Key Insights

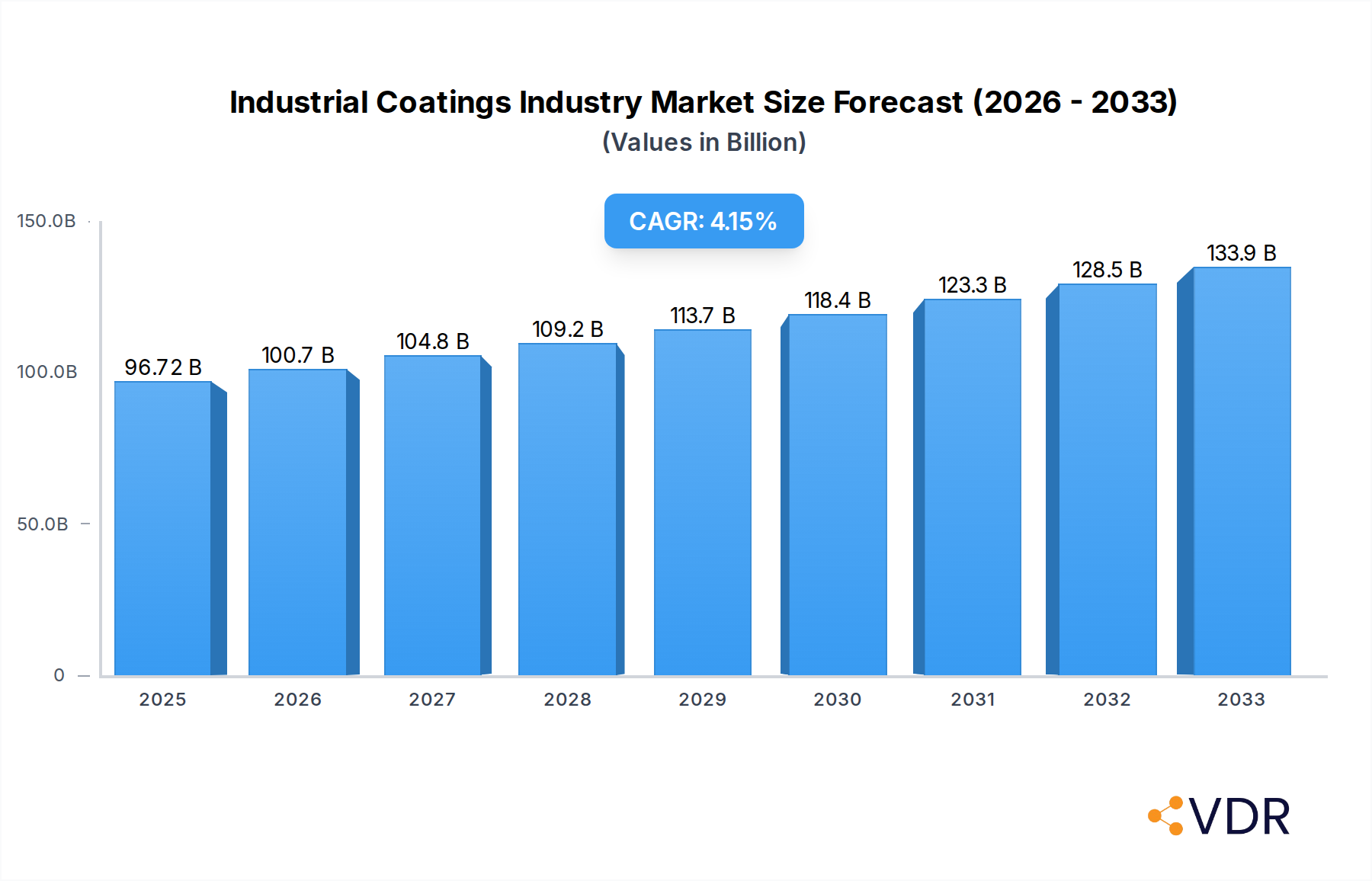

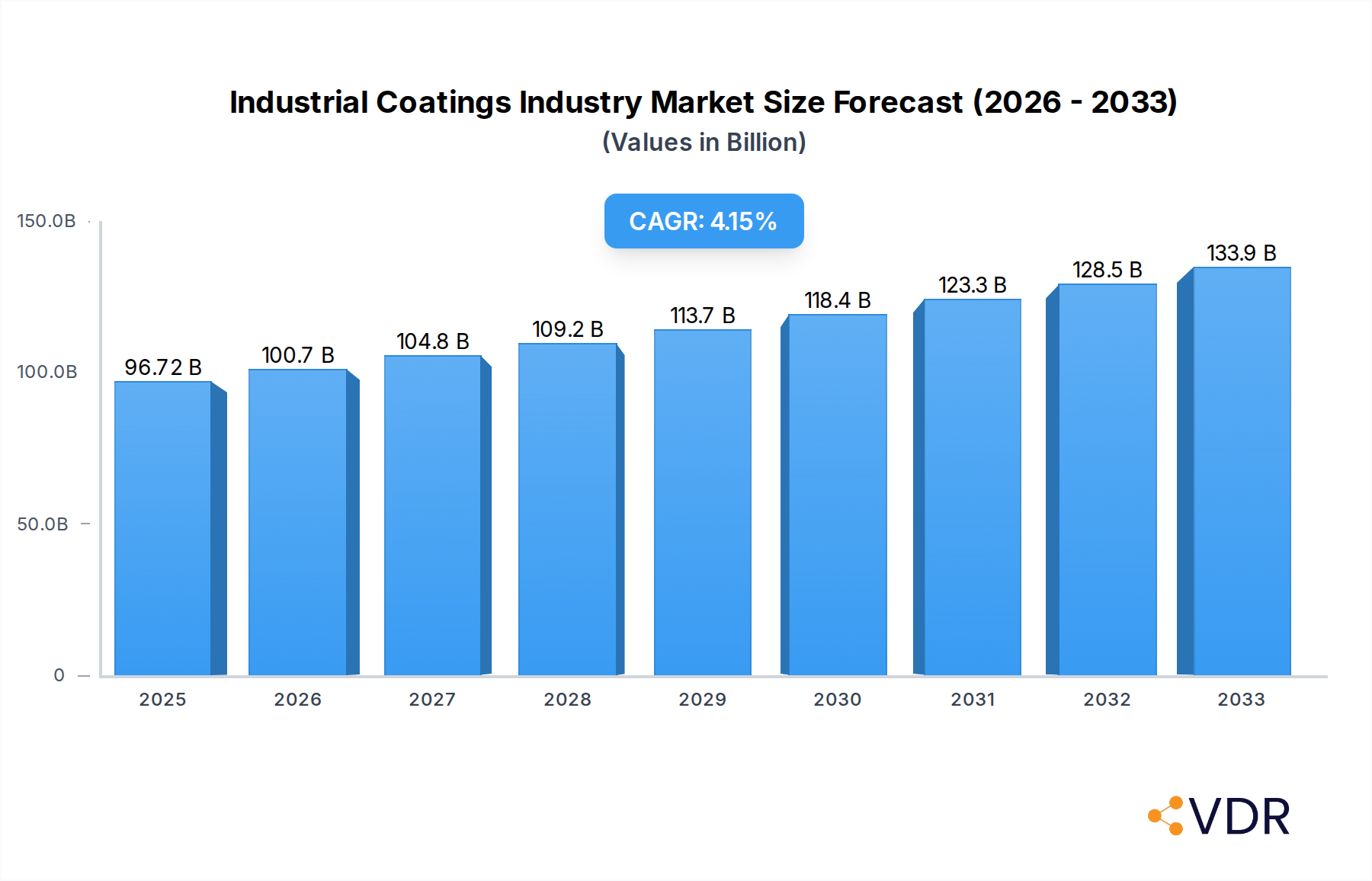

The global industrial coatings market is poised for substantial growth, projected to reach an estimated $96.72 billion in 2025. This expansion is driven by a robust compound annual growth rate (CAGR) of 4.1% during the forecast period. A key catalyst for this upward trajectory is the increasing demand from burgeoning end-user industries, particularly in infrastructure development and the oil and gas sector, where protective coatings are indispensable for asset longevity and operational efficiency. The growing emphasis on sustainability is also shaping the market, fostering innovation in water-borne and low-VOC (Volatile Organic Compound) solvent-borne technologies. These eco-friendly alternatives are gaining traction as regulatory pressures tighten and consumer awareness of environmental impact rises, signaling a significant shift towards greener solutions.

Industrial Coatings Industry Market Size (In Billion)

The market's dynamism is further characterized by the diverse range of resin technologies and their specific applications. Epoxy resins continue to dominate due to their exceptional durability, chemical resistance, and adhesion properties, making them a preferred choice for demanding protective coatings. Polyurethane and acrylic resins are also witnessing steady demand, offering versatility in terms of flexibility, UV resistance, and aesthetic appeal. While solvent-borne coatings retain a significant market share, the sustained innovation and increasing acceptance of water-borne technologies indicate a gradual but discernible trend towards more environmentally conscious formulations. Leading players like AkzoNobel, Sherwin-Williams, and PPG Industries are actively investing in research and development to cater to these evolving needs, suggesting a competitive landscape focused on technological advancement and sustainable product offerings to capture market share across various industrial segments.

Industrial Coatings Industry Company Market Share

This comprehensive report offers an in-depth analysis of the global Industrial Coatings Industry, exploring its intricate market dynamics, growth trajectories, and future potential. Covering the period from 2019 to 2033, with a base year of 2025, this research delves into the parent and child market segments, providing crucial insights for industry professionals, investors, and stakeholders. Gain a competitive edge with data-driven strategies and a clear understanding of the forces shaping the future of industrial coatings.

Industrial Coatings Industry Market Dynamics & Structure

The Industrial Coatings Industry is characterized by a moderately concentrated market, with key players like AkzoNobel N.V., The Sherwin-Williams Company, PPG Industries, and Jotun dominating significant market shares. Technological innovation remains a primary driver, with a consistent push towards sustainable solutions like water-borne coatings and low-VOC (Volatile Organic Compound) formulations. Regulatory frameworks, particularly those concerning environmental protection and worker safety, play a pivotal role in shaping product development and market entry. Competitive product substitutes, such as advanced material treatments and alternative protective measures, continuously challenge the status quo, necessitating ongoing innovation in coating performance. End-user demographics are diverse, ranging from large-scale infrastructure projects to specialized manufacturing sectors, each with unique demand drivers. Mergers and acquisitions (M&A) are a recurring trend, aimed at expanding geographical reach, consolidating market share, and acquiring advanced technologies. For instance, the acquisition of Sika AG's European industrial coatings business by Sherwin-Williams in June 2022 exemplifies this trend, strengthening its market presence in the region. The industry faces innovation barriers stemming from the high cost of R&D, stringent testing requirements for performance and durability, and the need for specialized application equipment.

- Market Concentration: Moderate, with top players holding significant market share.

- Technological Innovation Drivers: Sustainability, high-performance coatings, advanced application methods.

- Regulatory Frameworks: Environmental protection (VOC limits), health and safety standards.

- Competitive Product Substitutes: Advanced material treatments, alternative corrosion protection methods.

- End-User Demographics: Diverse, spanning infrastructure, automotive, marine, aerospace, and general manufacturing.

- M&A Trends: Strategic acquisitions for market expansion and technology integration.

Industrial Coatings Industry Growth Trends & Insights

The Industrial Coatings Industry is poised for robust growth, driven by an increasing demand for durable, protective, and aesthetically pleasing finishes across various sectors. The global market size is projected to experience a significant upswing, reaching an estimated USD 135.8 billion by 2025, with a projected Compound Annual Growth Rate (CAGR) of 6.2% from 2025 to 2033. This expansion is fueled by several key trends: the growing emphasis on infrastructure development and modernization globally, particularly in emerging economies; the continuous need for corrosion protection in harsh environments such as oil and gas exploration, mining, and marine applications; and the rising adoption of environmentally friendly coatings, including water-borne and powder coatings, due to increasing environmental consciousness and stringent regulations. Technological advancements, such as the development of smart coatings with self-healing or anti-microbial properties, are also contributing to market growth by offering enhanced functionality and value. Consumer behavior shifts are evident in the demand for customized solutions and coatings that offer extended lifecycles and reduced maintenance costs.

The adoption rate of advanced coating technologies is accelerating, with a notable shift away from traditional solvent-borne coatings towards more sustainable alternatives. For instance, the demand for epoxy resins, a key segment, is expected to grow substantially due to their excellent chemical resistance and adhesion properties, making them ideal for protective applications. Similarly, polyurethane coatings are gaining traction for their flexibility and durability. The protective coatings segment, encompassing oil and gas, mining, power, and infrastructure, is a major growth engine, driven by ongoing global investments in these sectors. The general industrial segment also contributes significantly, fueled by manufacturing output and the demand for coatings in automotive, aerospace, and appliance manufacturing. The market penetration of high-performance coatings is increasing as industries seek to improve product longevity and reduce lifecycle costs.

Dominant Regions, Countries, or Segments in Industrial Coatings Industry

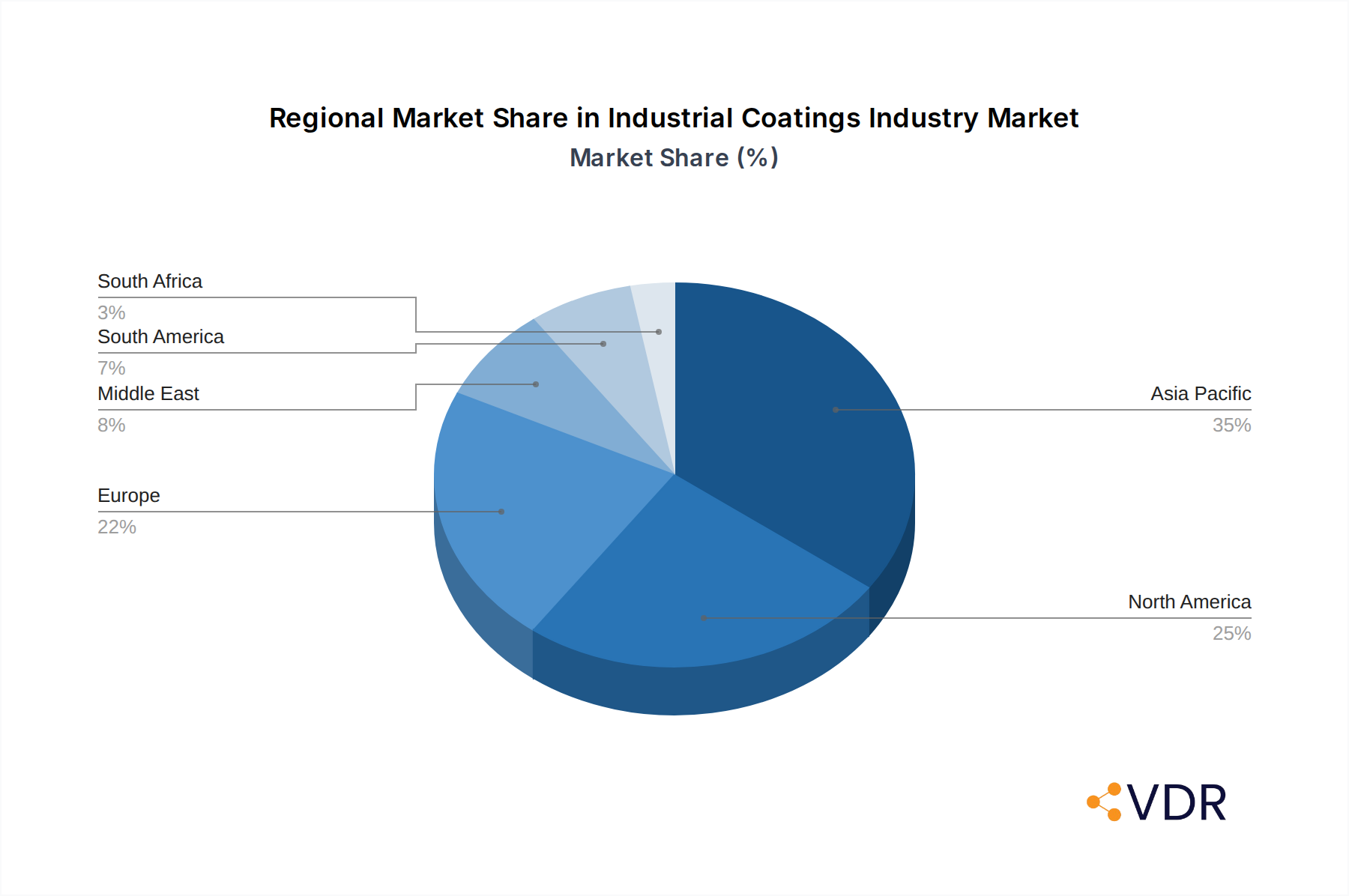

The Industrial Coatings Industry's growth is not uniform across all regions and segments, with several factors contributing to regional dominance and segment leadership. Asia-Pacific stands out as the dominant region, driven by rapid industrialization, extensive infrastructure projects, and a burgeoning manufacturing base in countries like China, India, and Southeast Asian nations. The region's substantial investments in automotive, construction, and electronics sectors directly translate into a high demand for various industrial coatings. Within this region, China is a significant contributor to market growth due to its status as a global manufacturing hub.

Among the resin segments, Epoxy coatings consistently hold a dominant position. Their exceptional chemical resistance, adhesion properties, and durability make them indispensable for protective coatings in demanding applications such as oil and gas pipelines, marine vessels, and industrial flooring. The projected market size for epoxy resins in the industrial coatings sector is estimated to be USD 35 billion in 2025. Following closely is Polyurethane coatings, which offer excellent flexibility, abrasion resistance, and UV stability, making them suitable for automotive topcoats, wood finishes, and various industrial machinery.

In terms of technology, Water-borne Coatings are witnessing the most significant growth trajectory. Driven by stringent environmental regulations and a global push for sustainability, these coatings are increasingly replacing traditional solvent-borne alternatives. Their lower VOC emissions and improved safety profiles are making them the preferred choice across numerous applications, projected to capture a substantial market share of over 40% by 2025. While solvent-borne coatings still hold a significant market share, their growth is moderating.

The Protective Coatings segment, particularly Oil and Gas and Infrastructure, are key drivers of market expansion. The need for robust corrosion protection in offshore platforms, pipelines, and bridges, coupled with ongoing global investments in energy infrastructure and public works, fuels the demand for high-performance protective coatings. The infrastructure sub-segment alone is estimated to account for USD 28 billion in 2025. The mining sector also contributes significantly, requiring durable coatings for heavy machinery and processing plants.

Industrial Coatings Industry Product Landscape

The Industrial Coatings Industry is characterized by a diverse and evolving product landscape, driven by the pursuit of enhanced performance, sustainability, and specialized applications. Key product innovations focus on improving durability, corrosion resistance, and environmental compatibility. For instance, the development of high-solids and powder coatings significantly reduces VOC emissions, aligning with global environmental mandates. Advanced resin formulations, such as novel epoxy hybrids and bio-based polyurethanes, are emerging, offering superior adhesion, chemical resistance, and reduced environmental impact. Application-specific coatings, including anti-fouling marine coatings, heat-resistant industrial coatings, and chemical-resistant linings for storage tanks, continue to be areas of intense development. Performance metrics such as extended service life, rapid curing times, and enhanced aesthetic appeal are crucial unique selling propositions for manufacturers.

Key Drivers, Barriers & Challenges in Industrial Coatings Industry

The Industrial Coatings Industry is propelled by several key drivers, including substantial investments in global infrastructure development, a persistent need for asset protection against corrosion and environmental degradation, and the increasing adoption of sustainable and eco-friendly coating technologies. Technological advancements, such as the development of smart coatings with self-healing or anti-corrosion properties, also act as significant growth accelerators. Government initiatives promoting green manufacturing and stringent environmental regulations favoring low-VOC coatings further stimulate market expansion.

However, the industry faces considerable barriers and challenges. Volatility in raw material prices, particularly for petrochemical-based resins and pigments, directly impacts production costs and profit margins. The complex and stringent regulatory landscape across different regions adds to compliance costs and product development timelines. Supply chain disruptions, as witnessed in recent years, can lead to material shortages and delivery delays. Furthermore, intense competition from established players and emerging regional manufacturers can exert downward pressure on prices, while the high cost of research and development for innovative, high-performance coatings can be a significant barrier, especially for smaller enterprises.

Emerging Opportunities in Industrial Coatings Industry

Emerging opportunities in the Industrial Coatings Industry are significantly influenced by the global transition towards sustainability and digitalization. The increasing demand for bio-based and recycled content coatings presents a substantial untapped market as industries seek to reduce their environmental footprint. The growth of the renewable energy sector, particularly solar and wind power, creates new avenues for specialized coatings that enhance efficiency and durability of infrastructure. Furthermore, the adoption of digital technologies like AI and IoT in manufacturing and application processes offers opportunities for developing smart coatings with embedded functionalities and for optimizing coating application and performance monitoring. The demand for specialized coatings in the aerospace and defense sectors, driven by technological advancements and the need for lightweight, high-performance materials, also represents a promising area for growth.

Growth Accelerators in the Industrial Coatings Industry Industry

Several factors are acting as significant growth accelerators for the Industrial Coatings Industry. Continuous technological breakthroughs in resin chemistry and formulation science are leading to the development of coatings with superior performance characteristics, such as enhanced durability, faster curing times, and improved environmental profiles. Strategic partnerships and collaborations between raw material suppliers, coating manufacturers, and end-users are fostering innovation and accelerating the adoption of new technologies. The increasing global focus on sustainability and the circular economy is a powerful accelerator, driving demand for eco-friendly coatings and encouraging manufacturers to invest in greener production processes. Furthermore, market expansion strategies targeting rapidly developing economies and specialized niche markets are contributing to sustained growth.

Key Players Shaping the Industrial Coatings Industry Market

- AkzoNobel N.V.

- Chugoku Marine Paints Ltd

- The Sherwin-Williams Company

- Jotun

- RPM International Inc

- Beckers Group

- BASF SE

- Axalta Coating Systems

- Hempel A/S

- Sika AG

- PPG Industries

- Kansai Paint Co Ltd

- Wacker Chemie AG

- Nippon Paint ( NIPSEA GROUP)

Notable Milestones in Industrial Coatings Industry Sector

- August 2022: PPG announced an USD 11 million investment to double its powder coatings production capacity at its San Juan del Rio, Mexico plant, with expansion completion expected by mid-2023 to meet anticipated future demand.

- June 2022: The Sherwin-Williams Company finalized the acquisition of Sika AG's European industrial coatings business, integrating it into its Performance Coatings Group operating segment.

- April 2022: PPG completed the acquisition of Arsonsisi, an Italian industrial coatings company, and its powder coatings business, gaining a highly automated powder manufacturing plant in Verbania, Italy.

In-Depth Industrial Coatings Industry Market Outlook

The Industrial Coatings Industry is charting a course for sustained and robust growth, with a promising future shaped by innovation and strategic market positioning. The ongoing shift towards sustainable and high-performance coatings will continue to be a primary growth accelerator, driven by stringent environmental regulations and increasing consumer and industrial demand for eco-friendly solutions. Investments in emerging economies, coupled with the perpetual need for asset protection and infrastructure development globally, will provide a steady demand stream. Furthermore, the exploration and adoption of advanced technologies like smart coatings and digital application techniques present significant opportunities for market differentiation and value creation. Strategic collaborations and targeted acquisitions are expected to play a crucial role in consolidating market share and expanding technological capabilities, ensuring a dynamic and evolving landscape for the Industrial Coatings Industry.

Industrial Coatings Industry Segmentation

-

1. Resin

- 1.1. Epoxy

- 1.2. Polyurethane

- 1.3. Acrylic

- 1.4. Polyester

- 1.5. Other Resins

-

2. Technology

- 2.1. Water-borne Coatings

- 2.2. Solvent-borne Coatings

- 2.3. Other Technologies

-

3. End-user Industry

- 3.1. General Industrial

-

3.2. Protective Coatings

- 3.2.1. Oil and Gas

- 3.2.2. Mining

- 3.2.3. Power

- 3.2.4. Infrastructure

- 3.2.5. Other Protective Coatings

Industrial Coatings Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. Italy

- 3.4. France

- 3.5. Russia

- 3.6. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

- 5. Middle East

-

6. Saudi Arabia

- 6.1. South Africa

- 6.2. Rest of Middle East

Industrial Coatings Industry Regional Market Share

Geographic Coverage of Industrial Coatings Industry

Industrial Coatings Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Resin

- 5.1.1. Epoxy

- 5.1.2. Polyurethane

- 5.1.3. Acrylic

- 5.1.4. Polyester

- 5.1.5. Other Resins

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Water-borne Coatings

- 5.2.2. Solvent-borne Coatings

- 5.2.3. Other Technologies

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. General Industrial

- 5.3.2. Protective Coatings

- 5.3.2.1. Oil and Gas

- 5.3.2.2. Mining

- 5.3.2.3. Power

- 5.3.2.4. Infrastructure

- 5.3.2.5. Other Protective Coatings

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.4.2. North America

- 5.4.3. Europe

- 5.4.4. South America

- 5.4.5. Middle East

- 5.4.6. Saudi Arabia

- 5.1. Market Analysis, Insights and Forecast - by Resin

- 6. Global Industrial Coatings Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Resin

- 6.1.1. Epoxy

- 6.1.2. Polyurethane

- 6.1.3. Acrylic

- 6.1.4. Polyester

- 6.1.5. Other Resins

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Water-borne Coatings

- 6.2.2. Solvent-borne Coatings

- 6.2.3. Other Technologies

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. General Industrial

- 6.3.2. Protective Coatings

- 6.3.2.1. Oil and Gas

- 6.3.2.2. Mining

- 6.3.2.3. Power

- 6.3.2.4. Infrastructure

- 6.3.2.5. Other Protective Coatings

- 6.1. Market Analysis, Insights and Forecast - by Resin

- 7. Asia Pacific Industrial Coatings Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Resin

- 7.1.1. Epoxy

- 7.1.2. Polyurethane

- 7.1.3. Acrylic

- 7.1.4. Polyester

- 7.1.5. Other Resins

- 7.2. Market Analysis, Insights and Forecast - by Technology

- 7.2.1. Water-borne Coatings

- 7.2.2. Solvent-borne Coatings

- 7.2.3. Other Technologies

- 7.3. Market Analysis, Insights and Forecast - by End-user Industry

- 7.3.1. General Industrial

- 7.3.2. Protective Coatings

- 7.3.2.1. Oil and Gas

- 7.3.2.2. Mining

- 7.3.2.3. Power

- 7.3.2.4. Infrastructure

- 7.3.2.5. Other Protective Coatings

- 7.1. Market Analysis, Insights and Forecast - by Resin

- 8. North America Industrial Coatings Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Resin

- 8.1.1. Epoxy

- 8.1.2. Polyurethane

- 8.1.3. Acrylic

- 8.1.4. Polyester

- 8.1.5. Other Resins

- 8.2. Market Analysis, Insights and Forecast - by Technology

- 8.2.1. Water-borne Coatings

- 8.2.2. Solvent-borne Coatings

- 8.2.3. Other Technologies

- 8.3. Market Analysis, Insights and Forecast - by End-user Industry

- 8.3.1. General Industrial

- 8.3.2. Protective Coatings

- 8.3.2.1. Oil and Gas

- 8.3.2.2. Mining

- 8.3.2.3. Power

- 8.3.2.4. Infrastructure

- 8.3.2.5. Other Protective Coatings

- 8.1. Market Analysis, Insights and Forecast - by Resin

- 9. Europe Industrial Coatings Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Resin

- 9.1.1. Epoxy

- 9.1.2. Polyurethane

- 9.1.3. Acrylic

- 9.1.4. Polyester

- 9.1.5. Other Resins

- 9.2. Market Analysis, Insights and Forecast - by Technology

- 9.2.1. Water-borne Coatings

- 9.2.2. Solvent-borne Coatings

- 9.2.3. Other Technologies

- 9.3. Market Analysis, Insights and Forecast - by End-user Industry

- 9.3.1. General Industrial

- 9.3.2. Protective Coatings

- 9.3.2.1. Oil and Gas

- 9.3.2.2. Mining

- 9.3.2.3. Power

- 9.3.2.4. Infrastructure

- 9.3.2.5. Other Protective Coatings

- 9.1. Market Analysis, Insights and Forecast - by Resin

- 10. South America Industrial Coatings Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Resin

- 10.1.1. Epoxy

- 10.1.2. Polyurethane

- 10.1.3. Acrylic

- 10.1.4. Polyester

- 10.1.5. Other Resins

- 10.2. Market Analysis, Insights and Forecast - by Technology

- 10.2.1. Water-borne Coatings

- 10.2.2. Solvent-borne Coatings

- 10.2.3. Other Technologies

- 10.3. Market Analysis, Insights and Forecast - by End-user Industry

- 10.3.1. General Industrial

- 10.3.2. Protective Coatings

- 10.3.2.1. Oil and Gas

- 10.3.2.2. Mining

- 10.3.2.3. Power

- 10.3.2.4. Infrastructure

- 10.3.2.5. Other Protective Coatings

- 10.1. Market Analysis, Insights and Forecast - by Resin

- 11. Middle East Industrial Coatings Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Resin

- 11.1.1. Epoxy

- 11.1.2. Polyurethane

- 11.1.3. Acrylic

- 11.1.4. Polyester

- 11.1.5. Other Resins

- 11.2. Market Analysis, Insights and Forecast - by Technology

- 11.2.1. Water-borne Coatings

- 11.2.2. Solvent-borne Coatings

- 11.2.3. Other Technologies

- 11.3. Market Analysis, Insights and Forecast - by End-user Industry

- 11.3.1. General Industrial

- 11.3.2. Protective Coatings

- 11.3.2.1. Oil and Gas

- 11.3.2.2. Mining

- 11.3.2.3. Power

- 11.3.2.4. Infrastructure

- 11.3.2.5. Other Protective Coatings

- 11.1. Market Analysis, Insights and Forecast - by Resin

- 12. Saudi Arabia Industrial Coatings Industry Analysis, Insights and Forecast, 2021-2033

- 12.1. Market Analysis, Insights and Forecast - by Resin

- 12.1.1. Epoxy

- 12.1.2. Polyurethane

- 12.1.3. Acrylic

- 12.1.4. Polyester

- 12.1.5. Other Resins

- 12.2. Market Analysis, Insights and Forecast - by Technology

- 12.2.1. Water-borne Coatings

- 12.2.2. Solvent-borne Coatings

- 12.2.3. Other Technologies

- 12.3. Market Analysis, Insights and Forecast - by End-user Industry

- 12.3.1. General Industrial

- 12.3.2. Protective Coatings

- 12.3.2.1. Oil and Gas

- 12.3.2.2. Mining

- 12.3.2.3. Power

- 12.3.2.4. Infrastructure

- 12.3.2.5. Other Protective Coatings

- 12.1. Market Analysis, Insights and Forecast - by Resin

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 AkzoNobel N V

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Chugoku Marine Paints Ltd

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 The Sherwin-Williams Company

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Jotun

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 RPM International Inc

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Beckers Group

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 BASF SE

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Axalta Coating Systems

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Hempel A/S

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Sika AG

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 PPG Industries

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 Kansai Paint Co Ltd

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.13 Wacker Chemie AG*List Not Exhaustive

- 13.1.13.1. Company Overview

- 13.1.13.2. Products

- 13.1.13.3. Company Financials

- 13.1.13.4. SWOT Analysis

- 13.1.14 Nippon Paint ( NIPSEA GROUP)

- 13.1.14.1. Company Overview

- 13.1.14.2. Products

- 13.1.14.3. Company Financials

- 13.1.14.4. SWOT Analysis

- 13.1.1 AkzoNobel N V

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Industrial Coatings Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Industrial Coatings Industry Volume Breakdown (liter , %) by Region 2025 & 2033

- Figure 3: Asia Pacific Industrial Coatings Industry Revenue (billion), by Resin 2025 & 2033

- Figure 4: Asia Pacific Industrial Coatings Industry Volume (liter ), by Resin 2025 & 2033

- Figure 5: Asia Pacific Industrial Coatings Industry Revenue Share (%), by Resin 2025 & 2033

- Figure 6: Asia Pacific Industrial Coatings Industry Volume Share (%), by Resin 2025 & 2033

- Figure 7: Asia Pacific Industrial Coatings Industry Revenue (billion), by Technology 2025 & 2033

- Figure 8: Asia Pacific Industrial Coatings Industry Volume (liter ), by Technology 2025 & 2033

- Figure 9: Asia Pacific Industrial Coatings Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 10: Asia Pacific Industrial Coatings Industry Volume Share (%), by Technology 2025 & 2033

- Figure 11: Asia Pacific Industrial Coatings Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 12: Asia Pacific Industrial Coatings Industry Volume (liter ), by End-user Industry 2025 & 2033

- Figure 13: Asia Pacific Industrial Coatings Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 14: Asia Pacific Industrial Coatings Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 15: Asia Pacific Industrial Coatings Industry Revenue (billion), by Country 2025 & 2033

- Figure 16: Asia Pacific Industrial Coatings Industry Volume (liter ), by Country 2025 & 2033

- Figure 17: Asia Pacific Industrial Coatings Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Industrial Coatings Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: North America Industrial Coatings Industry Revenue (billion), by Resin 2025 & 2033

- Figure 20: North America Industrial Coatings Industry Volume (liter ), by Resin 2025 & 2033

- Figure 21: North America Industrial Coatings Industry Revenue Share (%), by Resin 2025 & 2033

- Figure 22: North America Industrial Coatings Industry Volume Share (%), by Resin 2025 & 2033

- Figure 23: North America Industrial Coatings Industry Revenue (billion), by Technology 2025 & 2033

- Figure 24: North America Industrial Coatings Industry Volume (liter ), by Technology 2025 & 2033

- Figure 25: North America Industrial Coatings Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 26: North America Industrial Coatings Industry Volume Share (%), by Technology 2025 & 2033

- Figure 27: North America Industrial Coatings Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 28: North America Industrial Coatings Industry Volume (liter ), by End-user Industry 2025 & 2033

- Figure 29: North America Industrial Coatings Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: North America Industrial Coatings Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 31: North America Industrial Coatings Industry Revenue (billion), by Country 2025 & 2033

- Figure 32: North America Industrial Coatings Industry Volume (liter ), by Country 2025 & 2033

- Figure 33: North America Industrial Coatings Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: North America Industrial Coatings Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Europe Industrial Coatings Industry Revenue (billion), by Resin 2025 & 2033

- Figure 36: Europe Industrial Coatings Industry Volume (liter ), by Resin 2025 & 2033

- Figure 37: Europe Industrial Coatings Industry Revenue Share (%), by Resin 2025 & 2033

- Figure 38: Europe Industrial Coatings Industry Volume Share (%), by Resin 2025 & 2033

- Figure 39: Europe Industrial Coatings Industry Revenue (billion), by Technology 2025 & 2033

- Figure 40: Europe Industrial Coatings Industry Volume (liter ), by Technology 2025 & 2033

- Figure 41: Europe Industrial Coatings Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 42: Europe Industrial Coatings Industry Volume Share (%), by Technology 2025 & 2033

- Figure 43: Europe Industrial Coatings Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 44: Europe Industrial Coatings Industry Volume (liter ), by End-user Industry 2025 & 2033

- Figure 45: Europe Industrial Coatings Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 46: Europe Industrial Coatings Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 47: Europe Industrial Coatings Industry Revenue (billion), by Country 2025 & 2033

- Figure 48: Europe Industrial Coatings Industry Volume (liter ), by Country 2025 & 2033

- Figure 49: Europe Industrial Coatings Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Europe Industrial Coatings Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: South America Industrial Coatings Industry Revenue (billion), by Resin 2025 & 2033

- Figure 52: South America Industrial Coatings Industry Volume (liter ), by Resin 2025 & 2033

- Figure 53: South America Industrial Coatings Industry Revenue Share (%), by Resin 2025 & 2033

- Figure 54: South America Industrial Coatings Industry Volume Share (%), by Resin 2025 & 2033

- Figure 55: South America Industrial Coatings Industry Revenue (billion), by Technology 2025 & 2033

- Figure 56: South America Industrial Coatings Industry Volume (liter ), by Technology 2025 & 2033

- Figure 57: South America Industrial Coatings Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 58: South America Industrial Coatings Industry Volume Share (%), by Technology 2025 & 2033

- Figure 59: South America Industrial Coatings Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 60: South America Industrial Coatings Industry Volume (liter ), by End-user Industry 2025 & 2033

- Figure 61: South America Industrial Coatings Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 62: South America Industrial Coatings Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 63: South America Industrial Coatings Industry Revenue (billion), by Country 2025 & 2033

- Figure 64: South America Industrial Coatings Industry Volume (liter ), by Country 2025 & 2033

- Figure 65: South America Industrial Coatings Industry Revenue Share (%), by Country 2025 & 2033

- Figure 66: South America Industrial Coatings Industry Volume Share (%), by Country 2025 & 2033

- Figure 67: Middle East Industrial Coatings Industry Revenue (billion), by Resin 2025 & 2033

- Figure 68: Middle East Industrial Coatings Industry Volume (liter ), by Resin 2025 & 2033

- Figure 69: Middle East Industrial Coatings Industry Revenue Share (%), by Resin 2025 & 2033

- Figure 70: Middle East Industrial Coatings Industry Volume Share (%), by Resin 2025 & 2033

- Figure 71: Middle East Industrial Coatings Industry Revenue (billion), by Technology 2025 & 2033

- Figure 72: Middle East Industrial Coatings Industry Volume (liter ), by Technology 2025 & 2033

- Figure 73: Middle East Industrial Coatings Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 74: Middle East Industrial Coatings Industry Volume Share (%), by Technology 2025 & 2033

- Figure 75: Middle East Industrial Coatings Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 76: Middle East Industrial Coatings Industry Volume (liter ), by End-user Industry 2025 & 2033

- Figure 77: Middle East Industrial Coatings Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 78: Middle East Industrial Coatings Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 79: Middle East Industrial Coatings Industry Revenue (billion), by Country 2025 & 2033

- Figure 80: Middle East Industrial Coatings Industry Volume (liter ), by Country 2025 & 2033

- Figure 81: Middle East Industrial Coatings Industry Revenue Share (%), by Country 2025 & 2033

- Figure 82: Middle East Industrial Coatings Industry Volume Share (%), by Country 2025 & 2033

- Figure 83: Saudi Arabia Industrial Coatings Industry Revenue (billion), by Resin 2025 & 2033

- Figure 84: Saudi Arabia Industrial Coatings Industry Volume (liter ), by Resin 2025 & 2033

- Figure 85: Saudi Arabia Industrial Coatings Industry Revenue Share (%), by Resin 2025 & 2033

- Figure 86: Saudi Arabia Industrial Coatings Industry Volume Share (%), by Resin 2025 & 2033

- Figure 87: Saudi Arabia Industrial Coatings Industry Revenue (billion), by Technology 2025 & 2033

- Figure 88: Saudi Arabia Industrial Coatings Industry Volume (liter ), by Technology 2025 & 2033

- Figure 89: Saudi Arabia Industrial Coatings Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 90: Saudi Arabia Industrial Coatings Industry Volume Share (%), by Technology 2025 & 2033

- Figure 91: Saudi Arabia Industrial Coatings Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 92: Saudi Arabia Industrial Coatings Industry Volume (liter ), by End-user Industry 2025 & 2033

- Figure 93: Saudi Arabia Industrial Coatings Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 94: Saudi Arabia Industrial Coatings Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 95: Saudi Arabia Industrial Coatings Industry Revenue (billion), by Country 2025 & 2033

- Figure 96: Saudi Arabia Industrial Coatings Industry Volume (liter ), by Country 2025 & 2033

- Figure 97: Saudi Arabia Industrial Coatings Industry Revenue Share (%), by Country 2025 & 2033

- Figure 98: Saudi Arabia Industrial Coatings Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Industrial Coatings Industry Revenue billion Forecast, by Resin 2020 & 2033

- Table 2: Global Industrial Coatings Industry Volume liter Forecast, by Resin 2020 & 2033

- Table 3: Global Industrial Coatings Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 4: Global Industrial Coatings Industry Volume liter Forecast, by Technology 2020 & 2033

- Table 5: Global Industrial Coatings Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Industrial Coatings Industry Volume liter Forecast, by End-user Industry 2020 & 2033

- Table 7: Global Industrial Coatings Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: Global Industrial Coatings Industry Volume liter Forecast, by Region 2020 & 2033

- Table 9: Global Industrial Coatings Industry Revenue billion Forecast, by Resin 2020 & 2033

- Table 10: Global Industrial Coatings Industry Volume liter Forecast, by Resin 2020 & 2033

- Table 11: Global Industrial Coatings Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 12: Global Industrial Coatings Industry Volume liter Forecast, by Technology 2020 & 2033

- Table 13: Global Industrial Coatings Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 14: Global Industrial Coatings Industry Volume liter Forecast, by End-user Industry 2020 & 2033

- Table 15: Global Industrial Coatings Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Industrial Coatings Industry Volume liter Forecast, by Country 2020 & 2033

- Table 17: China Industrial Coatings Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: China Industrial Coatings Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 19: India Industrial Coatings Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: India Industrial Coatings Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 21: Japan Industrial Coatings Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Japan Industrial Coatings Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 23: South Korea Industrial Coatings Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: South Korea Industrial Coatings Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 25: Rest of Asia Pacific Industrial Coatings Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Rest of Asia Pacific Industrial Coatings Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 27: Global Industrial Coatings Industry Revenue billion Forecast, by Resin 2020 & 2033

- Table 28: Global Industrial Coatings Industry Volume liter Forecast, by Resin 2020 & 2033

- Table 29: Global Industrial Coatings Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 30: Global Industrial Coatings Industry Volume liter Forecast, by Technology 2020 & 2033

- Table 31: Global Industrial Coatings Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 32: Global Industrial Coatings Industry Volume liter Forecast, by End-user Industry 2020 & 2033

- Table 33: Global Industrial Coatings Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 34: Global Industrial Coatings Industry Volume liter Forecast, by Country 2020 & 2033

- Table 35: United States Industrial Coatings Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: United States Industrial Coatings Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 37: Canada Industrial Coatings Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Canada Industrial Coatings Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 39: Mexico Industrial Coatings Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Mexico Industrial Coatings Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 41: Global Industrial Coatings Industry Revenue billion Forecast, by Resin 2020 & 2033

- Table 42: Global Industrial Coatings Industry Volume liter Forecast, by Resin 2020 & 2033

- Table 43: Global Industrial Coatings Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 44: Global Industrial Coatings Industry Volume liter Forecast, by Technology 2020 & 2033

- Table 45: Global Industrial Coatings Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 46: Global Industrial Coatings Industry Volume liter Forecast, by End-user Industry 2020 & 2033

- Table 47: Global Industrial Coatings Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 48: Global Industrial Coatings Industry Volume liter Forecast, by Country 2020 & 2033

- Table 49: Germany Industrial Coatings Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Germany Industrial Coatings Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 51: United Kingdom Industrial Coatings Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: United Kingdom Industrial Coatings Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 53: Italy Industrial Coatings Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Italy Industrial Coatings Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 55: France Industrial Coatings Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: France Industrial Coatings Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 57: Russia Industrial Coatings Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 58: Russia Industrial Coatings Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 59: Rest of Europe Industrial Coatings Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 60: Rest of Europe Industrial Coatings Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 61: Global Industrial Coatings Industry Revenue billion Forecast, by Resin 2020 & 2033

- Table 62: Global Industrial Coatings Industry Volume liter Forecast, by Resin 2020 & 2033

- Table 63: Global Industrial Coatings Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 64: Global Industrial Coatings Industry Volume liter Forecast, by Technology 2020 & 2033

- Table 65: Global Industrial Coatings Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 66: Global Industrial Coatings Industry Volume liter Forecast, by End-user Industry 2020 & 2033

- Table 67: Global Industrial Coatings Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 68: Global Industrial Coatings Industry Volume liter Forecast, by Country 2020 & 2033

- Table 69: Brazil Industrial Coatings Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: Brazil Industrial Coatings Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 71: Argentina Industrial Coatings Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Argentina Industrial Coatings Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 73: Rest of South America Industrial Coatings Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 74: Rest of South America Industrial Coatings Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 75: Global Industrial Coatings Industry Revenue billion Forecast, by Resin 2020 & 2033

- Table 76: Global Industrial Coatings Industry Volume liter Forecast, by Resin 2020 & 2033

- Table 77: Global Industrial Coatings Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 78: Global Industrial Coatings Industry Volume liter Forecast, by Technology 2020 & 2033

- Table 79: Global Industrial Coatings Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 80: Global Industrial Coatings Industry Volume liter Forecast, by End-user Industry 2020 & 2033

- Table 81: Global Industrial Coatings Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 82: Global Industrial Coatings Industry Volume liter Forecast, by Country 2020 & 2033

- Table 83: Global Industrial Coatings Industry Revenue billion Forecast, by Resin 2020 & 2033

- Table 84: Global Industrial Coatings Industry Volume liter Forecast, by Resin 2020 & 2033

- Table 85: Global Industrial Coatings Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 86: Global Industrial Coatings Industry Volume liter Forecast, by Technology 2020 & 2033

- Table 87: Global Industrial Coatings Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 88: Global Industrial Coatings Industry Volume liter Forecast, by End-user Industry 2020 & 2033

- Table 89: Global Industrial Coatings Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 90: Global Industrial Coatings Industry Volume liter Forecast, by Country 2020 & 2033

- Table 91: South Africa Industrial Coatings Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: South Africa Industrial Coatings Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 93: Rest of Middle East Industrial Coatings Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 94: Rest of Middle East Industrial Coatings Industry Volume (liter ) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Industrial Coatings Industry?

The projected CAGR is approximately 4.1%.

2. Which companies are prominent players in the Industrial Coatings Industry?

Key companies in the market include AkzoNobel N V, Chugoku Marine Paints Ltd, The Sherwin-Williams Company, Jotun, RPM International Inc, Beckers Group, BASF SE, Axalta Coating Systems, Hempel A/S, Sika AG, PPG Industries, Kansai Paint Co Ltd, Wacker Chemie AG*List Not Exhaustive, Nippon Paint ( NIPSEA GROUP).

3. What are the main segments of the Industrial Coatings Industry?

The market segments include Resin, Technology, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 96.72 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for Protective Coatings; Increasing Applications in Oil and Gas Industry.

6. What are the notable trends driving market growth?

Increasing Applications in Oil and Gas Industry.

7. Are there any restraints impacting market growth?

Harmful Environmental Impact Of Solvent-borne Coatings; Impact of COVID-19 Outbreak.

8. Can you provide examples of recent developments in the market?

August 2022: PPG said it would spend USD 11 million to double the amount of powder coatings it can make at its plant in San Juan del Rio, Mexico.The project to expand should be done by the middle of 2023. This will allow the plant to meet the expected demand for powder coatings in Mexico in the future.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in liter .

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Industrial Coatings Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Industrial Coatings Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Industrial Coatings Industry?

To stay informed about further developments, trends, and reports in the Industrial Coatings Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence