Key Insights

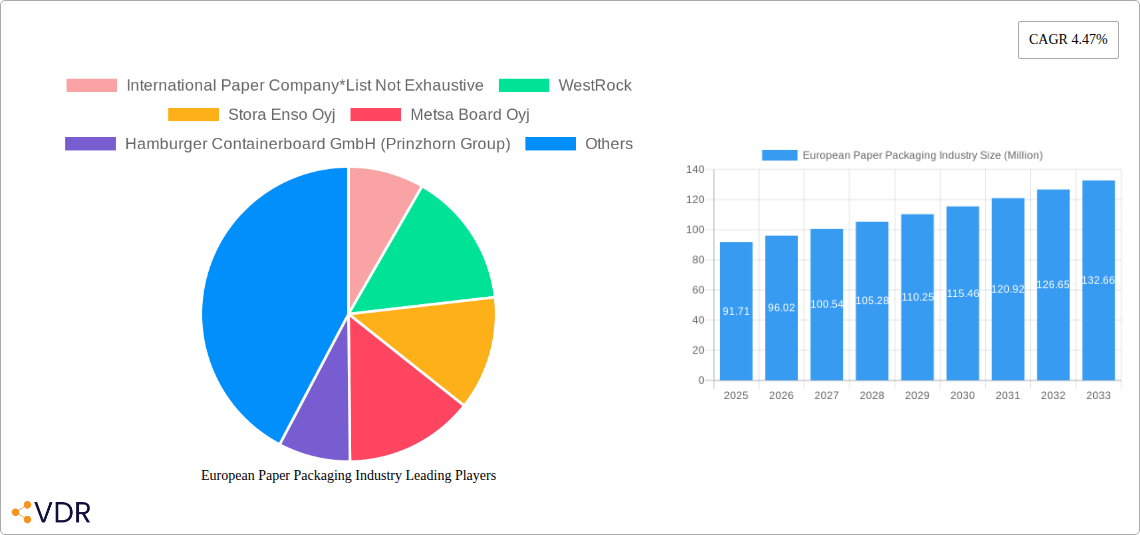

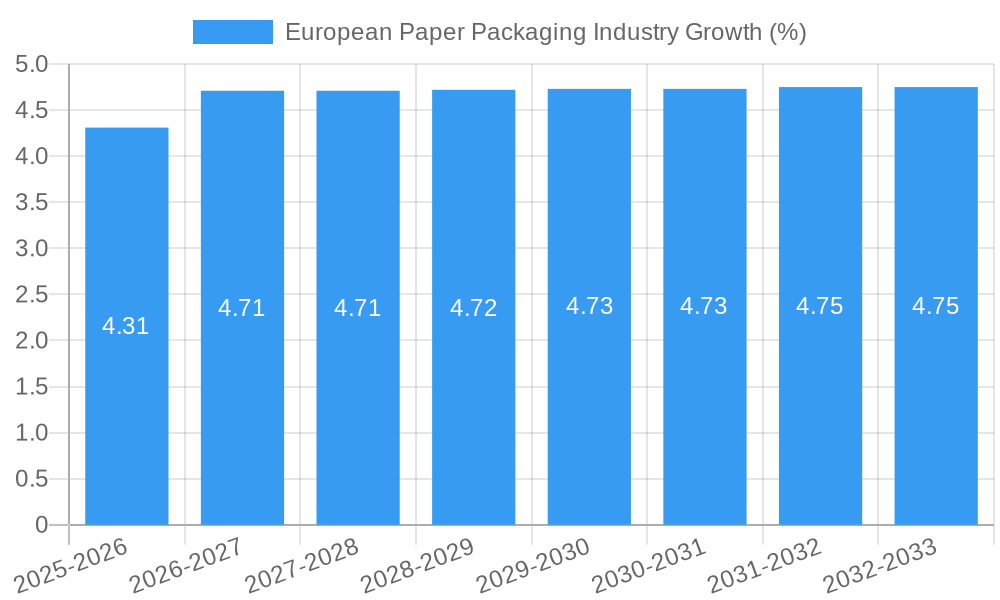

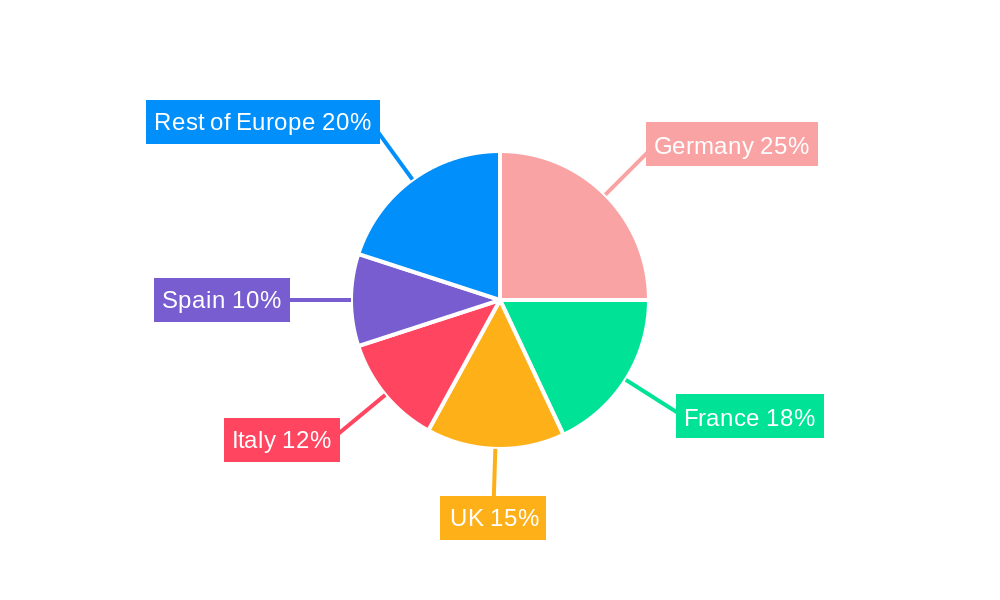

The European paper packaging market, valued at €91.71 million in 2025, is projected to experience steady growth, driven by a Compound Annual Growth Rate (CAGR) of 4.47% from 2025 to 2033. This expansion is fueled by several key factors. The rising e-commerce sector necessitates robust and sustainable packaging solutions, boosting demand for corrugated boxes and folding cartons. Simultaneously, the growing focus on sustainable and eco-friendly packaging options is driving innovation within the industry, with increased adoption of recycled and recyclable materials. Furthermore, the food and beverage sector, a major consumer of paper packaging, continues to expand, contributing significantly to market growth. Germany, France, and the United Kingdom represent the largest national markets within Europe, reflecting established manufacturing infrastructure and high consumer demand. However, competitive pressures from alternative packaging materials, such as plastics, and fluctuations in raw material prices pose potential restraints on market expansion. The market segmentation reveals a strong preference for folding cartons and corrugated boxes, with the food and beverage industry dominating end-user consumption. Companies such as International Paper, WestRock, and Smurfit Kappa are key players, showcasing established market presence and competitive strategies.

The forecast period (2025-2033) anticipates continued growth, though at a potentially moderated pace towards the latter half, as market saturation and economic conditions influence consumer spending. The industry's future success hinges on addressing sustainability concerns through responsible sourcing and innovative packaging designs. Continued investment in research and development, coupled with strategic collaborations across the supply chain, will be crucial for sustained market expansion. Furthermore, adapting to evolving consumer preferences and regulatory changes concerning packaging waste will be paramount for long-term competitiveness within the European paper packaging market. Geographic expansion within the European Union, targeting regions with high growth potential, also presents a viable strategy for companies seeking to enhance their market share.

European Paper Packaging Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the European paper packaging industry, covering market dynamics, growth trends, key players, and future outlook. The study period spans 2019-2033, with 2025 as the base and estimated year. This report is invaluable for industry professionals, investors, and strategic decision-makers seeking to understand and capitalize on opportunities within this dynamic sector. The market is segmented by type (folding cartons, corrugated boxes, other types), end-user industry (food, beverage, healthcare, personal care, tobacco, etc.), and country (United Kingdom, France, Germany, Italy, Spain, Rest of Europe). The total market size is projected to reach xx Million units by 2033.

European Paper Packaging Industry Market Dynamics & Structure

The European paper packaging market is characterized by a moderately concentrated landscape, with several large multinational players and a significant number of smaller regional companies. Market concentration is influenced by mergers and acquisitions (M&A) activity, with an estimated xx deals occurring between 2019 and 2024. Technological innovation, driven by sustainability concerns and e-commerce growth, is a key driver. Stringent regulatory frameworks, particularly regarding recyclability and plastic reduction, significantly impact market dynamics. The industry faces competition from alternative packaging materials like plastic and sustainable alternatives (e.g., biodegradable materials), but paper packaging maintains a strong position due to its cost-effectiveness, renewability, and recyclability. End-user demographics, including changing consumer preferences toward sustainable products, are shaping demand.

- Market Concentration: Moderately concentrated, with top 5 players holding approximately xx% market share in 2024.

- Technological Innovation: Focus on sustainable materials, automation, and improved printing technologies.

- Regulatory Framework: Stringent regulations on recyclability and waste reduction are driving innovation.

- Competitive Substitutes: Plastic and other sustainable alternatives pose a challenge, but paper retains a dominant position.

- M&A Activity: xx M&A deals between 2019-2024, indicating consolidation and expansion within the market.

- Innovation Barriers: High initial investment costs for new technologies and stringent regulatory compliance requirements.

European Paper Packaging Industry Growth Trends & Insights

The European paper packaging market exhibited steady growth during the historical period (2019-2024), driven primarily by increasing demand from the food & beverage and e-commerce sectors. The market size in 2024 was estimated at xx Million units. The Compound Annual Growth Rate (CAGR) during this period was approximately xx%. Technological disruptions, such as the adoption of lightweight packaging and improved printing techniques, are enhancing efficiency and expanding applications. Shifting consumer preferences towards sustainable and eco-friendly packaging are fueling demand for recyclable and renewable alternatives. Market penetration of sustainable paper packaging is increasing, with a projected xx% penetration rate by 2033. The forecast period (2025-2033) anticipates continued growth, driven by factors including population growth, increasing disposable income in several European countries, and the continued rise of e-commerce.

Dominant Regions, Countries, or Segments in European Paper Packaging Industry

Germany, the UK, and France are the dominant countries within the European paper packaging market, accounting for approximately xx% of the total market value in 2024. Within market segments, Corrugated Boxes command the largest share, followed by Folding Cartons. The food and beverage sector is the leading end-user industry, while the e-commerce sector is experiencing the fastest growth.

- Germany: Strong industrial base and high demand from various end-user industries.

- United Kingdom: Large and diversified economy, substantial e-commerce activity.

- France: Significant food and beverage sector, coupled with a growing focus on sustainability.

- Corrugated Boxes: Dominant segment due to versatility and suitability for diverse applications.

- Food & Beverage: Largest end-user segment, driven by consistent product demand.

- E-commerce: Fastest-growing segment, fueled by the rise of online shopping.

European Paper Packaging Industry Product Landscape

The European paper packaging market features a diverse range of products tailored to various applications. Innovations focus on lightweighting to reduce material consumption, enhanced printability for improved branding, and the incorporation of barrier coatings to extend shelf life. Technological advancements include the use of recycled fibers, biodegradable additives, and functional barrier papers to enhance sustainability. Key selling propositions include superior printability, cost-effectiveness, recyclability, and eco-friendliness.

Key Drivers, Barriers & Challenges in European Paper Packaging Industry

Key Drivers: Growing e-commerce, rising consumer demand for sustainable packaging, favorable government policies promoting recycling, and technological advancements in barrier coatings and lightweight materials.

Challenges: Fluctuations in raw material prices (e.g., pulp), competition from alternative packaging materials, increasing energy costs, and stringent environmental regulations that necessitate costly compliance measures. Supply chain disruptions due to geopolitical instability can impact the availability of raw materials, resulting in potential price increases and production delays.

Emerging Opportunities in European Paper Packaging Industry

Emerging opportunities lie in the growing demand for sustainable and eco-friendly packaging solutions within the e-commerce, food & beverage, and healthcare sectors. Innovations in biodegradable and compostable packaging, coupled with the development of functional barrier papers to replace plastic, present significant potential. Untapped markets include specialized packaging for niche products and the development of customized packaging solutions based on specific client needs.

Growth Accelerators in the European Paper Packaging Industry

Technological breakthroughs in barrier coatings, lightweighting techniques, and the development of recyclable and renewable materials are accelerating market growth. Strategic partnerships and collaborations between packaging manufacturers and end-user industries drive innovation and efficiency improvements. Expansion into new markets (e.g., emerging economies within Europe) and the development of bespoke packaging solutions are contributing to long-term growth.

Key Players Shaping the European Paper Packaging Industry Market

- International Paper Company

- WestRock

- Stora Enso Oyj

- Metsa Board Oyj

- Hamburger Containerboard GmbH (Prinzhorn Group)

- Svenska Cellulosa Aktiebolaget - SCA

- Papierfabrik Palm GmbH & Co KG

- DS Smith PLC

- Progroup AG

- Mondi Group

- Emin Leydier SA

- Smurfit Kappa

Notable Milestones in European Paper Packaging Industry Sector

- May 2022: Mondi partnered with beck packautomaten to launch a recyclable paper-based packaging solution for e-commerce, using 95% paper.

- May 2022: Smurfit Kappa acquired Atlas Packaging, strengthening its market position in the UK corrugated packaging sector.

In-Depth European Paper Packaging Industry Market Outlook

The European paper packaging industry is poised for continued growth, driven by strong demand from key sectors, the increasing adoption of sustainable practices, and technological advancements. Strategic opportunities exist in developing innovative, eco-friendly packaging solutions, expanding into high-growth markets, and establishing strategic partnerships to enhance supply chain efficiency and sustainability. The market's future success hinges on the ability of companies to adapt to evolving consumer preferences, comply with tightening environmental regulations, and leverage technological advancements to deliver superior and sustainable packaging solutions.

European Paper Packaging Industry Segmentation

-

1. Product Type

- 1.1. Folding Cartons

- 1.2. Corrugated Boxes

- 1.3. Other Product Type

-

2. End-user Industry

- 2.1. Food

- 2.2. Beverage

- 2.3. Healthcare

- 2.4. Personal Care and Household Care

- 2.5. E-Commerce

- 2.6. Tobacco

- 2.7. Other End-user Industries

European Paper Packaging Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

European Paper Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.47% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Demand From The Food And Beverage Sector; Increasing Growth Of E-commerce Creating Demand For Various Paper And Paperboard Packaging Types

- 3.3. Market Restrains

- 3.3.1. Effects Of Deforestation On Paper Packaging

- 3.4. Market Trends

- 3.4.1. Beverage Pakaging will Drive the Market Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. European Paper Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Folding Cartons

- 5.1.2. Corrugated Boxes

- 5.1.3. Other Product Type

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Food

- 5.2.2. Beverage

- 5.2.3. Healthcare

- 5.2.4. Personal Care and Household Care

- 5.2.5. E-Commerce

- 5.2.6. Tobacco

- 5.2.7. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Germany European Paper Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 7. France European Paper Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 8. Italy European Paper Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom European Paper Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands European Paper Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 11. Sweden European Paper Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe European Paper Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 International Paper Company*List Not Exhaustive

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 WestRock

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Stora Enso Oyj

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Metsa Board Oyj

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Hamburger Containerboard GmbH (Prinzhorn Group)

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Svenska Cellulosa Aktiebolaget - SCA

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Papierfabrik Palm GmbH & Co KG

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 DS Smith PLC

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Progroup AG

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Mondi Group

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 Emin Leydier SA

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.12 Smurfit Kappa

- 13.2.12.1. Overview

- 13.2.12.2. Products

- 13.2.12.3. SWOT Analysis

- 13.2.12.4. Recent Developments

- 13.2.12.5. Financials (Based on Availability)

- 13.2.1 International Paper Company*List Not Exhaustive

List of Figures

- Figure 1: European Paper Packaging Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: European Paper Packaging Industry Share (%) by Company 2024

List of Tables

- Table 1: European Paper Packaging Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: European Paper Packaging Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 3: European Paper Packaging Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 4: European Paper Packaging Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: European Paper Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Germany European Paper Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: France European Paper Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Italy European Paper Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: United Kingdom European Paper Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Netherlands European Paper Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Sweden European Paper Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Rest of Europe European Paper Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: European Paper Packaging Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 14: European Paper Packaging Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 15: European Paper Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: United Kingdom European Paper Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Germany European Paper Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: France European Paper Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Italy European Paper Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Spain European Paper Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Netherlands European Paper Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Belgium European Paper Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Sweden European Paper Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Norway European Paper Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Poland European Paper Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Denmark European Paper Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the European Paper Packaging Industry?

The projected CAGR is approximately 4.47%.

2. Which companies are prominent players in the European Paper Packaging Industry?

Key companies in the market include International Paper Company*List Not Exhaustive, WestRock, Stora Enso Oyj, Metsa Board Oyj, Hamburger Containerboard GmbH (Prinzhorn Group), Svenska Cellulosa Aktiebolaget - SCA, Papierfabrik Palm GmbH & Co KG, DS Smith PLC, Progroup AG, Mondi Group, Emin Leydier SA, Smurfit Kappa.

3. What are the main segments of the European Paper Packaging Industry?

The market segments include Product Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 91.71 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand From The Food And Beverage Sector; Increasing Growth Of E-commerce Creating Demand For Various Paper And Paperboard Packaging Types.

6. What are the notable trends driving market growth?

Beverage Pakaging will Drive the Market Growth.

7. Are there any restraints impacting market growth?

Effects Of Deforestation On Paper Packaging.

8. Can you provide examples of recent developments in the market?

May 2022: Mondi partnered with beck packautomaten to launch a strong, flexible paper-based packaging solution dedicated to the eCommerce industry. The solution uses 95% paper and is recyclable across all European paper waste streams. FunctionalBarrier Paper can replace unnecessary plastic packaging, enabling shipments to arrive safely in sustainable and right-sized packaging.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "European Paper Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the European Paper Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the European Paper Packaging Industry?

To stay informed about further developments, trends, and reports in the European Paper Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence