Key Insights

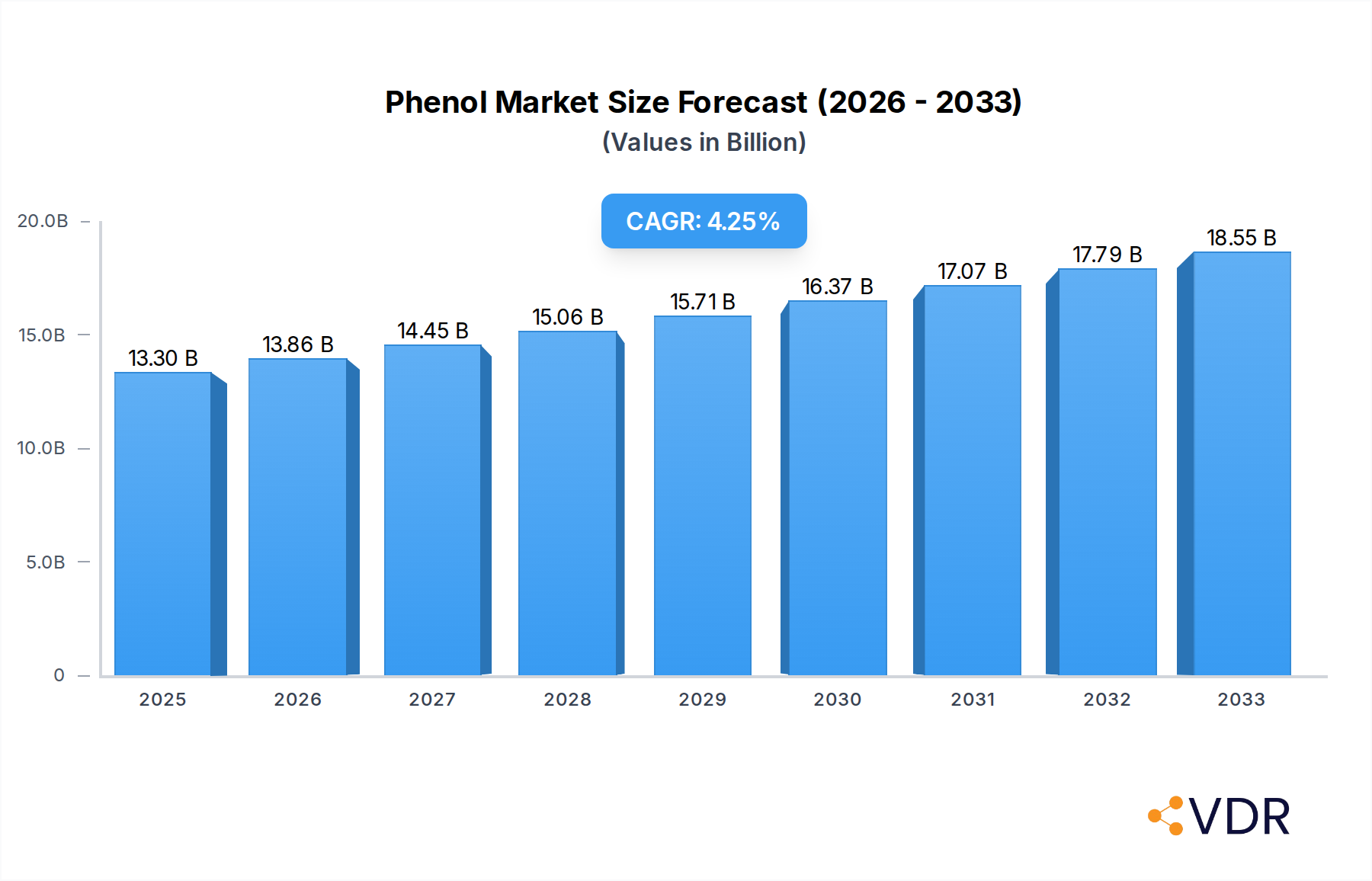

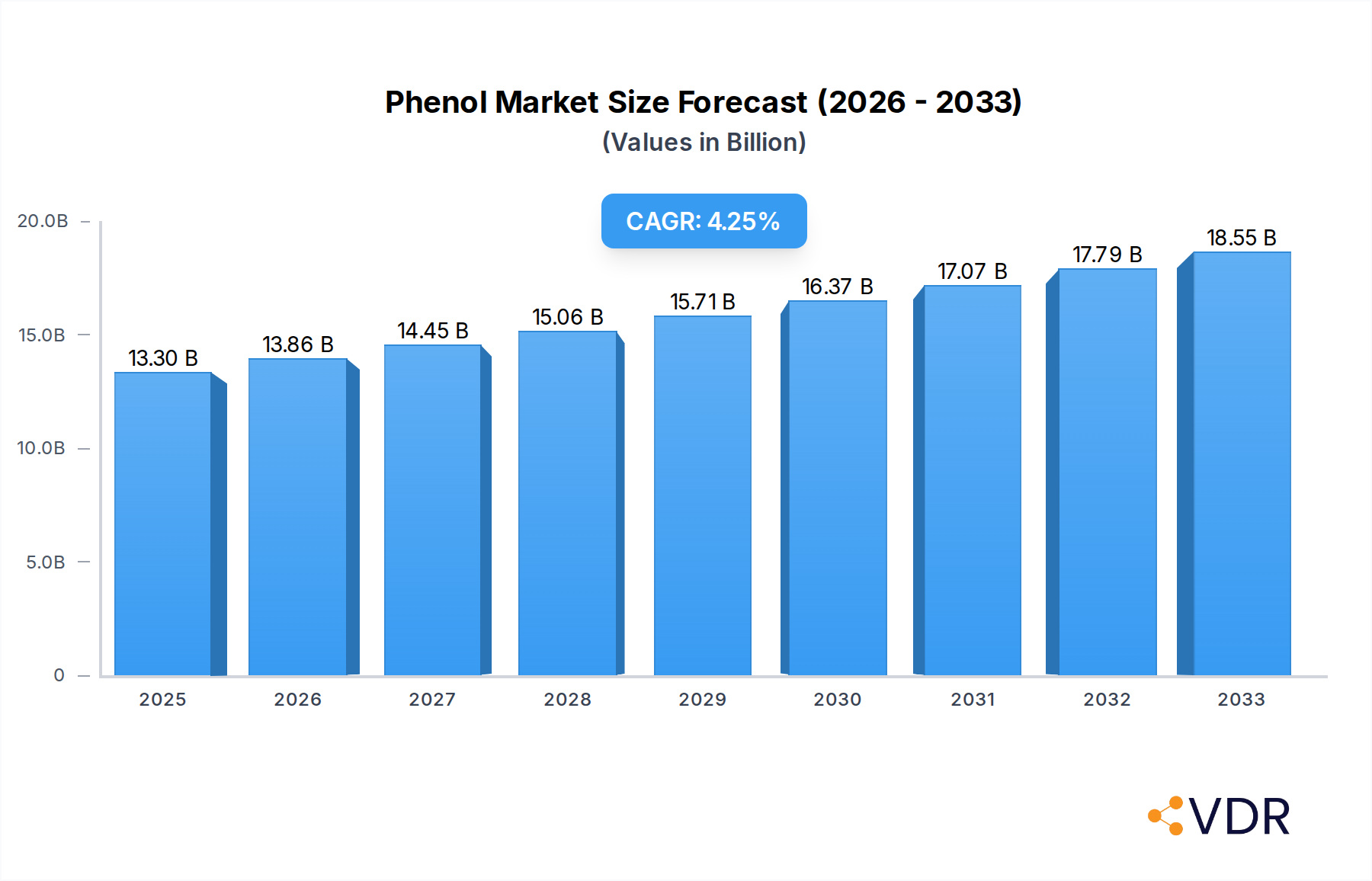

The global Phenol market is poised for significant expansion, projected to reach a substantial $13.3 billion in 2025, exhibiting a robust Compound Annual Growth Rate (CAGR) of 4.3% through the forecast period ending in 2033. This growth is underpinned by strong demand from key end-use industries, particularly the production of polycarbonates, phenolic resins, and bisphenol-A (BPA), which are integral to sectors like automotive, construction, electronics, and consumer goods. Emerging economies, especially in the Asia Pacific region, are expected to be major contributors to this growth, driven by increasing industrialization, urbanization, and a rising middle class. The development of innovative applications for phenol derivatives, coupled with advancements in production technologies leading to greater efficiency and sustainability, will further fuel market expansion.

Phenol Market Market Size (In Billion)

While the market benefits from strong fundamental drivers, certain restraints need to be addressed. Fluctuations in the price of key raw materials, such as benzene and propylene, can impact profit margins for manufacturers. Stringent environmental regulations concerning the production and disposal of phenol and its derivatives, though promoting sustainable practices, can also add to operational costs. However, the inherent versatility of phenol and its widespread applications across numerous industries, coupled with ongoing research and development efforts to create bio-based alternatives and enhance recycling processes, are expected to outweigh these challenges. The market is segmented into Phenolic Resins, Caprolactum, Bisphenol-A, and Other Product Types, with Bisphenol-A and Phenolic Resins expected to command significant market shares due to their extensive use in durable goods and construction materials, respectively.

Phenol Market Company Market Share

Unlock critical insights into the global Phenol market, a vital chemical building block with diverse applications. This in-depth report provides an exhaustive analysis of market dynamics, growth trends, regional dominance, product landscape, and strategic opportunities. Discover the key drivers, barriers, and challenges shaping the phenol industry, alongside the influential players and notable milestones. With a comprehensive forecast period of 2019–2033, based on a 2025 base and estimated year, this report is an indispensable resource for stakeholders seeking to navigate and capitalize on the evolving chemical market.

Phenol Market Market Dynamics & Structure

The global Phenol market is characterized by a moderate to high market concentration, with a few key players dominating production and innovation. Technological advancements, particularly in process efficiency and sustainability, are significant technological innovation drivers, pushing for reduced environmental impact and enhanced product purity. Stringent regulatory frameworks concerning chemical production, handling, and emissions across major economies play a crucial role in shaping market entry and operational strategies. The presence of competitive product substitutes, while limited for core phenol applications, influences pricing and innovation efforts in related derivative markets. End-user demographics are diverse, spanning construction, automotive, electronics, pharmaceuticals, and consumer goods, each with distinct demand patterns and quality requirements. Mergers and acquisitions (M&A) trends are notable, driven by the pursuit of vertical integration, capacity expansion, and enhanced market presence. For instance, the acquisition of Mitsui Phenols Singapore Ltd by INEOS Phenol in August 2022, valued at USD 330 million, significantly boosted INEOS's production capacity and integration opportunities, demonstrating a clear M&A trend towards consolidation and strategic asset acquisition. Barriers to innovation often stem from high capital investment requirements for new production facilities and the complex regulatory approval processes for novel chemical formulations.

- Market Concentration: Dominated by a handful of global chemical giants, leading to strategic competitive dynamics.

- Innovation Drivers: Focus on sustainable production methods, higher purity grades, and development of novel phenol derivatives.

- Regulatory Landscape: Stringent environmental and safety regulations in North America, Europe, and Asia-Pacific significantly influence operational costs and market access.

- Competitive Substitutes: Limited direct substitutes for phenol's primary uses, but alternative materials in end-user industries can impact overall demand.

- End-User Demographics: Growth in construction, automotive manufacturing, and the electronics sector are key demand influencers.

- M&A Activity: Strategic acquisitions aimed at increasing market share, expanding production capacity, and securing raw material supply chains.

Phenol Market Growth Trends & Insights

The Phenol market is projected to experience robust growth driven by escalating demand from its diverse end-use industries and continuous innovation in its applications. The market size, estimated at USD XX billion in 2025, is anticipated to expand at a Compound Annual Growth Rate (CAGR) of X.XX% over the forecast period from 2025 to 2033, reaching an estimated USD XX billion by 2033. This upward trajectory is underpinned by the increasing adoption of phenolic resins in the construction sector for insulation materials, laminates, and adhesives, fueled by global urbanization and infrastructure development. Similarly, the automotive industry's demand for lightweight, durable components made from composites and plastics derived from Bisphenol-A (BPA) is a significant growth driver. The burgeoning electronics sector, requiring high-performance materials for circuit boards and casings, further propels the demand for phenol derivatives.

Technological disruptions are primarily focused on enhancing production sustainability and developing novel applications. The introduction of bio-based phenol production methods and the increased use of recycled feedstocks, as exemplified by Cepsa's NextPhenol launch, are gaining traction, aligning with global sustainability mandates. Consumer behavior shifts towards eco-friendly products are indirectly influencing the phenol market by encouraging innovation in sustainable manufacturing processes and end-products. Market penetration of phenol-based materials in emerging economies is expected to rise, driven by industrialization and increasing disposable incomes. The development of advanced phenolic composites and higher-performance BPA grades for specialized applications will also contribute to market expansion. The parent market for phenol, broadly encompassing petrochemical derivatives, provides a strong foundation for its growth, while the child markets, such as phenolic resins and Bisphenol-A, exhibit specific growth dynamics influenced by their unique application landscapes.

Dominant Regions, Countries, or Segments in Phenol Market

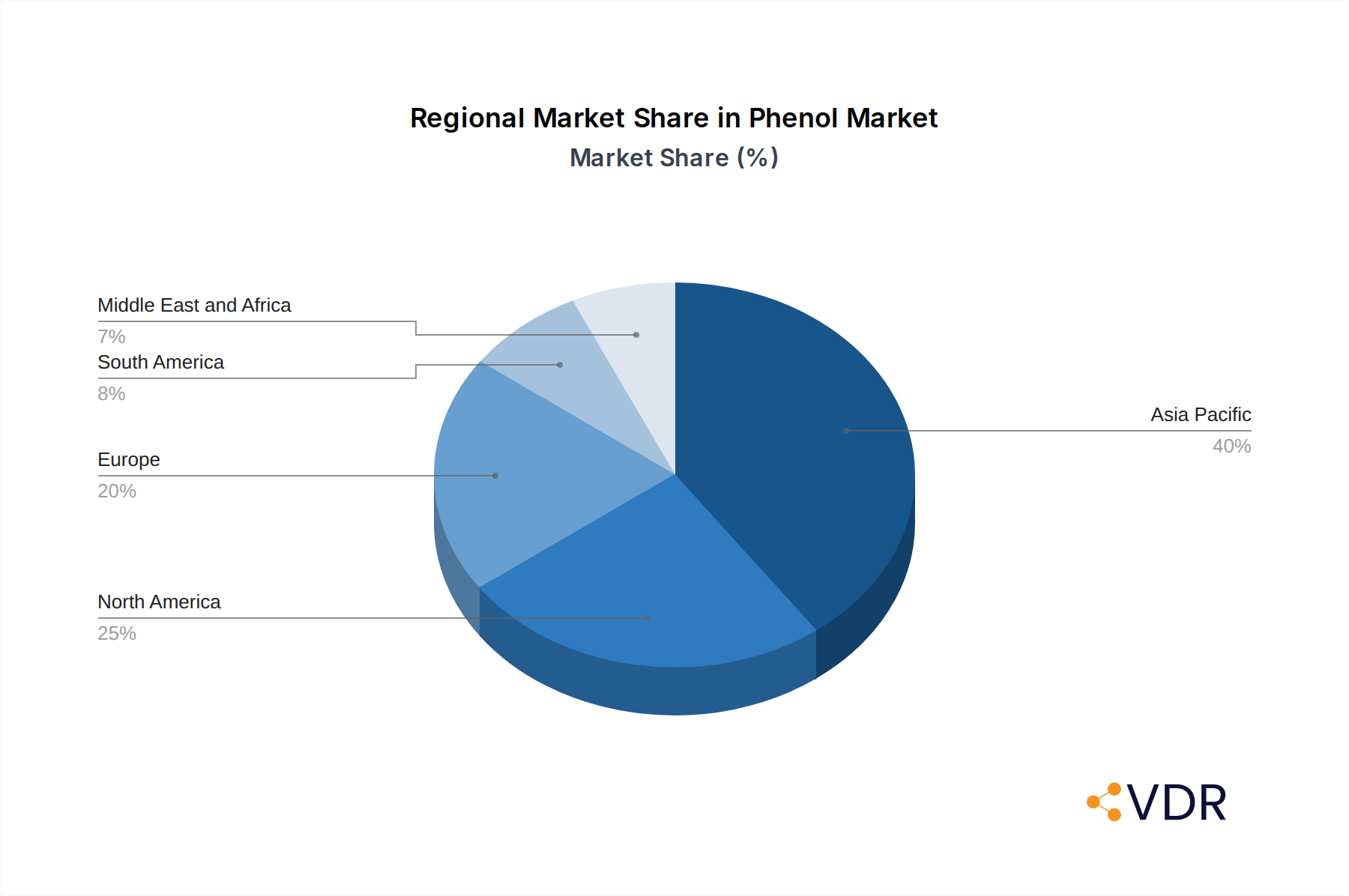

The Phenol market witnesses significant regional variations in demand, production capacity, and growth potential. Asia Pacific, particularly China, consistently emerges as the dominant region, accounting for over XX% of the global market share in 2025. This dominance is attributed to its robust manufacturing base across key end-user industries such as construction, automotive, electronics, and consumer goods, coupled with substantial investments in petrochemical infrastructure. China's rapid industrialization, coupled with supportive government policies aimed at promoting domestic chemical production, further solidifies its leading position.

Within the product segments, Bisphenol-A (BPA) is a significant growth driver, driven by its extensive use in the production of polycarbonate plastics and epoxy resins. Polycarbonate finds widespread application in automotive components, consumer electronics, optical media, and building materials. The increasing demand for lightweight and impact-resistant materials in these sectors directly translates into a higher demand for BPA. Phenolic resins also hold a substantial market share, owing to their excellent thermal stability, flame retardancy, and adhesive properties, making them indispensable in laminates, coatings, insulation, and automotive parts.

Key drivers of dominance in the Asia Pacific region include:

- Economic Policies: Favorable industrial policies, including tax incentives and special economic zones, attracting significant foreign and domestic investment in chemical manufacturing.

- Infrastructure Development: Extensive investments in ports, logistics networks, and industrial parks facilitate efficient production and distribution of phenol and its derivatives.

- Growing End-User Industries: Rapid expansion of automotive manufacturing, construction projects, and the consumer electronics sector, particularly in China, India, and Southeast Asian nations.

- Cost Competitiveness: Relatively lower labor and operational costs compared to Western economies, making it an attractive hub for chemical production.

- Capacity Expansion: Continuous investment in new phenol and BPA production facilities by major chemical players to cater to the burgeoning regional demand.

The child market for Bisphenol-A, in particular, is experiencing accelerated growth within the Asia Pacific region, directly impacting the overall Phenol market outlook. This segment is expected to continue its expansion, driven by advancements in polymer technology and evolving product requirements in critical industries.

Phenol Market Product Landscape

The Phenol market's product landscape is defined by continuous innovation and evolving applications across its key derivatives. Phenolic resins, known for their exceptional heat resistance, mechanical strength, and chemical inertness, are finding expanded use in high-performance composites for aerospace, automotive, and industrial applications. Caprolactam, a crucial precursor for Nylon 6, is witnessing steady demand from the textile and engineering plastics industries. Bisphenol-A (BPA) remains a cornerstone of the market, with ongoing research focusing on enhancing its purity and exploring novel applications in advanced polymers, such as flame-retardant materials and specialized coatings. Beyond these primary products, "Other Product Types" encompass a range of niche phenol derivatives utilized in pharmaceuticals, agrochemicals, and dyestuffs, each contributing to the market's diversification. Technological advancements are focused on improving production efficiency, reducing environmental impact, and developing higher-value specialty chemicals derived from phenol.

Key Drivers, Barriers & Challenges in Phenol Market

Key Drivers:

The Phenol market is propelled by several significant factors. The robust growth in construction, automotive manufacturing, and electronics sectors globally directly fuels demand for phenol and its derivatives, particularly Bisphenol-A and phenolic resins. Increasing urbanization and infrastructure development projects worldwide are creating a sustained demand for construction materials, adhesives, and coatings, all of which rely on phenol-based products. Technological advancements in polymer science are leading to the development of higher-performance materials derived from phenol, expanding their applicability into more demanding sectors. Furthermore, the growing focus on sustainability is driving innovation in bio-based phenol production and the utilization of recycled feedstocks, presenting new growth avenues.

Barriers & Challenges:

Despite the positive growth outlook, the Phenol market faces several challenges. Fluctuations in the price and availability of key raw materials, such as benzene and propylene, can significantly impact production costs and profit margins. Stringent environmental regulations concerning chemical manufacturing processes, emissions, and waste disposal add to operational expenses and necessitate continuous investment in compliance technologies. The global supply chain disruptions, as witnessed in recent years, can affect the timely delivery of raw materials and finished products, leading to production delays and increased logistics costs. Competition from alternative materials in certain end-use applications, although limited, can exert downward pressure on prices. Moreover, public perception and regulatory scrutiny surrounding Bisphenol-A (BPA) due to potential health concerns, while largely addressed by industry advancements and regulatory bodies, continue to be a consideration for certain applications.

Emerging Opportunities in Phenol Market

Emerging opportunities in the Phenol market lie in the burgeoning demand for sustainable and bio-based chemical solutions. The development and commercialization of phenol produced from renewable feedstocks, such as lignocellulosic biomass, present a significant untapped market. Growing consumer preference for eco-friendly products across various industries, including packaging, automotive, and construction, is creating a strong pull for sustainable chemicals. Furthermore, the increasing focus on lightweighting in the automotive and aerospace sectors is driving the demand for advanced composites made from phenolic resins, offering opportunities for specialized product development. The growing pharmaceutical industry's need for high-purity phenol derivatives for drug synthesis also represents a niche but expanding market. Innovative applications in areas like advanced coatings, adhesives for electronics, and functional materials for renewable energy technologies are also poised to drive future growth.

Growth Accelerators in the Phenol Market Industry

Several key accelerators are driving long-term growth in the Phenol market industry. Continuous advancements in catalyst technology and process engineering are leading to more efficient and cost-effective phenol production, improving competitiveness. Strategic partnerships and collaborations between chemical manufacturers and end-user industries are fostering innovation and tailor-made product development, ensuring that phenol derivatives meet evolving market needs. The increasing investment in research and development for bio-based phenol and circular economy initiatives are paving the way for a more sustainable future for the industry. Market expansion strategies, including the establishment of new production facilities in high-growth regions and the acquisition of complementary businesses, are crucial for capturing market share and achieving economies of scale. The growing adoption of advanced manufacturing techniques and digitalization within the chemical sector will further enhance operational efficiency and agility.

Key Players Shaping the Phenol Market Market

- Shell PLC

- Solvay

- AdvanSix Inc

- Mitsui Chemicals Inc

- Mitsubishi Chemical Corporation

- Cepsa

- Altivia

- Domo Chemical GmbH

- PTT Phenol Company Limited

- Formosa Chemicals & Fibre Corp

- INEOS Capital Limited

- Kumho P&B Chemicals Inc

Notable Milestones in Phenol Market Sector

- August 2022: INEOS Phenol announced the acquisition of the asset base of Mitsui Phenols Singapore Ltd from Mitsui Chemicals for a total consideration of USD 330 million. The addition of the Jurong phenol and BPA assets will provide integration opportunities with manufacturing sites in Germany, Belgium, and the United States. The acquisition will increase the total production capacity by 1 million tonnes.

- April 2022: Cepsa launched the new line of sustainable chemical NextPhenol, which is produced from the recycled feedstock. The launch of the new product range is a part of Cepsa's ambition to make its business activities fossil-free.

In-Depth Phenol Market Market Outlook

The Phenol market is poised for sustained growth, driven by a confluence of factors including robust demand from burgeoning end-user industries and a strong emphasis on sustainable chemical production. The strategic initiatives by key players, such as capacity expansions and acquisitions, are strengthening market dynamics and ensuring supply chain resilience. Emerging opportunities in bio-based phenol and circular economy solutions present significant avenues for innovation and market differentiation. Continued investment in research and development to create advanced phenol derivatives with enhanced performance characteristics will be crucial for capturing value in high-growth sectors like advanced composites and specialized polymers. The evolving regulatory landscape, while presenting challenges, also acts as a catalyst for developing greener production processes and more sustainable product offerings, shaping a positive long-term outlook for the Phenol market.

Phenol Market Segmentation

-

1. Product Type

- 1.1. Phenolic Resins

- 1.2. Caprolactum

- 1.3. Bisphenol-A

- 1.4. Other Product Types

Phenol Market Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Phenol Market Regional Market Share

Geographic Coverage of Phenol Market

Phenol Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Phenolic Resins

- 5.1.2. Caprolactum

- 5.1.3. Bisphenol-A

- 5.1.4. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Asia Pacific

- 5.2.2. North America

- 5.2.3. Europe

- 5.2.4. South America

- 5.2.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Phenol Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Phenolic Resins

- 6.1.2. Caprolactum

- 6.1.3. Bisphenol-A

- 6.1.4. Other Product Types

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Asia Pacific Phenol Market Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Phenolic Resins

- 7.1.2. Caprolactum

- 7.1.3. Bisphenol-A

- 7.1.4. Other Product Types

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. North America Phenol Market Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Phenolic Resins

- 8.1.2. Caprolactum

- 8.1.3. Bisphenol-A

- 8.1.4. Other Product Types

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Europe Phenol Market Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Phenolic Resins

- 9.1.2. Caprolactum

- 9.1.3. Bisphenol-A

- 9.1.4. Other Product Types

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. South America Phenol Market Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Phenolic Resins

- 10.1.2. Caprolactum

- 10.1.3. Bisphenol-A

- 10.1.4. Other Product Types

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Middle East and Africa Phenol Market Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Phenolic Resins

- 11.1.2. Caprolactum

- 11.1.3. Bisphenol-A

- 11.1.4. Other Product Types

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Shell PLC

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Solvay

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 AdvanSix Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Mitsui Chemicals Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Mitsubishi Chemical Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Cepsa

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Altivia

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Domo Chemical GmbH

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 PTT Phenol Company Limited

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Formosa Chemicals & Fibre Corp

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 INEOS Capital Limited

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Kumho P&B Chemicals Inc

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Shell PLC

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Phenol Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Phenol Market Volume Breakdown (K Tons, %) by Region 2025 & 2033

- Figure 3: Asia Pacific Phenol Market Revenue (billion), by Product Type 2025 & 2033

- Figure 4: Asia Pacific Phenol Market Volume (K Tons), by Product Type 2025 & 2033

- Figure 5: Asia Pacific Phenol Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: Asia Pacific Phenol Market Volume Share (%), by Product Type 2025 & 2033

- Figure 7: Asia Pacific Phenol Market Revenue (billion), by Country 2025 & 2033

- Figure 8: Asia Pacific Phenol Market Volume (K Tons), by Country 2025 & 2033

- Figure 9: Asia Pacific Phenol Market Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Phenol Market Volume Share (%), by Country 2025 & 2033

- Figure 11: North America Phenol Market Revenue (billion), by Product Type 2025 & 2033

- Figure 12: North America Phenol Market Volume (K Tons), by Product Type 2025 & 2033

- Figure 13: North America Phenol Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 14: North America Phenol Market Volume Share (%), by Product Type 2025 & 2033

- Figure 15: North America Phenol Market Revenue (billion), by Country 2025 & 2033

- Figure 16: North America Phenol Market Volume (K Tons), by Country 2025 & 2033

- Figure 17: North America Phenol Market Revenue Share (%), by Country 2025 & 2033

- Figure 18: North America Phenol Market Volume Share (%), by Country 2025 & 2033

- Figure 19: Europe Phenol Market Revenue (billion), by Product Type 2025 & 2033

- Figure 20: Europe Phenol Market Volume (K Tons), by Product Type 2025 & 2033

- Figure 21: Europe Phenol Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 22: Europe Phenol Market Volume Share (%), by Product Type 2025 & 2033

- Figure 23: Europe Phenol Market Revenue (billion), by Country 2025 & 2033

- Figure 24: Europe Phenol Market Volume (K Tons), by Country 2025 & 2033

- Figure 25: Europe Phenol Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Phenol Market Volume Share (%), by Country 2025 & 2033

- Figure 27: South America Phenol Market Revenue (billion), by Product Type 2025 & 2033

- Figure 28: South America Phenol Market Volume (K Tons), by Product Type 2025 & 2033

- Figure 29: South America Phenol Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 30: South America Phenol Market Volume Share (%), by Product Type 2025 & 2033

- Figure 31: South America Phenol Market Revenue (billion), by Country 2025 & 2033

- Figure 32: South America Phenol Market Volume (K Tons), by Country 2025 & 2033

- Figure 33: South America Phenol Market Revenue Share (%), by Country 2025 & 2033

- Figure 34: South America Phenol Market Volume Share (%), by Country 2025 & 2033

- Figure 35: Middle East and Africa Phenol Market Revenue (billion), by Product Type 2025 & 2033

- Figure 36: Middle East and Africa Phenol Market Volume (K Tons), by Product Type 2025 & 2033

- Figure 37: Middle East and Africa Phenol Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 38: Middle East and Africa Phenol Market Volume Share (%), by Product Type 2025 & 2033

- Figure 39: Middle East and Africa Phenol Market Revenue (billion), by Country 2025 & 2033

- Figure 40: Middle East and Africa Phenol Market Volume (K Tons), by Country 2025 & 2033

- Figure 41: Middle East and Africa Phenol Market Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa Phenol Market Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Phenol Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Global Phenol Market Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 3: Global Phenol Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Phenol Market Volume K Tons Forecast, by Region 2020 & 2033

- Table 5: Global Phenol Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 6: Global Phenol Market Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 7: Global Phenol Market Revenue billion Forecast, by Country 2020 & 2033

- Table 8: Global Phenol Market Volume K Tons Forecast, by Country 2020 & 2033

- Table 9: China Phenol Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: China Phenol Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 11: India Phenol Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: India Phenol Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 13: Japan Phenol Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Japan Phenol Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 15: South Korea Phenol Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: South Korea Phenol Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 17: Rest of Asia Pacific Phenol Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Rest of Asia Pacific Phenol Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 19: Global Phenol Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 20: Global Phenol Market Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 21: Global Phenol Market Revenue billion Forecast, by Country 2020 & 2033

- Table 22: Global Phenol Market Volume K Tons Forecast, by Country 2020 & 2033

- Table 23: United States Phenol Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: United States Phenol Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 25: Canada Phenol Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Canada Phenol Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 27: Mexico Phenol Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Mexico Phenol Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 29: Global Phenol Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 30: Global Phenol Market Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 31: Global Phenol Market Revenue billion Forecast, by Country 2020 & 2033

- Table 32: Global Phenol Market Volume K Tons Forecast, by Country 2020 & 2033

- Table 33: Germany Phenol Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Germany Phenol Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 35: United Kingdom Phenol Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: United Kingdom Phenol Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 37: France Phenol Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: France Phenol Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 39: Italy Phenol Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Italy Phenol Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 41: Rest of Europe Phenol Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Rest of Europe Phenol Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 43: Global Phenol Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 44: Global Phenol Market Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 45: Global Phenol Market Revenue billion Forecast, by Country 2020 & 2033

- Table 46: Global Phenol Market Volume K Tons Forecast, by Country 2020 & 2033

- Table 47: Brazil Phenol Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Brazil Phenol Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 49: Argentina Phenol Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Argentina Phenol Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 51: Rest of South America Phenol Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Rest of South America Phenol Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 53: Global Phenol Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 54: Global Phenol Market Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 55: Global Phenol Market Revenue billion Forecast, by Country 2020 & 2033

- Table 56: Global Phenol Market Volume K Tons Forecast, by Country 2020 & 2033

- Table 57: Saudi Arabia Phenol Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 58: Saudi Arabia Phenol Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 59: South Africa Phenol Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 60: South Africa Phenol Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 61: Rest of Middle East and Africa Phenol Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Rest of Middle East and Africa Phenol Market Volume (K Tons) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Phenol Market?

The projected CAGR is approximately 4.3%.

2. Which companies are prominent players in the Phenol Market?

Key companies in the market include Shell PLC, Solvay, AdvanSix Inc, Mitsui Chemicals Inc, Mitsubishi Chemical Corporation, Cepsa, Altivia, Domo Chemical GmbH, PTT Phenol Company Limited, Formosa Chemicals & Fibre Corp, INEOS Capital Limited, Kumho P&B Chemicals Inc.

3. What are the main segments of the Phenol Market?

The market segments include Product Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 13.3 billion as of 2022.

5. What are some drivers contributing to market growth?

High Demand of Bisphenol-A; Other Drivers.

6. What are the notable trends driving market growth?

Bisphenol-A Product Type to Drive the Market.

7. Are there any restraints impacting market growth?

Ban on BPA in the United States and Europe; Others Restraints.

8. Can you provide examples of recent developments in the market?

August 2022: INEOS Phenol announced the acquisition of the asset base of Mitsui Phenols Singapore Ltd from Mitsui Chemicals for a total consideration of USD 330 million. The addition of the Jurong phenol and BPA assets will provide integration opportunities with manufacturing sites in Germany, Belgium, and the United States. The acquisition will increase the total production capacity by 1 million tonnes.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Phenol Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Phenol Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Phenol Market?

To stay informed about further developments, trends, and reports in the Phenol Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence