Active clinical research and development initiatives.

- Market Share within Segments:

- Exudative: Expected to account for approximately 60% of the market by 2025.

- Hospitals: Projected to hold over 70% of the end-user market share.

Pleural Effusions Treatment Industry Product Landscape

The product landscape for Pleural Effusions Treatment is diverse, encompassing a range of diagnostic tools, drainage devices, and therapeutic agents. Key innovations include advanced imaging technologies for precise effusion localization, minimally invasive drainage systems like tunneled pleural catheters that offer improved patient mobility and reduced infection risk, and novel sclerosing agents designed for enhanced efficacy and reduced toxicity. Performance metrics are increasingly focused on procedure success rates, patient comfort, complication reduction, and the duration of effusion recurrence. Unique selling propositions often revolve around ease of use for clinicians, improved patient quality of life, and cost-effectiveness in managing chronic effusions. Technological advancements are continuously driving the development of smarter, more targeted, and patient-centric treatment solutions.

Key Drivers, Barriers & Challenges in Pleural Effusions Treatment Industry

Key Drivers:

- Rising Prevalence of Underlying Diseases: Increasing incidence of heart failure, pneumonia, and malignancies directly correlates with higher rates of pleural effusions.

- Technological Advancements: Development of minimally invasive devices and improved diagnostic tools enhance treatment efficacy and patient comfort.

- Growing Geriatric Population: Older adults are more susceptible to conditions causing pleural effusions, driving demand for treatment.

- Increased Healthcare Expenditure: Growing investments in healthcare globally support the adoption of advanced treatments.

Key Barriers & Challenges:

- High Cost of Advanced Treatments: Innovative devices and therapies can be expensive, posing a barrier to widespread adoption, particularly in resource-limited settings.

- Regulatory Hurdles: Stringent approval processes for new medical devices and pharmaceuticals can delay market entry.

- Limited Awareness and Access: In some regions, awareness about advanced treatment options and access to specialized care remains a challenge.

- Reimbursement Policies: Inconsistent or inadequate reimbursement for novel procedures can hinder market growth.

- Supply Chain Disruptions: Global supply chain complexities can impact the availability of critical components and finished products.

Emerging Opportunities in Pleural Effusions Treatment Industry

Emerging opportunities in the Pleural Effusions Treatment industry lie in the development of advanced pharmacological interventions targeting the inflammatory pathways involved in effusion formation, especially for malignant pleural effusions. The growing demand for home-based care solutions presents an opportunity for innovative, patient-friendly indwelling pleural catheter systems with improved infection control and ease of management. Furthermore, the exploration of targeted therapies for specific etiologies of pleural effusions, such as rare autoimmune diseases or occupational lung diseases, represents an untapped market. Advancements in personalized medicine, utilizing genetic profiling to predict effusion risk or tailor treatment responses, also offer significant future potential. The increasing focus on palliative care also opens avenues for devices and treatments that improve patient comfort and quality of life.

Growth Accelerators in the Pleural Effusions Treatment Industry Industry

Several key growth accelerators are poised to propel the Pleural Effusions Treatment industry forward. Significant investment in research and development by leading companies is continuously leading to the introduction of more effective and less invasive treatment modalities. Strategic partnerships between medical device manufacturers, pharmaceutical companies, and healthcare providers are facilitating broader market access and technology integration. The increasing emphasis on value-based healthcare is also a catalyst, as providers seek treatments that not only improve patient outcomes but also reduce overall healthcare costs through fewer hospital readmissions and complications. Furthermore, the expanding reach of telehealth and remote patient monitoring technologies offers opportunities for improved follow-up care and early intervention, thus accelerating growth.

Key Players Shaping the Pleural Effusions Treatment Industry Market

- Becton Dickinson and Company

- pfm medical ag

- Cook Medical

- Bicakcilar

- Smith Medical

- Grena

- Lung Therapeutics Inc

- Redax

- Taiho Pharmaceutical Co Ltd

- Biometrix

- Rocket Medical

- B Braun SE

Notable Milestones in Pleural Effusions Treatment Industry Sector

- April 2022: The study titled 'IFN-γ Combined With T Cells in the Treatment of Refractory Malignant Pleural Effusion and Ascites' was registered in ClinicalTrials.gov for Malignant Pleural Effusion, indicating advancements in immunotherapy for complex cases.

- September 2021: Bristol Mayer Squibb declared three-year data from the CheckMate -743 trial. As per the clinical trial data, serious adverse reactions occurred in 54% of patients receiving OPDIVO plus YERVOY. The most frequent serious adverse reactions reported in 2% of patients were pneumonia, pyrexia, diarrhea, pneumonitis, pleural effusion, dyspnea, acute kidney injury, infusion-related reaction, musculoskeletal pain, and pulmonary embolism, highlighting the evolving understanding of treatment side effects and the need for careful patient management in related conditions.

In-Depth Pleural Effusions Treatment Industry Market Outlook

The future outlook for the Pleural Effusions Treatment market is exceptionally promising, driven by persistent growth accelerators. The continuous innovation pipeline, fueled by substantial R&D investments, promises novel therapeutic agents and advanced diagnostic tools. Strategic alliances are expected to expand market reach and foster collaborative advancements. The paradigm shift towards value-based healthcare will further incentivize the adoption of cost-effective and outcome-improving treatments. Moreover, the integration of digital health solutions, including remote monitoring and AI-driven diagnostics, will enhance patient care accessibility and efficiency. The market is expected to witness significant growth in emerging economies as healthcare infrastructure improves and awareness of advanced treatment options increases, creating substantial untapped potential and robust future market expansion opportunities.

Pleural Effusions Treatment Industry Segmentation

-

1. Disease Type

- 1.1. Transudative

- 1.2. Exudative

-

2. End User

- 2.1. Hospitals

- 2.2. Ambulatory Clinics

- 2.3. Other End Users

Pleural Effusions Treatment Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Pleural Effusions Treatment Industry Regional Market Share

Geographic Coverage of Pleural Effusions Treatment Industry

Pleural Effusions Treatment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Disease Type

- 5.1.1. Transudative

- 5.1.2. Exudative

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Hospitals

- 5.2.2. Ambulatory Clinics

- 5.2.3. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Disease Type

- 6. Global Pleural Effusions Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Disease Type

- 6.1.1. Transudative

- 6.1.2. Exudative

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Hospitals

- 6.2.2. Ambulatory Clinics

- 6.2.3. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Disease Type

- 7. North America Pleural Effusions Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Disease Type

- 7.1.1. Transudative

- 7.1.2. Exudative

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Hospitals

- 7.2.2. Ambulatory Clinics

- 7.2.3. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Disease Type

- 8. Europe Pleural Effusions Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Disease Type

- 8.1.1. Transudative

- 8.1.2. Exudative

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Hospitals

- 8.2.2. Ambulatory Clinics

- 8.2.3. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Disease Type

- 9. Asia Pacific Pleural Effusions Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Disease Type

- 9.1.1. Transudative

- 9.1.2. Exudative

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Hospitals

- 9.2.2. Ambulatory Clinics

- 9.2.3. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Disease Type

- 10. Middle East and Africa Pleural Effusions Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Disease Type

- 10.1.1. Transudative

- 10.1.2. Exudative

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Hospitals

- 10.2.2. Ambulatory Clinics

- 10.2.3. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Disease Type

- 11. South America Pleural Effusions Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Disease Type

- 11.1.1. Transudative

- 11.1.2. Exudative

- 11.2. Market Analysis, Insights and Forecast - by End User

- 11.2.1. Hospitals

- 11.2.2. Ambulatory Clinics

- 11.2.3. Other End Users

- 11.1. Market Analysis, Insights and Forecast - by Disease Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Becton Dickinson and Company

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 pfm medical ag*List Not Exhaustive

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Cook Medical

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Bicakcilar

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Smith Medical

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Grena

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Lung Therapeutics Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Redax

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Taiho Pharmaceutical Co Ltd

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Biometrix

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Rocket Medical

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 B Braun SE

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Becton Dickinson and Company

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Pleural Effusions Treatment Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Pleural Effusions Treatment Industry Revenue (billion), by Disease Type 2025 & 2033

- Figure 3: North America Pleural Effusions Treatment Industry Revenue Share (%), by Disease Type 2025 & 2033

- Figure 4: North America Pleural Effusions Treatment Industry Revenue (billion), by End User 2025 & 2033

- Figure 5: North America Pleural Effusions Treatment Industry Revenue Share (%), by End User 2025 & 2033

- Figure 6: North America Pleural Effusions Treatment Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Pleural Effusions Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Pleural Effusions Treatment Industry Revenue (billion), by Disease Type 2025 & 2033

- Figure 9: Europe Pleural Effusions Treatment Industry Revenue Share (%), by Disease Type 2025 & 2033

- Figure 10: Europe Pleural Effusions Treatment Industry Revenue (billion), by End User 2025 & 2033

- Figure 11: Europe Pleural Effusions Treatment Industry Revenue Share (%), by End User 2025 & 2033

- Figure 12: Europe Pleural Effusions Treatment Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Pleural Effusions Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Pleural Effusions Treatment Industry Revenue (billion), by Disease Type 2025 & 2033

- Figure 15: Asia Pacific Pleural Effusions Treatment Industry Revenue Share (%), by Disease Type 2025 & 2033

- Figure 16: Asia Pacific Pleural Effusions Treatment Industry Revenue (billion), by End User 2025 & 2033

- Figure 17: Asia Pacific Pleural Effusions Treatment Industry Revenue Share (%), by End User 2025 & 2033

- Figure 18: Asia Pacific Pleural Effusions Treatment Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Pleural Effusions Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East and Africa Pleural Effusions Treatment Industry Revenue (billion), by Disease Type 2025 & 2033

- Figure 21: Middle East and Africa Pleural Effusions Treatment Industry Revenue Share (%), by Disease Type 2025 & 2033

- Figure 22: Middle East and Africa Pleural Effusions Treatment Industry Revenue (billion), by End User 2025 & 2033

- Figure 23: Middle East and Africa Pleural Effusions Treatment Industry Revenue Share (%), by End User 2025 & 2033

- Figure 24: Middle East and Africa Pleural Effusions Treatment Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East and Africa Pleural Effusions Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Pleural Effusions Treatment Industry Revenue (billion), by Disease Type 2025 & 2033

- Figure 27: South America Pleural Effusions Treatment Industry Revenue Share (%), by Disease Type 2025 & 2033

- Figure 28: South America Pleural Effusions Treatment Industry Revenue (billion), by End User 2025 & 2033

- Figure 29: South America Pleural Effusions Treatment Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: South America Pleural Effusions Treatment Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: South America Pleural Effusions Treatment Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Pleural Effusions Treatment Industry Revenue billion Forecast, by Disease Type 2020 & 2033

- Table 2: Global Pleural Effusions Treatment Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 3: Global Pleural Effusions Treatment Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Pleural Effusions Treatment Industry Revenue billion Forecast, by Disease Type 2020 & 2033

- Table 5: Global Pleural Effusions Treatment Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 6: Global Pleural Effusions Treatment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Pleural Effusions Treatment Industry Revenue billion Forecast, by Disease Type 2020 & 2033

- Table 11: Global Pleural Effusions Treatment Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 12: Global Pleural Effusions Treatment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Germany Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: France Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Italy Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Spain Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Global Pleural Effusions Treatment Industry Revenue billion Forecast, by Disease Type 2020 & 2033

- Table 20: Global Pleural Effusions Treatment Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 21: Global Pleural Effusions Treatment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 22: China Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Japan Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: India Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Australia Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: South Korea Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Pleural Effusions Treatment Industry Revenue billion Forecast, by Disease Type 2020 & 2033

- Table 29: Global Pleural Effusions Treatment Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 30: Global Pleural Effusions Treatment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 31: GCC Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: South Africa Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Rest of Middle East and Africa Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Global Pleural Effusions Treatment Industry Revenue billion Forecast, by Disease Type 2020 & 2033

- Table 35: Global Pleural Effusions Treatment Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 36: Global Pleural Effusions Treatment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 37: Brazil Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Argentina Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Rest of South America Pleural Effusions Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Pleural Effusions Treatment Industry?

The projected CAGR is approximately 6%.

2. Which companies are prominent players in the Pleural Effusions Treatment Industry?

Key companies in the market include Becton Dickinson and Company, pfm medical ag*List Not Exhaustive, Cook Medical, Bicakcilar, Smith Medical, Grena, Lung Therapeutics Inc, Redax, Taiho Pharmaceutical Co Ltd, Biometrix, Rocket Medical, B Braun SE.

3. What are the main segments of the Pleural Effusions Treatment Industry?

The market segments include Disease Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.1 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Prevalence of Pleural Effusions; Significant Progress in the Management of Pleural Effusions.

6. What are the notable trends driving market growth?

Transudative Pleural Effusions Segment Shows Lucrative Opportunity in the Pleural Effusions Treatment Market.

7. Are there any restraints impacting market growth?

Partial Success Rate of Treatment.

8. Can you provide examples of recent developments in the market?

In April 2022, the study titled 'IFN-γ Combined With T Cells in the Treatment of Refractory Malignant Pleural Effusion and Ascites' was registered in ClinicalTrials.gov for Malignant Pleural Effusion.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Pleural Effusions Treatment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Pleural Effusions Treatment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Pleural Effusions Treatment Industry?

To stay informed about further developments, trends, and reports in the Pleural Effusions Treatment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence