Key Insights

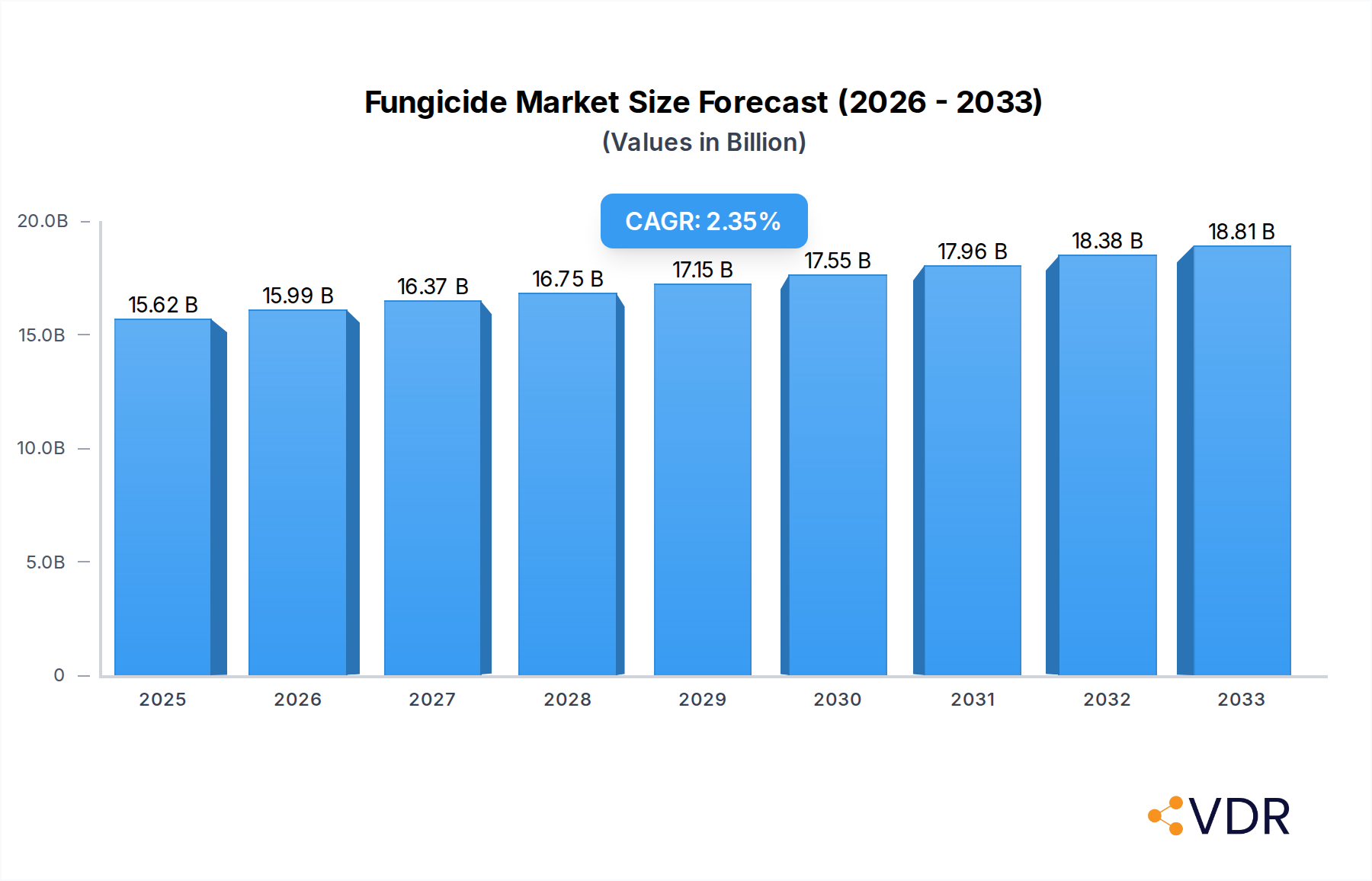

The global fungicide market is poised for steady expansion, with a projected market size of 15620 million by 2025. This growth is underpinned by a Compound Annual Growth Rate (CAGR) of 2.5% over the forecast period of 2025-2033. The increasing global population and the subsequent demand for enhanced food production are primary drivers for this market. Farmers are increasingly adopting advanced crop protection solutions to mitigate yield losses caused by fungal diseases, especially in the face of unpredictable weather patterns and the emergence of resistant fungal strains. The market’s expansion is further fueled by technological advancements in fungicide formulations, leading to more effective and environmentally sustainable products. Key application segments like grain crops, economic crops, and fruit and vegetable crops are expected to witness consistent demand, driven by the critical role fungicides play in ensuring crop health and quality across diverse agricultural landscapes.

Fungicide Market Size (In Billion)

Emerging trends such as the rising adoption of integrated pest management (IPM) strategies and the growing demand for organic fungicides are shaping the market dynamics. While traditional chemical fungicides continue to dominate, a noticeable shift towards bio-based and reduced-risk alternatives is observed, particularly in developed regions. However, the market faces certain restraints, including stringent regulatory frameworks governing the use and registration of agrochemicals, which can impact product launches and market access. Furthermore, the development of fungal resistance to existing fungicide chemistries necessitates continuous innovation and the introduction of new active ingredients. Despite these challenges, the robust demand for effective disease control, coupled with ongoing research and development efforts by major players like Syngenta, BASF, and Bayer, indicates a resilient and growing fungicide market that is crucial for global food security.

Fungicide Company Market Share

This in-depth report provides a detailed analysis of the global fungicide market, encompassing historical trends, current dynamics, and future projections. It offers critical insights for industry stakeholders, investors, and decision-makers seeking to understand the evolving landscape of crop protection. The report covers market size evolution, segment-specific growth, regional dominance, key player strategies, and emerging opportunities within the fungicide industry. With a focus on agricultural fungicides, crop disease management, and sustainable agriculture, this analysis is essential for navigating the complexities of the agrochemical market.

Fungicide Market Dynamics & Structure

The global fungicide market exhibits a moderate to high concentration, with a few key players like Syngenta, UPL, BASF, and Bayer holding significant market shares, estimated to be around 60% of the total market value in 2025. Technological innovation is a primary driver, with ongoing research and development focused on novel chemical formulations and biological alternatives to address evolving disease resistance and environmental concerns. Regulatory frameworks, particularly those concerning residue limits and environmental impact, significantly influence product development and market access. Competitive product substitutes, including biopesticides and integrated pest management (IPM) strategies, are gaining traction, though conventional fungicides remain dominant. End-user demographics are shifting towards larger-scale agricultural operations with a demand for high-efficacy solutions, while smaller farms are increasingly exploring cost-effective and sustainable options. Mergers and acquisitions (M&A) trends indicate strategic consolidation, with major companies acquiring smaller, innovative firms to expand their product portfolios and market reach. For instance, the period saw an average of 5-7 significant M&A deals annually within the agrochemical sector, with fungicide acquisitions comprising a notable portion. Innovation barriers include the lengthy and expensive registration process for new active ingredients and the growing public demand for reduced chemical use in agriculture.

- Market Concentration: Moderate to high, with top 5 companies holding approximately 60% market share in 2025.

- Technological Innovation: Driven by R&D in new chemistries, resistance management, and biological fungicides.

- Regulatory Frameworks: Stringent regulations impacting product approval and market entry globally.

- Competitive Substitutes: Rising adoption of biopesticides and IPM solutions.

- End-User Demographics: Increasing demand from large-scale commercial farms for advanced solutions.

- M&A Trends: Strategic acquisitions by major players to enhance portfolios and market access.

- Innovation Barriers: High R&D costs, lengthy registration processes, and public perception.

Fungicide Growth Trends & Insights

The global fungicide market has witnessed robust growth from 2019 to 2024, with an estimated market size of $25,500 million units in 2025, projected to reach $32,800 million units by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 3.2% during the forecast period. This expansion is fueled by the increasing global population, leading to higher demand for food production and consequently, greater reliance on crop protection solutions. Adoption rates for advanced fungicide formulations are steadily increasing, driven by the need to combat evolving plant diseases and manage fungicide resistance. Technological disruptions, such as the development of precision agriculture technologies and the integration of digital tools for disease monitoring and application optimization, are transforming the fungicide landscape. These advancements enable more targeted and efficient application, reducing overall chemical usage while maximizing efficacy. Consumer behavior shifts towards healthier and more sustainably produced food are also influencing the market, creating demand for both effective conventional fungicides and a growing segment of bio-fungicides. Market penetration of systemic fungicides, known for their preventive and curative properties, continues to grow across major crop types. The market penetration for broad-spectrum fungicides is estimated to be around 70% in developed agricultural economies in 2025. The rising frequency of extreme weather events due to climate change further exacerbates plant disease pressure, necessitating proactive and effective disease management strategies, thereby bolstering the demand for fungicides. Furthermore, governmental initiatives promoting food security and sustainable agricultural practices indirectly support the market's growth trajectory. The increasing acreage under high-value crops like fruits and vegetables, which are particularly susceptible to fungal infections, also contributes significantly to market expansion. The market is dynamic, with ongoing innovations in active ingredients and formulation technologies designed to improve efficacy, safety, and environmental profiles.

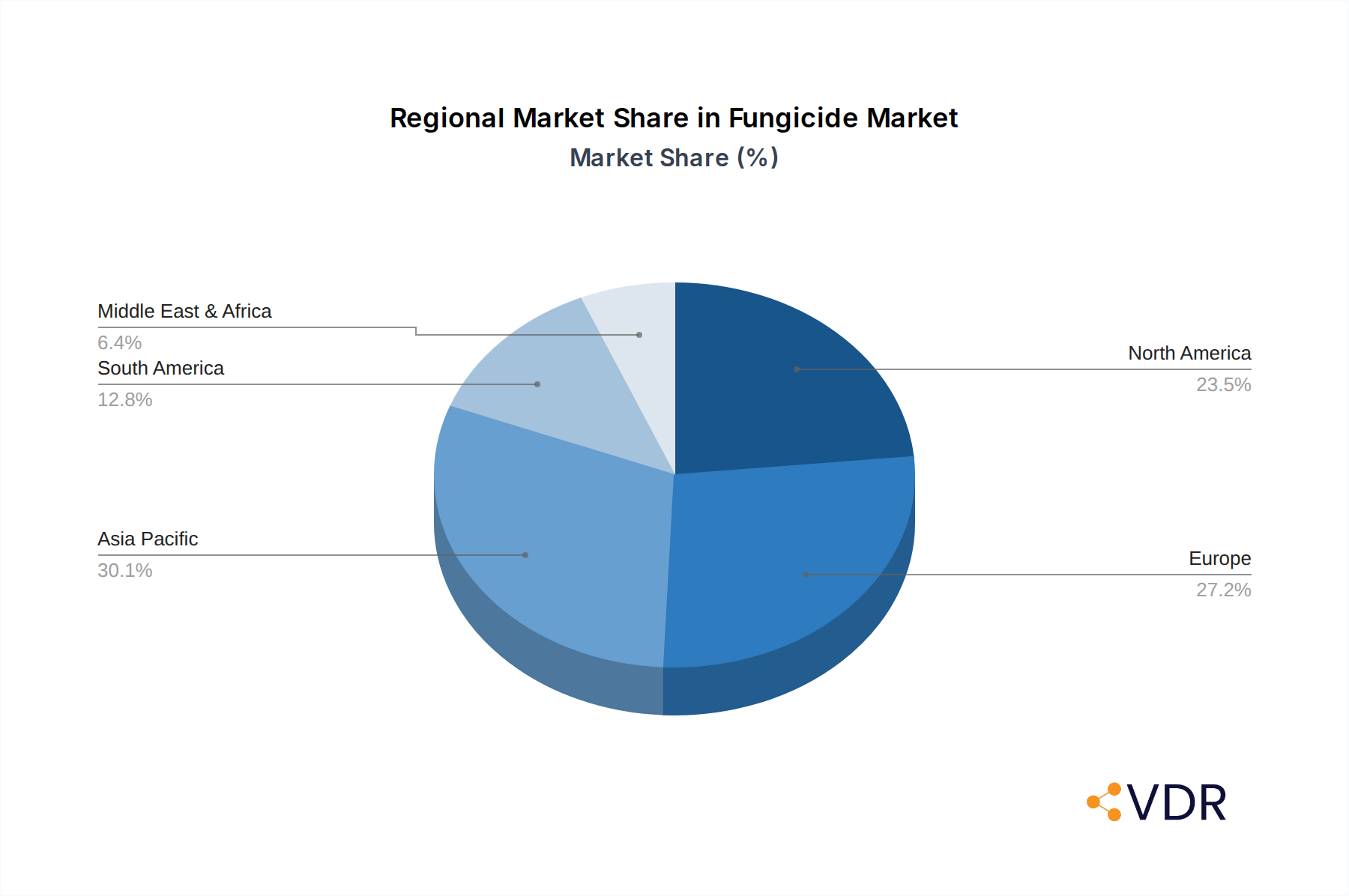

Dominant Regions, Countries, or Segments in Fungicide

The Grain Crops segment, particularly for applications like wheat, corn, and rice, is a dominant force in the global fungicide market, estimated to account for nearly 45% of the total market value in 2025. This dominance is driven by the vast acreage dedicated to grain cultivation worldwide and the significant economic impact of fungal diseases on these staple food crops. Key drivers for this segment’s growth include government policies aimed at enhancing food security, the need for increased yields to feed a growing global population, and the economic importance of grain exports in many regions. Asia Pacific is the leading region, projected to hold over 35% of the global fungicide market share in 2025, due to its large agricultural base, substantial investment in agricultural R&D, and the widespread prevalence of fungal diseases affecting major crops.

Within the Type segment, Azoxystrobin and Pyraclostrobin are leading fungicides, collectively estimated to hold over 30% of the market share in 2025 due to their broad-spectrum activity, excellent preventive and curative properties, and favorable cost-effectiveness. The demand for these strobilurin fungicides is propelled by their efficacy against a wide range of pathogens and their compatibility with integrated pest management programs.

- Dominant Application Segment: Grain Crops (estimated 45% market share in 2025)

- Key Drivers: Food security initiatives, increasing global food demand, significant economic impact of diseases on staple crops.

- Growth Potential: Continual need for yield enhancement and disease prevention in major cereal production.

- Dominant Regional Market: Asia Pacific (estimated 35% market share in 2025)

- Key Drivers: Large agricultural landmass, significant investment in agriculture, high incidence of crop diseases.

- Growth Potential: Rapid adoption of modern farming practices and agrochemicals.

- Leading Fungicide Types: Azoxystrobin and Pyraclostrobin (estimated combined 30% market share in 2025)

- Key Drivers: Broad-spectrum efficacy, preventive and curative action, cost-effectiveness, resistance management benefits.

- Growth Potential: Continued demand for proven and reliable fungicidal solutions.

Fungicide Product Landscape

The fungicide product landscape is characterized by continuous innovation, focusing on developing broad-spectrum and highly effective active ingredients. Azoxystrobin and Pyraclostrobin remain market leaders due to their proven efficacy against a wide array of fungal pathogens in crops like cereals, fruits, and vegetables. Emerging product lines are increasingly emphasizing biological fungicides and targeted chemistries that offer enhanced safety profiles and reduced environmental impact. Performance metrics such as efficacy against specific diseases, residual activity, and crop safety are key differentiators. The integration of novel co-formulations and advanced delivery systems aims to optimize uptake and translocation within plants, maximizing disease control and minimizing the need for repeat applications. For example, the development of microencapsulation technologies has improved the persistence and rainfastness of certain fungicide applications, enhancing their overall value proposition.

Key Drivers, Barriers & Challenges in Fungicide

The fungicide market is propelled by the imperative of increasing global food production to meet the demands of a growing population. Technological advancements in disease detection and precision application technologies are crucial drivers, enabling more efficient and targeted use of fungicides. Government policies supporting agricultural productivity and subsidies for crop protection inputs also play a significant role. The rising incidence of plant diseases, exacerbated by climate change and the globalization of trade, further fuels demand.

However, significant barriers exist, including stringent regulatory hurdles and the lengthy, costly process of registering new active ingredients. The growing consumer demand for organic and residue-free produce poses a challenge to conventional fungicide use, driving the development and adoption of bio-fungicides. Supply chain disruptions, geopolitical uncertainties, and price volatility of raw materials can impact production costs and availability. Furthermore, the increasing development of fungicide resistance among plant pathogens necessitates continuous R&D efforts to bring novel solutions to market.

Emerging Opportunities in Fungicide

Emerging opportunities in the fungicide market lie in the development and widespread adoption of biological fungicides. These products, derived from natural sources like microorganisms, offer a sustainable alternative with reduced environmental impact and a favorable safety profile, catering to the growing demand for organic produce. Precision agriculture technologies, including drone-based applications and sensor-based disease monitoring, present opportunities for more targeted and efficient fungicide use, leading to reduced chemical load and cost savings for farmers. Untapped markets in developing economies with expanding agricultural sectors also offer significant growth potential. Furthermore, the development of combination products and integrated pest management (IPM) solutions that synergize chemical and biological approaches presents a promising avenue for enhanced disease control and resistance management.

Growth Accelerators in the Fungicide Industry

Technological breakthroughs in gene editing and synthetic biology are accelerating the discovery and development of novel fungicide active ingredients with enhanced efficacy and specificity. Strategic partnerships between agrochemical companies and biotechnology firms are crucial for leveraging these advancements and bringing innovative products to market. Market expansion strategies targeting emerging economies with rapidly growing agricultural sectors, driven by increasing domestic food demand and export opportunities, are key growth accelerators. The continuous improvement of formulation technologies, leading to more user-friendly and environmentally sound products, also contributes to sustained market expansion. The increasing adoption of digital agriculture platforms for optimized crop management, including fungicide application, further propels growth by enhancing efficacy and reducing waste.

Key Players Shaping the Fungicide Market

Syngenta, UPL, FMC, BASF, Bayer, Nufarm, Pioneer (Dupont), Sumitomo Chemical, Dow AgroSciences, Marrone Bio Innovations (MBI), Indofil, Adama Agricultural Solutions, Arysta LifeScience, Forward International, IQV Agro, SipcamAdvan, Gowan, Isagro, Summit Agro USA, Everris (ICL), Certis USA, Acme Organics Private, Rotam, Sinochem, Limin Chemical, Shuangji Chemical, Jiangxi Heyi, Lier Chemical, Jiangsu Flag Chemical Industry, Jiangsu Frey Agrochemicals.

Notable Milestones in Fungicide Sector

- 2019: Launch of new broad-spectrum fungicide with enhanced rainfastness by Syngenta.

- 2020: UPL acquires specialty agrochemical assets, expanding its fungicide portfolio.

- 2021: BASF announces significant investment in R&D for novel biological fungicides.

- 2022: FMC develops a new fungicide targeting resistant strains of Powdery Mildew.

- 2023: Bayer partners with a biotech firm to develop innovative disease management solutions.

- 2024: Marrone Bio Innovations (MBI) receives regulatory approval for a new biofungicide for use in organic farming.

In-Depth Fungicide Market Outlook

The future fungicide market outlook is characterized by sustained growth, driven by the persistent need for enhanced global food security and the continuous threat of plant diseases. Key growth accelerators include ongoing innovation in both synthetic and biological fungicide chemistries, coupled with the increasing adoption of precision agriculture and digital farming tools. Strategic collaborations and market expansion into rapidly developing agricultural economies will further fuel demand. Companies focusing on sustainable solutions and integrated pest management strategies are poised to capture significant market share. The market will witness a gradual shift towards more targeted, environmentally friendly, and resistance-breaking fungicide solutions, offering lucrative opportunities for forward-thinking stakeholders in the agrochemical industry.

Fungicide Segmentation

-

1. Application

- 1.1. Grain Crops

- 1.2. Economic Crops

- 1.3. Fruit and Vegetable Crops

- 1.4. Other

-

2. Type

- 2.1. Azoxystrobin

- 2.2. Pyraclostrobin

- 2.3. Mancozeb

- 2.4. Trifloxystrobin

- 2.5. Prothioconazole

- 2.6. Copper fungicides

- 2.7. Epoxiconazole

- 2.8. Tebuconazole

- 2.9. Metalaxyl

- 2.10. Cyproconazole

Fungicide Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Fungicide Regional Market Share

Geographic Coverage of Fungicide

Fungicide REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Grain Crops

- 5.1.2. Economic Crops

- 5.1.3. Fruit and Vegetable Crops

- 5.1.4. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Azoxystrobin

- 5.2.2. Pyraclostrobin

- 5.2.3. Mancozeb

- 5.2.4. Trifloxystrobin

- 5.2.5. Prothioconazole

- 5.2.6. Copper fungicides

- 5.2.7. Epoxiconazole

- 5.2.8. Tebuconazole

- 5.2.9. Metalaxyl

- 5.2.10. Cyproconazole

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Fungicide Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Grain Crops

- 6.1.2. Economic Crops

- 6.1.3. Fruit and Vegetable Crops

- 6.1.4. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Azoxystrobin

- 6.2.2. Pyraclostrobin

- 6.2.3. Mancozeb

- 6.2.4. Trifloxystrobin

- 6.2.5. Prothioconazole

- 6.2.6. Copper fungicides

- 6.2.7. Epoxiconazole

- 6.2.8. Tebuconazole

- 6.2.9. Metalaxyl

- 6.2.10. Cyproconazole

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Fungicide Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Grain Crops

- 7.1.2. Economic Crops

- 7.1.3. Fruit and Vegetable Crops

- 7.1.4. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Azoxystrobin

- 7.2.2. Pyraclostrobin

- 7.2.3. Mancozeb

- 7.2.4. Trifloxystrobin

- 7.2.5. Prothioconazole

- 7.2.6. Copper fungicides

- 7.2.7. Epoxiconazole

- 7.2.8. Tebuconazole

- 7.2.9. Metalaxyl

- 7.2.10. Cyproconazole

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Fungicide Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Grain Crops

- 8.1.2. Economic Crops

- 8.1.3. Fruit and Vegetable Crops

- 8.1.4. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Azoxystrobin

- 8.2.2. Pyraclostrobin

- 8.2.3. Mancozeb

- 8.2.4. Trifloxystrobin

- 8.2.5. Prothioconazole

- 8.2.6. Copper fungicides

- 8.2.7. Epoxiconazole

- 8.2.8. Tebuconazole

- 8.2.9. Metalaxyl

- 8.2.10. Cyproconazole

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Fungicide Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Grain Crops

- 9.1.2. Economic Crops

- 9.1.3. Fruit and Vegetable Crops

- 9.1.4. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Azoxystrobin

- 9.2.2. Pyraclostrobin

- 9.2.3. Mancozeb

- 9.2.4. Trifloxystrobin

- 9.2.5. Prothioconazole

- 9.2.6. Copper fungicides

- 9.2.7. Epoxiconazole

- 9.2.8. Tebuconazole

- 9.2.9. Metalaxyl

- 9.2.10. Cyproconazole

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Fungicide Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Grain Crops

- 10.1.2. Economic Crops

- 10.1.3. Fruit and Vegetable Crops

- 10.1.4. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Azoxystrobin

- 10.2.2. Pyraclostrobin

- 10.2.3. Mancozeb

- 10.2.4. Trifloxystrobin

- 10.2.5. Prothioconazole

- 10.2.6. Copper fungicides

- 10.2.7. Epoxiconazole

- 10.2.8. Tebuconazole

- 10.2.9. Metalaxyl

- 10.2.10. Cyproconazole

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Fungicide Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Grain Crops

- 11.1.2. Economic Crops

- 11.1.3. Fruit and Vegetable Crops

- 11.1.4. Other

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Azoxystrobin

- 11.2.2. Pyraclostrobin

- 11.2.3. Mancozeb

- 11.2.4. Trifloxystrobin

- 11.2.5. Prothioconazole

- 11.2.6. Copper fungicides

- 11.2.7. Epoxiconazole

- 11.2.8. Tebuconazole

- 11.2.9. Metalaxyl

- 11.2.10. Cyproconazole

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Syngenta

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 UPL

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 FMC

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 BASF

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Bayer

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Nufarm

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Pioneer (Dupont)

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Sumitomo Chemical

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Dow AgroSciences

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Marrone Bio Innovations (MBI)

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Indofil

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Adama Agricultural Solutions

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Arysta LifeScience

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Forward International

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 IQV Agro

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 SipcamAdvan

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Gowan

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Isagro

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Summit Agro USA

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 Everris (ICL)

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 Certis USA

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.22 Acme Organics Private

- 12.1.22.1. Company Overview

- 12.1.22.2. Products

- 12.1.22.3. Company Financials

- 12.1.22.4. SWOT Analysis

- 12.1.23 Rotam

- 12.1.23.1. Company Overview

- 12.1.23.2. Products

- 12.1.23.3. Company Financials

- 12.1.23.4. SWOT Analysis

- 12.1.24 Sinochem

- 12.1.24.1. Company Overview

- 12.1.24.2. Products

- 12.1.24.3. Company Financials

- 12.1.24.4. SWOT Analysis

- 12.1.25 Limin Chemical

- 12.1.25.1. Company Overview

- 12.1.25.2. Products

- 12.1.25.3. Company Financials

- 12.1.25.4. SWOT Analysis

- 12.1.26 Shuangji Chemical

- 12.1.26.1. Company Overview

- 12.1.26.2. Products

- 12.1.26.3. Company Financials

- 12.1.26.4. SWOT Analysis

- 12.1.27 Jiangxi Heyi

- 12.1.27.1. Company Overview

- 12.1.27.2. Products

- 12.1.27.3. Company Financials

- 12.1.27.4. SWOT Analysis

- 12.1.28 Lier Chemical

- 12.1.28.1. Company Overview

- 12.1.28.2. Products

- 12.1.28.3. Company Financials

- 12.1.28.4. SWOT Analysis

- 12.1.29 Jiangsu Flag Chemical Industry

- 12.1.29.1. Company Overview

- 12.1.29.2. Products

- 12.1.29.3. Company Financials

- 12.1.29.4. SWOT Analysis

- 12.1.30 Jiangsu Frey Agrochemicals

- 12.1.30.1. Company Overview

- 12.1.30.2. Products

- 12.1.30.3. Company Financials

- 12.1.30.4. SWOT Analysis

- 12.1.1 Syngenta

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Fungicide Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Fungicide Revenue (million), by Application 2025 & 2033

- Figure 3: North America Fungicide Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Fungicide Revenue (million), by Type 2025 & 2033

- Figure 5: North America Fungicide Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Fungicide Revenue (million), by Country 2025 & 2033

- Figure 7: North America Fungicide Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Fungicide Revenue (million), by Application 2025 & 2033

- Figure 9: South America Fungicide Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Fungicide Revenue (million), by Type 2025 & 2033

- Figure 11: South America Fungicide Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Fungicide Revenue (million), by Country 2025 & 2033

- Figure 13: South America Fungicide Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Fungicide Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Fungicide Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Fungicide Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Fungicide Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Fungicide Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Fungicide Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Fungicide Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Fungicide Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Fungicide Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Fungicide Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Fungicide Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Fungicide Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Fungicide Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Fungicide Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Fungicide Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Fungicide Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Fungicide Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Fungicide Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Fungicide Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Fungicide Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Fungicide Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Fungicide Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Fungicide Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Fungicide Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Fungicide Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Fungicide Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Fungicide Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Fungicide Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Fungicide Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Fungicide Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Fungicide Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Fungicide Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Fungicide Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Fungicide Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Fungicide Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Fungicide Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Fungicide Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Fungicide Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Fungicide?

The projected CAGR is approximately 2.5%.

2. Which companies are prominent players in the Fungicide?

Key companies in the market include Syngenta, UPL, FMC, BASF, Bayer, Nufarm, Pioneer (Dupont), Sumitomo Chemical, Dow AgroSciences, Marrone Bio Innovations (MBI), Indofil, Adama Agricultural Solutions, Arysta LifeScience, Forward International, IQV Agro, SipcamAdvan, Gowan, Isagro, Summit Agro USA, Everris (ICL), Certis USA, Acme Organics Private, Rotam, Sinochem, Limin Chemical, Shuangji Chemical, Jiangxi Heyi, Lier Chemical, Jiangsu Flag Chemical Industry, Jiangsu Frey Agrochemicals.

3. What are the main segments of the Fungicide?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 15620 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5900.00, USD 8850.00, and USD 11800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Fungicide," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Fungicide report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Fungicide?

To stay informed about further developments, trends, and reports in the Fungicide, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence