Key Insights

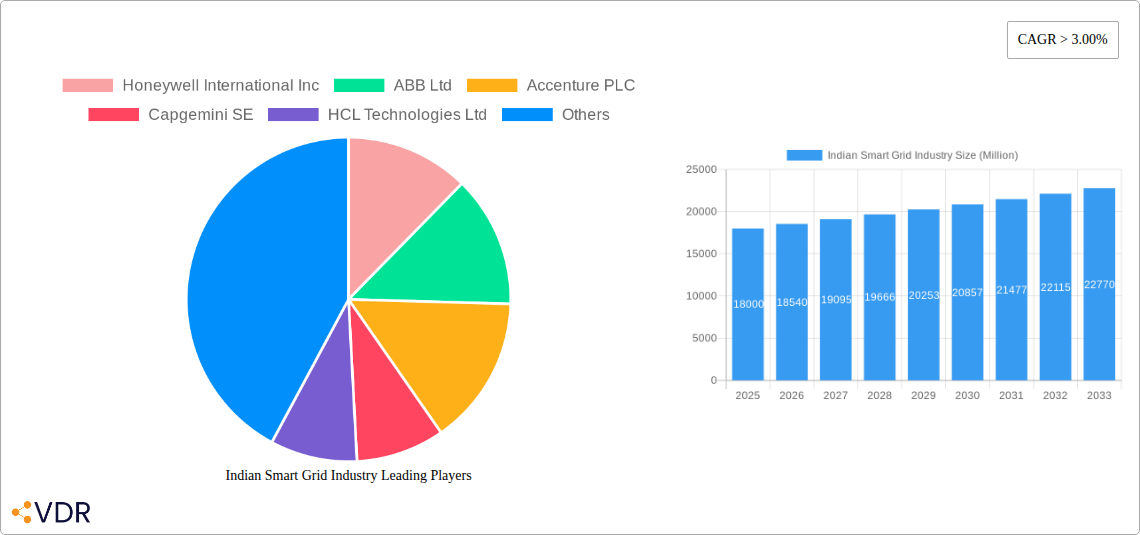

The Indian smart grid market is experiencing robust growth, driven by increasing electricity demand, the need for enhanced grid reliability, and the government's push for renewable energy integration. A compound annual growth rate (CAGR) exceeding 3% indicates a significant expansion over the forecast period (2025-2033). Key segments driving this growth include smart metering (AMI, smart meters, data concentrators), smart transmission and distribution (smart transformers, switches, sensors), and smart substations (digital substations, SCADA systems). The integration of advanced software and analytics (SCADA, DMS, EMS, AMI software) further enhances grid efficiency and operational capabilities. While data scarcity prevents precise quantification of the Indian market size, considering global trends and the country's substantial energy needs, a conservative estimate places the 2025 market value at approximately ₹150 billion (approximately $18 billion USD). This figure is expected to climb significantly by 2033, propelled by ongoing infrastructure development and a growing focus on sustainable energy practices.

Major players like Honeywell, ABB, Siemens, and Schneider Electric are actively participating in the Indian smart grid deployment, alongside domestic players like Power Grid Corporation of India. However, challenges such as high initial investment costs, regulatory hurdles, and the need for skilled workforce remain. Overcoming these obstacles through public-private partnerships, targeted policy reforms, and skills development initiatives will be crucial for realizing the full potential of the Indian smart grid market. The market is segmented geographically, with significant opportunities across diverse regions within India, reflecting varying levels of infrastructure development and energy consumption patterns. Future growth will hinge on effective technology adoption, strong policy support, and successful collaborations between industry stakeholders and the government.

Indian Smart Grid Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Indian smart grid industry, covering market dynamics, growth trends, key players, and future outlook. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report offers invaluable insights for industry professionals, investors, and policymakers. The report delves into the parent market of energy infrastructure and the child markets of smart metering, smart transmission and distribution, smart substations, and smart grid software and analytics.

Indian Smart Grid Industry Market Dynamics & Structure

This section analyzes the competitive landscape, technological advancements, regulatory environment, and market trends within the Indian smart grid industry. The market is characterized by a mix of established international players and emerging domestic companies.

Market Concentration: The market exhibits moderate concentration, with key players like Honeywell International Inc, ABB Ltd, Accenture PLC, Capgemini SE, HCL Technologies Ltd, Siemens AG, Cisco Systems Inc, Schneider Electric SE, General Electric Company, and Power Grid Corporation of India Limited holding significant market share. However, the market is also witnessing the emergence of several smaller, specialized companies. The overall market share of the top 5 players is estimated at xx%.

Technological Innovation: Key drivers of innovation include the integration of advanced metering infrastructure (AMI), the adoption of Internet of Things (IoT) technologies, and the increasing deployment of artificial intelligence (AI) and machine learning (ML) for grid management. Barriers to innovation include high initial investment costs and a lack of skilled workforce.

Regulatory Framework: The Indian government's initiatives promoting renewable energy integration and smart grid adoption are creating favorable conditions for market growth. However, inconsistent regulatory policies across different states can pose challenges.

Competitive Product Substitutes: While there are no direct substitutes for smart grid technologies, traditional grid infrastructure remains a competitive alternative, particularly in areas with limited investment capacity.

End-User Demographics: The primary end-users are power distribution companies (DISCOMs), transmission utilities, and large industrial consumers.

M&A Trends: The number of M&A deals in the Indian smart grid sector increased by xx% in 2022 compared to 2021, primarily driven by consolidation among smaller players and strategic acquisitions by larger companies.

Indian Smart Grid Industry Growth Trends & Insights

The Indian smart grid market is experiencing robust growth, driven by increasing electricity demand, government initiatives promoting energy efficiency, and the need to modernize aging infrastructure. The market size, currently valued at xx Million in 2025, is projected to reach xx Million by 2033, exhibiting a CAGR of xx% during the forecast period (2025-2033). Smart meter adoption is a key growth driver, fueled by government mandates and consumer demand for improved billing accuracy and prepaid options. Technological advancements, such as the integration of AI/ML for predictive maintenance and grid optimization, are further accelerating market expansion. Consumer behavior is shifting towards greater energy consciousness and a preference for digitalized billing and payment solutions.

Dominant Regions, Countries, or Segments in Indian Smart Grid Industry

The smart metering segment currently holds the largest market share due to the government's focus on AMI deployment. States such as Uttar Pradesh and Maharashtra are leading the adoption of smart meters, driven by large-scale tender awards. The smart transmission and distribution segment is expected to experience significant growth in the coming years, propelled by investments in grid modernization and expansion. Urban areas with high electricity demand are showing greater adoption rates compared to rural areas due to better infrastructure and higher consumer awareness. Key growth drivers include:

- Government Policies: The Indian government's initiatives promoting renewable energy integration and smart grid adoption.

- Infrastructure Development: Investment in grid modernization and expansion projects.

- Technological Advancements: The emergence of new technologies such as AI and IoT.

- Economic Growth: The continuous growth of the Indian economy driving up energy consumption.

Indian Smart Grid Industry Product Landscape

The Indian smart grid market offers a wide range of products, including advanced metering infrastructure (AMI) systems, smart transformers, smart sensors, SCADA systems, and grid management software. These products are characterized by increasing levels of sophistication and integration, with features such as remote monitoring, real-time data analysis, and predictive maintenance capabilities. Key differentiators include cost-effectiveness, ease of installation, and compatibility with existing infrastructure.

Key Drivers, Barriers & Challenges in Indian Smart Grid Industry

Key Drivers:

- Government initiatives promoting smart grid deployment.

- Increasing demand for reliable and efficient power supply.

- Technological advancements enabling cost-effective solutions.

Challenges:

- High initial investment costs for smart grid technologies.

- Lack of skilled workforce for installation and maintenance.

- Complex regulatory landscape and inter-agency coordination challenges. This leads to delays in project implementation and increased costs. The impact is estimated to be a xx% delay in project completion in some cases.

Emerging Opportunities in Indian Smart Grid Industry

Emerging opportunities include the growing demand for distributed generation solutions, the integration of electric vehicles (EVs) into the grid, and the expansion of smart grid solutions to rural areas. The use of blockchain technology for enhanced security and transparency in energy transactions also presents a significant opportunity.

Growth Accelerators in the Indian Smart Grid Industry

Long-term growth will be driven by continued government support, technological innovation, and strategic partnerships between domestic and international companies. Expansion into rural areas and the integration of smart grid technologies with other infrastructure systems such as water and gas will create significant new market opportunities.

Key Players Shaping the Indian Smart Grid Industry Market

- Honeywell International Inc

- ABB Ltd

- Accenture PLC

- Capgemini SE

- HCL Technologies Ltd

- Siemens AG

- Cisco Systems Inc

- Schneider Electric SE

- General Electric Company

- Power Grid Corporation of India Limited

Notable Milestones in Indian Smart Grid Industry Sector

- October 2022: Bids submitted for installation of approximately 28.5 Million prepaid smart meters in Uttar Pradesh.

- February 2023: BEST announces plans to install smart meters for 1.05 Million consumers in Mumbai.

In-Depth Indian Smart Grid Industry Market Outlook

The Indian smart grid market is poised for sustained growth, driven by strong government support, increasing energy demand, and technological advancements. The integration of renewable energy sources and the development of smart cities will further fuel market expansion. Strategic partnerships and investments in research and development will play a crucial role in shaping the future of the Indian smart grid industry. Opportunities exist for companies to capitalize on this growth by offering innovative, cost-effective, and reliable solutions.

Indian Smart Grid Industry Segmentation

- 1. Transmission

- 2. Advanced Metering Infrastructure (AMI)

- 3. Communication Technology

- 4. Other Technology Application Areas

Indian Smart Grid Industry Segmentation By Geography

- 1. India

Indian Smart Grid Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 3.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Growing Power Demand from the Commercial and Industrial Sectors

- 3.3. Market Restrains

- 3.3.1. 4.; Stringent Environmental and Safety Regulations

- 3.4. Market Trends

- 3.4.1. Advanced Metering Infrastructure (AMI) is Expected to Witness Significant Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Indian Smart Grid Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Transmission

- 5.2. Market Analysis, Insights and Forecast - by Advanced Metering Infrastructure (AMI)

- 5.3. Market Analysis, Insights and Forecast - by Communication Technology

- 5.4. Market Analysis, Insights and Forecast - by Other Technology Application Areas

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. India

- 5.1. Market Analysis, Insights and Forecast - by Transmission

- 6. China Indian Smart Grid Industry Analysis, Insights and Forecast, 2019-2031

- 7. Japan Indian Smart Grid Industry Analysis, Insights and Forecast, 2019-2031

- 8. India Indian Smart Grid Industry Analysis, Insights and Forecast, 2019-2031

- 9. South Korea Indian Smart Grid Industry Analysis, Insights and Forecast, 2019-2031

- 10. Taiwan Indian Smart Grid Industry Analysis, Insights and Forecast, 2019-2031

- 11. Australia Indian Smart Grid Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Asia-Pacific Indian Smart Grid Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Honeywell International Inc

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 ABB Ltd

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Accenture PLC

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Capgemini SE

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 HCL Technologies Ltd

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Siemens AG*List Not Exhaustive

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Cisco Systems Inc

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Schneider Electric SE

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 General Electric Company

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Power Grid Corporation of India Limited

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.1 Honeywell International Inc

List of Figures

- Figure 1: Indian Smart Grid Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Indian Smart Grid Industry Share (%) by Company 2024

List of Tables

- Table 1: Indian Smart Grid Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Indian Smart Grid Industry Revenue Million Forecast, by Transmission 2019 & 2032

- Table 3: Indian Smart Grid Industry Revenue Million Forecast, by Advanced Metering Infrastructure (AMI) 2019 & 2032

- Table 4: Indian Smart Grid Industry Revenue Million Forecast, by Communication Technology 2019 & 2032

- Table 5: Indian Smart Grid Industry Revenue Million Forecast, by Other Technology Application Areas 2019 & 2032

- Table 6: Indian Smart Grid Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 7: Indian Smart Grid Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: China Indian Smart Grid Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Japan Indian Smart Grid Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: India Indian Smart Grid Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: South Korea Indian Smart Grid Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Taiwan Indian Smart Grid Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Australia Indian Smart Grid Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Rest of Asia-Pacific Indian Smart Grid Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Indian Smart Grid Industry Revenue Million Forecast, by Transmission 2019 & 2032

- Table 16: Indian Smart Grid Industry Revenue Million Forecast, by Advanced Metering Infrastructure (AMI) 2019 & 2032

- Table 17: Indian Smart Grid Industry Revenue Million Forecast, by Communication Technology 2019 & 2032

- Table 18: Indian Smart Grid Industry Revenue Million Forecast, by Other Technology Application Areas 2019 & 2032

- Table 19: Indian Smart Grid Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Indian Smart Grid Industry?

The projected CAGR is approximately > 3.00%.

2. Which companies are prominent players in the Indian Smart Grid Industry?

Key companies in the market include Honeywell International Inc, ABB Ltd, Accenture PLC, Capgemini SE, HCL Technologies Ltd, Siemens AG*List Not Exhaustive, Cisco Systems Inc, Schneider Electric SE, General Electric Company, Power Grid Corporation of India Limited.

3. What are the main segments of the Indian Smart Grid Industry?

The market segments include Transmission, Advanced Metering Infrastructure (AMI), Communication Technology, Other Technology Application Areas.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Growing Power Demand from the Commercial and Industrial Sectors.

6. What are the notable trends driving market growth?

Advanced Metering Infrastructure (AMI) is Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

4.; Stringent Environmental and Safety Regulations.

8. Can you provide examples of recent developments in the market?

February 2023: The Brihanmumbai Electric Supply and Transport (BEST) announced that the company is likely to start installing smart meters for its 10.5 lakh power consumers from March 2023 onward. These devices will be enabled with 4G and 5G SIM cards and will offer pre-paid payment options for consumers.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Indian Smart Grid Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Indian Smart Grid Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Indian Smart Grid Industry?

To stay informed about further developments, trends, and reports in the Indian Smart Grid Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence