Key Insights

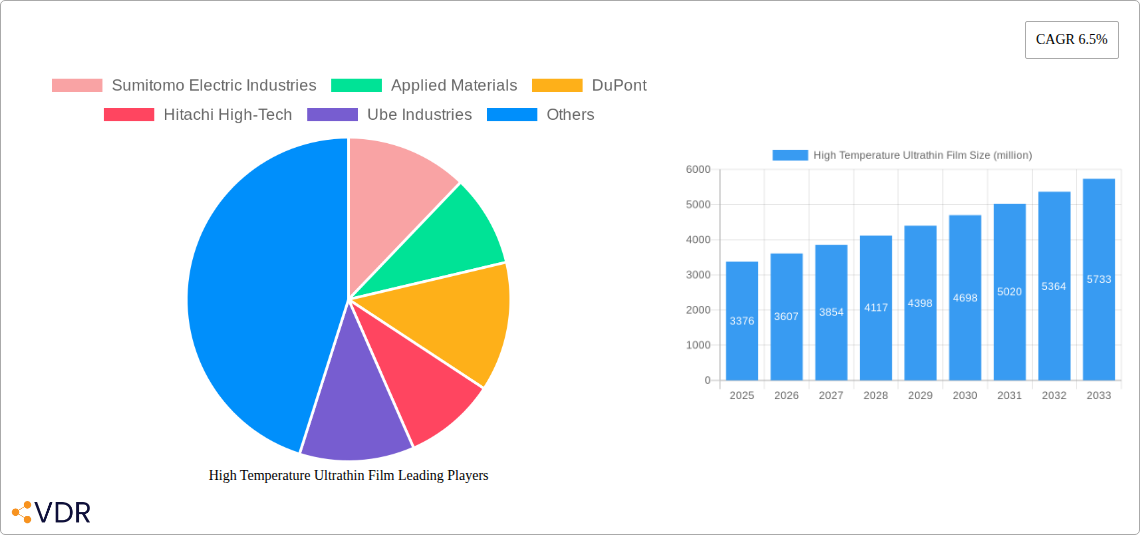

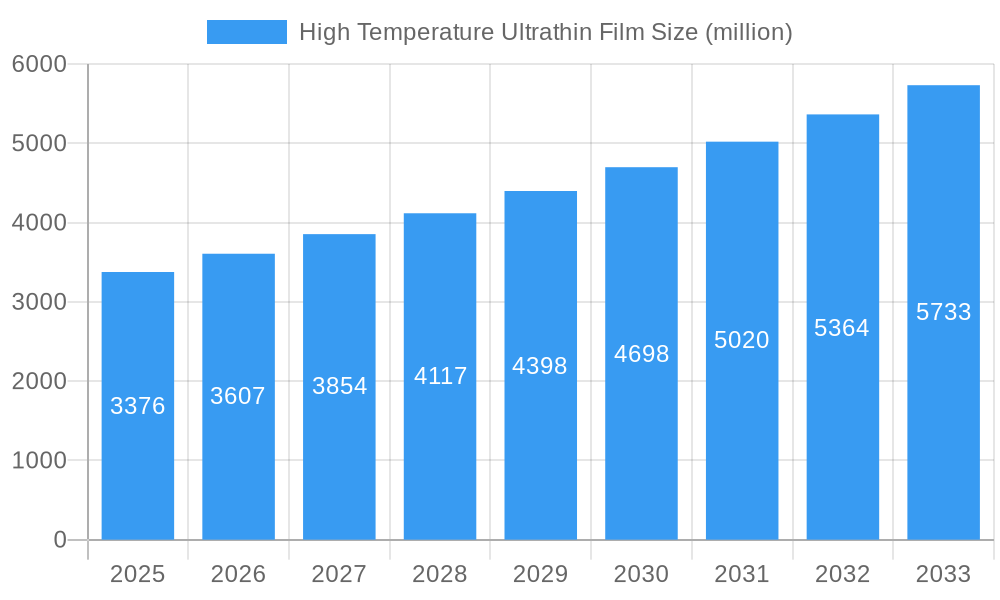

The High Temperature Ultrathin Film market is poised for robust growth, projected to reach an estimated \$3376 million by 2025. Driven by a compelling compound annual growth rate (CAGR) of 6.5% from 2025 to 2033, this sector is experiencing significant expansion fueled by an increasing demand for advanced materials in critical industries. The electronics and semiconductors sector is a primary beneficiary, leveraging these films for enhanced device performance and miniaturization. The energy sector is also a key driver, with applications in solar cells, batteries, and advanced power management systems benefiting from the unique properties of ultrathin films at elevated temperatures. Furthermore, the aerospace industry is increasingly adopting these materials for their lightweight and high-strength characteristics, contributing to improved fuel efficiency and performance in extreme conditions. Emerging trends point towards the development of novel film compositions and deposition techniques that further enhance thermal stability and electrical conductivity, opening up new avenues for innovation.

High Temperature Ultrathin Film Market Size (In Billion)

The market's trajectory is further supported by advancements in silicon-based films, which offer superior performance and scalability for various applications. While metal/alloy films continue to hold a significant share, ongoing research and development are expanding the utility of alternative materials. However, the market is not without its challenges. High manufacturing costs associated with precise deposition processes and the need for specialized equipment can act as restraints. Supply chain complexities for rare earth materials and stringent quality control requirements also present hurdles. Despite these factors, the overarching trend of technological miniaturization, increasing energy efficiency demands, and the relentless pursuit of higher performance across diverse industries are expected to propel the High Temperature Ultrathin Film market forward. The increasing adoption in emerging applications like advanced displays and next-generation sensors will further solidify its growth trajectory.

High Temperature Ultrathin Film Company Market Share

High Temperature Ultrathin Film Market Analysis: Navigating Extreme Environments for Advanced Applications (2019-2033)

This comprehensive report delves into the High Temperature Ultrathin Film Market, a critical sector fueling innovation across Electronics and Semiconductors, Energy, and Aerospace. With a robust study period spanning 2019–2033, including a base year of 2025 and a forecast period of 2025–2033, this analysis offers unparalleled insights into market dynamics, growth trajectories, and emerging opportunities. We dissect the market into key segments, including Metal/Alloy Film, Silicon-Based Film, and Other types, providing granular analysis of their respective contributions to the global market. Quantified in million units, our data paints a clear picture of the market's present state and future potential.

High Temperature Ultrathin Film Market Dynamics & Structure

The High Temperature Ultrathin Film market exhibits a moderately concentrated structure, with key players like Sumitomo Electric Industries, Applied Materials, DuPont, and Hitachi High-Tech holding significant shares. Technological innovation is the primary driver, fueled by the escalating demand for materials that can withstand extreme thermal stresses in advanced electronics, renewable energy systems, and aerospace components. Regulatory frameworks, particularly those related to environmental impact and material safety, play an increasingly influential role in shaping product development and market entry. Competitive product substitutes, while present, often lack the specialized performance characteristics of ultrathin films in high-temperature environments. End-user demographics are shifting towards industries requiring miniaturization, enhanced durability, and superior thermal management, driving demand for sophisticated solutions. Mergers and acquisitions (M&A) are a growing trend, as larger entities seek to consolidate market positions and acquire proprietary technologies, exemplified by X reported M&A deals in the historical period, valued at $XX million.

- Market Concentration: Moderately concentrated, with a few dominant players and a growing number of specialized niche providers.

- Technological Innovation Drivers: Miniaturization of electronic devices, demand for higher energy efficiency in power generation and storage, and the need for lighter, more resilient aerospace materials.

- Regulatory Frameworks: Increasing focus on stringent material performance standards for extreme environments and sustainable manufacturing practices.

- Competitive Product Substitutes: Traditional thick films and bulk materials, often lacking the performance density and specific properties of ultrathin films.

- End-User Demographics: High growth in industries such as 5G infrastructure, electric vehicles, advanced computing, and next-generation power grids.

- M&A Trends: Consolidation aimed at acquiring intellectual property and expanding product portfolios, with an estimated X significant M&A transactions in the forecast period.

High Temperature Ultrathin Film Growth Trends & Insights

The High Temperature Ultrathin Film market is poised for substantial growth, driven by the insatiable demand for advanced materials capable of operating under extreme thermal conditions. The market size is projected to expand from $XX million in 2019 to an estimated $XX million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of XX% during the forecast period (2025–2033). Adoption rates are accelerating across key application sectors, particularly in the Electronics and Semiconductors segment, where ultrathin films are integral to the production of high-performance processors, advanced memory devices, and robust power electronics that generate minimal heat and operate reliably at elevated temperatures. The Energy sector is witnessing significant uptake for applications in solar cells, high-temperature fuel cells, and advanced battery technologies, contributing XX% to the overall market share. Furthermore, the Aerospace industry's relentless pursuit of lighter, stronger, and more heat-resistant components for jet engines, spacecraft, and satellite systems is a major growth catalyst. Technological disruptions, including advancements in deposition techniques like Atomic Layer Deposition (ALD) and Chemical Vapor Deposition (CVD), are enabling the creation of films with unprecedented precision, uniformity, and thermal stability. Consumer behavior shifts are indirectly impacting this market, as the demand for more powerful and efficient electronic devices, electric vehicles, and sustainable energy solutions necessitates the use of these high-performance materials. The market penetration of high-temperature ultrathin films is expected to increase from XX% in 2019 to an anticipated XX% by 2033, underscoring their growing indispensability.

Dominant Regions, Countries, or Segments in High Temperature Ultrathin Film

The Electronics and Semiconductors segment stands as the undeniable leader in the High Temperature Ultrathin Film market, driving global demand and innovation. This segment is projected to contribute an estimated XX% to the total market value by 2033. The dominance of this application is fueled by the relentless miniaturization and performance enhancement requirements in consumer electronics, telecommunications infrastructure (especially 5G deployment), automotive electronics, and high-performance computing. Countries with robust semiconductor manufacturing capabilities, such as South Korea, Taiwan, and the United States, are at the forefront of this demand. Economic policies supporting advanced manufacturing, significant R&D investments in material science, and the presence of major semiconductor fabrication plants act as key drivers.

Within the Type segment, Metal/Alloy Films are expected to maintain a significant market share, estimated at XX%, due to their excellent thermal conductivity, electrical properties, and durability under high-temperature conditions. Applications range from interconnects and diffusion barriers in integrated circuits to protective coatings and thermal management layers.

The Energy sector, particularly in applications like high-efficiency solar panels and advanced battery technologies, is also a substantial growth area, expected to capture XX% of the market by 2033. Countries investing heavily in renewable energy infrastructure and advanced power storage solutions, such as China and Germany, are key contributors to this segment's growth. Government incentives for clean energy technologies and the increasing global focus on energy independence further bolster this demand.

The Aerospace segment, while a smaller contributor in terms of volume currently, represents a high-value niche market, driven by the stringent performance requirements for aircraft and spacecraft components. Advancements in materials science for extreme environments are crucial for this sector, with the United States and European Union nations leading in R&D and adoption.

- Dominant Application Segment: Electronics and Semiconductors (XX% projected market share by 2033).

- Key Drivers for Dominance: Miniaturization, 5G infrastructure, automotive electronics, high-performance computing.

- Leading Countries: South Korea, Taiwan, United States (for Electronics & Semiconductors).

- Dominant Film Type: Metal/Alloy Films (XX% projected market share).

- Key Drivers for Energy Segment: Renewable energy investment, advanced battery technologies, government incentives.

- Leading Countries for Energy: China, Germany.

- Growth Potential in Aerospace: High-value niche, driven by extreme environment requirements.

High Temperature Ultrathin Film Product Landscape

The product landscape of high-temperature ultrathin films is characterized by ongoing innovation focused on enhancing thermal stability, electrical conductivity, and mechanical integrity. Sumitomo Electric Industries is renowned for its advanced metal/alloy films offering exceptional performance in demanding semiconductor applications. Applied Materials consistently pushes the boundaries with deposition technologies enabling the precise fabrication of ultrathin films for a wide array of electronics. DuPont provides specialized silicon-based films and composite materials crucial for high-temperature insulation and protection in energy and aerospace sectors. Hitachi High-Tech offers sophisticated equipment and materials for fabricating ultrathin films with superior uniformity and purity. Performance metrics such as maximum operating temperature (often exceeding 500°C), film thickness (ranging from nanometers to a few micrometers), and electrical resistivity are key differentiators. Unique selling propositions include tailored film compositions for specific applications and improved adhesion properties under extreme thermal cycling.

Key Drivers, Barriers & Challenges in High Temperature Ultrathin Film

The High Temperature Ultrathin Film market is propelled by several key drivers. The ever-increasing demand for smaller, more powerful, and more reliable electronic devices is a primary force, especially in the Electronics and Semiconductors sector. Advancements in renewable energy technologies, such as high-temperature solar cells and advanced battery systems, create significant opportunities. The stringent requirements of the Aerospace industry for lightweight, heat-resistant components further fuel innovation. Technological breakthroughs in deposition techniques like ALD and CVD enable the precise manufacturing of these advanced materials.

- Key Drivers:

- Miniaturization and performance demands in Electronics & Semiconductors.

- Growth of renewable energy technologies and energy storage solutions.

- Stringent performance requirements in the Aerospace industry.

- Technological advancements in deposition methods (ALD, CVD).

However, the market faces several barriers and challenges. The high cost of raw materials and the sophisticated manufacturing processes required for ultrathin films contribute to a higher price point. Scaling up production while maintaining stringent quality control remains a significant hurdle. Supply chain disruptions for specialized precursor materials can impact availability and lead times, as evidenced by the XX% increase in lead times during recent global disruptions. Regulatory compliance for new materials and their environmental impact can also be a lengthy and costly process. Competitive pressures from alternative materials, although often not directly comparable, can also pose a challenge.

- Key Barriers & Challenges:

- High production costs due to specialized materials and processes.

- Challenges in scaling up manufacturing while maintaining quality.

- Vulnerability to supply chain disruptions for precursor materials.

- Stringent regulatory compliance and environmental impact assessments.

- Competition from alternative material solutions.

Emerging Opportunities in High Temperature Ultrathin Film

Emerging opportunities in the High Temperature Ultrathin Film market lie in niche but rapidly growing applications. The development of next-generation sensors capable of operating in extreme industrial environments (e.g., oil and gas exploration, chemical processing) presents a significant avenue. Advancements in wearable electronics that require robust, flexible, and thermally stable films are another area of high potential. The burgeoning field of quantum computing, which necessitates highly specialized materials for cryogenic and high-temperature shielding, also offers lucrative prospects. Furthermore, the integration of ultrathin films into biomedical devices that require sterilization at high temperatures or prolonged implant durations will open new frontiers.

Growth Accelerators in the High Temperature Ultrathin Film Industry

Several catalysts are accelerating growth in the High Temperature Ultrathin Film industry. Continuous research and development efforts are yielding novel film compositions with enhanced thermal and electrical properties. Strategic partnerships between material manufacturers and end-product innovators are crucial for co-developing tailor-made solutions and accelerating market adoption. The increasing global investment in advanced manufacturing infrastructure and the growing awareness of the critical role these materials play in enabling next-generation technologies are significant growth accelerators. Furthermore, the push for sustainable energy solutions and the electrification of transportation are creating sustained demand for high-performance materials.

Key Players Shaping the High Temperature Ultrathin Film Market

- Sumitomo Electric Industries

- Applied Materials

- DuPont

- Hitachi High-Tech

- Ube Industries

- NATL RES INST FOR METALS

- Honeywell

- Mitsui Chemicals

- BGI

Notable Milestones in High Temperature Ultrathin Film Sector

- 2019: Sumitomo Electric Industries announces breakthrough in developing ultrathin films with enhanced thermal conductivity for advanced cooling solutions in electronics.

- 2020: Applied Materials introduces a new generation of deposition tools enabling finer control over ultrathin film growth for next-gen semiconductors.

- 2021 (Q3): DuPont expands its portfolio of high-temperature dielectric films for critical applications in the energy sector.

- 2022: Hitachi High-Tech showcases advancements in ultrathin film characterization techniques, improving quality control for aerospace applications.

- 2023 (H1): Ube Industries partners with a leading automotive manufacturer to integrate ultrathin films into next-generation electric vehicle battery components.

- 2024 (Q4): NATL RES INST FOR METALS publishes research on novel ceramic ultrathin films with unprecedented thermal stability.

In-Depth High Temperature Ultrathin Film Market Outlook

The future of the High Temperature Ultrathin Film market is exceptionally bright, driven by a confluence of technological advancements and escalating industry demands. Growth accelerators such as continued breakthroughs in material science, the proliferation of 5G networks, and the urgent need for efficient energy storage and electric vehicle components will sustain robust market expansion. Strategic collaborations between leading companies like Applied Materials and application-specific innovators will be instrumental in developing customized solutions that address complex engineering challenges. The market's trajectory is firmly set towards increasing adoption across emerging sectors, promising significant value creation and the enablement of transformative technologies in the years to come. The market is projected to reach $XX million by 2033, with a consistent CAGR of XX%.

High Temperature Ultrathin Film Segmentation

-

1. Application

- 1.1. Electronics and Semiconductors

- 1.2. Energy

- 1.3. Aerospace

- 1.4. Other

-

2. Type

- 2.1. Metal/Alloy Film

- 2.2. Silicon-Based Film

- 2.3. Other

High Temperature Ultrathin Film Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

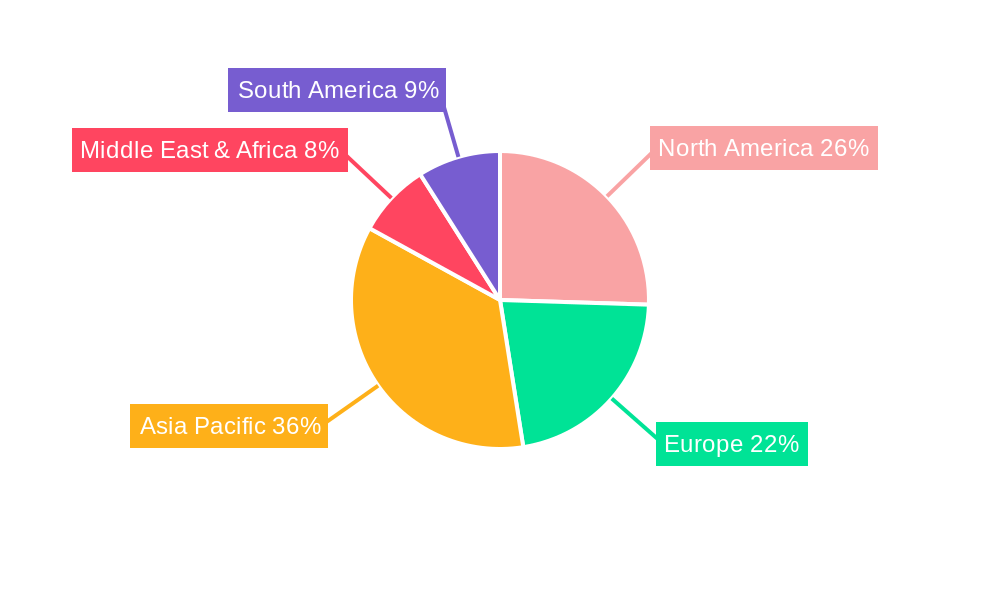

High Temperature Ultrathin Film Regional Market Share

Geographic Coverage of High Temperature Ultrathin Film

High Temperature Ultrathin Film REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Electronics and Semiconductors

- 5.1.2. Energy

- 5.1.3. Aerospace

- 5.1.4. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Metal/Alloy Film

- 5.2.2. Silicon-Based Film

- 5.2.3. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global High Temperature Ultrathin Film Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Electronics and Semiconductors

- 6.1.2. Energy

- 6.1.3. Aerospace

- 6.1.4. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Metal/Alloy Film

- 6.2.2. Silicon-Based Film

- 6.2.3. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America High Temperature Ultrathin Film Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Electronics and Semiconductors

- 7.1.2. Energy

- 7.1.3. Aerospace

- 7.1.4. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Metal/Alloy Film

- 7.2.2. Silicon-Based Film

- 7.2.3. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America High Temperature Ultrathin Film Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Electronics and Semiconductors

- 8.1.2. Energy

- 8.1.3. Aerospace

- 8.1.4. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Metal/Alloy Film

- 8.2.2. Silicon-Based Film

- 8.2.3. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe High Temperature Ultrathin Film Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Electronics and Semiconductors

- 9.1.2. Energy

- 9.1.3. Aerospace

- 9.1.4. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Metal/Alloy Film

- 9.2.2. Silicon-Based Film

- 9.2.3. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa High Temperature Ultrathin Film Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Electronics and Semiconductors

- 10.1.2. Energy

- 10.1.3. Aerospace

- 10.1.4. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Metal/Alloy Film

- 10.2.2. Silicon-Based Film

- 10.2.3. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific High Temperature Ultrathin Film Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Electronics and Semiconductors

- 11.1.2. Energy

- 11.1.3. Aerospace

- 11.1.4. Other

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Metal/Alloy Film

- 11.2.2. Silicon-Based Film

- 11.2.3. Other

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Sumitomo Electric Industries

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Applied Materials

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 DuPont

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Hitachi High-Tech

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Ube Industries

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 NATL RES INST FOR METALS

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Honeywell

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Mitsui Chemicals

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 BGI

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 Sumitomo Electric Industries

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global High Temperature Ultrathin Film Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America High Temperature Ultrathin Film Revenue (million), by Application 2025 & 2033

- Figure 3: North America High Temperature Ultrathin Film Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America High Temperature Ultrathin Film Revenue (million), by Type 2025 & 2033

- Figure 5: North America High Temperature Ultrathin Film Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America High Temperature Ultrathin Film Revenue (million), by Country 2025 & 2033

- Figure 7: North America High Temperature Ultrathin Film Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America High Temperature Ultrathin Film Revenue (million), by Application 2025 & 2033

- Figure 9: South America High Temperature Ultrathin Film Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America High Temperature Ultrathin Film Revenue (million), by Type 2025 & 2033

- Figure 11: South America High Temperature Ultrathin Film Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America High Temperature Ultrathin Film Revenue (million), by Country 2025 & 2033

- Figure 13: South America High Temperature Ultrathin Film Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe High Temperature Ultrathin Film Revenue (million), by Application 2025 & 2033

- Figure 15: Europe High Temperature Ultrathin Film Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe High Temperature Ultrathin Film Revenue (million), by Type 2025 & 2033

- Figure 17: Europe High Temperature Ultrathin Film Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe High Temperature Ultrathin Film Revenue (million), by Country 2025 & 2033

- Figure 19: Europe High Temperature Ultrathin Film Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa High Temperature Ultrathin Film Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa High Temperature Ultrathin Film Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa High Temperature Ultrathin Film Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa High Temperature Ultrathin Film Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa High Temperature Ultrathin Film Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa High Temperature Ultrathin Film Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific High Temperature Ultrathin Film Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific High Temperature Ultrathin Film Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific High Temperature Ultrathin Film Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific High Temperature Ultrathin Film Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific High Temperature Ultrathin Film Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific High Temperature Ultrathin Film Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global High Temperature Ultrathin Film Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global High Temperature Ultrathin Film Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global High Temperature Ultrathin Film Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global High Temperature Ultrathin Film Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global High Temperature Ultrathin Film Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global High Temperature Ultrathin Film Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global High Temperature Ultrathin Film Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global High Temperature Ultrathin Film Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global High Temperature Ultrathin Film Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global High Temperature Ultrathin Film Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global High Temperature Ultrathin Film Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global High Temperature Ultrathin Film Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global High Temperature Ultrathin Film Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global High Temperature Ultrathin Film Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global High Temperature Ultrathin Film Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global High Temperature Ultrathin Film Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global High Temperature Ultrathin Film Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global High Temperature Ultrathin Film Revenue million Forecast, by Country 2020 & 2033

- Table 40: China High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific High Temperature Ultrathin Film Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the High Temperature Ultrathin Film?

The projected CAGR is approximately 6.5%.

2. Which companies are prominent players in the High Temperature Ultrathin Film?

Key companies in the market include Sumitomo Electric Industries, Applied Materials, DuPont, Hitachi High-Tech, Ube Industries, NATL RES INST FOR METALS, Honeywell, Mitsui Chemicals, BGI.

3. What are the main segments of the High Temperature Ultrathin Film?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 3376 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "High Temperature Ultrathin Film," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the High Temperature Ultrathin Film report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the High Temperature Ultrathin Film?

To stay informed about further developments, trends, and reports in the High Temperature Ultrathin Film, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence