Key Insights

The global mobile phone semiconductor market is poised for significant expansion, projected to reach a substantial market size of approximately $115 billion by 2025, with a robust Compound Annual Growth Rate (CAGR) of 7.49% anticipated to propel it through 2033. This impressive growth trajectory is primarily fueled by the relentless demand for advanced smartphone features, including AI-powered applications, high-resolution imaging, and enhanced connectivity through 5G and Wi-Fi 6/6E. The increasing sophistication of mobile processors, critical for seamless multitasking and immersive gaming experiences, along with the growing need for higher capacity and faster memory modules to support these functionalities, are key drivers. Furthermore, the proliferation of smart features in mid-range and budget smartphones, driven by fierce competition and consumer expectations, is democratizing access to sophisticated mobile technology, further bolstering market demand. The analog segment, vital for signal processing and power management, also experiences steady growth due to its indispensable role in every mobile device.

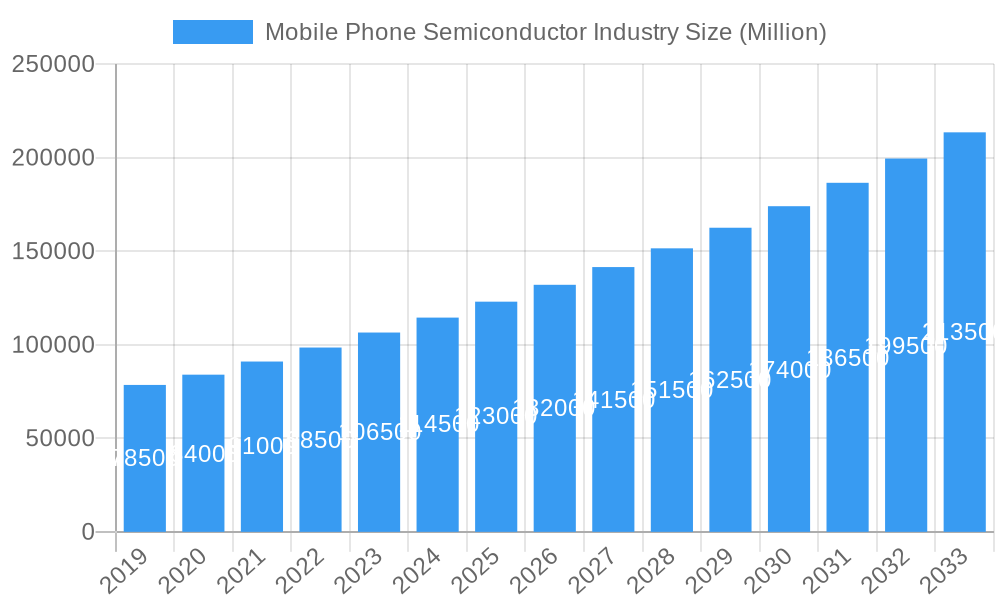

Mobile Phone Semiconductor Industry Market Size (In Billion)

The market is characterized by intense innovation and strategic collaborations among leading players like Samsung Electronics, Qualcomm Technologies Inc., and Intel Corporation. These companies are investing heavily in research and development to miniaturize components, improve power efficiency, and integrate more advanced functionalities into smaller form factors. However, the industry faces certain restraints, including the escalating cost of advanced manufacturing processes and the potential for supply chain disruptions, which could impact production volumes and pricing. Geographically, the Asia Pacific region is expected to maintain its dominant market share, driven by high smartphone penetration rates and manufacturing hubs. North America and Europe represent significant markets with a strong demand for premium devices and emerging technologies. The industry's ability to navigate geopolitical complexities, material sourcing challenges, and the constant race for technological superiority will be crucial in realizing its full growth potential over the forecast period.

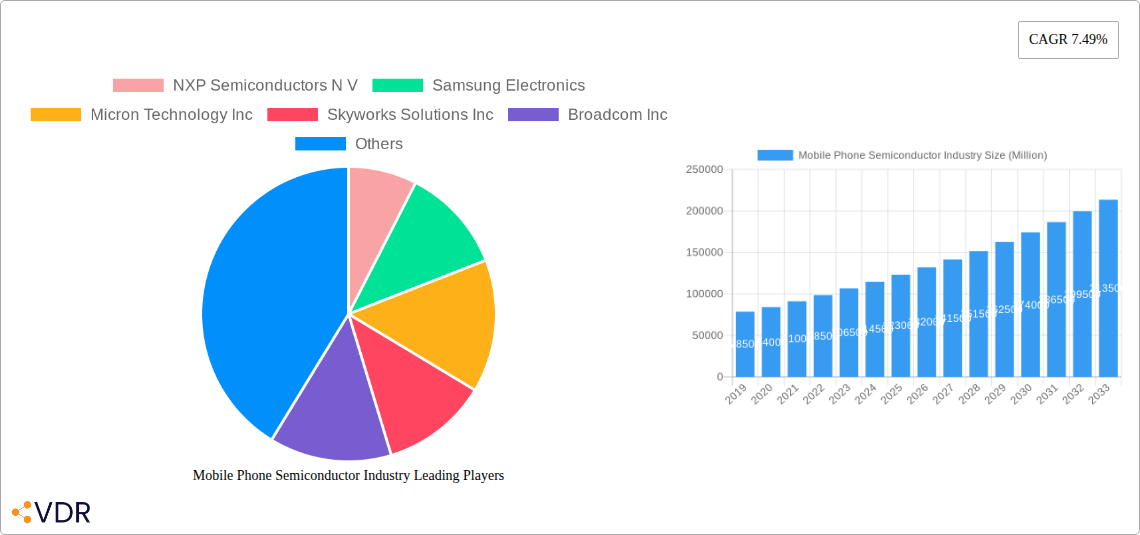

Mobile Phone Semiconductor Industry Company Market Share

This comprehensive report offers an in-depth analysis of the global Mobile Phone Semiconductor Industry, a critical and rapidly evolving sector. We delve into market dynamics, growth trajectories, regional dominance, product landscapes, key players, and future opportunities, providing actionable insights for industry stakeholders. Covering a study period from 2019 to 2033, with a base year of 2025, this report leverages extensive data and expert analysis to predict the market's evolution.

Mobile Phone Semiconductor Industry Market Dynamics & Structure

The mobile phone semiconductor industry is characterized by high market concentration, dominated by a few key players, with the parent market for semiconductors influencing its structure significantly. Technological innovation, particularly in areas like advanced process nodes and AI integration, serves as a primary driver, alongside evolving regulatory frameworks that impact manufacturing and trade. Competitive product substitutes, while less direct, include advancements in alternative device technologies that could reduce reliance on traditional mobile devices. End-user demographics, increasingly focused on premium features and extended device lifecycles, shape demand. Mergers and acquisitions (M&A) remain a constant, consolidating market share and driving innovation. For instance, the industry witnessed xx M&A deals in the historical period (2019-2024), with an estimated xx billion USD in transaction value. Barriers to innovation include the immense capital expenditure required for R&D and manufacturing, coupled with lengthy product development cycles.

- Market Concentration: Dominated by a few major integrated device manufacturers (IDMs) and fabless companies.

- Technological Innovation: Driven by Moore's Law, miniaturization, power efficiency, and the integration of AI accelerators.

- Regulatory Frameworks: Impacting supply chains, trade policies, and intellectual property rights.

- Competitive Substitutes: Emerging flexible displays and integrated wearable technologies can influence future demand.

- End-User Demographics: Shifting towards demand for advanced camera systems, 5G capabilities, and longer battery life.

- M&A Trends: Consolidation for economies of scale and strategic acquisition of critical technologies.

Mobile Phone Semiconductor Industry Growth Trends & Insights

The mobile phone semiconductor market is poised for robust growth, projected to expand from xx Million units in the historical period to xx Million units by 2033. This upward trajectory is fueled by increasing smartphone penetration in emerging economies, the continuous demand for upgraded features and performance, and the widespread adoption of 5G technology. The average selling price (ASP) of mobile semiconductors has seen a steady increase, driven by the incorporation of more sophisticated components like advanced processors, high-resolution image sensors, and enhanced memory modules. Technological disruptions, such as the development of novel materials and fabrication techniques, are set to redefine device capabilities, leading to the proliferation of foldable phones, advanced augmented reality (AR) applications, and more integrated Internet of Things (IoT) functionalities within smartphones. Consumer behavior shifts are evident in the growing preference for premium devices that offer superior performance, longer battery life, and advanced camera capabilities, directly impacting the demand for high-end mobile processors and memory chips. The CAGR for the forecast period (2025-2033) is estimated at xx%. Market penetration of advanced semiconductor technologies within smartphones is projected to reach xx% by 2033.

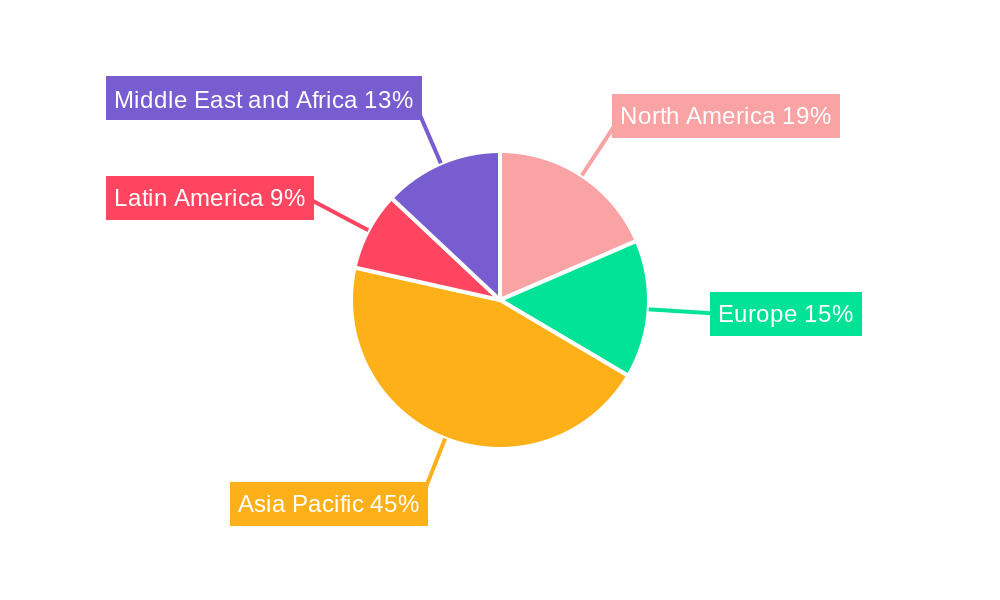

Dominant Regions, Countries, or Segments in Mobile Phone Semiconductor Industry

Asia Pacific currently stands as the dominant region in the mobile phone semiconductor industry, driven by its extensive manufacturing capabilities and the massive consumer base for smartphones. Countries like China, South Korea, and Taiwan are at the forefront of both semiconductor production and mobile device consumption. The Component Type: Mobile Processors segment, encompassing CPUs, GPUs, and NPUs, is a significant growth driver, witnessing a projected market size of xx Million units by 2033. This dominance is attributed to the increasing complexity of mobile applications, the demand for faster processing speeds, and the integration of AI capabilities for enhanced user experiences. Economic policies promoting domestic semiconductor manufacturing, coupled with substantial investments in R&D, have further bolstered the region's position. The infrastructure development in terms of advanced foundries and R&D centers is unparalleled, supporting the continuous innovation in this segment. South Korea, for instance, commands a significant market share in memory chips, a critical component for mobile devices. The growth potential in this segment is immense, driven by the ever-increasing demand for more powerful and efficient mobile processing units that can handle complex tasks like high-resolution video processing, advanced gaming, and seamless multitasking.

- Key Drivers in Asia Pacific:

- Government incentives for semiconductor manufacturing and R&D.

- Large and growing consumer market for smartphones.

- Presence of leading mobile device manufacturers.

- Advanced foundry and assembly infrastructure.

- Dominant Segment - Mobile Processors:

- Demand for high-performance CPUs and GPUs.

- Integration of Neural Processing Units (NPUs) for AI.

- Advancements in power efficiency.

- Market Share & Growth Potential: Asia Pacific holds an estimated xx% market share, with mobile processors expected to grow at a CAGR of xx% from 2025-2033.

Mobile Phone Semiconductor Industry Product Landscape

The product landscape of the mobile phone semiconductor industry is marked by relentless innovation in component design and functionality. Mobile processors are becoming increasingly powerful and energy-efficient, integrating dedicated AI cores to accelerate machine learning tasks. Memory chips are evolving towards higher densities and faster speeds, with advancements like LPDDR5X enabling smoother multitasking and quicker data access. Logic chips are crucial for managing complex device operations, with ongoing miniaturization driving performance improvements. Analog semiconductors are vital for signal processing, power management, and connectivity, with an emphasis on improved accuracy and reduced power consumption. The unique selling proposition of these components lies in their ability to enable the latest smartphone features, from advanced camera systems and immersive gaming experiences to seamless 5G connectivity and extended battery life.

Key Drivers, Barriers & Challenges in Mobile Phone Semiconductor Industry

Key Drivers: The mobile phone semiconductor industry is propelled by the insatiable demand for advanced smartphone features, the relentless pursuit of miniaturization and power efficiency, and the global rollout of 5G networks, which necessitates upgraded modem and RF front-end chips. Technological advancements in AI integration and quantum computing research also represent significant future drivers.

Barriers & Challenges: Significant challenges include the extremely high capital expenditure required for wafer fabrication facilities, leading to substantial barriers to entry. Geopolitical tensions and supply chain disruptions, as highlighted by global chip shortages, pose considerable risks. Intense competition among leading players, coupled with lengthy product development cycles and stringent regulatory compliance, further complicate the landscape. The cost of raw materials and the increasing complexity of manufacturing processes also contribute to these challenges.

Emerging Opportunities in Mobile Phone Semiconductor Industry

Emerging opportunities lie in the development of specialized semiconductors for foldable and flexible displays, catering to the growing demand for innovative form factors. The expansion of the Internet of Things (IoT) ecosystem, with smartphones acting as central control hubs, opens avenues for integrated connectivity solutions. Furthermore, advancements in neuromorphic computing and edge AI processing within mobile devices present significant potential for next-generation AI capabilities. The increasing focus on sustainability also creates opportunities for energy-efficient semiconductor designs and recycled materials in manufacturing.

Growth Accelerators in the Mobile Phone Semiconductor Industry Industry

Catalysts driving long-term growth include the continued evolution of 5G and the imminent rollout of 6G technologies, demanding more sophisticated RF components and baseband processors. Strategic partnerships between semiconductor manufacturers and smartphone brands are crucial for co-developing next-generation technologies. Market expansion strategies targeting untapped developing economies, coupled with the integration of advanced security features and biometric authentication, will further accelerate growth. The ongoing innovation in camera sensor technology and the demand for immersive augmented and virtual reality experiences on mobile devices also act as significant growth accelerators.

Key Players Shaping the Mobile Phone Semiconductor Industry Market

- NXP Semiconductors N V

- Samsung Electronics

- Micron Technology Inc

- Skyworks Solutions Inc

- Broadcom Inc

- Qorvo Inc

- Qualcomm Technologies Inc

- Huawei Technologies Co Ltd

- MediaTek Inc

- Intel Corporation

Notable Milestones in Mobile Phone Semiconductor Industry Sector

- November 2022: Micron Technology launched its 1-beta DRAM, aiming to improve power efficiency by 15% and bit density by 35% for memory chips, underpinning a new generation of memory for Micron.

- October 2022: Polymatech, a semiconductor chip manufacturer, initiated production of its Opto-semiconductors and memory modules, marking a significant part of its USD 1 billion investment in semiconductor chip manufacturing.

In-Depth Mobile Phone Semiconductor Industry Market Outlook

The mobile phone semiconductor industry is projected for substantial future growth, driven by the accelerating pace of technological innovation and evolving consumer demands. The increasing integration of AI, the expansion of 5G and future 6G networks, and the demand for more sophisticated mobile computing power will continue to fuel the market. Strategic investments in advanced manufacturing technologies, coupled with the development of specialized chips for emerging applications like foldable devices and AR/VR integration, will shape the future landscape. Opportunities in developing markets and the persistent need for enhanced device performance and energy efficiency present a robust outlook for continued expansion and innovation.

Mobile Phone Semiconductor Industry Segmentation

-

1. Component Type

- 1.1. Mobile Processors

- 1.2. Memory

- 1.3. Logic Chips

- 1.4. Analog

Mobile Phone Semiconductor Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Mobile Phone Semiconductor Industry Regional Market Share

Geographic Coverage of Mobile Phone Semiconductor Industry

Mobile Phone Semiconductor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.49% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component Type

- 5.1.1. Mobile Processors

- 5.1.2. Memory

- 5.1.3. Logic Chips

- 5.1.4. Analog

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Latin America

- 5.2.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Component Type

- 6. Global Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component Type

- 6.1.1. Mobile Processors

- 6.1.2. Memory

- 6.1.3. Logic Chips

- 6.1.4. Analog

- 6.1. Market Analysis, Insights and Forecast - by Component Type

- 7. North America Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Component Type

- 7.1.1. Mobile Processors

- 7.1.2. Memory

- 7.1.3. Logic Chips

- 7.1.4. Analog

- 7.1. Market Analysis, Insights and Forecast - by Component Type

- 8. Europe Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Component Type

- 8.1.1. Mobile Processors

- 8.1.2. Memory

- 8.1.3. Logic Chips

- 8.1.4. Analog

- 8.1. Market Analysis, Insights and Forecast - by Component Type

- 9. Asia Pacific Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Component Type

- 9.1.1. Mobile Processors

- 9.1.2. Memory

- 9.1.3. Logic Chips

- 9.1.4. Analog

- 9.1. Market Analysis, Insights and Forecast - by Component Type

- 10. Latin America Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Component Type

- 10.1.1. Mobile Processors

- 10.1.2. Memory

- 10.1.3. Logic Chips

- 10.1.4. Analog

- 10.1. Market Analysis, Insights and Forecast - by Component Type

- 11. Middle East and Africa Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Component Type

- 11.1.1. Mobile Processors

- 11.1.2. Memory

- 11.1.3. Logic Chips

- 11.1.4. Analog

- 11.1. Market Analysis, Insights and Forecast - by Component Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 NXP Semiconductors N V

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Samsung Electronics

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Micron Technology Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Skyworks Solutions Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Broadcom Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Qorvo Inc *List Not Exhaustive

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Qualcomm Technologies Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Huawei Technologies Co Ltd

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 MediaTek Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Intel Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 NXP Semiconductors N V

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Mobile Phone Semiconductor Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Mobile Phone Semiconductor Industry Revenue (Million), by Component Type 2025 & 2033

- Figure 3: North America Mobile Phone Semiconductor Industry Revenue Share (%), by Component Type 2025 & 2033

- Figure 4: North America Mobile Phone Semiconductor Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: North America Mobile Phone Semiconductor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Mobile Phone Semiconductor Industry Revenue (Million), by Component Type 2025 & 2033

- Figure 7: Europe Mobile Phone Semiconductor Industry Revenue Share (%), by Component Type 2025 & 2033

- Figure 8: Europe Mobile Phone Semiconductor Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: Europe Mobile Phone Semiconductor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Mobile Phone Semiconductor Industry Revenue (Million), by Component Type 2025 & 2033

- Figure 11: Asia Pacific Mobile Phone Semiconductor Industry Revenue Share (%), by Component Type 2025 & 2033

- Figure 12: Asia Pacific Mobile Phone Semiconductor Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Asia Pacific Mobile Phone Semiconductor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Latin America Mobile Phone Semiconductor Industry Revenue (Million), by Component Type 2025 & 2033

- Figure 15: Latin America Mobile Phone Semiconductor Industry Revenue Share (%), by Component Type 2025 & 2033

- Figure 16: Latin America Mobile Phone Semiconductor Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Latin America Mobile Phone Semiconductor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Middle East and Africa Mobile Phone Semiconductor Industry Revenue (Million), by Component Type 2025 & 2033

- Figure 19: Middle East and Africa Mobile Phone Semiconductor Industry Revenue Share (%), by Component Type 2025 & 2033

- Figure 20: Middle East and Africa Mobile Phone Semiconductor Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Middle East and Africa Mobile Phone Semiconductor Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Component Type 2020 & 2033

- Table 2: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Component Type 2020 & 2033

- Table 4: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Component Type 2020 & 2033

- Table 6: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Component Type 2020 & 2033

- Table 8: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Component Type 2020 & 2033

- Table 10: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Component Type 2020 & 2033

- Table 12: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Mobile Phone Semiconductor Industry?

The projected CAGR is approximately 7.49%.

2. Which companies are prominent players in the Mobile Phone Semiconductor Industry?

Key companies in the market include NXP Semiconductors N V, Samsung Electronics, Micron Technology Inc, Skyworks Solutions Inc, Broadcom Inc, Qorvo Inc *List Not Exhaustive, Qualcomm Technologies Inc, Huawei Technologies Co Ltd, MediaTek Inc, Intel Corporation.

3. What are the main segments of the Mobile Phone Semiconductor Industry?

The market segments include Component Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rapid Introduction of Next-generation Mobile-communications Standard. LTE or 4G; Emergence of 'Multicom' Solutions.

6. What are the notable trends driving market growth?

Memory to Significantly Drive the Market.

7. Are there any restraints impacting market growth?

Complexity Regarding Manufacturing; Consumer Demand Exceeding Factory Capacity.

8. Can you provide examples of recent developments in the market?

November 2022 - Micron Technology launched its 1-beta DRAM with an aim to improve power efficiency by 15% and bit density by 35% for memory chips. The new DRAM chips would underpin a new generation of memory chips for Micron.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Mobile Phone Semiconductor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Mobile Phone Semiconductor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Mobile Phone Semiconductor Industry?

To stay informed about further developments, trends, and reports in the Mobile Phone Semiconductor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence