Key Insights

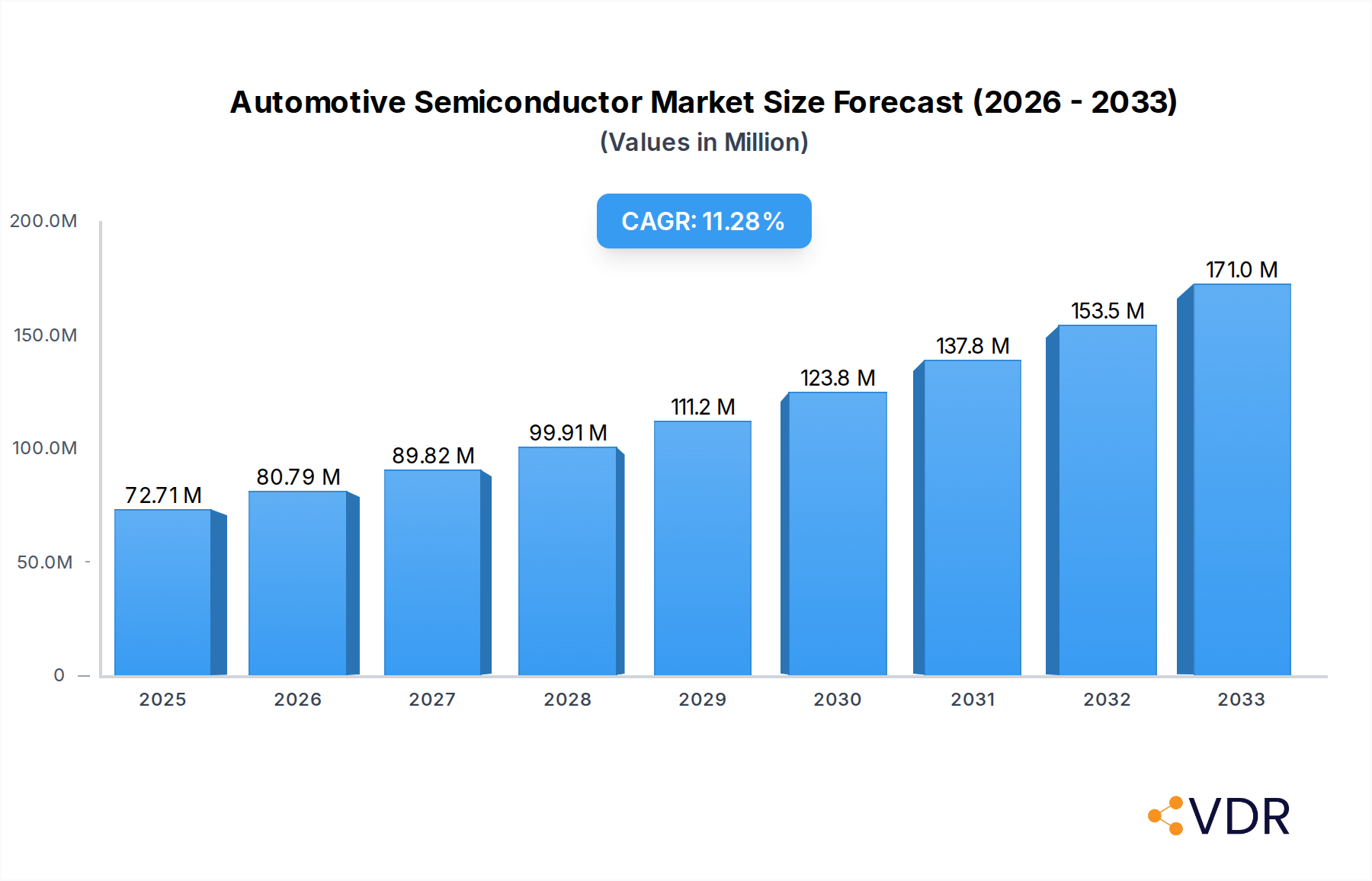

The global Automotive Semiconductor Market is experiencing robust expansion, projected to reach $72.71 Billion by 2025, with an impressive Compound Annual Growth Rate (CAGR) of 11.14% expected through 2033. This substantial growth is fueled by several interconnected drivers. The escalating demand for advanced driver-assistance systems (ADAS), in-car infotainment, and the burgeoning adoption of electric vehicles (EVs) are primary catalysts. Modern vehicles are increasingly reliant on sophisticated electronic components for everything from engine management and safety features like collision avoidance and lane-keeping assist, to advanced navigation, seamless connectivity, and personalized user experiences. Furthermore, stringent government regulations worldwide mandating improved safety and emissions standards are compelling automakers to integrate more advanced semiconductor technologies. The automotive industry's ongoing transformation, driven by innovation in autonomous driving and connected car technologies, continues to push the boundaries of semiconductor requirements.

Automotive Semiconductor Market Market Size (In Million)

Key trends shaping the Automotive Semiconductor Market include the miniaturization and increased power efficiency of components, the growing importance of AI and machine learning in vehicle functionalities, and the shift towards centralized computing architectures within vehicles. The market is also witnessing a surge in demand for specialized semiconductors such as processors for AI algorithms, advanced sensors for environmental perception, high-speed memory devices, and efficient power management ICs essential for EV powertrains. However, the market faces certain restraints, including the complexities of supply chain management for highly specialized components, the significant R&D investment required for cutting-edge technologies, and the evolving regulatory landscape. Despite these challenges, the market's trajectory remains overwhelmingly positive, driven by the relentless pursuit of safer, smarter, and more sustainable mobility solutions across all vehicle segments, from passenger cars to heavy commercial vehicles.

Automotive Semiconductor Market Company Market Share

Automotive Semiconductor Market Report: Driving Future Mobility with Advanced Chips

This comprehensive report delves into the Automotive Semiconductor Market, a critical sector underpinning the evolution of modern vehicles. Explore intricate market dynamics, growth trajectories, regional dominance, product innovations, key drivers, emerging opportunities, and the strategies of leading players. With a detailed analysis spanning the Historical Period (2019-2024), Base Year (2025), and extending to the Forecast Period (2025-2033), this report provides unparalleled insights into a market projected for significant expansion. Discover the intricate interplay of parent market (semiconductors) and child market (automotive) forces shaping the future of mobility. All quantitative values are presented in Million units.

Automotive Semiconductor Market Market Dynamics & Structure

The Automotive Semiconductor Market is characterized by a moderately concentrated structure, with a few dominant players holding significant market share. Technological innovation remains the primary driver, fueled by the escalating demand for advanced driver-assistance systems (ADAS), in-car infotainment, and the rapid electrification of vehicles. Regulatory frameworks, particularly concerning vehicle safety and emissions, indirectly influence semiconductor design and adoption. Competitive product substitutes are limited in the core automotive semiconductor space, but innovation in materials and manufacturing processes can disrupt existing supply chains. End-user demographics, encompassing a growing global middle class with an increasing appetite for technologically advanced vehicles, further propel demand. Mergers and acquisitions (M&A) are a notable trend, with companies consolidating to enhance their product portfolios, expand geographical reach, and secure critical supply chains.

- Market Concentration: Dominated by a few key players, but with a growing number of specialized suppliers.

- Technological Innovation: Driven by ADAS, EVs, and autonomous driving features.

- Regulatory Impact: Safety and emissions standards necessitate advanced semiconductor solutions.

- End-User Demand: Rising consumer expectations for sophisticated in-car technology.

- M&A Activity: Strategic consolidations to gain market share and technological capabilities.

- Innovation Barriers: High R&D costs, long product development cycles, and stringent automotive qualification processes.

Automotive Semiconductor Market Growth Trends & Insights

The Automotive Semiconductor Market is poised for robust growth, driven by the transformative shifts occurring within the automotive industry. The accelerating adoption of electric vehicles (EVs) is a paramount growth catalyst, necessitating a surge in demand for power semiconductors, battery management ICs, and advanced sensor technologies to optimize performance and efficiency. Similarly, the relentless pursuit of enhanced vehicle safety and convenience is fueling the expansion of ADAS features, requiring sophisticated processors, memory devices, and RF components for radar, lidar, and camera systems. The integration of connectivity and infotainment systems is creating a substantial market for high-performance computing chips, display drivers, and audio processing units. Consumer preferences are increasingly tilting towards connected and intelligent vehicles, further incentivizing automotive manufacturers to embed more advanced semiconductor solutions. This dynamic interplay of technological advancements, evolving consumer expectations, and the inherent need for improved vehicle functionality will collectively drive the market's expansion. The market size is projected to grow from 180,500 Million units in 2025 to 310,200 Million units by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 7.0% during the forecast period. The penetration of advanced semiconductor technologies in new vehicle models is expected to reach 85% by 2033, indicating a significant shift in automotive manufacturing priorities.

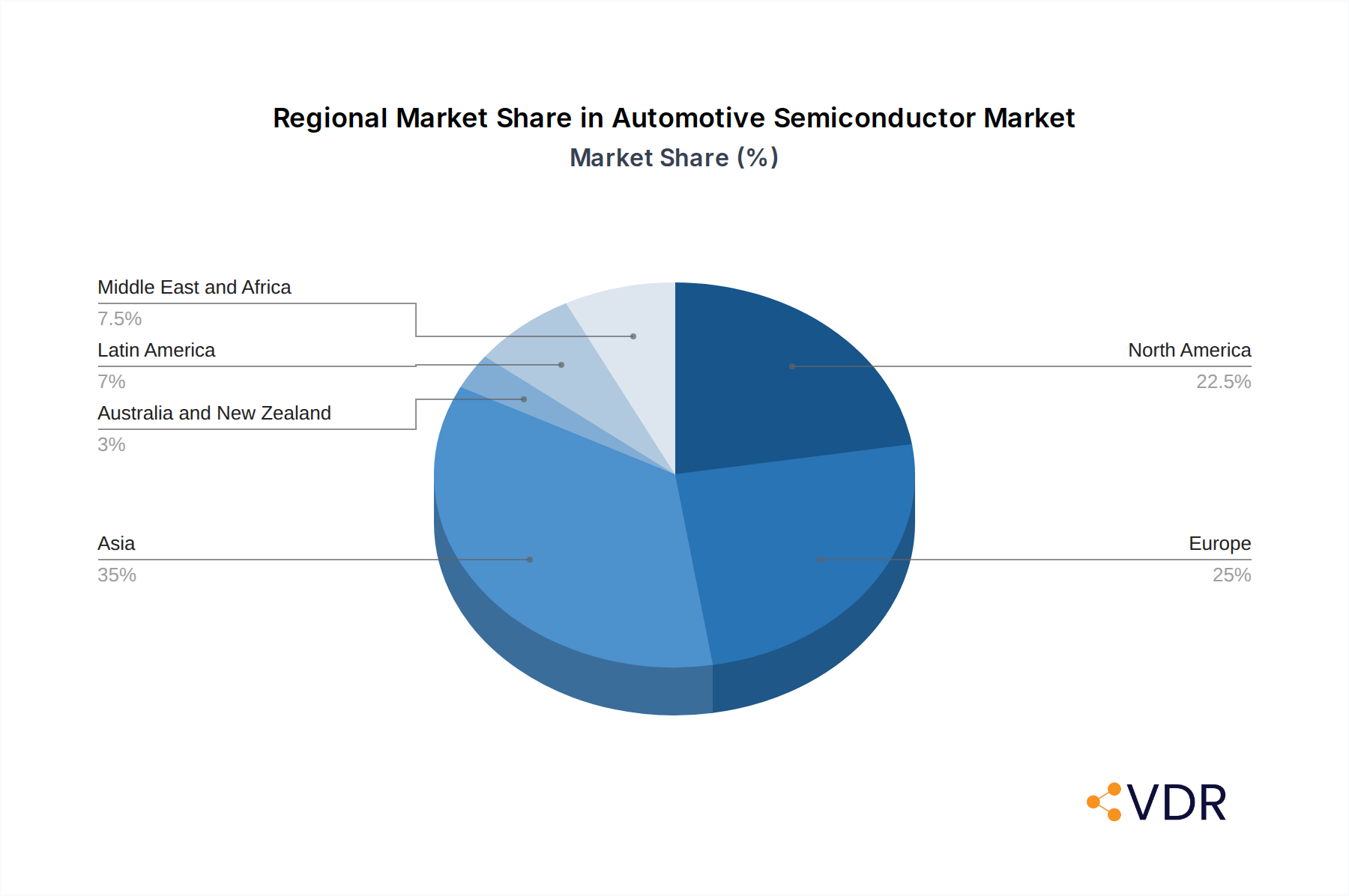

Dominant Regions, Countries, or Segments in Automotive Semiconductor Market

The Automotive Semiconductor Market exhibits strong growth driven by several key segments and regions. Within Vehicle Type, Passenger Vehicles represent the largest and fastest-growing segment. This dominance stems from their high sales volumes globally and the increasing integration of sophisticated electronics for safety, comfort, and entertainment. The rising disposable incomes in emerging economies and the continued demand for premium features in developed markets further bolster this segment.

Among Components, Integrated Circuits (ICs) hold the lion's share and are projected to maintain their lead. This broad category encompasses microcontrollers, application processors, and power management ICs, all of which are indispensable for modern vehicle functions. Sensors are another rapidly expanding component, crucial for ADAS, autonomous driving, and powertrain management, with significant growth anticipated for image sensors, radar sensors, and LiDAR components.

In terms of Applications, Power Electronics and Safety are the primary growth drivers. The electrification trend is directly boosting the demand for power semiconductors in EV powertrains, charging infrastructure, and battery management systems. Simultaneously, stringent safety regulations and consumer demand for advanced safety features are accelerating the adoption of semiconductors in ADAS and active safety systems.

Geographically, Asia Pacific, particularly China, is emerging as a dominant region. This is attributed to its massive automotive production base, growing domestic demand for vehicles, and significant government support for the EV sector and semiconductor manufacturing. North America and Europe also remain strong markets, driven by advanced automotive technologies, high safety standards, and a robust aftermarket for automotive electronics.

- Dominant Vehicle Type: Passenger Vehicles – driven by high sales volumes and demand for advanced features.

- Key Component Growth: Integrated Circuits (ICs) and Sensors – essential for all vehicle electronic systems.

- Leading Applications: Power Electronics (due to EV adoption) and Safety (due to regulatory and consumer demand).

- Regional Leadership: Asia Pacific (especially China) – fueled by manufacturing prowess and EV expansion.

- Growth Potential: Significant opportunities exist in the burgeoning EV market and the continuous evolution of autonomous driving technologies.

Automotive Semiconductor Market Product Landscape

The Automotive Semiconductor Market is characterized by a dynamic product landscape focused on enhancing vehicle safety, efficiency, and connectivity. Innovations in Processors are enabling more powerful and efficient computation for ADAS and infotainment systems. Sensors, ranging from advanced image sensors to radar and LiDAR, are crucial for perception and navigation in autonomous driving. Memory Devices are expanding to accommodate the ever-increasing data generated by vehicle sensors and complex software. Integrated Circuits (ICs), including microcontrollers and power management ICs, are becoming more specialized and efficient for specific automotive applications. Discrete Power Devices are vital for managing power flow in EVs, while RF Devices are indispensable for vehicle communication and connectivity. These advancements collectively contribute to lighter, more energy-efficient, and intelligent vehicles.

Key Drivers, Barriers & Challenges in Automotive Semiconductor Market

The Automotive Semiconductor Market is propelled by several key drivers. The burgeoning electrification of vehicles is a monumental force, demanding a substantial increase in power semiconductors and associated ICs for battery management and powertrain control. The persistent drive towards autonomous driving necessitates sophisticated processors, high-performance sensors (like radar, lidar, and cameras), and advanced memory solutions. Increasing vehicle connectivity and the demand for advanced in-car infotainment systems are creating significant growth opportunities for communication chips, processors, and display drivers. Stringent vehicle safety regulations worldwide are mandating the integration of ADAS features, directly boosting semiconductor demand.

Conversely, the market faces significant barriers and challenges. Supply chain disruptions, as evidenced by recent global events, remain a critical concern, impacting production volumes and lead times. The long product development cycles and stringent qualification processes in the automotive industry present a barrier to rapid innovation and market entry. High research and development (R&D) costs associated with developing advanced semiconductor technologies require substantial investment. Intensifying competition among established players and emerging entrants, coupled with the threat of price erosion, adds another layer of complexity. The complexity of automotive electronic architectures and the need for robust cybersecurity measures further challenge manufacturers.

Emerging Opportunities in Automotive Semiconductor Market

Emerging opportunities in the Automotive Semiconductor Market are vast and transformative. The rapid growth of the Electric Vehicle (EV) market presents immense potential for specialized power semiconductors, battery management ICs, and highly efficient power conversion components. The advancement of autonomous driving technologies will continue to fuel demand for cutting-edge sensors, AI-accelerating processors, and high-bandwidth memory solutions. The increasing integration of Vehicle-to-Everything (V2X) communication will open new avenues for RF devices and advanced connectivity chips. Furthermore, the growing trend of software-defined vehicles presents opportunities for more powerful and flexible computing platforms, enabling over-the-air updates and new feature deployments. The demand for advanced in-cabin experience, including immersive infotainment, augmented reality displays, and driver monitoring systems, will also drive innovation in related semiconductor technologies.

Growth Accelerators in the Automotive Semiconductor Market Industry

Several catalysts are accelerating long-term growth within the Automotive Semiconductor Market Industry. The relentless pace of technological breakthroughs in AI, machine learning, and advanced materials science is enabling the development of more powerful, efficient, and cost-effective semiconductor solutions specifically tailored for automotive applications. Strategic partnerships and collaborations between semiconductor manufacturers, automotive OEMs, and Tier-1 suppliers are crucial for co-developing innovative solutions and streamlining the integration process, thus shortening time-to-market. The growing global emphasis on sustainability and emissions reduction is a powerful accelerator, driving the demand for semiconductors that enhance EV performance and fuel efficiency in traditional internal combustion engine vehicles. Moreover, government initiatives and subsidies aimed at promoting EV adoption and domestic semiconductor manufacturing are creating a favorable investment climate and further stimulating market expansion.

Key Players Shaping the Automotive Semiconductor Market Market

- Infineon Technologies AG

- Renesas Electronics Corporation

- Micron Technology

- Texas Instruments Inc

- Toshiba Electronic Devices & Storage Corporation (Toshiba Corporation)

- STMicroelectronics NV

- Robert Bosch GmbH

- Onsemi (Semiconductor Components Industries LLC)

- Analog Devices Inc

- ROHM Co Ltd

- NXP Semiconductors NV

Notable Milestones in Automotive Semiconductor Market Sector

- April 2024: Infineon Technologies AG solidified its dominance in the automotive semiconductor market, with TechInsights reporting bolstered market share across all regions, maintaining top positions in South Korea and China, and achieving substantial progress in the Japanese automotive semiconductor sector. Infineon reinforced its standing as the second-largest player in Europe and secured a spot in the top three in North America.

- April 2024: Renesas Electronics Corporation announced the commencement of operations at its Kofu Factory in Kai City, Yamanashi Prefecture, Japan, aiming to boost its production capacity of power semiconductors in anticipation of growing demand for electric vehicles (EVs).

In-Depth Automotive Semiconductor Market Market Outlook

The Automotive Semiconductor Market outlook remains exceptionally bright, driven by deep-seated industry transformations. Future growth will be significantly shaped by the increasing sophistication of autonomous driving systems, requiring advanced processors and sensor fusion technologies. The ongoing transition to electric mobility will continue to be a primary growth engine, spurring demand for high-performance power semiconductors and efficient energy management solutions. The expanding integration of connected car features and digital cockpits will necessitate more powerful computing platforms and seamless connectivity modules. Strategic investments in advanced manufacturing capabilities and a focus on resilient supply chains will be critical for players to capitalize on these opportunities. Emerging markets, with their rapidly growing automotive sectors and increasing adoption of new technologies, also present substantial untapped potential for market expansion and innovation.

Automotive Semiconductor Market Segmentation

-

1. Vehicle Type

- 1.1. Passenger Vehicle

- 1.2. Light Commercial Vehicle

- 1.3. Heavy Commercial Vehicle

-

2. Component

- 2.1. Processors

- 2.2. Sensors

- 2.3. Memory Devices

- 2.4. Integrated Circuits

- 2.5. Discrete Power Devices

- 2.6. RF Devices

-

3. Application

- 3.1. Chassis

- 3.2. Power Electronics

- 3.3. Safety

- 3.4. Body Electronics

- 3.5. Comforts/Entertainment Unit

- 3.6. Other Applications

Automotive Semiconductor Market Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Automotive Semiconductor Market Regional Market Share

Geographic Coverage of Automotive Semiconductor Market

Automotive Semiconductor Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.14% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Passenger Vehicle

- 5.1.2. Light Commercial Vehicle

- 5.1.3. Heavy Commercial Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Component

- 5.2.1. Processors

- 5.2.2. Sensors

- 5.2.3. Memory Devices

- 5.2.4. Integrated Circuits

- 5.2.5. Discrete Power Devices

- 5.2.6. RF Devices

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Chassis

- 5.3.2. Power Electronics

- 5.3.3. Safety

- 5.3.4. Body Electronics

- 5.3.5. Comforts/Entertainment Unit

- 5.3.6. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia

- 5.4.4. Australia and New Zealand

- 5.4.5. Latin America

- 5.4.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. Global Automotive Semiconductor Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Passenger Vehicle

- 6.1.2. Light Commercial Vehicle

- 6.1.3. Heavy Commercial Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Component

- 6.2.1. Processors

- 6.2.2. Sensors

- 6.2.3. Memory Devices

- 6.2.4. Integrated Circuits

- 6.2.5. Discrete Power Devices

- 6.2.6. RF Devices

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Chassis

- 6.3.2. Power Electronics

- 6.3.3. Safety

- 6.3.4. Body Electronics

- 6.3.5. Comforts/Entertainment Unit

- 6.3.6. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. North America Automotive Semiconductor Market Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.1.1. Passenger Vehicle

- 7.1.2. Light Commercial Vehicle

- 7.1.3. Heavy Commercial Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Component

- 7.2.1. Processors

- 7.2.2. Sensors

- 7.2.3. Memory Devices

- 7.2.4. Integrated Circuits

- 7.2.5. Discrete Power Devices

- 7.2.6. RF Devices

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Chassis

- 7.3.2. Power Electronics

- 7.3.3. Safety

- 7.3.4. Body Electronics

- 7.3.5. Comforts/Entertainment Unit

- 7.3.6. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 8. Europe Automotive Semiconductor Market Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.1.1. Passenger Vehicle

- 8.1.2. Light Commercial Vehicle

- 8.1.3. Heavy Commercial Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Component

- 8.2.1. Processors

- 8.2.2. Sensors

- 8.2.3. Memory Devices

- 8.2.4. Integrated Circuits

- 8.2.5. Discrete Power Devices

- 8.2.6. RF Devices

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Chassis

- 8.3.2. Power Electronics

- 8.3.3. Safety

- 8.3.4. Body Electronics

- 8.3.5. Comforts/Entertainment Unit

- 8.3.6. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 9. Asia Automotive Semiconductor Market Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.1.1. Passenger Vehicle

- 9.1.2. Light Commercial Vehicle

- 9.1.3. Heavy Commercial Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Component

- 9.2.1. Processors

- 9.2.2. Sensors

- 9.2.3. Memory Devices

- 9.2.4. Integrated Circuits

- 9.2.5. Discrete Power Devices

- 9.2.6. RF Devices

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Chassis

- 9.3.2. Power Electronics

- 9.3.3. Safety

- 9.3.4. Body Electronics

- 9.3.5. Comforts/Entertainment Unit

- 9.3.6. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 10. Australia and New Zealand Automotive Semiconductor Market Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.1.1. Passenger Vehicle

- 10.1.2. Light Commercial Vehicle

- 10.1.3. Heavy Commercial Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Component

- 10.2.1. Processors

- 10.2.2. Sensors

- 10.2.3. Memory Devices

- 10.2.4. Integrated Circuits

- 10.2.5. Discrete Power Devices

- 10.2.6. RF Devices

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Chassis

- 10.3.2. Power Electronics

- 10.3.3. Safety

- 10.3.4. Body Electronics

- 10.3.5. Comforts/Entertainment Unit

- 10.3.6. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 11. Latin America Automotive Semiconductor Market Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 11.1.1. Passenger Vehicle

- 11.1.2. Light Commercial Vehicle

- 11.1.3. Heavy Commercial Vehicle

- 11.2. Market Analysis, Insights and Forecast - by Component

- 11.2.1. Processors

- 11.2.2. Sensors

- 11.2.3. Memory Devices

- 11.2.4. Integrated Circuits

- 11.2.5. Discrete Power Devices

- 11.2.6. RF Devices

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Chassis

- 11.3.2. Power Electronics

- 11.3.3. Safety

- 11.3.4. Body Electronics

- 11.3.5. Comforts/Entertainment Unit

- 11.3.6. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 12. Middle East and Africa Automotive Semiconductor Market Analysis, Insights and Forecast, 2021-2033

- 12.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 12.1.1. Passenger Vehicle

- 12.1.2. Light Commercial Vehicle

- 12.1.3. Heavy Commercial Vehicle

- 12.2. Market Analysis, Insights and Forecast - by Component

- 12.2.1. Processors

- 12.2.2. Sensors

- 12.2.3. Memory Devices

- 12.2.4. Integrated Circuits

- 12.2.5. Discrete Power Devices

- 12.2.6. RF Devices

- 12.3. Market Analysis, Insights and Forecast - by Application

- 12.3.1. Chassis

- 12.3.2. Power Electronics

- 12.3.3. Safety

- 12.3.4. Body Electronics

- 12.3.5. Comforts/Entertainment Unit

- 12.3.6. Other Applications

- 12.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Infineon Technologies AG

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Renesas Electronics Corporaton

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Micron Technology

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Texas Instrument Inc

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Toshiba Electronic Devices & Storage Corporation (Toshiba Corporation)

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 STMicroelectronics NV

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Robert Bosch GmbH

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Onsemi (Semiconductor Components Industries LLC)

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Analog Devices Inc

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 ROHM Co Lt

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 NXP Semiconductor NV

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.1 Infineon Technologies AG

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Automotive Semiconductor Market Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Semiconductor Market Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 3: North America Automotive Semiconductor Market Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 4: North America Automotive Semiconductor Market Revenue (Million), by Component 2025 & 2033

- Figure 5: North America Automotive Semiconductor Market Revenue Share (%), by Component 2025 & 2033

- Figure 6: North America Automotive Semiconductor Market Revenue (Million), by Application 2025 & 2033

- Figure 7: North America Automotive Semiconductor Market Revenue Share (%), by Application 2025 & 2033

- Figure 8: North America Automotive Semiconductor Market Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Automotive Semiconductor Market Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Automotive Semiconductor Market Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 11: Europe Automotive Semiconductor Market Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 12: Europe Automotive Semiconductor Market Revenue (Million), by Component 2025 & 2033

- Figure 13: Europe Automotive Semiconductor Market Revenue Share (%), by Component 2025 & 2033

- Figure 14: Europe Automotive Semiconductor Market Revenue (Million), by Application 2025 & 2033

- Figure 15: Europe Automotive Semiconductor Market Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Semiconductor Market Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Automotive Semiconductor Market Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Automotive Semiconductor Market Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 19: Asia Automotive Semiconductor Market Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 20: Asia Automotive Semiconductor Market Revenue (Million), by Component 2025 & 2033

- Figure 21: Asia Automotive Semiconductor Market Revenue Share (%), by Component 2025 & 2033

- Figure 22: Asia Automotive Semiconductor Market Revenue (Million), by Application 2025 & 2033

- Figure 23: Asia Automotive Semiconductor Market Revenue Share (%), by Application 2025 & 2033

- Figure 24: Asia Automotive Semiconductor Market Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Automotive Semiconductor Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Australia and New Zealand Automotive Semiconductor Market Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 27: Australia and New Zealand Automotive Semiconductor Market Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 28: Australia and New Zealand Automotive Semiconductor Market Revenue (Million), by Component 2025 & 2033

- Figure 29: Australia and New Zealand Automotive Semiconductor Market Revenue Share (%), by Component 2025 & 2033

- Figure 30: Australia and New Zealand Automotive Semiconductor Market Revenue (Million), by Application 2025 & 2033

- Figure 31: Australia and New Zealand Automotive Semiconductor Market Revenue Share (%), by Application 2025 & 2033

- Figure 32: Australia and New Zealand Automotive Semiconductor Market Revenue (Million), by Country 2025 & 2033

- Figure 33: Australia and New Zealand Automotive Semiconductor Market Revenue Share (%), by Country 2025 & 2033

- Figure 34: Latin America Automotive Semiconductor Market Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 35: Latin America Automotive Semiconductor Market Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 36: Latin America Automotive Semiconductor Market Revenue (Million), by Component 2025 & 2033

- Figure 37: Latin America Automotive Semiconductor Market Revenue Share (%), by Component 2025 & 2033

- Figure 38: Latin America Automotive Semiconductor Market Revenue (Million), by Application 2025 & 2033

- Figure 39: Latin America Automotive Semiconductor Market Revenue Share (%), by Application 2025 & 2033

- Figure 40: Latin America Automotive Semiconductor Market Revenue (Million), by Country 2025 & 2033

- Figure 41: Latin America Automotive Semiconductor Market Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa Automotive Semiconductor Market Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 43: Middle East and Africa Automotive Semiconductor Market Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 44: Middle East and Africa Automotive Semiconductor Market Revenue (Million), by Component 2025 & 2033

- Figure 45: Middle East and Africa Automotive Semiconductor Market Revenue Share (%), by Component 2025 & 2033

- Figure 46: Middle East and Africa Automotive Semiconductor Market Revenue (Million), by Application 2025 & 2033

- Figure 47: Middle East and Africa Automotive Semiconductor Market Revenue Share (%), by Application 2025 & 2033

- Figure 48: Middle East and Africa Automotive Semiconductor Market Revenue (Million), by Country 2025 & 2033

- Figure 49: Middle East and Africa Automotive Semiconductor Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Semiconductor Market Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 2: Global Automotive Semiconductor Market Revenue Million Forecast, by Component 2020 & 2033

- Table 3: Global Automotive Semiconductor Market Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Global Automotive Semiconductor Market Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Automotive Semiconductor Market Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 6: Global Automotive Semiconductor Market Revenue Million Forecast, by Component 2020 & 2033

- Table 7: Global Automotive Semiconductor Market Revenue Million Forecast, by Application 2020 & 2033

- Table 8: Global Automotive Semiconductor Market Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Global Automotive Semiconductor Market Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 10: Global Automotive Semiconductor Market Revenue Million Forecast, by Component 2020 & 2033

- Table 11: Global Automotive Semiconductor Market Revenue Million Forecast, by Application 2020 & 2033

- Table 12: Global Automotive Semiconductor Market Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Automotive Semiconductor Market Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 14: Global Automotive Semiconductor Market Revenue Million Forecast, by Component 2020 & 2033

- Table 15: Global Automotive Semiconductor Market Revenue Million Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Semiconductor Market Revenue Million Forecast, by Country 2020 & 2033

- Table 17: Global Automotive Semiconductor Market Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 18: Global Automotive Semiconductor Market Revenue Million Forecast, by Component 2020 & 2033

- Table 19: Global Automotive Semiconductor Market Revenue Million Forecast, by Application 2020 & 2033

- Table 20: Global Automotive Semiconductor Market Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Global Automotive Semiconductor Market Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 22: Global Automotive Semiconductor Market Revenue Million Forecast, by Component 2020 & 2033

- Table 23: Global Automotive Semiconductor Market Revenue Million Forecast, by Application 2020 & 2033

- Table 24: Global Automotive Semiconductor Market Revenue Million Forecast, by Country 2020 & 2033

- Table 25: Global Automotive Semiconductor Market Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 26: Global Automotive Semiconductor Market Revenue Million Forecast, by Component 2020 & 2033

- Table 27: Global Automotive Semiconductor Market Revenue Million Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Semiconductor Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Semiconductor Market?

The projected CAGR is approximately 11.14%.

2. Which companies are prominent players in the Automotive Semiconductor Market?

Key companies in the market include Infineon Technologies AG, Renesas Electronics Corporaton, Micron Technology, Texas Instrument Inc, Toshiba Electronic Devices & Storage Corporation (Toshiba Corporation), STMicroelectronics NV, Robert Bosch GmbH, Onsemi (Semiconductor Components Industries LLC), Analog Devices Inc, ROHM Co Lt, NXP Semiconductor NV.

3. What are the main segments of the Automotive Semiconductor Market?

The market segments include Vehicle Type, Component, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 72.71 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Vehicle Production; Rising Demand for Advanced Safety and Comfort Systems.

6. What are the notable trends driving market growth?

Passenger Vehicles to Hold Major Market Share.

7. Are there any restraints impacting market growth?

Higher Cost of Advanced Featured Vehicles.

8. Can you provide examples of recent developments in the market?

April 2024: Infineon Technologies AG solidified its dominance in the automotive semiconductor market. TechInsights reported that Infineon bolstered its market share across all regions and maintained its top position in South Korea and China. Notably, Infineon achieved substantial progress in the Japanese automotive semiconductor sector. Infineon reinforced its standing as the second-largest player in Europe and secured a spot in the top three in North America.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Semiconductor Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Semiconductor Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Semiconductor Market?

To stay informed about further developments, trends, and reports in the Automotive Semiconductor Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence