Key Insights

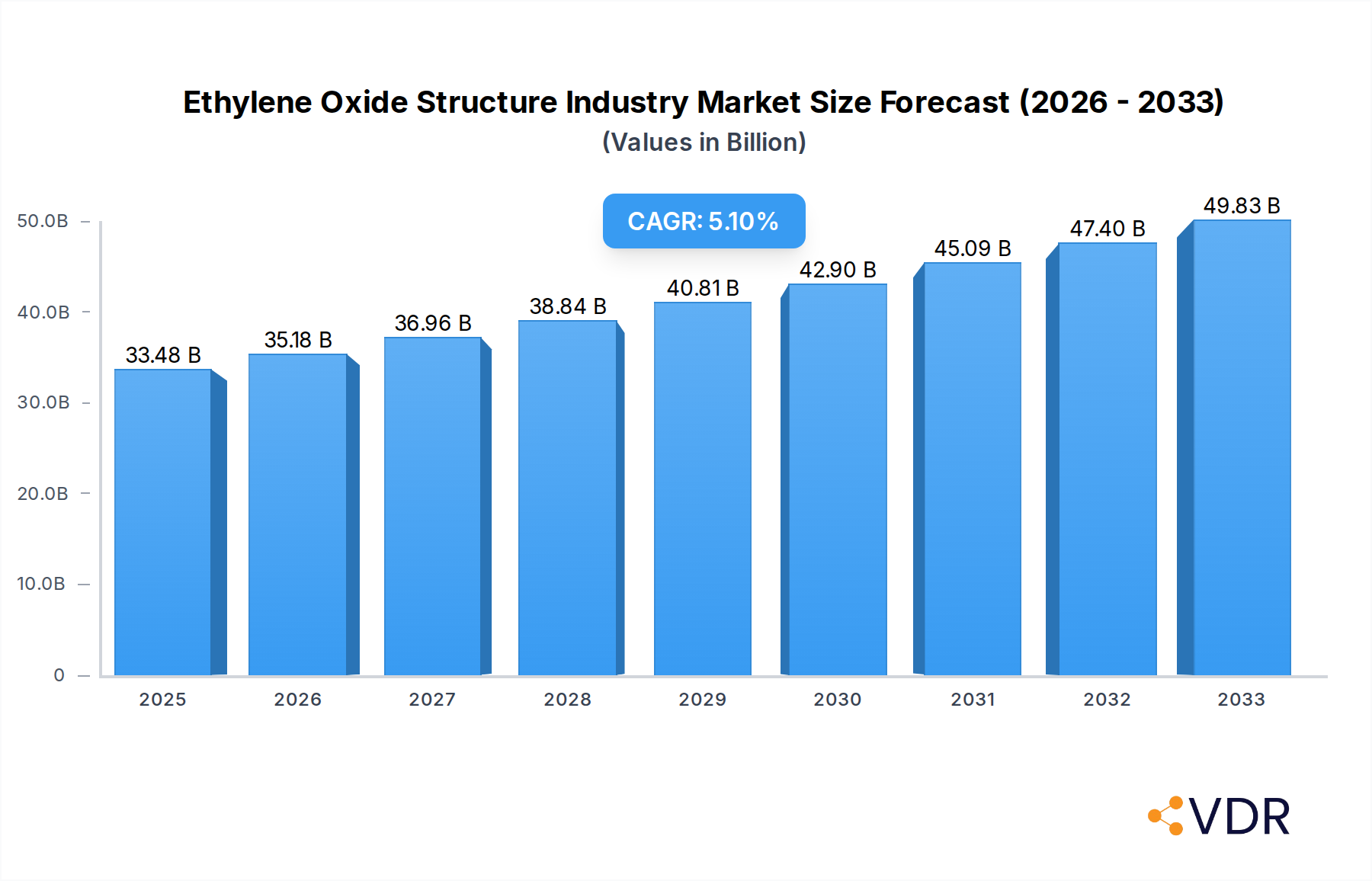

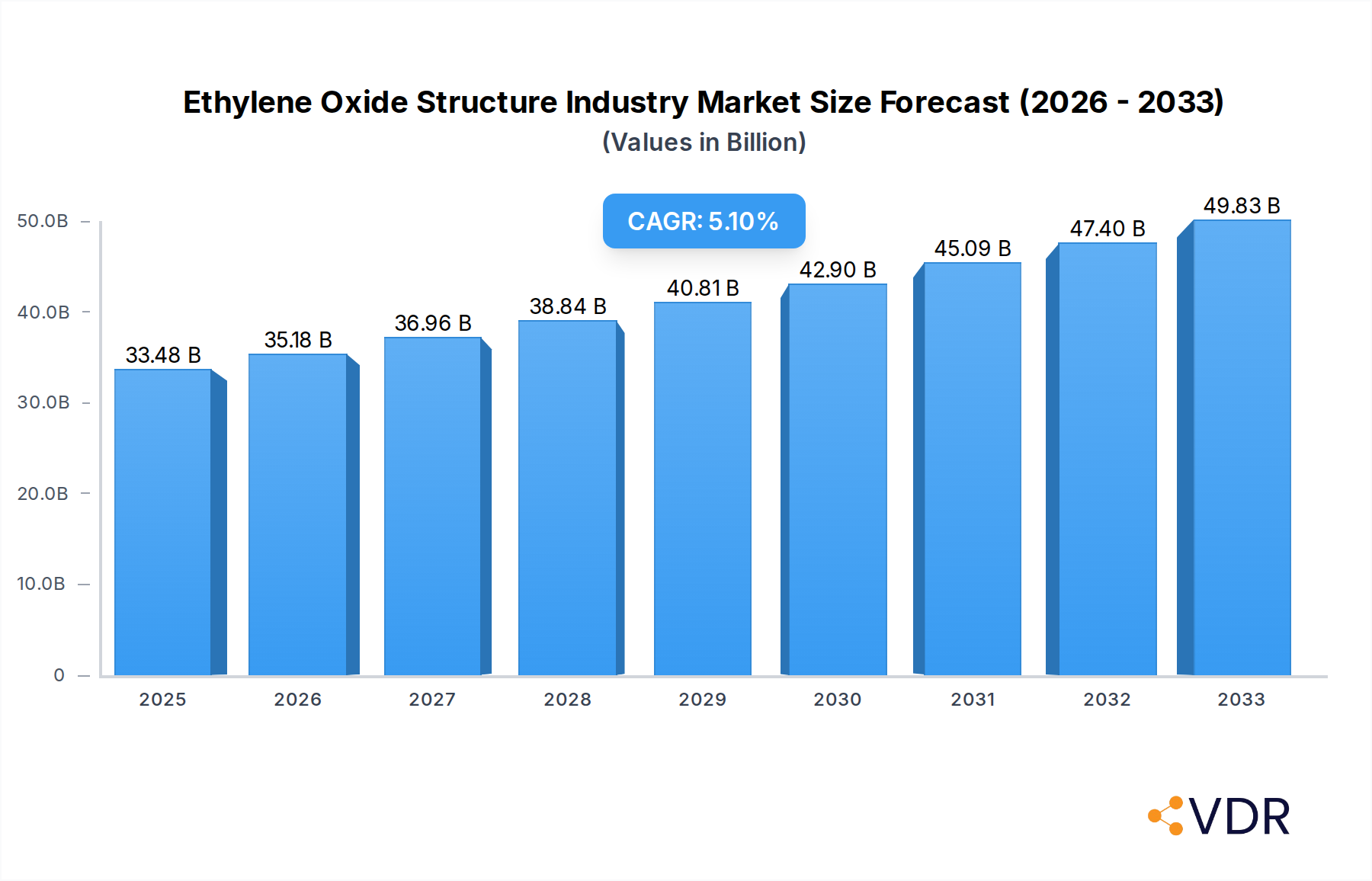

The global Ethylene Oxide market is poised for significant expansion, driven by its fundamental role as a precursor in numerous chemical manufacturing processes. With a projected market size of $33,483 million in 2025, the industry is expected to grow at a robust CAGR of 5.13% through 2033. This growth is underpinned by escalating demand from key end-user industries, including automotive, where it is crucial for antifreeze and coolants; textiles, for polyester fiber production; and personal care, for surfactants and emulsifiers. The increasing consumer demand for detergents and pharmaceuticals further fuels the need for ethylene oxide derivatives. Geographically, the Asia Pacific region, led by China and India, is anticipated to dominate market share due to rapid industrialization and a burgeoning middle class. North America and Europe also represent substantial markets, driven by advanced manufacturing capabilities and a strong emphasis on R&D for novel applications.

Ethylene Oxide Structure Industry Market Size (In Billion)

The market's dynamism is shaped by a series of interconnected drivers and trends. A primary driver is the increasing global population and the subsequent rise in demand for consumer goods that rely on ethylene oxide derivatives, such as plastics, solvents, and personal hygiene products. Technological advancements in production processes, leading to greater efficiency and reduced environmental impact, are also propelling growth. Emerging applications in specialty chemicals and the development of bio-based ethylene oxide are creating new avenues for market penetration. However, the industry faces restraints such as volatile raw material prices, particularly crude oil, which directly impacts ethylene production costs. Stringent environmental regulations concerning the handling and emissions of ethylene oxide also necessitate significant investment in compliance and safety measures. Despite these challenges, the inherent versatility of ethylene oxide and its indispensable role in a vast array of everyday products ensure its continued market prominence and expansion in the coming years.

Ethylene Oxide Structure Industry Company Market Share

Ethylene Oxide Structure Industry: Comprehensive Market Analysis and Future Outlook (2019-2033)

This in-depth report provides a definitive analysis of the global Ethylene Oxide (EO) Structure Industry, covering its intricate market dynamics, growth trajectory, regional dominance, product landscape, and key strategic drivers. With a focus on high-traffic keywords such as "ethylene oxide derivatives," "monoethylene glycol market," "ethoxylates applications," and "ethanolamines industry," this report is optimized for maximum search engine visibility and engagement among industry professionals, investors, and stakeholders. We present a comprehensive outlook from 2019 to 2033, with a detailed Base Year of 2025, offering critical insights into parent and child markets for enhanced strategic decision-making. All quantitative data is presented in million units.

Ethylene Oxide Structure Industry Market Dynamics & Structure

The Ethylene Oxide (EO) Structure Industry is characterized by a moderately concentrated market, driven by significant technological innovation in its downstream derivatives. Key players leverage advanced catalytic processes and scale economies to maintain competitive advantages. Regulatory frameworks, particularly concerning safety and environmental impact, play a crucial role in shaping manufacturing practices and investment decisions. Competitive product substitutes, while present in some niche applications, are largely outpaced by the versatility and cost-effectiveness of EO derivatives. End-user demographics are evolving, with increasing demand from emerging economies and a growing preference for specialized applications. Mergers and acquisitions (M&A) are strategic tools employed by major companies to consolidate market share, expand product portfolios, and gain access to new technologies or geographic regions.

- Market Concentration: Dominated by a few large multinational corporations, with significant contributions from regional players.

- Technological Innovation: Focus on process efficiency, catalyst development, and the creation of novel EO derivatives with enhanced performance.

- Regulatory Frameworks: Stringent environmental and safety standards, influencing operational costs and R&D investments.

- Competitive Substitutes: Limited impact due to the broad applicability and established value chain of EO derivatives.

- End-User Demographics: Growing demand from developing nations, coupled with a shift towards high-value, specialized applications.

- M&A Trends: Strategic acquisitions and joint ventures to secure raw material supply, expand capacity, and enter new market segments.

Ethylene Oxide Structure Industry Growth Trends & Insights

The global Ethylene Oxide (EO) Structure Industry is poised for robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of XX% between 2025 and 2033. This expansion is underpinned by a confluence of factors including a rising global population, increasing industrialization, and sustained demand across a wide spectrum of end-user industries. The market size, estimated at XX million units in 2025, is expected to reach XX million units by 2033. Adoption rates of EO derivatives are accelerating, particularly in regions undergoing rapid economic development. Technological disruptions, such as advancements in EO production processes and the development of bio-based alternatives, are continuously reshaping the competitive landscape. Consumer behavior shifts, including a growing awareness of sustainability and product performance, are influencing the demand for specific EO derivatives, such as those used in eco-friendly detergents and advanced material applications.

- Market Size Evolution: Significant growth trajectory driven by increasing downstream demand.

- Adoption Rates: Accelerating adoption across diverse end-user industries, especially in emerging markets.

- Technological Disruptions: Innovations in production efficiency and the emergence of sustainable EO derivatives.

- Consumer Behavior Shifts: Growing preference for high-performance and environmentally conscious products, influencing EO derivative selection.

- Market Penetration: Increasing penetration of EO derivatives into established and emerging applications, solidifying their indispensable role in modern manufacturing.

Dominant Regions, Countries, or Segments in Ethylene Oxide Structure Industry

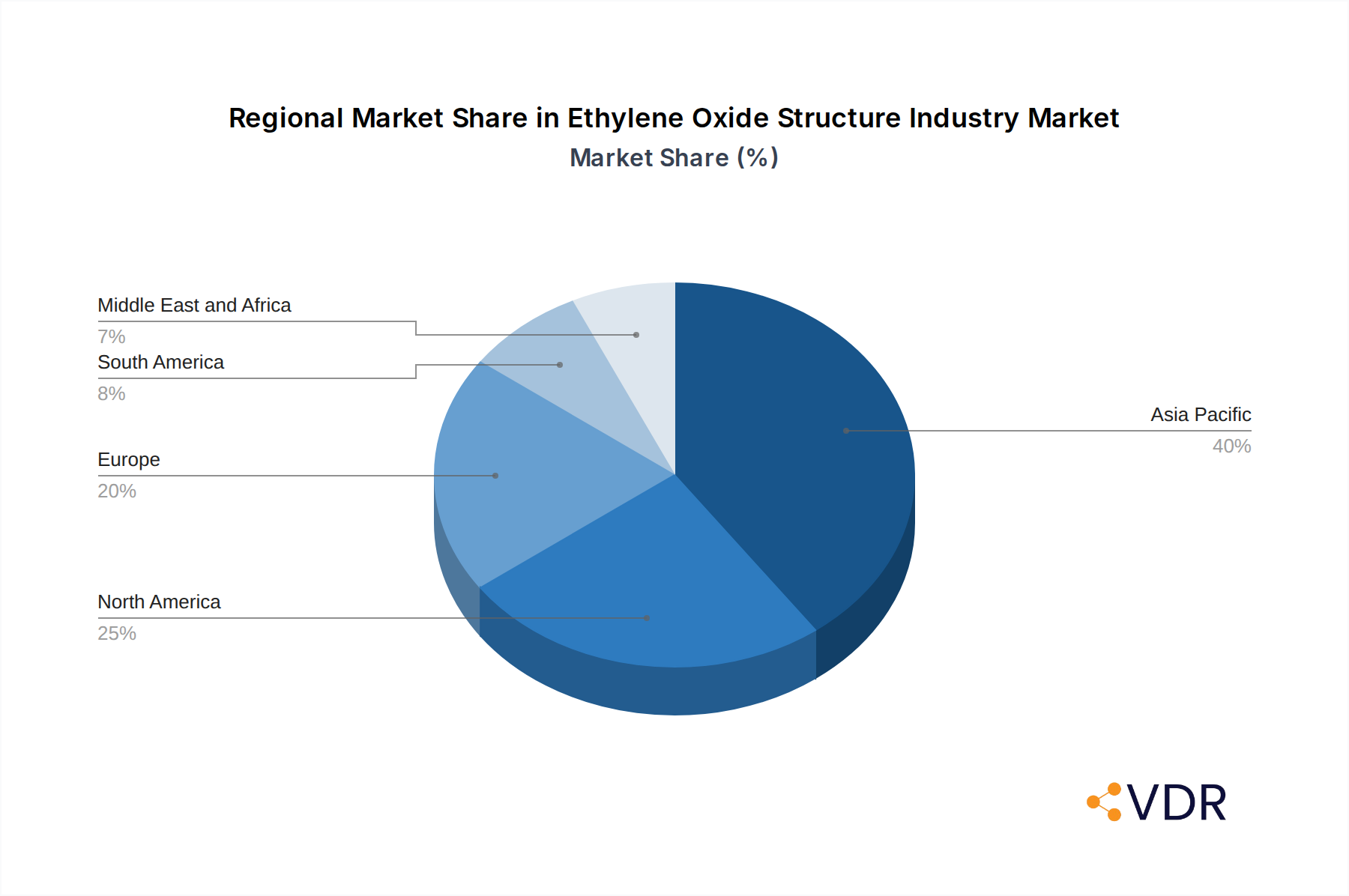

The Ethylene Oxide (EO) Structure Industry is experiencing significant growth and dominance across several key regions and segments. Asia Pacific, led by China and India, currently holds the largest market share, driven by robust industrial growth, a burgeoning manufacturing sector, and substantial investments in petrochemical infrastructure. The Ethylene Glycols segment, particularly Monoethylene Glycol (MEG), stands as the dominant derivative, propelled by its extensive use in the production of polyester fibers and PET (Polyethylene Terephthalate) resins, which are integral to the textile and packaging industries, respectively. Within end-user industries, the Textile sector remains a primary consumer of MEG, while the Detergents industry exhibits strong demand for ethoxylates.

Dominant Region: Asia Pacific (especially China and India)

- Key Drivers: Rapid industrialization, strong manufacturing base, significant government support for petrochemical industries, and a large domestic consumer market.

- Market Share: Accounts for over XX% of the global EO market.

- Growth Potential: Continual expansion driven by ongoing investments and increasing demand for downstream products.

Dominant Derivative Segment: Ethylene Glycols

- Monoethylene Glycol (MEG): Primary driver due to its extensive use in polyester and PET production.

- Market Share: Estimated at XX% of the total EO derivative market.

- Growth Drivers: Sustained demand from textile and packaging sectors, increasing production of synthetic fibers and plastic bottles.

- Diethylene Glycol (DEG) & Triethylene Glycol (TEG): Significant demand from applications like plasticizers, humectants, and solvents.

- Monoethylene Glycol (MEG): Primary driver due to its extensive use in polyester and PET production.

Dominant End-User Industry: Textile Industry

- Key Drivers: Global demand for apparel, home furnishings, and industrial textiles.

- Impact: Direct correlation between textile production volumes and MEG consumption.

Emerging Dominant Segments:

- Ethoxylates: Growing demand in the detergents and personal care sectors due to their surfactant properties.

- Ethanolamines: Increasing application in gas treating, pharmaceuticals, and agrochemicals.

Ethylene Oxide Structure Industry Product Landscape

The Ethylene Oxide (EO) structure industry encompasses a diverse range of critical derivatives that serve as foundational building blocks for countless industrial and consumer products. Ethylene Glycols, including Monoethylene Glycol (MEG), Diethylene Glycol (DEG), and Triethylene Glycol (TEG), are paramount, with MEG being the largest volume derivative utilized primarily in polyester fibers and PET resins. Ethoxylates are vital as surfactants in detergents and personal care products, offering excellent cleaning and emulsifying properties. Ethanolamines, such as Monoethanolamine (MEA), Diethanolamine (DEA), and Triethanolamine (TEA), find extensive applications in gas sweetening, pharmaceuticals, and as emulsifiers. Glycol Ethers serve as versatile solvents in paints, coatings, and cleaners. Polyethylene Glycol (PEG), with its varying molecular weights, is indispensable in pharmaceuticals, cosmetics, and as a lubricant. This diverse product landscape underscores the foundational role of EO in modern manufacturing.

Key Drivers, Barriers & Challenges in Ethylene Oxide Structure Industry

Key Drivers:

The Ethylene Oxide (EO) Structure Industry is propelled by several significant drivers. The burgeoning demand for polyester fibers and PET resins in the global textile and packaging industries remains a primary growth engine, directly fueling the consumption of Monoethylene Glycol (MEG). Rapid industrialization and urbanization in emerging economies, particularly in Asia, are creating substantial demand for EO derivatives across various sectors, including automotive, construction, and consumer goods. Technological advancements in EO production processes are enhancing efficiency and cost-effectiveness, while the development of specialized EO derivatives with improved performance characteristics is opening new application avenues. The growing emphasis on personal care and hygiene products is driving the demand for ethoxylates, while the need for effective gas treatment in the energy sector supports the consumption of ethanolamines.

Key Barriers & Challenges:

Despite its robust growth prospects, the EO Structure Industry faces several challenges. Volatility in the prices of key raw materials, particularly ethylene and natural gas, poses a significant risk to profit margins and pricing strategies. Stringent environmental regulations and safety concerns associated with the production and handling of EO necessitate substantial investments in compliance and safety measures, potentially increasing operational costs. The capital-intensive nature of EO production facilities can be a barrier to entry for new players. Furthermore, geopolitical instability and supply chain disruptions can impact the availability and cost of raw materials and finished products, affecting global trade dynamics. Intense competition among established players and the emergence of potential bio-based alternatives for certain derivatives also present competitive pressures.

Emerging Opportunities in Ethylene Oxide Structure Industry

Emerging opportunities within the Ethylene Oxide (EO) Structure Industry are manifold and present significant growth potential. The increasing global focus on sustainability is driving demand for bio-based EO derivatives and processes, creating avenues for innovation and market differentiation. The burgeoning pharmaceutical and healthcare sectors are creating new applications for polyethylene glycols (PEGs) and specialty ethanolamines, particularly in drug delivery systems and medical formulations. The automotive industry's shift towards electric vehicles is also indirectly creating opportunities for EO derivatives used in battery manufacturing and lightweight materials. Furthermore, the growing demand for high-performance agrochemicals and advanced materials in developing economies presents a fertile ground for expanding the market reach of various EO derivatives.

Growth Accelerators in the Ethylene Oxide Structure Industry Industry

Several catalysts are accelerating the long-term growth of the Ethylene Oxide (EO) Structure Industry. Ongoing technological breakthroughs in catalyst design and process optimization are leading to more efficient and cost-effective EO production, thereby enhancing competitiveness. Strategic partnerships and joint ventures between major industry players are fostering collaboration, enabling the sharing of R&D resources, and facilitating market expansion into new geographies. The continuous innovation in developing novel EO derivatives with specialized properties tailored to evolving end-user needs is a significant growth driver. Moreover, the increasing global demand for consumer goods, driven by population growth and rising disposable incomes, provides a foundational impetus for the sustained expansion of the EO derivatives market.

Key Players Shaping the Ethylene Oxide Structure Industry Market

- Sasol

- Clariant

- Shell plc

- China Petrochemical Corporation

- INEOS

- Reliance Industries Limited

- BASF SE

- LyondellBasell Industries Holdings B V

- India Glycols Limited

- SABIC

- Dow

- NIPPON SHOKUBAI CO LTD

- LOTTE Chemical Corporation

Notable Milestones in Ethylene Oxide Structure Industry Sector

- April 2022: BASF SE and China Petrochemical Corporation announced the expansion of their Verbund site in Nanjing, China (BASF-YPC Co., Ltd.), focusing on increasing capacities for downstream chemicals including ethanolamines, a key derivative of ethylene oxide.

- January 2022: ExxonMobil and SABIC announced the successful startup of Gulf Coast Growth Ventures' manufacturing facility in San Patricio County, Texas, featuring a world-scale mono-ethylene glycol (a derivative of ethylene oxide) unit with a capacity of 1.1 million metric tons per year.

In-Depth Ethylene Oxide Structure Industry Market Outlook

The Ethylene Oxide (EO) Structure Industry is set for sustained and significant growth, fueled by innovation and expanding applications. The outlook is shaped by increasing demand for its core derivatives like Ethylene Glycols (MEG, DEG, TEG) from the burgeoning textile and packaging sectors, and ethoxylates from the growing detergent and personal care industries. Strategic investments in capacity expansions, particularly in emerging markets, coupled with ongoing research into advanced production technologies and the development of specialty EO derivatives, will be key growth accelerators. Furthermore, the industry's ability to adapt to evolving sustainability mandates and the increasing adoption of EO derivatives in high-value applications like pharmaceuticals and advanced materials will solidify its indispensable role in the global chemical landscape.

Ethylene Oxide Structure Industry Segmentation

-

1. Derivative

-

1.1. Ethylene Glycols

- 1.1.1. Monoethylene Glycol (MEG)

- 1.1.2. Diethylene Glycol (DEG)

- 1.1.3. Triethylene Glycol (TEG)

- 1.2. Ethoxylates

- 1.3. Ethanolamines

- 1.4. Glycol Ethers

- 1.5. Polyethylene Glycol

- 1.6. Other Derivatives

-

1.1. Ethylene Glycols

-

2. End-user Industry

- 2.1. Automotive

- 2.2. Agrochemicals

- 2.3. Food and Beverage

- 2.4. Textile

- 2.5. Personal Care

- 2.6. Pharmaceuticals

- 2.7. Detergents

- 2.8. Other End-user Industries

Ethylene Oxide Structure Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. Italy

- 3.4. France

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Ethylene Oxide Structure Industry Regional Market Share

Geographic Coverage of Ethylene Oxide Structure Industry

Ethylene Oxide Structure Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Derivative

- 5.1.1. Ethylene Glycols

- 5.1.1.1. Monoethylene Glycol (MEG)

- 5.1.1.2. Diethylene Glycol (DEG)

- 5.1.1.3. Triethylene Glycol (TEG)

- 5.1.2. Ethoxylates

- 5.1.3. Ethanolamines

- 5.1.4. Glycol Ethers

- 5.1.5. Polyethylene Glycol

- 5.1.6. Other Derivatives

- 5.1.1. Ethylene Glycols

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Automotive

- 5.2.2. Agrochemicals

- 5.2.3. Food and Beverage

- 5.2.4. Textile

- 5.2.5. Personal Care

- 5.2.6. Pharmaceuticals

- 5.2.7. Detergents

- 5.2.8. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Derivative

- 6. Global Ethylene Oxide Structure Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Derivative

- 6.1.1. Ethylene Glycols

- 6.1.1.1. Monoethylene Glycol (MEG)

- 6.1.1.2. Diethylene Glycol (DEG)

- 6.1.1.3. Triethylene Glycol (TEG)

- 6.1.2. Ethoxylates

- 6.1.3. Ethanolamines

- 6.1.4. Glycol Ethers

- 6.1.5. Polyethylene Glycol

- 6.1.6. Other Derivatives

- 6.1.1. Ethylene Glycols

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Automotive

- 6.2.2. Agrochemicals

- 6.2.3. Food and Beverage

- 6.2.4. Textile

- 6.2.5. Personal Care

- 6.2.6. Pharmaceuticals

- 6.2.7. Detergents

- 6.2.8. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Derivative

- 7. Asia Pacific Ethylene Oxide Structure Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Derivative

- 7.1.1. Ethylene Glycols

- 7.1.1.1. Monoethylene Glycol (MEG)

- 7.1.1.2. Diethylene Glycol (DEG)

- 7.1.1.3. Triethylene Glycol (TEG)

- 7.1.2. Ethoxylates

- 7.1.3. Ethanolamines

- 7.1.4. Glycol Ethers

- 7.1.5. Polyethylene Glycol

- 7.1.6. Other Derivatives

- 7.1.1. Ethylene Glycols

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Automotive

- 7.2.2. Agrochemicals

- 7.2.3. Food and Beverage

- 7.2.4. Textile

- 7.2.5. Personal Care

- 7.2.6. Pharmaceuticals

- 7.2.7. Detergents

- 7.2.8. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Derivative

- 8. North America Ethylene Oxide Structure Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Derivative

- 8.1.1. Ethylene Glycols

- 8.1.1.1. Monoethylene Glycol (MEG)

- 8.1.1.2. Diethylene Glycol (DEG)

- 8.1.1.3. Triethylene Glycol (TEG)

- 8.1.2. Ethoxylates

- 8.1.3. Ethanolamines

- 8.1.4. Glycol Ethers

- 8.1.5. Polyethylene Glycol

- 8.1.6. Other Derivatives

- 8.1.1. Ethylene Glycols

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Automotive

- 8.2.2. Agrochemicals

- 8.2.3. Food and Beverage

- 8.2.4. Textile

- 8.2.5. Personal Care

- 8.2.6. Pharmaceuticals

- 8.2.7. Detergents

- 8.2.8. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Derivative

- 9. Europe Ethylene Oxide Structure Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Derivative

- 9.1.1. Ethylene Glycols

- 9.1.1.1. Monoethylene Glycol (MEG)

- 9.1.1.2. Diethylene Glycol (DEG)

- 9.1.1.3. Triethylene Glycol (TEG)

- 9.1.2. Ethoxylates

- 9.1.3. Ethanolamines

- 9.1.4. Glycol Ethers

- 9.1.5. Polyethylene Glycol

- 9.1.6. Other Derivatives

- 9.1.1. Ethylene Glycols

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Automotive

- 9.2.2. Agrochemicals

- 9.2.3. Food and Beverage

- 9.2.4. Textile

- 9.2.5. Personal Care

- 9.2.6. Pharmaceuticals

- 9.2.7. Detergents

- 9.2.8. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Derivative

- 10. South America Ethylene Oxide Structure Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Derivative

- 10.1.1. Ethylene Glycols

- 10.1.1.1. Monoethylene Glycol (MEG)

- 10.1.1.2. Diethylene Glycol (DEG)

- 10.1.1.3. Triethylene Glycol (TEG)

- 10.1.2. Ethoxylates

- 10.1.3. Ethanolamines

- 10.1.4. Glycol Ethers

- 10.1.5. Polyethylene Glycol

- 10.1.6. Other Derivatives

- 10.1.1. Ethylene Glycols

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Automotive

- 10.2.2. Agrochemicals

- 10.2.3. Food and Beverage

- 10.2.4. Textile

- 10.2.5. Personal Care

- 10.2.6. Pharmaceuticals

- 10.2.7. Detergents

- 10.2.8. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Derivative

- 11. Middle East and Africa Ethylene Oxide Structure Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Derivative

- 11.1.1. Ethylene Glycols

- 11.1.1.1. Monoethylene Glycol (MEG)

- 11.1.1.2. Diethylene Glycol (DEG)

- 11.1.1.3. Triethylene Glycol (TEG)

- 11.1.2. Ethoxylates

- 11.1.3. Ethanolamines

- 11.1.4. Glycol Ethers

- 11.1.5. Polyethylene Glycol

- 11.1.6. Other Derivatives

- 11.1.1. Ethylene Glycols

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. Automotive

- 11.2.2. Agrochemicals

- 11.2.3. Food and Beverage

- 11.2.4. Textile

- 11.2.5. Personal Care

- 11.2.6. Pharmaceuticals

- 11.2.7. Detergents

- 11.2.8. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Derivative

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Sasol

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Clariant

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Shell plc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 China Petrochemical Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 INEOS

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Reliance Industries Limited

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 BASF SE

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 LyondellBasell Industries Holdings B V

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 India Glycols Limited

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 SABIC

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Dow

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 NIPPON SHOKUBAI CO LTD

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 LOTTE Chemical Corporation

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 Sasol

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Ethylene Oxide Structure Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Ethylene Oxide Structure Industry Revenue (billion), by Derivative 2025 & 2033

- Figure 3: Asia Pacific Ethylene Oxide Structure Industry Revenue Share (%), by Derivative 2025 & 2033

- Figure 4: Asia Pacific Ethylene Oxide Structure Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 5: Asia Pacific Ethylene Oxide Structure Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: Asia Pacific Ethylene Oxide Structure Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: Asia Pacific Ethylene Oxide Structure Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: North America Ethylene Oxide Structure Industry Revenue (billion), by Derivative 2025 & 2033

- Figure 9: North America Ethylene Oxide Structure Industry Revenue Share (%), by Derivative 2025 & 2033

- Figure 10: North America Ethylene Oxide Structure Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 11: North America Ethylene Oxide Structure Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: North America Ethylene Oxide Structure Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: North America Ethylene Oxide Structure Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Ethylene Oxide Structure Industry Revenue (billion), by Derivative 2025 & 2033

- Figure 15: Europe Ethylene Oxide Structure Industry Revenue Share (%), by Derivative 2025 & 2033

- Figure 16: Europe Ethylene Oxide Structure Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 17: Europe Ethylene Oxide Structure Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: Europe Ethylene Oxide Structure Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Ethylene Oxide Structure Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America Ethylene Oxide Structure Industry Revenue (billion), by Derivative 2025 & 2033

- Figure 21: South America Ethylene Oxide Structure Industry Revenue Share (%), by Derivative 2025 & 2033

- Figure 22: South America Ethylene Oxide Structure Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 23: South America Ethylene Oxide Structure Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: South America Ethylene Oxide Structure Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: South America Ethylene Oxide Structure Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Ethylene Oxide Structure Industry Revenue (billion), by Derivative 2025 & 2033

- Figure 27: Middle East and Africa Ethylene Oxide Structure Industry Revenue Share (%), by Derivative 2025 & 2033

- Figure 28: Middle East and Africa Ethylene Oxide Structure Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 29: Middle East and Africa Ethylene Oxide Structure Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Middle East and Africa Ethylene Oxide Structure Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa Ethylene Oxide Structure Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Ethylene Oxide Structure Industry Revenue billion Forecast, by Derivative 2020 & 2033

- Table 2: Global Ethylene Oxide Structure Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: Global Ethylene Oxide Structure Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Ethylene Oxide Structure Industry Revenue billion Forecast, by Derivative 2020 & 2033

- Table 5: Global Ethylene Oxide Structure Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Ethylene Oxide Structure Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: China Ethylene Oxide Structure Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: India Ethylene Oxide Structure Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Japan Ethylene Oxide Structure Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: South Korea Ethylene Oxide Structure Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Rest of Asia Pacific Ethylene Oxide Structure Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Global Ethylene Oxide Structure Industry Revenue billion Forecast, by Derivative 2020 & 2033

- Table 13: Global Ethylene Oxide Structure Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 14: Global Ethylene Oxide Structure Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United States Ethylene Oxide Structure Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Ethylene Oxide Structure Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Mexico Ethylene Oxide Structure Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Global Ethylene Oxide Structure Industry Revenue billion Forecast, by Derivative 2020 & 2033

- Table 19: Global Ethylene Oxide Structure Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 20: Global Ethylene Oxide Structure Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Germany Ethylene Oxide Structure Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: United Kingdom Ethylene Oxide Structure Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Italy Ethylene Oxide Structure Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: France Ethylene Oxide Structure Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Rest of Europe Ethylene Oxide Structure Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Global Ethylene Oxide Structure Industry Revenue billion Forecast, by Derivative 2020 & 2033

- Table 27: Global Ethylene Oxide Structure Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 28: Global Ethylene Oxide Structure Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 29: Brazil Ethylene Oxide Structure Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Argentina Ethylene Oxide Structure Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of South America Ethylene Oxide Structure Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global Ethylene Oxide Structure Industry Revenue billion Forecast, by Derivative 2020 & 2033

- Table 33: Global Ethylene Oxide Structure Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 34: Global Ethylene Oxide Structure Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 35: Saudi Arabia Ethylene Oxide Structure Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: South Africa Ethylene Oxide Structure Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Rest of Middle East and Africa Ethylene Oxide Structure Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ethylene Oxide Structure Industry?

The projected CAGR is approximately 4.4%.

2. Which companies are prominent players in the Ethylene Oxide Structure Industry?

Key companies in the market include Sasol, Clariant, Shell plc, China Petrochemical Corporation, INEOS, Reliance Industries Limited, BASF SE, LyondellBasell Industries Holdings B V, India Glycols Limited, SABIC, Dow, NIPPON SHOKUBAI CO LTD, LOTTE Chemical Corporation.

3. What are the main segments of the Ethylene Oxide Structure Industry?

The market segments include Derivative, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.42 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Usage of PET in the Food and Beverage Industry; Increasing Demand for Household and Personal Care Products in the Developing Countries.

6. What are the notable trends driving market growth?

Increasing Demand from the Textile Industry.

7. Are there any restraints impacting market growth?

Health and Environmental Effects over High Exposure.

8. Can you provide examples of recent developments in the market?

In April 2022: BASF SE and China Petrochemical Corporation announced the expansion of their Verbund site located in China operated by BASF-YPC Co., Ltd. It is a 50-50 joint venture of both companies in Nanjing. The expansion will focus on increasing the capacities of many downstream chemicals, including ethanolamines which are the derivatives of ethylene oxide.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ethylene Oxide Structure Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ethylene Oxide Structure Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ethylene Oxide Structure Industry?

To stay informed about further developments, trends, and reports in the Ethylene Oxide Structure Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence