Key Insights

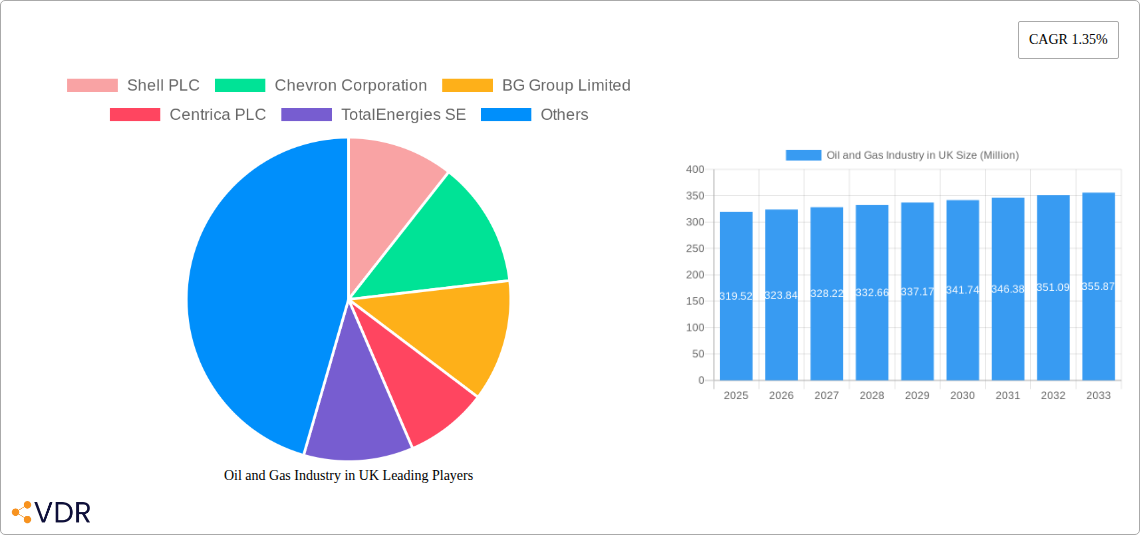

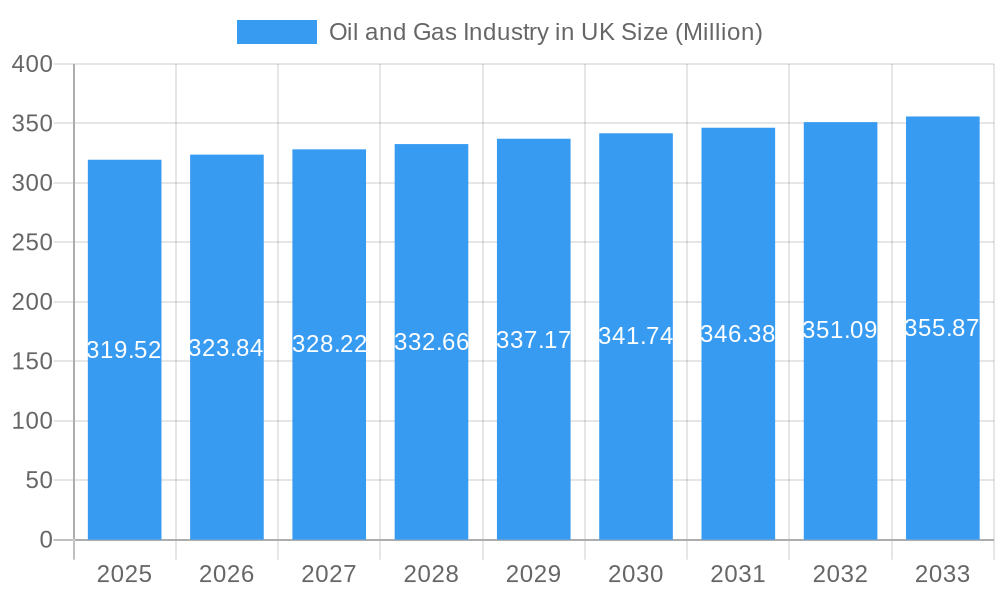

The UK oil and gas industry is poised for a period of moderate but consistent growth, projected to reach approximately USD 319.52 million by 2025. This steady expansion is underpinned by a compound annual growth rate (CAGR) of 1.35%, indicating a stable market trajectory through to 2033. Key drivers for this growth are expected to stem from the ongoing demand for energy, particularly in the downstream sector for refined products, and the continued necessity of the upstream sector for domestic supply and strategic energy security. Technological advancements in extraction and processing, coupled with a strategic focus on optimizing existing infrastructure, will also play a crucial role in sustaining this growth. Furthermore, investments in decarbonization technologies within the traditional oil and gas framework, such as carbon capture and storage (CCS), are becoming increasingly important drivers, ensuring the industry's relevance in a shifting energy landscape. The midstream segment, encompassing transportation and storage, will benefit from increased production and refined product movement.

Oil and Gas Industry in UK Market Size (In Million)

Despite the overall positive outlook, the sector faces significant restraints. Foremost among these are the escalating regulatory pressures and a global drive towards renewable energy sources, which could temper long-term investment in fossil fuels. Volatility in global commodity prices, geopolitical instability, and the substantial capital expenditure required for exploration and production also present considerable challenges. However, the industry is demonstrating resilience by focusing on operational efficiency, cost optimization, and diversification into lower-carbon solutions. The strategic importance of the UK as a mature oil and gas producer within Europe, coupled with its established infrastructure and skilled workforce, provides a robust foundation. Major players like Shell PLC, Chevron Corporation, and TotalEnergies SE are actively navigating these complexities, investing in both traditional operations and emerging energy technologies to secure their future market positions within Europe and beyond.

Oil and Gas Industry in UK Company Market Share

This in-depth report provides a definitive analysis of the United Kingdom's oil and gas sector, covering market dynamics, growth trends, regional dominance, product landscapes, key drivers, challenges, emerging opportunities, and the strategic initiatives of leading industry players. Leveraging proprietary data and expert insights, this study offers unparalleled value for stakeholders seeking to navigate this vital industry.

Oil and Gas Industry in UK Market Dynamics & Structure

The UK oil and gas industry is characterized by a moderately concentrated market, with major players like Shell PLC and BP PLC holding significant influence, particularly in the Upstream and Downstream segments. Technological innovation, driven by the imperative for enhanced efficiency and reduced environmental impact, is a key differentiator. AI-powered exploration and production technologies, as exemplified by Shell PLC's collaboration with SparkCognition in May 2023, are rapidly gaining traction. The regulatory framework, while evolving to promote sustainability, presents both opportunities and challenges. Competitive product substitutes, primarily from renewable energy sources, are increasingly impacting market share, necessitating strategic adaptation. End-user demographics are shifting, with growing demand for cleaner energy solutions influencing investment priorities. Mergers and acquisitions (M&A) trends continue to shape the competitive landscape, with ongoing consolidation and strategic divestitures. The estimated M&A deal volume for the historical period (2019-2024) stands at approximately $8,500 million, reflecting significant industry restructuring. Barriers to innovation include the substantial capital investment required for new technologies and the inherent risks associated with offshore exploration.

- Market Concentration: Dominated by a few large, integrated energy companies.

- Technological Innovation: Focus on AI, automation, and decarbonization technologies.

- Regulatory Framework: Evolving policies towards net-zero emissions and energy security.

- Competitive Substitutes: Growing influence of renewable energy sources.

- End-User Demographics: Shifting preferences towards sustainable energy solutions.

- M&A Trends: Consolidation and strategic partnerships driving market restructuring.

Oil and Gas Industry in UK Growth Trends & Insights

The UK oil and gas industry has experienced dynamic growth and transformation over the historical period (2019-2024), with an estimated market size of $65,000 million in 2024. The forecast period (2025-2033) projects a Compound Annual Growth Rate (CAGR) of approximately 2.5%, reaching an estimated market size of $79,000 million by 2033. This growth is underpinned by robust domestic production, particularly from the North Sea, and the continued demand for oil and gas in various industrial and energy applications. Adoption rates of advanced exploration and extraction technologies are accelerating, driven by the need to maximize recovery from mature fields and enhance operational efficiency. Technological disruptions, such as the integration of big data analytics and artificial intelligence, are revolutionizing exploration, production, and refining processes, leading to significant cost reductions and improved safety standards. Consumer behavior shifts, influenced by increasing environmental awareness and the drive towards decarbonization, are creating demand for lower-carbon intensity fuels and integrated energy solutions, compelling companies to diversify their portfolios. The market penetration of conventional oil and gas is being challenged by renewable energy but remains crucial for energy security during the transition.

Dominant Regions, Countries, or Segments in Oil and Gas Industry in UK

The Upstream sector is the dominant force driving growth within the UK oil and gas industry. This segment, encompassing the exploration and production of crude oil and natural gas, accounts for approximately 55% of the total market value. The North Sea, specifically, is the primary hub for upstream activities, benefiting from established infrastructure, a skilled workforce, and significant proven reserves. Economic policies aimed at bolstering domestic energy security and incentivizing investment in mature fields, such as those implemented by the UK government, are key drivers of growth in this region. Infrastructure development, including offshore platforms, pipelines, and processing facilities, has been a cornerstone of upstream operations for decades, ensuring efficient extraction and transportation of hydrocarbons. The market share of the upstream segment is projected to remain strong throughout the forecast period, though its growth rate will be influenced by global energy prices and the pace of the energy transition.

- Upstream Sector Dominance: Responsible for the majority of market value creation.

- North Sea as a Hub: Continual exploration and production activities drive regional growth.

- Key Drivers:

- Economic Policies: Government incentives for domestic production and energy security.

- Infrastructure: Established offshore platforms, pipelines, and processing facilities.

- Technological Advancements: Enhanced oil recovery techniques and digital solutions.

- Skilled Workforce: Experienced personnel in offshore exploration and operations.

- Growth Potential: Sustained by mature field optimization and potential new discoveries.

Oil and Gas Industry in UK Product Landscape

The UK oil and gas industry's product landscape is dominated by refined petroleum products, including gasoline, diesel, jet fuel, and heating oil, serving critical transportation and industrial needs. The upstream segment yields crude oil and natural gas, which are the primary feedstocks for the downstream refining and petrochemical sectors. Innovations are increasingly focused on improving the efficiency and environmental performance of existing products, such as the development of low-sulfur fuels and cleaner burning natural gas. Technological advancements in extraction and refining processes are leading to higher yields and reduced energy consumption. The unique selling proposition of traditional oil and gas products lies in their established infrastructure and high energy density, though this is increasingly being challenged by the rise of lower-carbon alternatives.

Key Drivers, Barriers & Challenges in Oil and Gas Industry in UK

Key Drivers:

- Energy Security Imperative: The ongoing global geopolitical landscape highlights the critical need for stable domestic energy supply.

- Technological Advancements: AI, big data, and automation are improving efficiency and reducing operational costs.

- Economic Recovery: Continued industrial activity and consumer demand for energy services.

- Investment in Mature Fields: Strategic investments to maximize output from existing reserves.

Barriers & Challenges:

- Decarbonization Pressures: Increasing regulatory and societal demands for reduced carbon emissions.

- Volatile Global Energy Prices: Fluctuations in oil and gas prices impact profitability and investment decisions.

- Supply Chain Disruptions: Geopolitical events and global logistics challenges can affect the availability of materials and equipment.

- Aging Infrastructure: The need for significant investment in maintaining and upgrading existing facilities.

- Competition from Renewables: Growing market share of renewable energy sources, impacting long-term demand for fossil fuels.

Emerging Opportunities in Oil and Gas Industry in UK

Emerging opportunities in the UK oil and gas sector lie in the transition to lower-carbon energy solutions. This includes the development and deployment of carbon capture, utilization, and storage (CCUS) technologies to decarbonize existing operations and industrial processes. The production of blue hydrogen, derived from natural gas with CCUS, presents a significant opportunity to leverage existing gas infrastructure for a cleaner fuel source. Furthermore, the industry can explore opportunities in the integration of offshore wind power with oil and gas platforms for offshore electrification, reducing operational emissions. Untapped markets for natural gas as a transition fuel, particularly in industrial sectors seeking to move away from coal, also represent a promising avenue.

Growth Accelerators in the Oil and Gas Industry in UK Industry

Long-term growth in the UK oil and gas industry will be significantly accelerated by continued investment in technological innovation for both conventional and emerging energy solutions. Strategic partnerships between oil and gas majors and technology providers, such as the collaboration between Shell PLC and SparkCognition, are crucial for unlocking efficiency gains and developing advanced solutions. Market expansion strategies that focus on integrated energy services, including renewable energy alongside traditional offerings, will be vital for sustained revenue streams. Furthermore, government support through tax incentives and regulatory frameworks that facilitate the development of CCUS and hydrogen production will act as significant catalysts for growth.

Key Players Shaping the Oil and Gas Industry in UK Market

- Shell PLC

- Chevron Corporation

- BG Group Limited

- Centrica PLC

- TotalEnergies SE

- Cadent Gas Ltd

- BP PLC

- ESSO UK Limited

- Valaris PLC

- Dana Petroleum E&P Limited

Notable Milestones in Oil and Gas Industry in UK Sector

- May 2023: Shell PLC and big-data analytics company SparkCognition announced their collaboration, stating that Shell will leverage artificial intelligence-based technology to enhance offshore oil exploration and production in deep-sea exploration and production.

- May 2022: BP PLC announced that they are going to invest USD 22.5 billion in the oil and gas fields located in the North Sea by the end of 2030 to ramp up production activities in the region with decreased emissions. This will help the United Kingdom boost its energy security and sustainably meet its increased energy demands.

In-Depth Oil and Gas Industry in UK Market Outlook

The future market potential of the UK oil and gas industry is intricately linked to its ability to adapt to the global energy transition. Strategic opportunities lie in becoming a leader in low-carbon solutions such as carbon capture and hydrogen production, leveraging existing infrastructure and expertise. Continued investment in mature North Sea fields, coupled with the adoption of advanced digital technologies, will ensure continued, albeit evolving, output. The industry's role in maintaining energy security during this transition remains paramount, creating a demand for reliable energy sources. Stakeholders who embrace innovation and diversification will be best positioned for sustained success.

Oil and Gas Industry in UK Segmentation

-

1. Sector

- 1.1. Upstream

- 1.2. Midstream

- 1.3. Downstream

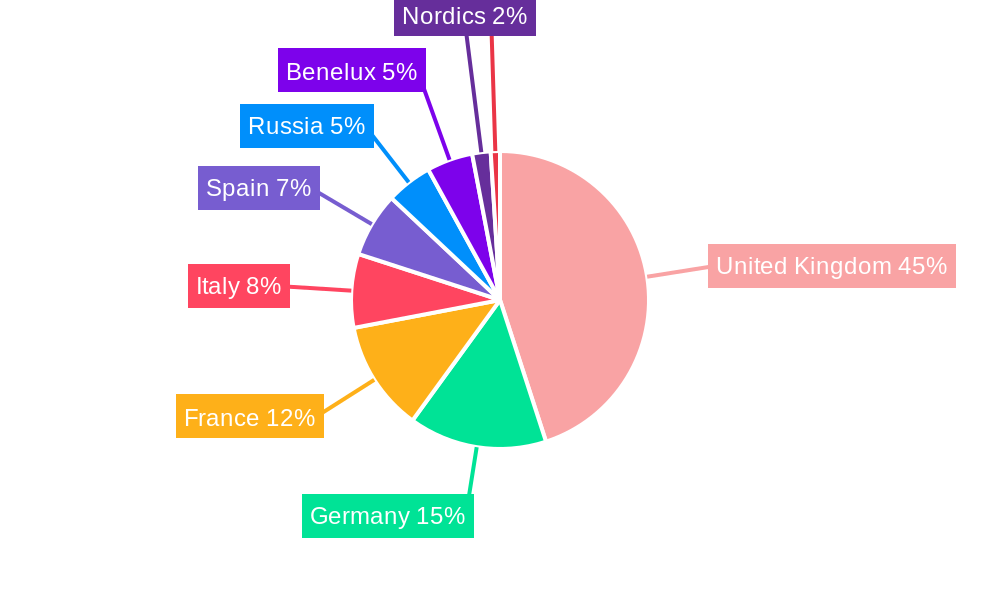

Oil and Gas Industry in UK Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Russia

- 1.7. Benelux

- 1.8. Nordics

- 1.9. Rest of Europe

Oil and Gas Industry in UK Regional Market Share

Geographic Coverage of Oil and Gas Industry in UK

Oil and Gas Industry in UK REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 1.35% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 5.1.1. Upstream

- 5.1.2. Midstream

- 5.1.3. Downstream

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 6. Oil and Gas Industry in UK Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 6.1.1. Upstream

- 6.1.2. Midstream

- 6.1.3. Downstream

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Shell PLC

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Chevron Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 BG Group Limited

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Centrica PLC

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 TotalEnergies SE

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Cadent Gas Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 BP PLC

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 ESSO UK Limited

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Valaris PLC

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Dana Petroleum E&P Limited

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Shell PLC

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Oil and Gas Industry in UK Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Oil and Gas Industry in UK Share (%) by Company 2025

List of Tables

- Table 1: Oil and Gas Industry in UK Revenue Million Forecast, by Sector 2020 & 2033

- Table 2: Oil and Gas Industry in UK Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Oil and Gas Industry in UK Revenue Million Forecast, by Sector 2020 & 2033

- Table 4: Oil and Gas Industry in UK Revenue Million Forecast, by Country 2020 & 2033

- Table 5: United Kingdom Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2020 & 2033

- Table 6: Germany Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2020 & 2033

- Table 7: France Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Italy Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Spain Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Russia Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Benelux Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Nordics Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Rest of Europe Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Oil and Gas Industry in UK?

The projected CAGR is approximately 1.35%.

2. Which companies are prominent players in the Oil and Gas Industry in UK?

Key companies in the market include Shell PLC, Chevron Corporation, BG Group Limited, Centrica PLC, TotalEnergies SE, Cadent Gas Ltd, BP PLC, ESSO UK Limited, Valaris PLC, Dana Petroleum E&P Limited.

3. What are the main segments of the Oil and Gas Industry in UK?

The market segments include Sector.

4. Can you provide details about the market size?

The market size is estimated to be USD 319.52 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Domestic Oil and Gas Production4.; Investments in Oil and Gas Infrastructure Development.

6. What are the notable trends driving market growth?

Upstream Segment Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Growth of Renewable Energy.

8. Can you provide examples of recent developments in the market?

May 2023: Shell PLC, a major oil and gas company from the United Kingdom, and big-data analytics company SparkCognition announced their collaboration, stating that Shell will leverage artificial intelligence-based technology to enhance offshore oil exploration and production in deep-sea exploration and production.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Oil and Gas Industry in UK," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Oil and Gas Industry in UK report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Oil and Gas Industry in UK?

To stay informed about further developments, trends, and reports in the Oil and Gas Industry in UK, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence