Key Insights

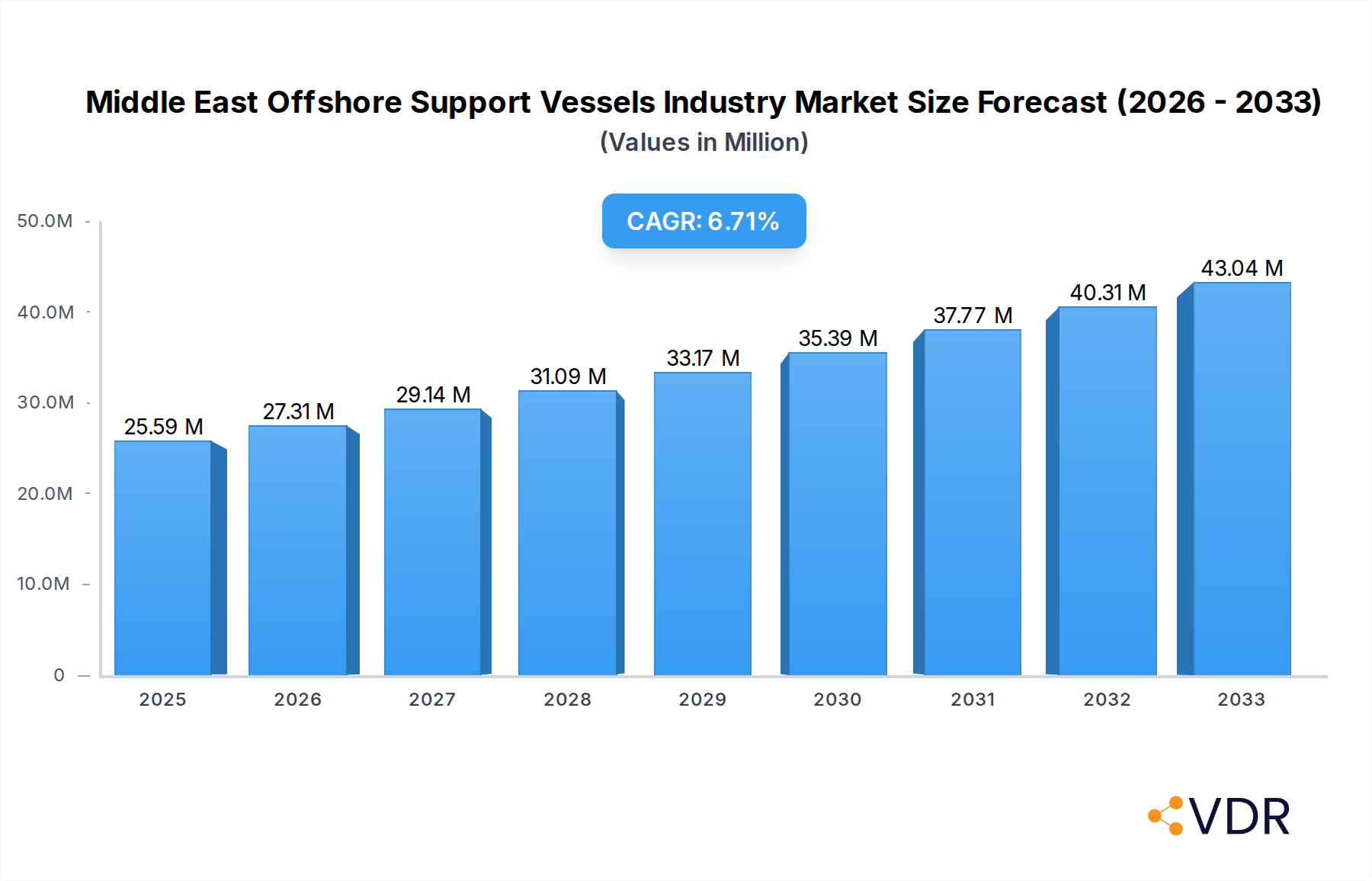

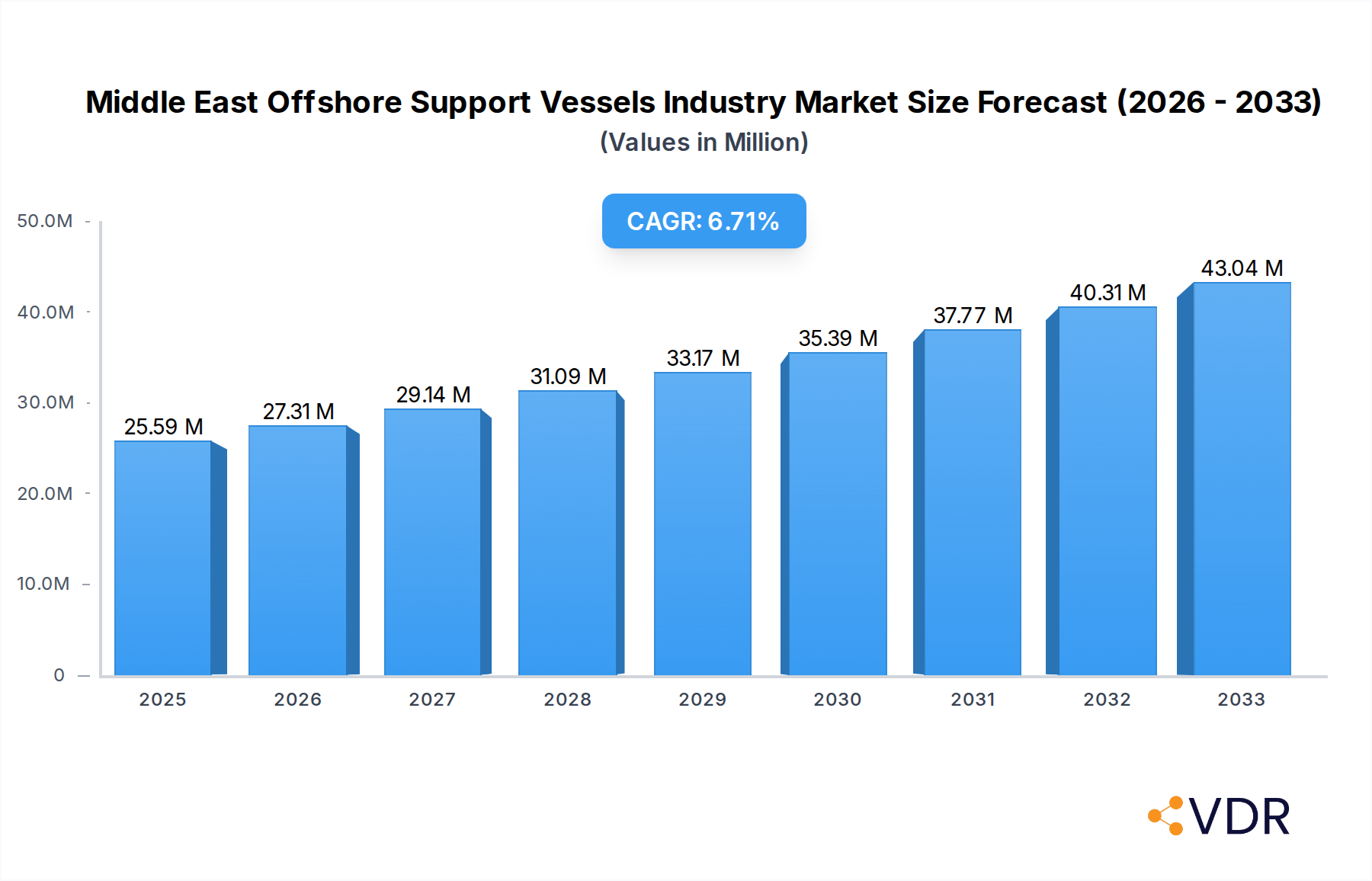

The Middle East Offshore Support Vessels (OSVs) industry is poised for significant expansion, projected to reach a robust USD 25.59 million by 2025, driven by a healthy compound annual growth rate (CAGR) of 6.50%. This growth trajectory is underpinned by substantial investments in oil and gas exploration and production activities across the region. Key drivers include the increasing demand for energy, particularly from emerging economies, and the ongoing development of new offshore fields. Furthermore, the growing emphasis on enhanced oil recovery (EOR) techniques necessitates a larger and more sophisticated fleet of OSVs to support these complex operations. The market segmentation reveals a strong demand for Platform Supply Vessels (PSVs), which are crucial for transporting essential supplies and equipment to offshore installations. Other vessel types, including Anchor Handling Tugs, also play vital roles in maintaining operational efficiency and safety. Geographically, Saudi Arabia, the United Arab Emirates, and Qatar are expected to lead this market expansion, owing to their extensive offshore infrastructure and ambitious production targets.

Middle East Offshore Support Vessels Industry Market Size (In Million)

While the market exhibits strong growth potential, certain restraints could influence its pace. These include the fluctuating prices of crude oil, which can impact upstream investment decisions and subsequently the demand for OSVs. Additionally, increasingly stringent environmental regulations and the rising adoption of renewable energy sources could pose long-term challenges, prompting a shift in investment focus. However, the strategic importance of offshore resources for Middle Eastern economies, coupled with advancements in OSV technology and operational efficiency, are expected to mitigate these restraints. The competitive landscape features prominent players such as Maersk AS, Tidewater Inc., and Seacor Marine Holdings Inc., alongside national oil companies like Abu Dhabi National Oil Company (ADNOC), all vying for market share through fleet modernization, service diversification, and strategic partnerships. The forecast period from 2025 to 2033 indicates sustained growth, with an estimated market value of approximately USD 41.57 million by 2033, reflecting the continued reliance on offshore energy resources in the Middle East.

Middle East Offshore Support Vessels Industry Company Market Share

Middle East Offshore Support Vessels Industry Report: Market Analysis, Trends, and Forecast (2019–2033)

This comprehensive report provides an in-depth analysis of the Middle East Offshore Support Vessels (OSVs) industry, covering market dynamics, growth trends, regional dominance, product landscape, key drivers, challenges, opportunities, and key players. With a study period spanning from 2019 to 2033, including a base year of 2025 and a forecast period from 2025 to 2033, this report offers valuable insights for stakeholders seeking to understand and capitalize on this rapidly evolving sector. We meticulously analyze parent and child markets, integrating high-traffic keywords such as "offshore support vessels," "OSVs," "maritime offshore," "oil and gas logistics," "vessel chartering," and "offshore construction," to maximize SEO visibility and engage industry professionals. All monetary values are presented in millions of units.

Middle East Offshore Support Vessels Industry Market Dynamics & Structure

The Middle East Offshore Support Vessels (OSVs) market is characterized by a moderately concentrated structure, with a few major international and regional players dominating the landscape. Technological innovation is primarily driven by the demand for advanced, fuel-efficient, and environmentally compliant vessels, alongside specialized equipment for complex offshore operations. Regulatory frameworks are increasingly focusing on safety, environmental protection, and local content requirements, influencing operational strategies and investment decisions. Competitive product substitutes are limited within the core OSV segment, but alternative service providers and innovative project execution methods can pose indirect competition. End-user demographics are primarily driven by national oil companies (NOCs) and international oil companies (IOCs) involved in offshore exploration and production. Mergers and acquisitions (M&A) are a significant trend, consolidating market share and expanding service portfolios.

- Market Concentration: Dominated by key players like Maersk AS, Offshore International (OFCO), and Tidewater Inc., with regional entities like Abu Dhabi National Oil Company (ADNOC) significantly influencing the market.

- Technological Innovation: Focus on hybrid propulsion, autonomous operations, and advanced subsea intervention capabilities.

- Regulatory Frameworks: Stringent HSE regulations and increasing emphasis on local content policies by GCC nations.

- M&A Trends: Significant consolidation observed, exemplified by ADNOC L&S's acquisition of Zakher Marine International (ZMI).

Middle East Offshore Support Vessels Industry Growth Trends & Insights

The Middle East Offshore Support Vessels (OSVs) market is poised for robust growth, driven by escalating offshore oil and gas production activities and significant investments in infrastructure development across the region. The market size is projected to witness a substantial Compound Annual Growth Rate (CAGR) throughout the forecast period. Adoption rates for specialized OSVs, particularly those equipped for complex subsea operations and enhanced environmental performance, are on the rise. Technological disruptions are emerging in the form of digitalization, remote monitoring, and the integration of AI for operational efficiency and predictive maintenance. Shifts in consumer behavior, driven by a greater emphasis on sustainability and cost-effectiveness, are compelling OSV operators to invest in greener technologies and more efficient vessel designs. The expansion of offshore fields and the exploration of new frontiers further necessitate a growing fleet to support these activities.

The increasing demand for offshore exploration and production (E&P) activities in the Middle East is a primary catalyst for the sustained growth of the OSV market. National oil companies and international oil companies are intensifying their efforts to tap into the region's vast hydrocarbon reserves, requiring a continuous supply of specialized vessels for various offshore operations. This includes drilling support, platform supply, construction, and maintenance activities. The emphasis on deep-water exploration and the development of marginal fields are further contributing to the demand for advanced OSVs with greater capabilities.

Furthermore, the evolving energy landscape, with a growing focus on liquefied natural gas (LNG) and the ongoing energy transition, is also indirectly impacting the OSV market. While the demand for traditional oil and gas support remains strong, there is a discernible trend towards vessels that can also support offshore renewable energy projects, such as wind farms. This diversification of demand creates new avenues for growth and innovation within the OSV sector.

The adoption of advanced technologies is another significant growth driver. From AI-powered route optimization to the implementation of IoT devices for real-time vessel monitoring, the industry is embracing digitalization to enhance operational efficiency, reduce costs, and improve safety. This technological integration is not only transforming existing operations but also paving the way for new service offerings and business models.

Consumer behavior is also adapting. Clients are increasingly looking for integrated service providers that can offer a comprehensive suite of offshore solutions, rather than just vessel chartering. This trend is encouraging OSV operators to expand their service portfolios and forge strategic partnerships to offer end-to-end solutions. Moreover, a growing awareness of environmental concerns is pushing for more sustainable operations, leading to a preference for vessels with lower emissions and greater fuel efficiency.

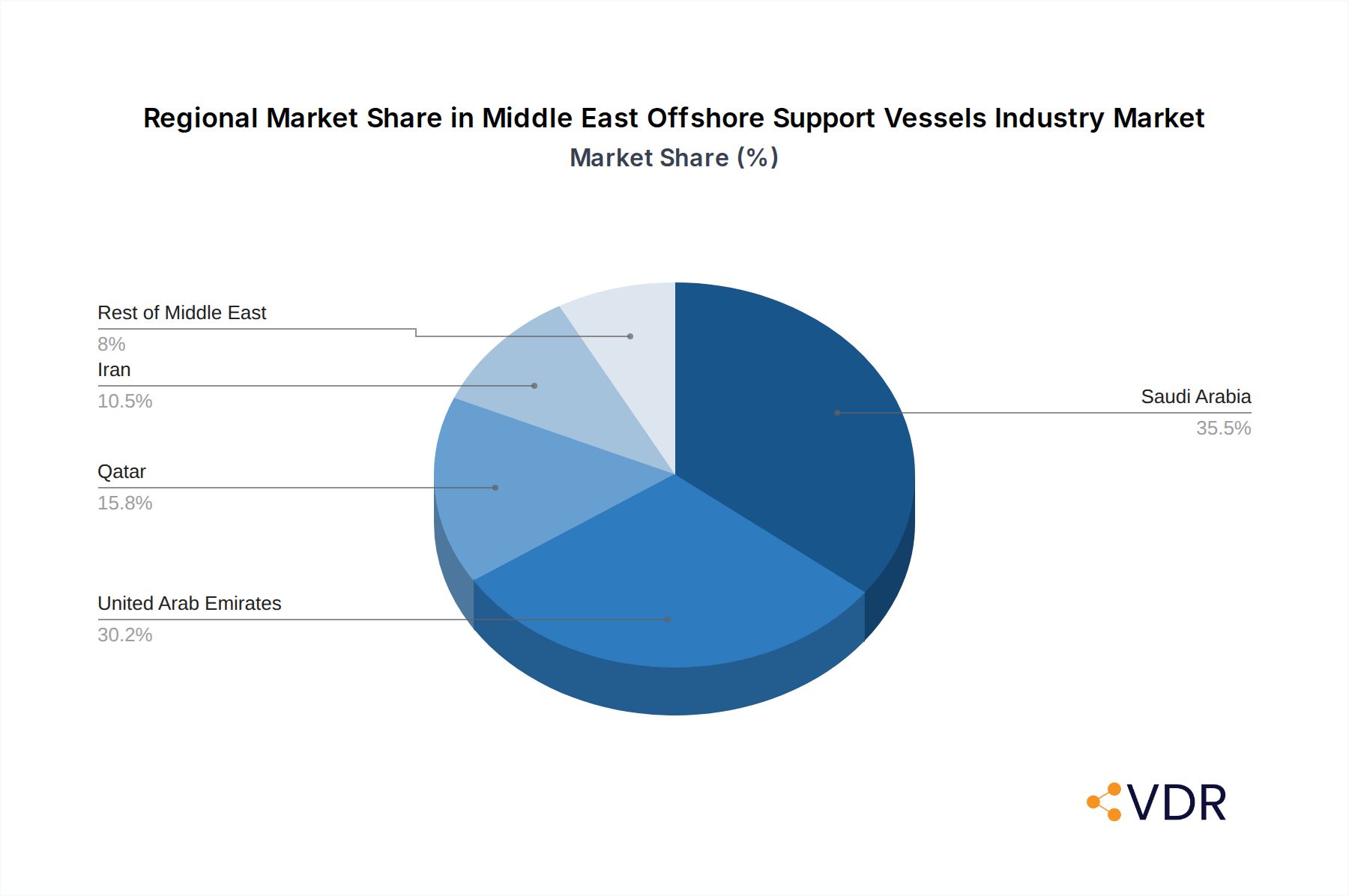

Dominant Regions, Countries, or Segments in Middle East Offshore Support Vessels Industry

The Middle East Offshore Support Vessels (OSVs) industry is overwhelmingly dominated by Saudi Arabia, driven by its colossal offshore oil and gas reserves and ambitious production enhancement plans. The country's proactive approach to expanding its offshore capabilities, particularly in fields like Marjan, Berri, and Safaniya, directly translates into substantial demand for a diverse range of OSVs. Economic policies, massive capital investments by national oil companies, and extensive infrastructure development projects further solidify Saudi Arabia's leading position. The sheer scale of its offshore operations, coupled with ongoing and planned expansions, ensures a consistent and significant requirement for various vessel types.

- Saudi Arabia: Holds the largest market share due to its extensive offshore oil fields and government-backed production enhancement initiatives.

- Key Drivers: Expansion of Marjan, Berri, and Safaniya fields; increased offshore construction activities; government focus on boosting oil production capacity.

- Market Share: Expected to account for over xx% of the regional OSV market by 2025.

- Growth Potential: High, driven by long-term production targets and ongoing project pipelines.

The United Arab Emirates (UAE), particularly Abu Dhabi, stands as another pivotal market, characterized by its strategic acquisitions and substantial fleet expansion. ADNOC's aggressive growth strategy, including the acquisition of Zakher Marine International (ZMI), underscores the UAE's commitment to strengthening its offshore support capabilities. The country's diversified offshore portfolio, encompassing both oil and gas and burgeoning renewable energy projects, contributes to a steady demand for a wide array of OSVs.

- United Arab Emirates: A significant market player with a strong focus on fleet modernization and expansion, especially driven by ADNOC.

- Key Drivers: ADNOC's strategic acquisitions; expansion of offshore oil and gas fields; growing interest in offshore wind energy projects.

- Market Share: Estimated to hold around xx% of the regional market by 2025.

Qatar remains a crucial contributor, primarily driven by its extensive liquefied natural gas (LNG) export infrastructure and ongoing expansions of its North Field. The sheer volume of LNG production necessitates continuous support from OSVs for platform maintenance, supply logistics, and specialized maritime services.

- Qatar: Driven by its world-leading LNG production and ongoing North Field expansion projects.

- Key Drivers: North Field East and North Field South expansion projects; consistent demand for LNG transportation and support vessels.

Iran, despite geopolitical complexities, possesses significant offshore hydrocarbon potential, contributing to a notable segment of the OSV market, primarily focused on its domestic production needs. The Rest of the Middle East region, encompassing countries like Kuwait and Oman, also contributes to the overall market demand, albeit with smaller individual shares.

The segment of Platform Supply Vessels (PSVs) represents a dominant category within the Middle East OSV market, essential for transporting vital supplies, equipment, and personnel to offshore platforms. However, Other Types, including specialized vessels like Anchor Handling Tug Supply (AHTS) vessels, offshore construction vessels (OSCVs), and dive support vessels (DSVs), are experiencing robust growth due to the increasing complexity of offshore projects and the trend towards deeper water exploration.

Middle East Offshore Support Vessels Industry Product Landscape

The product landscape of the Middle East Offshore Support Vessels (OSVs) industry is increasingly defined by specialized, high-performance vessels designed for the demanding offshore environment. Innovations focus on enhancing fuel efficiency through hybrid propulsion systems and advanced hull designs, reducing operational costs and environmental impact. Applications range from routine supply runs and crew transfers to complex subsea construction, inspection, maintenance, and repair (IMR) operations. Performance metrics such as bollard pull, deck cargo capacity, and maneuverability are critical differentiators, especially for Anchor Handling Tug Supply (AHTS) and Platform Supply Vessels (PSVs). The trend is towards more technologically advanced vessels equipped with dynamic positioning systems, advanced navigation, and enhanced safety features to meet the evolving needs of offshore exploration and production.

Key Drivers, Barriers & Challenges in Middle East Offshore Support Vessels Industry

Key Drivers:

- Escalating Offshore Oil & Gas Production: Sustained demand from national and international oil companies to meet global energy needs.

- Infrastructure Development: Significant investments in new offshore platforms, pipelines, and subsea infrastructure.

- Technological Advancements: Adoption of more efficient, environmentally friendly, and specialized vessels.

- Government Support & Policies: Favorable regulatory environments and local content initiatives promoting domestic industry growth.

Barriers & Challenges:

- Volatile Oil Prices: Fluctuations in crude oil prices can impact exploration and production budgets, indirectly affecting OSV demand.

- Geopolitical Instability: Regional political tensions can lead to project delays and operational disruptions.

- High Capital Investment: Acquiring and maintaining a modern OSV fleet requires substantial capital expenditure.

- Skilled Workforce Shortage: A persistent challenge in attracting and retaining qualified maritime personnel.

- Environmental Regulations: Increasing stringency of environmental regulations necessitates continuous investment in compliance and new technologies.

Emerging Opportunities in Middle East Offshore Support Vessels Industry

Emerging opportunities in the Middle East Offshore Support Vessels (OSVs) industry are driven by the growing emphasis on renewable energy integration and the exploration of deeper offshore reserves. The development of offshore wind farms presents a significant new avenue for OSV operators, requiring specialized vessels for construction, installation, and maintenance. Furthermore, the increasing complexity of offshore oil and gas projects, particularly in deeper waters, fuels demand for advanced subsea construction vessels (OSCVs) and remotely operated vehicles (ROVs). The adoption of digitalization and automation technologies offers opportunities for enhanced operational efficiency and new service models, such as remote fleet management and predictive maintenance.

Growth Accelerators in the Middle East Offshore Support Vessels Industry Industry

Long-term growth in the Middle East Offshore Support Vessels (OSVs) industry is being significantly accelerated by strategic partnerships and joint ventures between international OSV operators and local entities. These collaborations facilitate knowledge transfer, access to local markets, and compliance with local content requirements. Technological breakthroughs, particularly in areas like autonomous vessel operation, advanced subsea robotics, and the integration of green propulsion systems, are poised to drive efficiency and sustainability, attracting further investment. Market expansion strategies, including diversification into renewable energy support services and the development of integrated offshore logistics solutions, are also key accelerators.

Key Players Shaping the Middle East Offshore Support Vessels Industry Market

- Maersk AS

- Offshore International (OFCO)

- Tidewater Inc

- Seacor Marine Holdings Inc

- Baltic Marine Services LLC

- Abu Dhabi National Oil Company (ADNOC)

- Bourbon Corporation SA

Notable Milestones in Middle East Offshore Support Vessels Industry Sector

- May 2023: Saudi Aramco announced plans to enhance Middle East oil field production capacity from 12 to 13 million barrels of oil per day (bopd) by 2027, with a significant portion from offshore sources, leading to increased demand for offshore construction and vessel augmentation.

- July 2022: ADNOC Logistics & Services (ADNOC L&S) acquired Zakher Marine International (ZMI), a major offshore support vessel operator, integrating 24 jack-up barges and 38 OSVs, potentially expanding its fleet to over 300 vessels.

- March 2022: Shuaa Capital acquired Allianz Marine and Logistics Services, a significant M&A event in the Middle East maritime offshore sector, highlighting market consolidation.

In-Depth Middle East Offshore Support Vessels Industry Market Outlook

The Middle East Offshore Support Vessels (OSVs) industry is set for sustained expansion, propelled by the region's unwavering commitment to oil and gas production and its increasing focus on renewable energy initiatives. Strategic investments in expanding offshore fields and developing new energy infrastructure will continue to fuel demand for a diverse fleet of OSVs. The ongoing trend towards digitalization and the adoption of advanced technologies will enhance operational efficiency and create opportunities for innovative service offerings. Furthermore, the growing demand for greener and more sustainable maritime solutions will drive the development and deployment of eco-friendly vessels. The consolidation of market players through strategic mergers and acquisitions is expected to continue, leading to more integrated and capable service providers. Opportunities lie in catering to the specialized needs of deep-water exploration, offshore wind farm construction, and the provision of comprehensive offshore logistics solutions. The market outlook is highly positive, with significant growth potential driven by both traditional and emerging energy sectors.

Middle East Offshore Support Vessels Industry Segmentation

-

1. Type

- 1.1. Anchor H

- 1.2. Platform Supply Vessels (PSV)

- 1.3. Other Types

-

2. Geography

- 2.1. Saudi Arabia

- 2.2. United Arab Emirates

- 2.3. Qatar

- 2.4. Iran

- 2.5. Rest of Middle East

Middle East Offshore Support Vessels Industry Segmentation By Geography

- 1. Saudi Arabia

- 2. United Arab Emirates

- 3. Qatar

- 4. Iran

- 5. Rest of Middle East

Middle East Offshore Support Vessels Industry Regional Market Share

Geographic Coverage of Middle East Offshore Support Vessels Industry

Middle East Offshore Support Vessels Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.50% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Anchor H

- 5.1.2. Platform Supply Vessels (PSV)

- 5.1.3. Other Types

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. Saudi Arabia

- 5.2.2. United Arab Emirates

- 5.2.3. Qatar

- 5.2.4. Iran

- 5.2.5. Rest of Middle East

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Saudi Arabia

- 5.3.2. United Arab Emirates

- 5.3.3. Qatar

- 5.3.4. Iran

- 5.3.5. Rest of Middle East

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Middle East Offshore Support Vessels Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Anchor H

- 6.1.2. Platform Supply Vessels (PSV)

- 6.1.3. Other Types

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. Saudi Arabia

- 6.2.2. United Arab Emirates

- 6.2.3. Qatar

- 6.2.4. Iran

- 6.2.5. Rest of Middle East

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Saudi Arabia Middle East Offshore Support Vessels Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Anchor H

- 7.1.2. Platform Supply Vessels (PSV)

- 7.1.3. Other Types

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. Saudi Arabia

- 7.2.2. United Arab Emirates

- 7.2.3. Qatar

- 7.2.4. Iran

- 7.2.5. Rest of Middle East

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. United Arab Emirates Middle East Offshore Support Vessels Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Anchor H

- 8.1.2. Platform Supply Vessels (PSV)

- 8.1.3. Other Types

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. Saudi Arabia

- 8.2.2. United Arab Emirates

- 8.2.3. Qatar

- 8.2.4. Iran

- 8.2.5. Rest of Middle East

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Qatar Middle East Offshore Support Vessels Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Anchor H

- 9.1.2. Platform Supply Vessels (PSV)

- 9.1.3. Other Types

- 9.2. Market Analysis, Insights and Forecast - by Geography

- 9.2.1. Saudi Arabia

- 9.2.2. United Arab Emirates

- 9.2.3. Qatar

- 9.2.4. Iran

- 9.2.5. Rest of Middle East

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Iran Middle East Offshore Support Vessels Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Anchor H

- 10.1.2. Platform Supply Vessels (PSV)

- 10.1.3. Other Types

- 10.2. Market Analysis, Insights and Forecast - by Geography

- 10.2.1. Saudi Arabia

- 10.2.2. United Arab Emirates

- 10.2.3. Qatar

- 10.2.4. Iran

- 10.2.5. Rest of Middle East

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Rest of Middle East Middle East Offshore Support Vessels Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Anchor H

- 11.1.2. Platform Supply Vessels (PSV)

- 11.1.3. Other Types

- 11.2. Market Analysis, Insights and Forecast - by Geography

- 11.2.1. Saudi Arabia

- 11.2.2. United Arab Emirates

- 11.2.3. Qatar

- 11.2.4. Iran

- 11.2.5. Rest of Middle East

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Maersk AS

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Offshore International (OFCO)

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Tidewater Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Seacor Marine Holdings Inc *List Not Exhaustive

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Baltic Marine Services LLC

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Abu Dhabi National Oil Company (ADNOC)

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Bourbon Corporation SA

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.1 Maersk AS

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Middle East Offshore Support Vessels Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Middle East Offshore Support Vessels Industry Share (%) by Company 2025

List of Tables

- Table 1: Middle East Offshore Support Vessels Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Middle East Offshore Support Vessels Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 3: Middle East Offshore Support Vessels Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Middle East Offshore Support Vessels Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Middle East Offshore Support Vessels Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 6: Middle East Offshore Support Vessels Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Middle East Offshore Support Vessels Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 8: Middle East Offshore Support Vessels Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 9: Middle East Offshore Support Vessels Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Middle East Offshore Support Vessels Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 11: Middle East Offshore Support Vessels Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 12: Middle East Offshore Support Vessels Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Middle East Offshore Support Vessels Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 14: Middle East Offshore Support Vessels Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 15: Middle East Offshore Support Vessels Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Middle East Offshore Support Vessels Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 17: Middle East Offshore Support Vessels Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 18: Middle East Offshore Support Vessels Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle East Offshore Support Vessels Industry?

The projected CAGR is approximately 6.50%.

2. Which companies are prominent players in the Middle East Offshore Support Vessels Industry?

Key companies in the market include Maersk AS, Offshore International (OFCO), Tidewater Inc, Seacor Marine Holdings Inc *List Not Exhaustive, Baltic Marine Services LLC, Abu Dhabi National Oil Company (ADNOC), Bourbon Corporation SA.

3. What are the main segments of the Middle East Offshore Support Vessels Industry?

The market segments include Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 25.59 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Offshore Exploration and Production Activities4.; Development of Offshore Wind Energy.

6. What are the notable trends driving market growth?

Platform Supply Vessels (PSVs) are Likely to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Rising Demand for Dynamic Positioning (DP) Drilling Rigs.

8. Can you provide examples of recent developments in the market?

In May 2023, Saudi Aramco announced that by 2027, it plans to enhance the production capacity of the Middle East's oil fields from 12 million to 13 million barrels of oil per day (bopd). Notably, a significant portion of this increased production will come from offshore sources, including expanding fields like Marjan, Berri, and Safaniya. As a result, there will likely be considerable demand for offshore construction activities. Consequently, there may be a necessity to augment the fleet of various vessels, including jack-up barges, crew boats, platform supply boats, offshore subsea construction vessels (OSCVs), and offshore support vessels (OSVs). Thus, the fleet's expansion is underway to accommodate the anticipated requirements for offshore operations.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle East Offshore Support Vessels Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle East Offshore Support Vessels Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle East Offshore Support Vessels Industry?

To stay informed about further developments, trends, and reports in the Middle East Offshore Support Vessels Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence