Key Insights

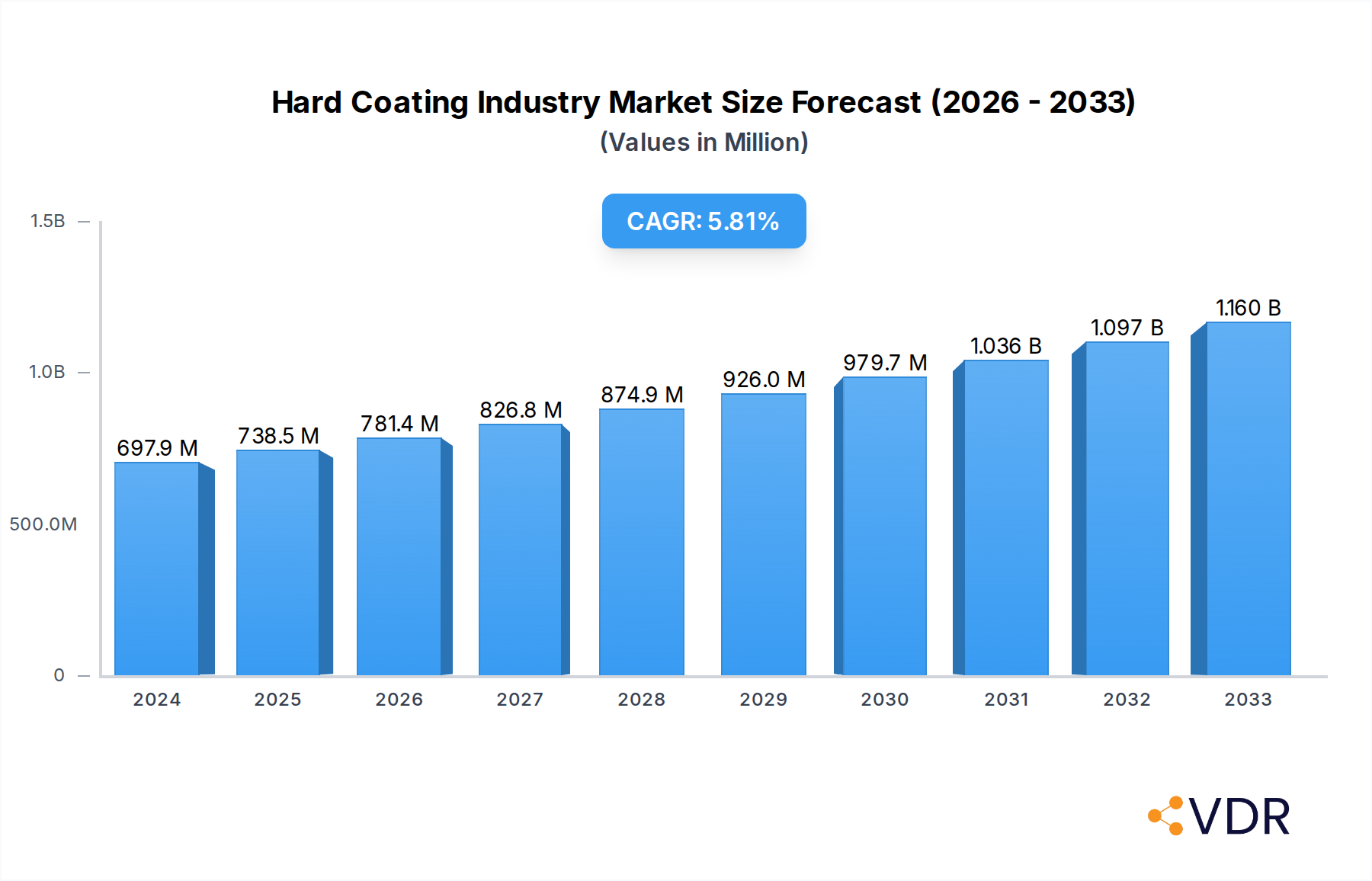

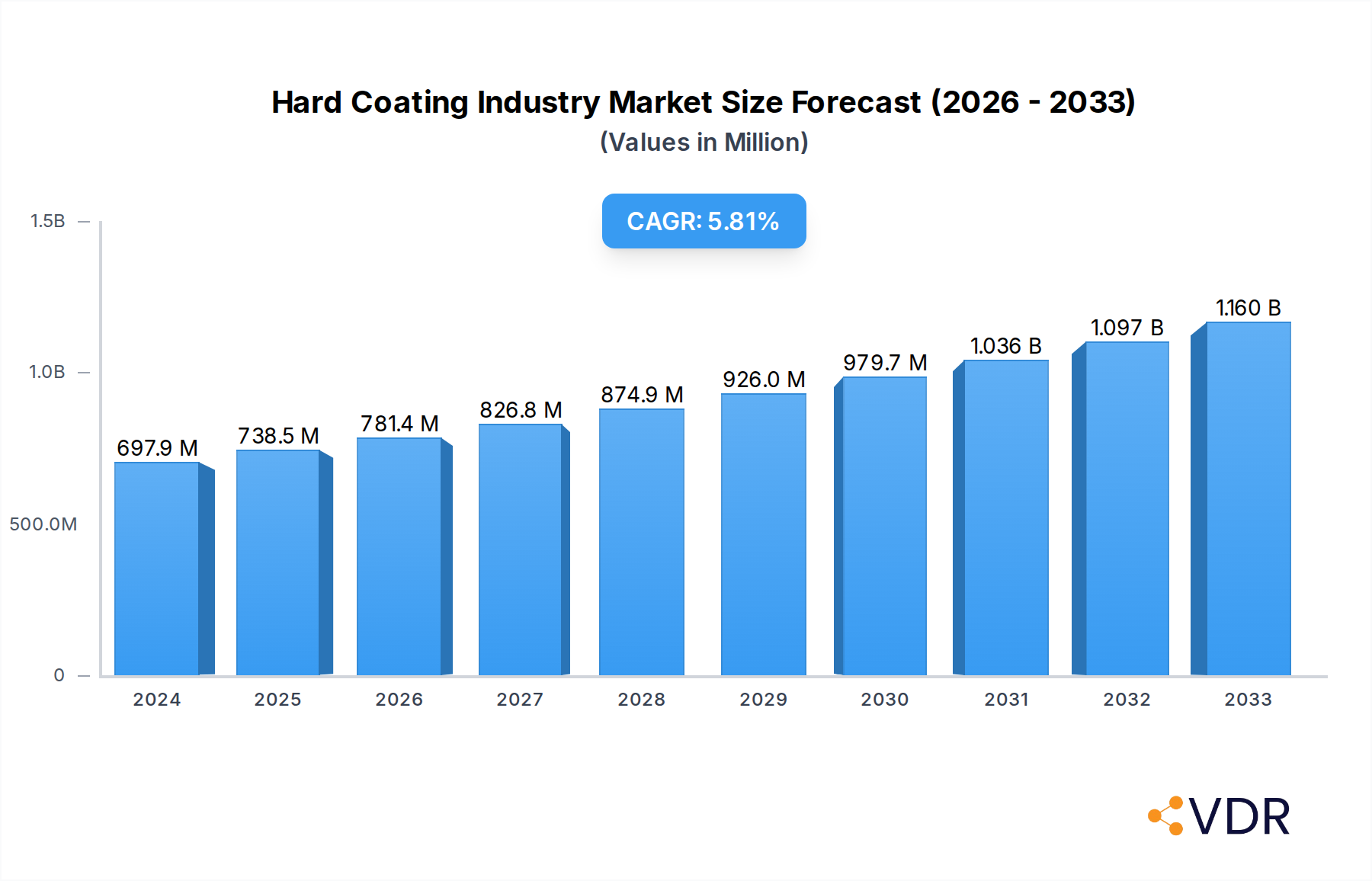

The global Hard Coating Industry is experiencing robust growth, projected to reach an estimated $697.9 million by 2024, with a compelling Compound Annual Growth Rate (CAGR) of 5.8% expected to propel it through 2033. This expansion is primarily driven by the increasing demand for enhanced durability, wear resistance, and performance across a multitude of industrial applications. Key market drivers include the burgeoning automotive sector's need for high-performance components, the continuous innovation in manufacturing processes requiring specialized surface treatments, and the growing adoption of advanced materials in sectors like aerospace and defense. Furthermore, the rising emphasis on extending product lifecycles and reducing maintenance costs significantly fuels the adoption of hard coatings, making them an indispensable solution for a wide array of manufacturing challenges.

Hard Coating Industry Market Size (In Million)

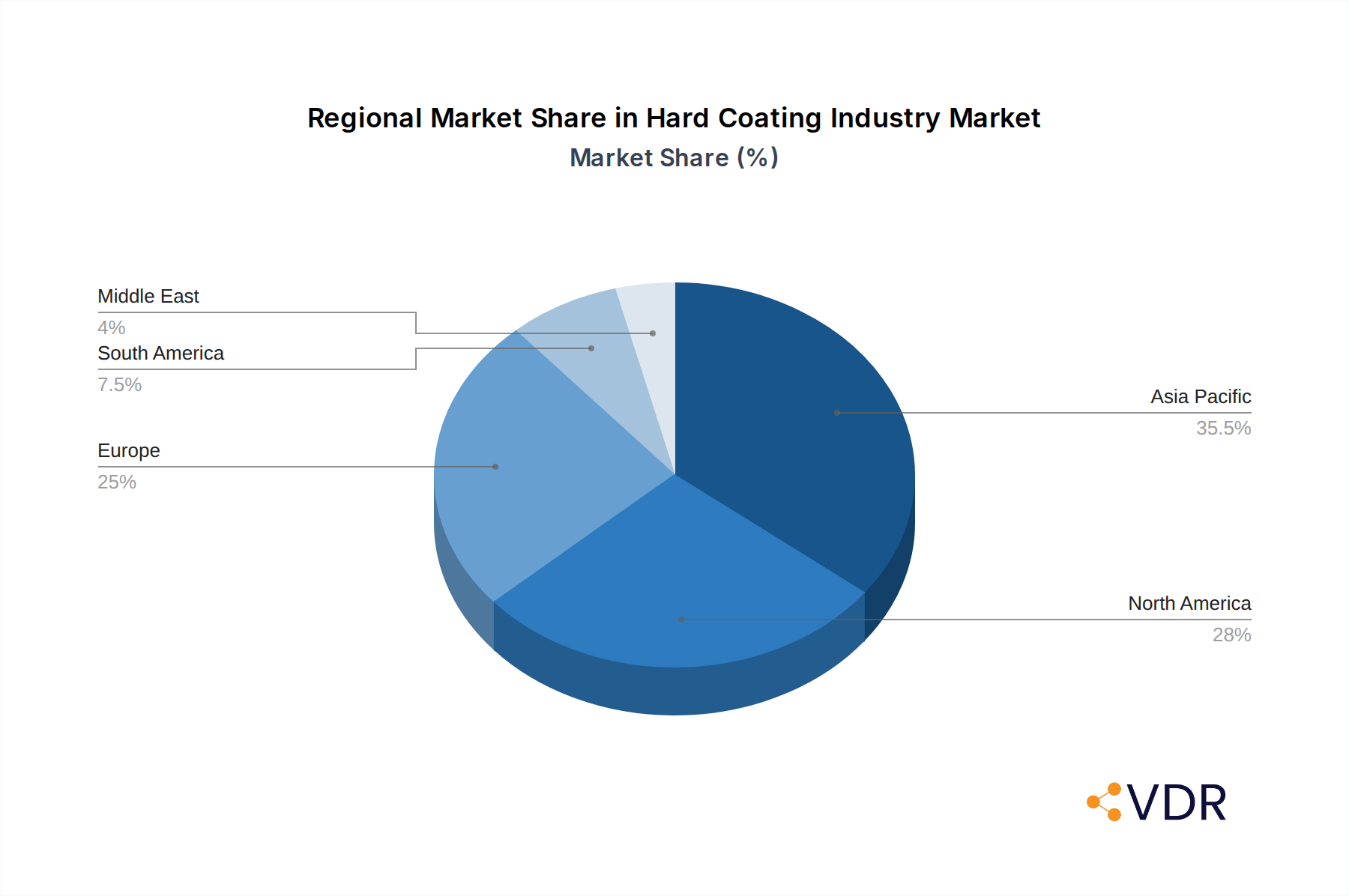

The market is characterized by a diverse range of segments, offering tailored solutions for specific needs. In terms of material types, carbon-based coatings, oxides, nitrides, and carbides are prominent, each offering unique properties like extreme hardness, chemical inertness, and thermal resistance. The PVD (Physical Vapor Deposition) and CVD (Chemical Vapor Deposition) techniques dominate the application landscape, enabling precise and uniform coating deposition. Geographically, the Asia Pacific region, led by China and India, is anticipated to be a major growth engine, owing to its rapid industrialization and substantial manufacturing base. While the market presents significant opportunities, potential restraints such as the high initial investment costs for advanced coating equipment and the availability of skilled labor could pose challenges. However, ongoing technological advancements and increasing awareness of the long-term economic benefits are expected to mitigate these factors, ensuring sustained market expansion.

Hard Coating Industry Company Market Share

Comprehensive Hard Coating Industry Report: Market Dynamics, Growth Trends, and Future Outlook (2019-2033)

This in-depth market report offers a panoramic view of the global Hard Coating Industry, meticulously analyzing its intricate dynamics, robust growth trajectories, and the pivotal role of parent and child markets. Covering the historical period from 2019 to 2024 and projecting forward to 2033, with a base and estimated year of 2025, this analysis provides critical insights for industry stakeholders seeking to navigate this high-growth sector. The report quantifies market evolution in million units, focusing on key segments, innovative techniques, diverse applications, and critical end-user industries.

Hard Coating Industry Market Dynamics & Structure

The Hard Coating Industry exhibits a moderate to high level of market concentration, with key players investing heavily in research and development to drive technological innovation. The increasing demand for enhanced durability, wear resistance, and aesthetic appeal across various sectors fuels the adoption of advanced hard coating technologies. Regulatory frameworks, particularly those related to environmental impact and material safety, are gradually influencing manufacturing processes and product development, encouraging the use of more sustainable coating materials. Competitive product substitutes, such as advanced polymers and alternative surface treatments, present a constant challenge, pushing manufacturers to continuously innovate and differentiate their offerings. End-user demographics are shifting towards industries requiring high-performance solutions, including automotive, aerospace, and electronics, driving specialized coating demands. Mergers and acquisitions (M&A) are notable trends, with larger entities acquiring innovative smaller firms to expand their technological portfolios and market reach. For instance, the volume of M&A deals in the specialty coatings sector has seen a steady rise, with an estimated 25-30% increase in deal activity over the past three years, reflecting strategic consolidation and the pursuit of market dominance. Barriers to innovation include the high cost of specialized equipment, the need for skilled labor, and lengthy validation processes for new coating formulations and application techniques.

- Market Concentration: Moderate to High, with a few dominant players and a growing number of specialized niche providers.

- Technological Innovation Drivers: Demand for enhanced durability, wear resistance, corrosion protection, friction reduction, and aesthetic appeal.

- Regulatory Frameworks: Growing emphasis on environmental compliance, REACH, and RoHS directives impacting material selection and manufacturing processes.

- Competitive Product Substitutes: Advanced polymers, ceramic coatings, and novel surface engineering techniques.

- End-User Demographics: Increasing demand from automotive, aerospace, industrial manufacturing, and electronics sectors.

- M&A Trends: Strategic acquisitions to gain access to novel technologies and expand market share.

Hard Coating Industry Growth Trends & Insights

The global Hard Coating Industry is poised for significant expansion, driven by escalating demand for enhanced material performance and longevity across a multitude of applications. The market is anticipated to grow at a Compound Annual Growth Rate (CAGR) of approximately 7.5% from 2025 to 2033, reaching an estimated market size of $35,000 million units by the end of the forecast period. This robust growth is underpinned by continuous technological advancements in coating materials and application techniques, particularly in the realms of Physical Vapor Deposition (PVD) and Chemical Vapor Deposition (CVD). The increasing adoption of these technologies in sectors like automotive for engine components, cutting tools for improved efficiency, and optics for enhanced clarity and protection, significantly contributes to market penetration. Consumer behavior is also evolving, with a growing preference for durable, high-performance products that offer extended lifespans, thereby boosting the demand for hard coatings. Furthermore, industry developments such as the integration of AI in process optimization and the development of self-healing and anti-microbial hard coatings are opening up new avenues for market expansion. The parent market, encompassing the broader surface treatment and finishing sector, provides a fertile ground for hard coatings to thrive, benefiting from established supply chains and a wide network of manufacturers. Child markets, such as specialized coatings for additive manufacturing or advanced protective layers for renewable energy components, are emerging as significant growth drivers. The market penetration for high-performance hard coatings in niche applications is expected to rise from approximately 45% in 2025 to over 60% by 2033, underscoring the growing indispensability of these solutions.

Dominant Regions, Countries, or Segments in Hard Coating Industry

The dominance in the Hard Coating Industry is multifaceted, with specific regions, countries, and segments exhibiting exceptional growth and market share. Geographically, Asia-Pacific stands out as the leading region, driven by its robust manufacturing base, burgeoning automotive sector, and substantial investments in industrial infrastructure. Countries like China, Japan, and South Korea are at the forefront, owing to their strong presence in electronics manufacturing, automotive production, and toolmaking industries. In terms of Material Type, Nitrides, particularly Titanium Nitride (TiN) and Chromium Nitride (CrN), are commanding significant market share due to their superior hardness, wear resistance, and chemical inertness, making them ideal for cutting tools and industrial applications. The PVD (Physical Vapor Deposition) technique is the most dominant application method, offering precise control, excellent film quality, and the ability to coat complex shapes without significant heat input. This technique is widely favored for its versatility and cost-effectiveness in producing thin, hard coatings. Within the Application segment, Cutting tools represent a substantial market, as the demand for efficient and durable tools for machining metals and other materials continues to grow exponentially. The Automotive end-user industry is a key driver of this dominance, with hard coatings being extensively used for engine components, transmission parts, and decorative elements to enhance performance, durability, and aesthetics. Economic policies in Asia-Pacific, such as government initiatives promoting advanced manufacturing and technological adoption, coupled with substantial infrastructure development, further bolster the growth of the hard coating market in this region. The market share of Nitride-based coatings in the industrial applications segment is estimated to be around 40%, with PVD techniques accounting for approximately 65% of all hard coating applications. The automotive sector's demand for hard coatings is projected to grow at a CAGR of 8.2% from 2025 to 2033.

- Leading Region: Asia-Pacific (China, Japan, South Korea)

- Dominant Material Type: Nitrides (TiN, CrN)

- Dominant Technique: PVD (Physical Vapor Deposition)

- Dominant Application: Cutting Tools

- Dominant End-user Industry: Automotive

- Key Drivers: Strong manufacturing base, automotive sector growth, technological advancements, supportive government policies, infrastructure development.

Hard Coating Industry Product Landscape

The product landscape of the Hard Coating Industry is characterized by continuous innovation, with a focus on enhancing performance metrics such as hardness, wear resistance, friction reduction, and corrosion protection. Companies are developing advanced coating materials, including nanocomposite hard coatings and multi-layer structures, to achieve synergistic property enhancements. These products find extensive applications in cutting tools, significantly extending their lifespan and improving machining efficiency. Decorative coatings are also a growing segment, offering aesthetic appeal combined with robust protection for consumer goods and automotive interiors. In the optics sector, ultra-hard and anti-reflective coatings are crucial for lenses and displays. Performance metrics such as Vickers hardness exceeding 25 GPa and friction coefficients below 0.2 are becoming standard for high-end applications. Technological advancements in PVD and CVD processes enable the deposition of coatings with atomic-level precision, leading to superior film adhesion and uniformity.

Key Drivers, Barriers & Challenges in Hard Coating Industry

The Hard Coating Industry is propelled by several key drivers, including the escalating demand for enhanced material performance and durability across various end-user industries, particularly automotive, aerospace, and industrial manufacturing. Technological advancements in deposition techniques like PVD and CVD, leading to superior coating properties, are crucial growth accelerators. The increasing emphasis on extending product lifespans and reducing maintenance costs also fuels market expansion.

Key Drivers:

- Performance Enhancement: Demand for superior hardness, wear resistance, and corrosion protection.

- Technological Advancements: Innovations in PVD, CVD, and new material formulations.

- Cost Reduction: Extended product life, reduced maintenance, and improved manufacturing efficiency.

- Sustainability Initiatives: Development of eco-friendly coating processes and materials.

Key Barriers & Challenges:

Supply chain disruptions, especially for rare earth elements and specialized precursor materials, pose a significant challenge, impacting production timelines and costs, with an estimated 15% increase in raw material costs over the past two years. The high capital investment required for advanced coating equipment and the need for skilled labor to operate and maintain these systems represent substantial entry barriers. Stringent regulatory compliance, particularly concerning environmental impact and worker safety, adds complexity and cost to manufacturing processes. Intense competition from both established players and emerging technologies also exerts pressure on pricing and innovation cycles.

Emerging Opportunities in Hard Coating Industry

Emerging opportunities within the Hard Coating Industry are diverse and promising. The growing market for electric vehicles (EVs) presents a significant avenue, with demand for specialized coatings for battery components, electric motors, and lightweight structural parts. The expansion of additive manufacturing (3D printing) is creating a need for advanced hard coatings that can enhance the performance and durability of 3D-printed components. The increasing focus on renewable energy sources, such as wind turbines and solar panels, also necessitates specialized coatings for improved resilience and longevity in harsh environments. Furthermore, the development of "smart" coatings with self-healing, anti-icing, or anti-microbial properties offers substantial untapped market potential.

Growth Accelerators in the Hard Coating Industry Industry

The long-term growth of the Hard Coating Industry is significantly accelerated by a confluence of technological breakthroughs and strategic market expansion. The continuous refinement of PVD and CVD techniques, alongside the exploration of novel deposition methods, is enabling the creation of coatings with unprecedented performance characteristics. Collaborations between coating manufacturers and end-user industries are fostering co-development of tailor-made solutions, driving adoption in specialized applications. Strategic partnerships with research institutions are also crucial for pushing the boundaries of material science and coating technology, leading to the development of next-generation hard coatings. Furthermore, market expansion into developing economies, driven by industrialization and infrastructure development, provides a substantial runway for sustained growth.

Key Players Shaping the Hard Coating Industry Market

- MBI Coatings

- DIARC-Technology Oy

- Hardcoatings Inc

- Kobe Steel Ltd

- Sulzer Ltd

- IHI Ionbond AG

- OC Oerlikon Management AG

- CemeCon

- Momentive

- Dhake Industries

- Duralar Technologies

- Voestalpine Eifeler Group

- Ultra Optics

- IHI Hauzer BV

- Carl Zeiss AG

- ASB Industries Inc

- Platit AG

- Exxene Corporation

- SDC Technologies Inc

- Gencoa Ltd

Notable Milestones in Hard Coating Industry Sector

- 2019: Launch of advanced DLC (Diamond-Like Carbon) coatings with significantly improved wear resistance for automotive components.

- 2020: Development of novel ceramic hard coatings offering superior thermal barrier properties for aerospace applications.

- 2021: Increased investment in R&D for sustainable and eco-friendly hard coating processes and materials.

- 2022: Introduction of high-throughput PVD systems enabling faster and more cost-effective coating of large batches.

- 2023: Strategic partnerships formed to develop specialized hard coatings for the rapidly growing electric vehicle battery market.

- 2024: Advancements in multi-layer hard coating architectures achieving synergistic improvements in hardness and toughness.

In-Depth Hard Coating Industry Market Outlook

The future of the Hard Coating Industry appears exceptionally robust, driven by the persistent demand for superior material performance and the relentless pace of technological innovation. Growth accelerators, including the development of advanced nanocomposite and gradient coatings, alongside advancements in plasma-enhanced CVD and magnetron sputtering techniques, will continue to push the performance envelope. The expanding applications in emerging sectors like electric mobility, renewable energy, and advanced medical devices present significant untapped market potential. Strategic alliances, market penetration into developing regions, and a continued focus on developing environmentally sustainable coating solutions will be pivotal in capitalizing on these opportunities. The industry is set to witness sustained growth, fueled by its critical role in enhancing product durability, efficiency, and functionality across the global manufacturing landscape.

Hard Coating Industry Segmentation

-

1. Material Type

- 1.1. Carbon-based

- 1.2. Oxides

- 1.3. Nitrides

- 1.4. Carbides

- 1.5. Other Materials

-

2. Technique

- 2.1. PVD (Physical Vapor Deposition)

- 2.2. CVD (Chemical Vapor Deposition)

-

3. Application

- 3.1. Cutting tools

- 3.2. Decorative Coatings

- 3.3. Optics

- 3.4. Gears and Bearings

- 3.5. Other Applications

-

4. End-user Industry

- 4.1. Building and Construction

- 4.2. General manufacturing

- 4.3. Automotive

- 4.4. Transportation

- 4.5. Industrial

- 4.6. Other End-user Industries

Hard Coating Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. Italy

- 3.4. France

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

- 5. Middle East

-

6. Saudi Arabia

- 6.1. South Africa

- 6.2. Rest of Middle East

Hard Coating Industry Regional Market Share

Geographic Coverage of Hard Coating Industry

Hard Coating Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Carbon-based

- 5.1.2. Oxides

- 5.1.3. Nitrides

- 5.1.4. Carbides

- 5.1.5. Other Materials

- 5.2. Market Analysis, Insights and Forecast - by Technique

- 5.2.1. PVD (Physical Vapor Deposition)

- 5.2.2. CVD (Chemical Vapor Deposition)

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Cutting tools

- 5.3.2. Decorative Coatings

- 5.3.3. Optics

- 5.3.4. Gears and Bearings

- 5.3.5. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by End-user Industry

- 5.4.1. Building and Construction

- 5.4.2. General manufacturing

- 5.4.3. Automotive

- 5.4.4. Transportation

- 5.4.5. Industrial

- 5.4.6. Other End-user Industries

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Asia Pacific

- 5.5.2. North America

- 5.5.3. Europe

- 5.5.4. South America

- 5.5.5. Middle East

- 5.5.6. Saudi Arabia

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. Global Hard Coating Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Carbon-based

- 6.1.2. Oxides

- 6.1.3. Nitrides

- 6.1.4. Carbides

- 6.1.5. Other Materials

- 6.2. Market Analysis, Insights and Forecast - by Technique

- 6.2.1. PVD (Physical Vapor Deposition)

- 6.2.2. CVD (Chemical Vapor Deposition)

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Cutting tools

- 6.3.2. Decorative Coatings

- 6.3.3. Optics

- 6.3.4. Gears and Bearings

- 6.3.5. Other Applications

- 6.4. Market Analysis, Insights and Forecast - by End-user Industry

- 6.4.1. Building and Construction

- 6.4.2. General manufacturing

- 6.4.3. Automotive

- 6.4.4. Transportation

- 6.4.5. Industrial

- 6.4.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. Asia Pacific Hard Coating Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 7.1.1. Carbon-based

- 7.1.2. Oxides

- 7.1.3. Nitrides

- 7.1.4. Carbides

- 7.1.5. Other Materials

- 7.2. Market Analysis, Insights and Forecast - by Technique

- 7.2.1. PVD (Physical Vapor Deposition)

- 7.2.2. CVD (Chemical Vapor Deposition)

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Cutting tools

- 7.3.2. Decorative Coatings

- 7.3.3. Optics

- 7.3.4. Gears and Bearings

- 7.3.5. Other Applications

- 7.4. Market Analysis, Insights and Forecast - by End-user Industry

- 7.4.1. Building and Construction

- 7.4.2. General manufacturing

- 7.4.3. Automotive

- 7.4.4. Transportation

- 7.4.5. Industrial

- 7.4.6. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 8. North America Hard Coating Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 8.1.1. Carbon-based

- 8.1.2. Oxides

- 8.1.3. Nitrides

- 8.1.4. Carbides

- 8.1.5. Other Materials

- 8.2. Market Analysis, Insights and Forecast - by Technique

- 8.2.1. PVD (Physical Vapor Deposition)

- 8.2.2. CVD (Chemical Vapor Deposition)

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Cutting tools

- 8.3.2. Decorative Coatings

- 8.3.3. Optics

- 8.3.4. Gears and Bearings

- 8.3.5. Other Applications

- 8.4. Market Analysis, Insights and Forecast - by End-user Industry

- 8.4.1. Building and Construction

- 8.4.2. General manufacturing

- 8.4.3. Automotive

- 8.4.4. Transportation

- 8.4.5. Industrial

- 8.4.6. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 9. Europe Hard Coating Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 9.1.1. Carbon-based

- 9.1.2. Oxides

- 9.1.3. Nitrides

- 9.1.4. Carbides

- 9.1.5. Other Materials

- 9.2. Market Analysis, Insights and Forecast - by Technique

- 9.2.1. PVD (Physical Vapor Deposition)

- 9.2.2. CVD (Chemical Vapor Deposition)

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Cutting tools

- 9.3.2. Decorative Coatings

- 9.3.3. Optics

- 9.3.4. Gears and Bearings

- 9.3.5. Other Applications

- 9.4. Market Analysis, Insights and Forecast - by End-user Industry

- 9.4.1. Building and Construction

- 9.4.2. General manufacturing

- 9.4.3. Automotive

- 9.4.4. Transportation

- 9.4.5. Industrial

- 9.4.6. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 10. South America Hard Coating Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 10.1.1. Carbon-based

- 10.1.2. Oxides

- 10.1.3. Nitrides

- 10.1.4. Carbides

- 10.1.5. Other Materials

- 10.2. Market Analysis, Insights and Forecast - by Technique

- 10.2.1. PVD (Physical Vapor Deposition)

- 10.2.2. CVD (Chemical Vapor Deposition)

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Cutting tools

- 10.3.2. Decorative Coatings

- 10.3.3. Optics

- 10.3.4. Gears and Bearings

- 10.3.5. Other Applications

- 10.4. Market Analysis, Insights and Forecast - by End-user Industry

- 10.4.1. Building and Construction

- 10.4.2. General manufacturing

- 10.4.3. Automotive

- 10.4.4. Transportation

- 10.4.5. Industrial

- 10.4.6. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 11. Middle East Hard Coating Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Material Type

- 11.1.1. Carbon-based

- 11.1.2. Oxides

- 11.1.3. Nitrides

- 11.1.4. Carbides

- 11.1.5. Other Materials

- 11.2. Market Analysis, Insights and Forecast - by Technique

- 11.2.1. PVD (Physical Vapor Deposition)

- 11.2.2. CVD (Chemical Vapor Deposition)

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Cutting tools

- 11.3.2. Decorative Coatings

- 11.3.3. Optics

- 11.3.4. Gears and Bearings

- 11.3.5. Other Applications

- 11.4. Market Analysis, Insights and Forecast - by End-user Industry

- 11.4.1. Building and Construction

- 11.4.2. General manufacturing

- 11.4.3. Automotive

- 11.4.4. Transportation

- 11.4.5. Industrial

- 11.4.6. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Material Type

- 12. Saudi Arabia Hard Coating Industry Analysis, Insights and Forecast, 2021-2033

- 12.1. Market Analysis, Insights and Forecast - by Material Type

- 12.1.1. Carbon-based

- 12.1.2. Oxides

- 12.1.3. Nitrides

- 12.1.4. Carbides

- 12.1.5. Other Materials

- 12.2. Market Analysis, Insights and Forecast - by Technique

- 12.2.1. PVD (Physical Vapor Deposition)

- 12.2.2. CVD (Chemical Vapor Deposition)

- 12.3. Market Analysis, Insights and Forecast - by Application

- 12.3.1. Cutting tools

- 12.3.2. Decorative Coatings

- 12.3.3. Optics

- 12.3.4. Gears and Bearings

- 12.3.5. Other Applications

- 12.4. Market Analysis, Insights and Forecast - by End-user Industry

- 12.4.1. Building and Construction

- 12.4.2. General manufacturing

- 12.4.3. Automotive

- 12.4.4. Transportation

- 12.4.5. Industrial

- 12.4.6. Other End-user Industries

- 12.1. Market Analysis, Insights and Forecast - by Material Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 MBI Coatings

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 DIARC-Technology Oy

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Hardcoatings Inc

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Kobe Steel Ltd

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Sulzer Ltd

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 IHI Ionbond AG

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 OC Oerlikon Management AG

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 CemeCon

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Momentive

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 DhakeIndustries

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Duralar Technologies

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 Voestalpine Eifeler Group*List Not Exhaustive

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.13 Ultra Optics

- 13.1.13.1. Company Overview

- 13.1.13.2. Products

- 13.1.13.3. Company Financials

- 13.1.13.4. SWOT Analysis

- 13.1.14 IHI Hauzer BV

- 13.1.14.1. Company Overview

- 13.1.14.2. Products

- 13.1.14.3. Company Financials

- 13.1.14.4. SWOT Analysis

- 13.1.15 Carl Zeiss AG

- 13.1.15.1. Company Overview

- 13.1.15.2. Products

- 13.1.15.3. Company Financials

- 13.1.15.4. SWOT Analysis

- 13.1.16 ASB Industries Inc

- 13.1.16.1. Company Overview

- 13.1.16.2. Products

- 13.1.16.3. Company Financials

- 13.1.16.4. SWOT Analysis

- 13.1.17 Platit AG

- 13.1.17.1. Company Overview

- 13.1.17.2. Products

- 13.1.17.3. Company Financials

- 13.1.17.4. SWOT Analysis

- 13.1.18 Exxene Corporation

- 13.1.18.1. Company Overview

- 13.1.18.2. Products

- 13.1.18.3. Company Financials

- 13.1.18.4. SWOT Analysis

- 13.1.19 SDC Technologies Inc

- 13.1.19.1. Company Overview

- 13.1.19.2. Products

- 13.1.19.3. Company Financials

- 13.1.19.4. SWOT Analysis

- 13.1.20 Gencoa Ltd

- 13.1.20.1. Company Overview

- 13.1.20.2. Products

- 13.1.20.3. Company Financials

- 13.1.20.4. SWOT Analysis

- 13.1.1 MBI Coatings

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Hard Coating Industry Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Hard Coating Industry Revenue (million), by Material Type 2025 & 2033

- Figure 3: Asia Pacific Hard Coating Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 4: Asia Pacific Hard Coating Industry Revenue (million), by Technique 2025 & 2033

- Figure 5: Asia Pacific Hard Coating Industry Revenue Share (%), by Technique 2025 & 2033

- Figure 6: Asia Pacific Hard Coating Industry Revenue (million), by Application 2025 & 2033

- Figure 7: Asia Pacific Hard Coating Industry Revenue Share (%), by Application 2025 & 2033

- Figure 8: Asia Pacific Hard Coating Industry Revenue (million), by End-user Industry 2025 & 2033

- Figure 9: Asia Pacific Hard Coating Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 10: Asia Pacific Hard Coating Industry Revenue (million), by Country 2025 & 2033

- Figure 11: Asia Pacific Hard Coating Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: North America Hard Coating Industry Revenue (million), by Material Type 2025 & 2033

- Figure 13: North America Hard Coating Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 14: North America Hard Coating Industry Revenue (million), by Technique 2025 & 2033

- Figure 15: North America Hard Coating Industry Revenue Share (%), by Technique 2025 & 2033

- Figure 16: North America Hard Coating Industry Revenue (million), by Application 2025 & 2033

- Figure 17: North America Hard Coating Industry Revenue Share (%), by Application 2025 & 2033

- Figure 18: North America Hard Coating Industry Revenue (million), by End-user Industry 2025 & 2033

- Figure 19: North America Hard Coating Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 20: North America Hard Coating Industry Revenue (million), by Country 2025 & 2033

- Figure 21: North America Hard Coating Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Europe Hard Coating Industry Revenue (million), by Material Type 2025 & 2033

- Figure 23: Europe Hard Coating Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 24: Europe Hard Coating Industry Revenue (million), by Technique 2025 & 2033

- Figure 25: Europe Hard Coating Industry Revenue Share (%), by Technique 2025 & 2033

- Figure 26: Europe Hard Coating Industry Revenue (million), by Application 2025 & 2033

- Figure 27: Europe Hard Coating Industry Revenue Share (%), by Application 2025 & 2033

- Figure 28: Europe Hard Coating Industry Revenue (million), by End-user Industry 2025 & 2033

- Figure 29: Europe Hard Coating Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Europe Hard Coating Industry Revenue (million), by Country 2025 & 2033

- Figure 31: Europe Hard Coating Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: South America Hard Coating Industry Revenue (million), by Material Type 2025 & 2033

- Figure 33: South America Hard Coating Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 34: South America Hard Coating Industry Revenue (million), by Technique 2025 & 2033

- Figure 35: South America Hard Coating Industry Revenue Share (%), by Technique 2025 & 2033

- Figure 36: South America Hard Coating Industry Revenue (million), by Application 2025 & 2033

- Figure 37: South America Hard Coating Industry Revenue Share (%), by Application 2025 & 2033

- Figure 38: South America Hard Coating Industry Revenue (million), by End-user Industry 2025 & 2033

- Figure 39: South America Hard Coating Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 40: South America Hard Coating Industry Revenue (million), by Country 2025 & 2033

- Figure 41: South America Hard Coating Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East Hard Coating Industry Revenue (million), by Material Type 2025 & 2033

- Figure 43: Middle East Hard Coating Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 44: Middle East Hard Coating Industry Revenue (million), by Technique 2025 & 2033

- Figure 45: Middle East Hard Coating Industry Revenue Share (%), by Technique 2025 & 2033

- Figure 46: Middle East Hard Coating Industry Revenue (million), by Application 2025 & 2033

- Figure 47: Middle East Hard Coating Industry Revenue Share (%), by Application 2025 & 2033

- Figure 48: Middle East Hard Coating Industry Revenue (million), by End-user Industry 2025 & 2033

- Figure 49: Middle East Hard Coating Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 50: Middle East Hard Coating Industry Revenue (million), by Country 2025 & 2033

- Figure 51: Middle East Hard Coating Industry Revenue Share (%), by Country 2025 & 2033

- Figure 52: Saudi Arabia Hard Coating Industry Revenue (million), by Material Type 2025 & 2033

- Figure 53: Saudi Arabia Hard Coating Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 54: Saudi Arabia Hard Coating Industry Revenue (million), by Technique 2025 & 2033

- Figure 55: Saudi Arabia Hard Coating Industry Revenue Share (%), by Technique 2025 & 2033

- Figure 56: Saudi Arabia Hard Coating Industry Revenue (million), by Application 2025 & 2033

- Figure 57: Saudi Arabia Hard Coating Industry Revenue Share (%), by Application 2025 & 2033

- Figure 58: Saudi Arabia Hard Coating Industry Revenue (million), by End-user Industry 2025 & 2033

- Figure 59: Saudi Arabia Hard Coating Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 60: Saudi Arabia Hard Coating Industry Revenue (million), by Country 2025 & 2033

- Figure 61: Saudi Arabia Hard Coating Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Hard Coating Industry Revenue million Forecast, by Material Type 2020 & 2033

- Table 2: Global Hard Coating Industry Revenue million Forecast, by Technique 2020 & 2033

- Table 3: Global Hard Coating Industry Revenue million Forecast, by Application 2020 & 2033

- Table 4: Global Hard Coating Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 5: Global Hard Coating Industry Revenue million Forecast, by Region 2020 & 2033

- Table 6: Global Hard Coating Industry Revenue million Forecast, by Material Type 2020 & 2033

- Table 7: Global Hard Coating Industry Revenue million Forecast, by Technique 2020 & 2033

- Table 8: Global Hard Coating Industry Revenue million Forecast, by Application 2020 & 2033

- Table 9: Global Hard Coating Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 10: Global Hard Coating Industry Revenue million Forecast, by Country 2020 & 2033

- Table 11: China Hard Coating Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 12: India Hard Coating Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 13: Japan Hard Coating Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: South Korea Hard Coating Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of Asia Pacific Hard Coating Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Hard Coating Industry Revenue million Forecast, by Material Type 2020 & 2033

- Table 17: Global Hard Coating Industry Revenue million Forecast, by Technique 2020 & 2033

- Table 18: Global Hard Coating Industry Revenue million Forecast, by Application 2020 & 2033

- Table 19: Global Hard Coating Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 20: Global Hard Coating Industry Revenue million Forecast, by Country 2020 & 2033

- Table 21: United States Hard Coating Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Canada Hard Coating Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Mexico Hard Coating Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Global Hard Coating Industry Revenue million Forecast, by Material Type 2020 & 2033

- Table 25: Global Hard Coating Industry Revenue million Forecast, by Technique 2020 & 2033

- Table 26: Global Hard Coating Industry Revenue million Forecast, by Application 2020 & 2033

- Table 27: Global Hard Coating Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 28: Global Hard Coating Industry Revenue million Forecast, by Country 2020 & 2033

- Table 29: Germany Hard Coating Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: United Kingdom Hard Coating Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 31: Italy Hard Coating Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: France Hard Coating Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: Rest of Europe Hard Coating Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: Global Hard Coating Industry Revenue million Forecast, by Material Type 2020 & 2033

- Table 35: Global Hard Coating Industry Revenue million Forecast, by Technique 2020 & 2033

- Table 36: Global Hard Coating Industry Revenue million Forecast, by Application 2020 & 2033

- Table 37: Global Hard Coating Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 38: Global Hard Coating Industry Revenue million Forecast, by Country 2020 & 2033

- Table 39: Brazil Hard Coating Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Argentina Hard Coating Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: Rest of South America Hard Coating Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Global Hard Coating Industry Revenue million Forecast, by Material Type 2020 & 2033

- Table 43: Global Hard Coating Industry Revenue million Forecast, by Technique 2020 & 2033

- Table 44: Global Hard Coating Industry Revenue million Forecast, by Application 2020 & 2033

- Table 45: Global Hard Coating Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 46: Global Hard Coating Industry Revenue million Forecast, by Country 2020 & 2033

- Table 47: Global Hard Coating Industry Revenue million Forecast, by Material Type 2020 & 2033

- Table 48: Global Hard Coating Industry Revenue million Forecast, by Technique 2020 & 2033

- Table 49: Global Hard Coating Industry Revenue million Forecast, by Application 2020 & 2033

- Table 50: Global Hard Coating Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 51: Global Hard Coating Industry Revenue million Forecast, by Country 2020 & 2033

- Table 52: South Africa Hard Coating Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 53: Rest of Middle East Hard Coating Industry Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Hard Coating Industry?

The projected CAGR is approximately 8.5%.

2. Which companies are prominent players in the Hard Coating Industry?

Key companies in the market include MBI Coatings, DIARC-Technology Oy, Hardcoatings Inc, Kobe Steel Ltd, Sulzer Ltd, IHI Ionbond AG, OC Oerlikon Management AG, CemeCon, Momentive, DhakeIndustries, Duralar Technologies, Voestalpine Eifeler Group*List Not Exhaustive, Ultra Optics, IHI Hauzer BV, Carl Zeiss AG, ASB Industries Inc, Platit AG, Exxene Corporation, SDC Technologies Inc, Gencoa Ltd.

3. What are the main segments of the Hard Coating Industry?

The market segments include Material Type, Technique, Application, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 2023 million as of 2022.

5. What are some drivers contributing to market growth?

; Rapidly Growing Demand from Healthcare Sectors; Increasing Usage of Hard Coatings in Developing Nations.

6. What are the notable trends driving market growth?

Optics Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

; High Capital Requirement.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Hard Coating Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Hard Coating Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Hard Coating Industry?

To stay informed about further developments, trends, and reports in the Hard Coating Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence