Key Insights

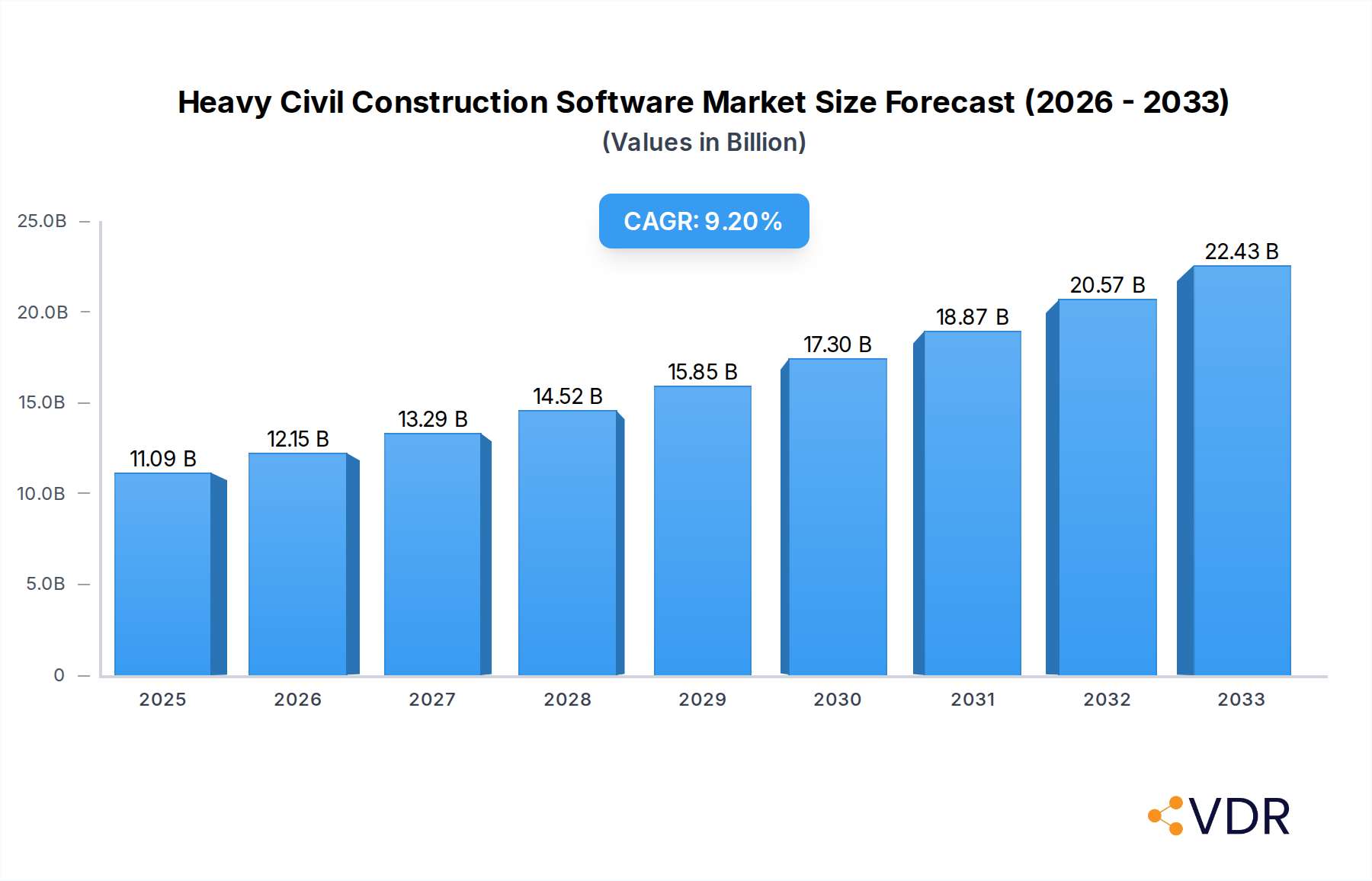

The global Heavy Civil Construction Software market is poised for robust expansion, projected to reach $11.09 billion in 2025 and grow at a compelling Compound Annual Growth Rate (CAGR) of 9.6% through 2033. This significant market value underscores the increasing adoption of digital solutions within the heavy civil sector, a trend driven by the demand for enhanced efficiency, improved project management, and greater cost control. Key drivers fueling this growth include the ongoing global infrastructure development and modernization initiatives, the necessity for streamlined project workflows in complex civil projects, and the rising emphasis on data-driven decision-making to mitigate risks and optimize resource allocation. Furthermore, the software solutions are becoming indispensable for managing large-scale projects like bridges, roads, dams, and public transit systems, where meticulous planning, real-time tracking, and precise execution are paramount. The industry's inherent complexity and the scale of capital investment necessitate advanced tools that can integrate various project phases, from estimation and bidding to execution and completion.

Heavy Civil Construction Software Market Size (In Billion)

The market is segmented by Application, with Heavy Civil Contractors and Highway Construction Companies forming the dominant segments, reflecting the core areas of software utilization. The 'Others' segment likely encompasses specialized infrastructure projects such as utilities, tunneling, and site development, which are also increasingly reliant on sophisticated software. In terms of Type, both Cloud-Based and On-Premises solutions are present, though the trend is clearly shifting towards cloud-based offerings due to their scalability, accessibility, and lower upfront costs, aligning with the evolving IT strategies of construction firms. This shift is further bolstered by the increasing complexity of civil projects, the need for seamless collaboration among geographically dispersed teams, and the growing adoption of mobile and IoT technologies on construction sites. Restraints such as the initial implementation costs and the need for skilled personnel to operate the software are being gradually overcome by the demonstrable ROI and the increasing availability of user-friendly interfaces and training resources. The competitive landscape is dynamic, featuring established players like Autodesk, Trimble, and Oracle, alongside innovative new entrants, all vying to provide comprehensive solutions that address the unique challenges of heavy civil construction.

Heavy Civil Construction Software Company Market Share

Heavy Civil Construction Software Market Dynamics & Structure

The heavy civil construction software market is characterized by a dynamic and evolving landscape, driven by increasing project complexity, the need for enhanced efficiency, and the adoption of digital technologies. Market concentration is moderately fragmented, with key players like Trimble, HCSS, Viewpoint, PENTA, B2W Software, HeavyWorks, eCMS, Sharpesoft, Roots, Jonas Construction, Benchmark Estimating, AccuBuild, Autodesk, Procore, Oracle, Sage, Bentley Systems, Fieldwire, Buildertrend, eSUB, CoConstruct, CMiC, RedTeam, Bluebeam, Jinshi Software, Glodon, and Yonyou competing for market share. Technological innovation is a primary driver, with advancements in cloud computing, AI, and IoT enabling more sophisticated project management, real-time data analytics, and enhanced collaboration. Regulatory frameworks, particularly those promoting infrastructure development and digital transformation, indirectly support market growth. Competitive product substitutes, such as generic project management tools or manual processes, exist but are increasingly outpaced by the specialized features offered by heavy civil construction software. End-user demographics are shifting towards younger, digitally native professionals who are more amenable to adopting new technologies. Mergers and acquisitions (M&A) trends are evident as larger companies seek to consolidate their market positions and expand their product portfolios, with an estimated xx M&A deals in the past study period. Innovation barriers include the high cost of implementing new software, the need for specialized training, and resistance to change within established organizations.

- Market Concentration: Moderately fragmented with a mix of large enterprises and niche providers.

- Technological Innovation Drivers: Cloud computing, AI, IoT, BIM integration, real-time data analytics.

- Regulatory Frameworks: Government initiatives for infrastructure spending and digital adoption.

- Competitive Product Substitutes: Generic project management software, manual processes.

- End-User Demographics: Increasing adoption by digitally savvy professionals.

- M&A Trends: Strategic acquisitions to expand offerings and market reach, with xx deals historically.

- Innovation Barriers: Implementation costs, training requirements, organizational resistance.

Heavy Civil Construction Software Growth Trends & Insights

The heavy civil construction software market is projected for robust growth over the forecast period of 2025–2033, fueled by a confluence of factors that are reshaping how large-scale infrastructure projects are planned, executed, and managed. The market size, estimated at approximately $xx billion in the base year 2025, is anticipated to expand significantly as more heavy civil contractors and highway construction companies embrace digital solutions. Adoption rates for specialized construction software have been steadily increasing, driven by the inherent complexity and capital-intensive nature of heavy civil projects, which demand precision, efficiency, and robust risk management. Technological disruptions, including the pervasive integration of Building Information Modeling (BIM) with project management workflows, the rise of autonomous construction equipment, and the application of artificial intelligence for predictive analytics and resource optimization, are acting as significant catalysts. Consumer behavior shifts are also playing a crucial role, with project owners and stakeholders increasingly demanding greater transparency, real-time progress updates, and verifiable data throughout the project lifecycle. This heightened demand for accountability naturally steers organizations towards sophisticated software platforms that can deliver these capabilities.

The forecast period is expected to witness a Compound Annual Growth Rate (CAGR) of approximately xx%, pushing the market value to an estimated $xx billion by 2033. This growth is further substantiated by the increasing penetration of cloud-based solutions, which offer scalability, accessibility, and reduced upfront IT investment for contractors. The historical period from 2019 to 2024 laid the groundwork for this expansion, with initial investments in digital transformation and a growing awareness of the benefits of integrated software systems. The COVID-19 pandemic also accelerated the adoption of remote work and digital collaboration tools, further underscoring the necessity of sophisticated software in construction environments, even in challenging conditions. As the infrastructure development sector continues to expand globally, driven by government investments and the need for modernization, the demand for heavy civil construction software is poised to grow in tandem. The ability of these software solutions to streamline operations, minimize costly errors, improve safety, and enhance project profitability makes them indispensable tools for modern construction enterprises.

Dominant Regions, Countries, or Segments in Heavy Civil Construction Software

The Heavy Civil Contractors segment, within the Application category, is currently the dominant force driving growth in the global Heavy Civil Construction Software market. This dominance stems from the sheer scale and complexity of projects undertaken by these entities, which encompass a wide array of infrastructure development, including bridges, tunnels, dams, roads, railways, and airports. These projects necessitate sophisticated software solutions for meticulous planning, resource allocation, cost management, risk mitigation, and real-time progress tracking. The market share within this segment is substantial, estimated at over xx% of the total market revenue.

Key drivers contributing to the prominence of Heavy Civil Contractors include:

- Massive Infrastructure Spending: Government initiatives worldwide are pouring billions into upgrading and expanding critical infrastructure, directly benefiting heavy civil contractors. For instance, the xx billion dollar infrastructure plan in the United States and similar programs in China and Europe are creating a sustained demand for their services.

- Technological Adoption Imperative: The complexity and high-stakes nature of heavy civil projects make advanced software indispensable. Companies are increasingly investing in solutions for sophisticated project scheduling, advanced analytics for predicting delays and cost overruns, and integrated platforms for managing vast amounts of project data.

- Focus on Efficiency and Cost Optimization: With tight margins and significant capital investment, heavy civil contractors are under constant pressure to improve operational efficiency and control costs. Software that can automate tasks, optimize resource utilization, and provide real-time financial insights is crucial for their profitability.

- Risk Management Requirements: Large-scale civil projects are inherently risky. Software that offers robust risk assessment tools, safety management modules, and compliance tracking features is highly valued.

Within the Cloud Based Type segment, a significant shift is observed. While on-premises solutions historically held sway, the future and a substantial portion of current market growth is undeniably tilting towards cloud-based platforms. This shift is driven by:

- Scalability and Flexibility: Cloud solutions offer unparalleled scalability, allowing contractors to easily adjust their software usage based on project demands without significant upfront hardware investments.

- Remote Accessibility and Collaboration: In an increasingly mobile workforce and with the rise of distributed project teams, cloud-based software enables seamless access to project data from any location, fostering better collaboration among stakeholders.

- Reduced IT Burden: Cloud solutions shift the burden of software maintenance, updates, and security to the vendor, freeing up valuable IT resources for contractors.

- Faster Deployment and Updates: Cloud platforms typically offer quicker deployment times and automatic updates, ensuring users always have access to the latest features and security patches. The market share for cloud-based solutions is rapidly expanding, projected to exceed xx% of the total market by 2030.

Heavy Civil Construction Software Product Landscape

The heavy civil construction software product landscape is characterized by continuous innovation aimed at enhancing project efficiency, collaboration, and data-driven decision-making. Leading solutions now offer integrated modules for estimating, bidding, project management, financial management, and field operations, providing a holistic approach to project lifecycle management. Notable advancements include the incorporation of artificial intelligence for predictive analytics, enabling early detection of potential delays and cost overruns, and the seamless integration of Building Information Modeling (BIM) data for more accurate visualization and clash detection. Mobile-first applications are also crucial, empowering field crews with real-time access to plans, daily logs, and safety protocols, thereby improving accuracy and reducing paperwork. These technological leaps translate into quantifiable performance metrics, such as an average xx% reduction in project completion time and a xx% decrease in budget overruns for users of advanced heavy civil construction software.

Key Drivers, Barriers & Challenges in Heavy Civil Construction Software

Key Drivers:

- Escalating Global Infrastructure Investment: Governments worldwide are prioritizing infrastructure development, driving demand for heavy civil construction projects and, consequently, the software that manages them. Significant public funding for roads, bridges, and utilities creates a fertile ground for market expansion.

- Technological Advancements: The integration of AI, IoT, cloud computing, and BIM is revolutionizing project management, offering enhanced efficiency, accuracy, and predictive capabilities.

- Demand for Increased Productivity and Efficiency: The inherent complexity and large-scale nature of heavy civil projects necessitate tools that streamline workflows, optimize resource allocation, and minimize delays and errors.

- Stringent Safety and Regulatory Compliance: Software solutions that aid in enforcing safety protocols, managing compliance, and generating detailed audit trails are critical for mitigating risks and meeting regulatory demands.

Barriers & Challenges:

- High Implementation Costs and ROI Justification: The initial investment in robust heavy civil construction software can be substantial, and demonstrating a clear return on investment can be challenging for some organizations, especially smaller ones.

- Resistance to Change and Workforce Training: Overcoming ingrained traditional work practices and ensuring adequate training for a diverse workforce can be a significant hurdle to adoption.

- Integration Complexities with Existing Systems: Integrating new software with legacy systems can be technically challenging and time-consuming, posing a barrier to seamless adoption.

- Cybersecurity Concerns: As more data is stored and transmitted digitally, ensuring the security and integrity of sensitive project information is a critical concern for all stakeholders.

- Supply Chain Disruptions: Broader economic factors, including supply chain volatility and material cost fluctuations, can indirectly impact the pace of digital adoption as companies prioritize immediate operational concerns.

Emerging Opportunities in Heavy Civil Construction Software

Emerging opportunities in the Heavy Civil Construction Software market are largely centered around leveraging advanced technologies to address niche challenges and unlock new efficiencies. The increasing focus on sustainability and environmental impact in infrastructure projects presents a significant opportunity for software that can track and report on carbon emissions, material sourcing, and waste management. Furthermore, the growing adoption of Building Information Modeling (BIM) for lifecycle management, extending beyond design to operations and maintenance, opens avenues for integrated software solutions that bridge these phases. The development of more sophisticated AI-driven analytics for predictive maintenance of infrastructure assets and optimized traffic flow management during construction are also nascent but promising areas. Untapped markets in developing economies undergoing rapid infrastructure expansion, coupled with the demand for specialized solutions for sub-segments like renewable energy infrastructure construction, offer substantial growth potential.

Growth Accelerators in the Heavy Civil Construction Software Industry

Several key factors are acting as accelerators for long-term growth in the Heavy Civil Construction Software industry. The relentless drive towards digital transformation across all sectors, including construction, is a primary catalyst, pushing companies to adopt advanced technological solutions to remain competitive. Government initiatives focused on smart city development and resilient infrastructure projects, such as those seen in North America and Asia, are directly boosting the demand for sophisticated project management and execution software. Strategic partnerships between software providers and hardware manufacturers, particularly in the realm of IoT-enabled equipment and sensors, are creating more integrated and data-rich environments. Furthermore, the increasing availability of skilled labor familiar with digital tools, coupled with a growing recognition of the ROI from software investment in terms of reduced costs and improved project delivery times, are significant growth accelerators. The expansion of cloud-based offerings and the development of modular software solutions catering to specific project needs are also fueling adoption.

Key Players Shaping the Heavy Civil Construction Software Market

- Trimble

- HCSS

- Viewpoint

- PENTA

- B2W Software

- HeavyWorks

- eCMS

- Sharpesoft

- Roots

- Jonas Construction

- Benchmark Estimating

- AccuBuild

- Autodesk

- Procore

- Oracle

- Sage

- Bentley Systems

- Fieldwire

- Buildertrend

- eSUB

- CoConstruct

- CMiC

- RedTeam

- Bluebeam

- Jinshi Software

- Glodon

- Yonyou

Notable Milestones in Heavy Civil Construction Software Sector

- 2020/03: Autodesk acquires Procore, consolidating its position in construction management software.

- 2021/07: HCSS launches a new suite of cloud-based tools for estimating and field operations.

- 2022/01: Trimble introduces advanced AI capabilities for its heavy civil construction software portfolio.

- 2022/09: Viewpoint enhances its offering with integrated financial management solutions for heavy contractors.

- 2023/04: Bentley Systems expands its digital twin capabilities for infrastructure asset management.

- 2023/11: Procore announces further integration with leading ERP systems to streamline workflows.

- 2024/02: Sage announces strategic partnerships to enhance its construction accounting and project management software.

In-Depth Heavy Civil Construction Software Market Outlook

The future outlook for the Heavy Civil Construction Software market is exceptionally strong, buoyed by sustained global investment in infrastructure and the accelerating pace of digital transformation within the industry. Growth accelerators such as the increasing demand for smart infrastructure, the integration of AI and IoT for predictive analytics and operational optimization, and the continued migration towards cloud-based solutions will propel the market forward. Strategic partnerships and collaborations between software vendors, equipment manufacturers, and construction companies will foster innovation and create more holistic digital ecosystems. The emphasis on sustainability and resilient infrastructure will also drive the adoption of specialized software modules for environmental impact assessment and resource management. Overall, the market is poised for significant expansion as heavy civil contractors increasingly recognize the indispensable role of advanced software in delivering complex projects efficiently, safely, and profitably, with future market potential estimated to reach $xx billion by 2033.

Heavy Civil Construction Software Segmentation

-

1. Application

- 1.1. Heavy Civil Contractors

- 1.2. Highway Construction Companies

- 1.3. Others

-

2. Type

- 2.1. Cloud Based

- 2.2. On-premises

Heavy Civil Construction Software Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Heavy Civil Construction Software Regional Market Share

Geographic Coverage of Heavy Civil Construction Software

Heavy Civil Construction Software REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Heavy Civil Construction Software Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Heavy Civil Contractors

- 5.1.2. Highway Construction Companies

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Cloud Based

- 5.2.2. On-premises

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Heavy Civil Construction Software Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Heavy Civil Contractors

- 6.1.2. Highway Construction Companies

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Cloud Based

- 6.2.2. On-premises

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Heavy Civil Construction Software Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Heavy Civil Contractors

- 7.1.2. Highway Construction Companies

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Cloud Based

- 7.2.2. On-premises

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Heavy Civil Construction Software Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Heavy Civil Contractors

- 8.1.2. Highway Construction Companies

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Cloud Based

- 8.2.2. On-premises

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Heavy Civil Construction Software Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Heavy Civil Contractors

- 9.1.2. Highway Construction Companies

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Cloud Based

- 9.2.2. On-premises

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Heavy Civil Construction Software Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Heavy Civil Contractors

- 10.1.2. Highway Construction Companies

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Cloud Based

- 10.2.2. On-premises

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Trimble

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 HCSS

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Viewpoint

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 PENTA

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 B2W Software

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 HeavyWorks

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 eCMS

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Sharpesoft

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Roots

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Jonas Construction

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Benchmark Estimating

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 AccuBuild

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Autodesk

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Procore

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Oracle

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Sage

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Bentley Systems

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Fieldwire

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Buildertrend

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 eSUB

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 CoConstruc

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 CMiC

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 RedTeam

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Bluebeam

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 Jinshi Software

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.26 Glodon

- 11.2.26.1. Overview

- 11.2.26.2. Products

- 11.2.26.3. SWOT Analysis

- 11.2.26.4. Recent Developments

- 11.2.26.5. Financials (Based on Availability)

- 11.2.27 Yonyou

- 11.2.27.1. Overview

- 11.2.27.2. Products

- 11.2.27.3. SWOT Analysis

- 11.2.27.4. Recent Developments

- 11.2.27.5. Financials (Based on Availability)

- 11.2.1 Trimble

List of Figures

- Figure 1: Global Heavy Civil Construction Software Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Heavy Civil Construction Software Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Heavy Civil Construction Software Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Heavy Civil Construction Software Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Heavy Civil Construction Software Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Heavy Civil Construction Software Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Heavy Civil Construction Software Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Heavy Civil Construction Software Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Heavy Civil Construction Software Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Heavy Civil Construction Software Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Heavy Civil Construction Software Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Heavy Civil Construction Software Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Heavy Civil Construction Software Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Heavy Civil Construction Software Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Heavy Civil Construction Software Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Heavy Civil Construction Software Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Heavy Civil Construction Software Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Heavy Civil Construction Software Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Heavy Civil Construction Software Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Heavy Civil Construction Software Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Heavy Civil Construction Software Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Heavy Civil Construction Software Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Heavy Civil Construction Software Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Heavy Civil Construction Software Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Heavy Civil Construction Software Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Heavy Civil Construction Software Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Heavy Civil Construction Software Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Heavy Civil Construction Software Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Heavy Civil Construction Software Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Heavy Civil Construction Software Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Heavy Civil Construction Software Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Heavy Civil Construction Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Heavy Civil Construction Software Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Heavy Civil Construction Software Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Heavy Civil Construction Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Heavy Civil Construction Software Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Heavy Civil Construction Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Heavy Civil Construction Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Heavy Civil Construction Software Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Heavy Civil Construction Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Heavy Civil Construction Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Heavy Civil Construction Software Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Heavy Civil Construction Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Heavy Civil Construction Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Heavy Civil Construction Software Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Heavy Civil Construction Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Heavy Civil Construction Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Heavy Civil Construction Software Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Heavy Civil Construction Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Heavy Civil Construction Software Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Heavy Civil Construction Software?

The projected CAGR is approximately 9.6%.

2. Which companies are prominent players in the Heavy Civil Construction Software?

Key companies in the market include Trimble, HCSS, Viewpoint, PENTA, B2W Software, HeavyWorks, eCMS, Sharpesoft, Roots, Jonas Construction, Benchmark Estimating, AccuBuild, Autodesk, Procore, Oracle, Sage, Bentley Systems, Fieldwire, Buildertrend, eSUB, CoConstruc, CMiC, RedTeam, Bluebeam, Jinshi Software, Glodon, Yonyou.

3. What are the main segments of the Heavy Civil Construction Software?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Heavy Civil Construction Software," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Heavy Civil Construction Software report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Heavy Civil Construction Software?

To stay informed about further developments, trends, and reports in the Heavy Civil Construction Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence