Key Insights

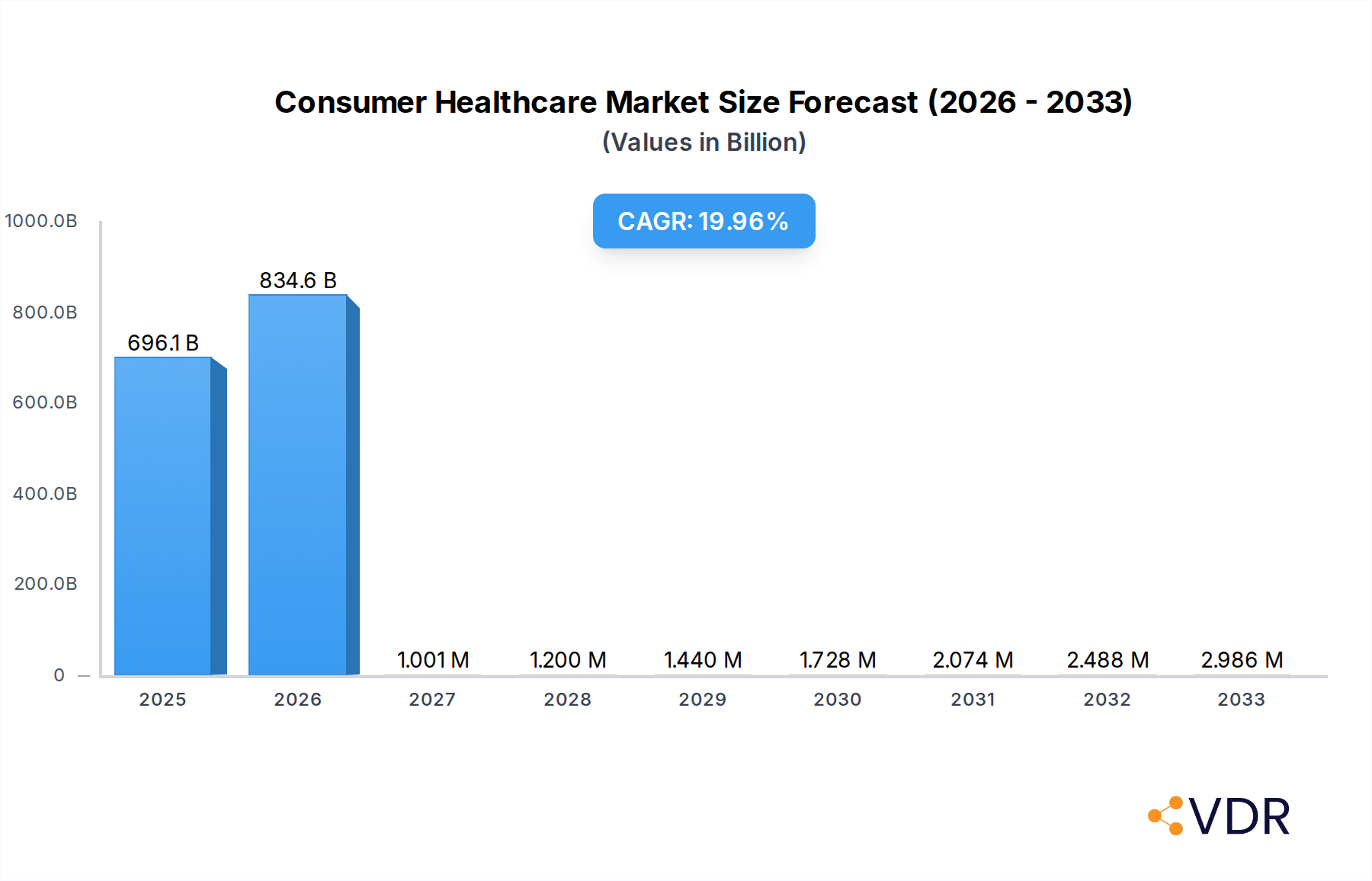

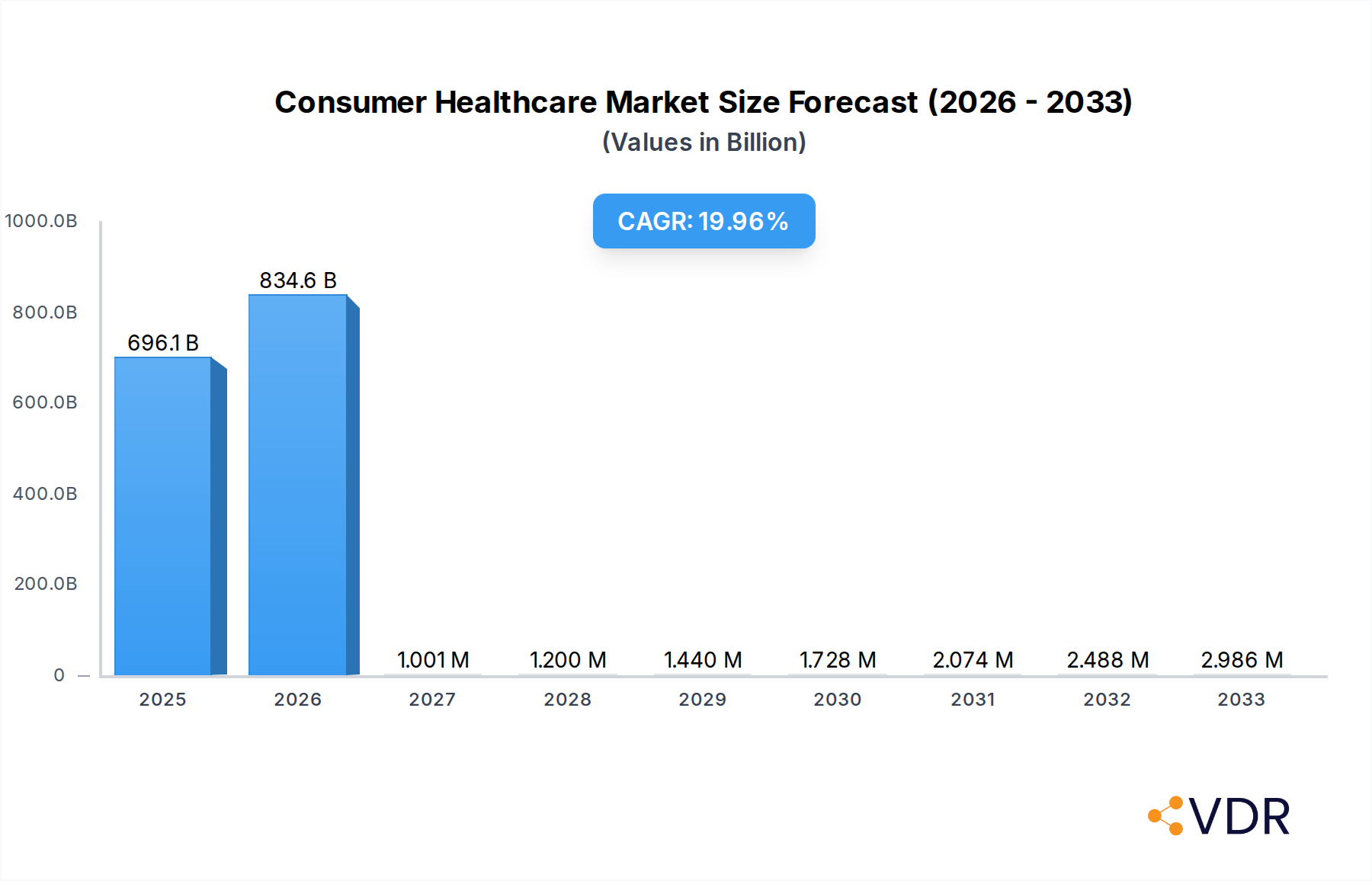

The global Consumer Healthcare market is poised for significant expansion, projected to reach USD 696.1 billion in 2025. This robust growth is fueled by an impressive Compound Annual Growth Rate (CAGR) of 19.9% throughout the forecast period. This upward trajectory is primarily driven by a confluence of factors including increasing consumer awareness regarding preventative health and wellness, a growing demand for over-the-counter (OTC) pharmaceuticals, and a rising preference for dietary supplements. The aging global population, coupled with a higher disposable income in emerging economies, further accentuates the demand for accessible and effective consumer healthcare solutions. Furthermore, the burgeoning online pharmacy segment is democratizing access to these products, making them more convenient and affordable for a wider demographic. Technological advancements in product formulation and innovative delivery systems are also contributing to market dynamism, offering consumers more tailored and effective options.

Consumer Healthcare Market Size (In Billion)

The market's evolution is also shaped by key trends such as the increasing integration of digital health solutions, personalized nutrition, and a growing emphasis on natural and organic ingredients in both pharmaceuticals and supplements. While the market exhibits strong growth potential, certain restraints exist, including stringent regulatory frameworks in some regions and intense competition among a large pool of established and emerging players. However, strategic initiatives by key companies, including product innovation, mergers and acquisitions, and expanding distribution networks, are expected to overcome these challenges. The diverse segmentation, encompassing hospital pharmacies, retail pharmacies, and online pharmacies, along with OTC pharmaceuticals and dietary supplements, indicates a broad and dynamic market landscape catering to a wide spectrum of consumer needs and preferences across various regions like North America, Europe, Asia Pacific, and others.

Consumer Healthcare Company Market Share

Comprehensive Consumer Healthcare Market Analysis: Dynamics, Trends, and Future Outlook (2019-2033)

This in-depth report provides a definitive analysis of the global Consumer Healthcare market, covering market dynamics, growth trends, regional dominance, product landscape, key drivers, barriers, opportunities, and a detailed outlook for the period 2019-2033. Leveraging proprietary research and extensive industry data, this report equips stakeholders with critical insights to navigate the evolving consumer health sector, encompassing both parent and child market segments. The report focuses on high-traffic keywords relevant to industry professionals and decision-makers.

Consumer Healthcare Market Dynamics & Structure

The global consumer healthcare market is characterized by a moderately consolidated structure, with major players like Johnson & Johnson, Bayer Healthcare, GlaxoSmithKline, Sanofi, and Pfizer holding significant market shares. Technological innovation, particularly in areas like personalized nutrition, digital health integration, and advanced delivery systems for OTC pharmaceuticals, acts as a key driver. Stringent regulatory frameworks governing product safety and efficacy, managed by bodies like the FDA and EMA, influence market entry and product development. The presence of competitive product substitutes, including traditional remedies and emerging wellness products, necessitates continuous innovation and strong brand differentiation. End-user demographics are shifting towards an aging population with increased disposable income and a growing preference for preventative health solutions, alongside a younger, digitally-savvy demographic seeking convenient and accessible health products. Mergers and Acquisitions (M&A) remain a prevalent strategy for market expansion and portfolio diversification, with an average of 15-20 significant deals recorded annually in the historical period.

- Market Concentration: Moderately concentrated with top 5 players accounting for approximately 55-60% of the market share in the estimated year 2025.

- Technological Innovation Drivers: Personalized nutrition, AI-driven diagnostics, wearable health trackers, advanced delivery mechanisms for OTC pharmaceuticals, and sustainable product formulations.

- Regulatory Frameworks: FDA, EMA, national health authorities, compliance with GMP, and evolving data privacy regulations for digital health solutions.

- Competitive Product Substitutes: Herbal supplements, functional foods, traditional medicine, private label brands, and direct-to-consumer diagnostic kits.

- End-User Demographics: Aging population, millennials, Gen Z, individuals with chronic conditions, and health-conscious consumers.

- M&A Trends: Strategic acquisitions of innovative startups, divestitures of non-core assets, and collaborations for R&D and market access.

Consumer Healthcare Growth Trends & Insights

The consumer healthcare market is poised for substantial growth, driven by increasing health awareness, an aging global population, and a growing preference for self-care and preventative health solutions. The global market size is projected to expand from approximately $370 billion units in the historical period to an estimated $580 billion units by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of around 4.5% during the forecast period. Adoption rates for dietary supplements and OTC pharmaceuticals are accelerating, fueled by accessible product information and rising disposable incomes in emerging economies. Technological disruptions, including the integration of AI in product recommendation engines and personalized health plans, are transforming how consumers engage with healthcare products. Consumer behavior shifts are marked by a greater emphasis on holistic wellness, a demand for transparent ingredient sourcing, and a preference for digital channels for product research and purchase. The online pharmacy segment, in particular, is experiencing rapid expansion, projected to grow at a CAGR of over 6% during the forecast period.

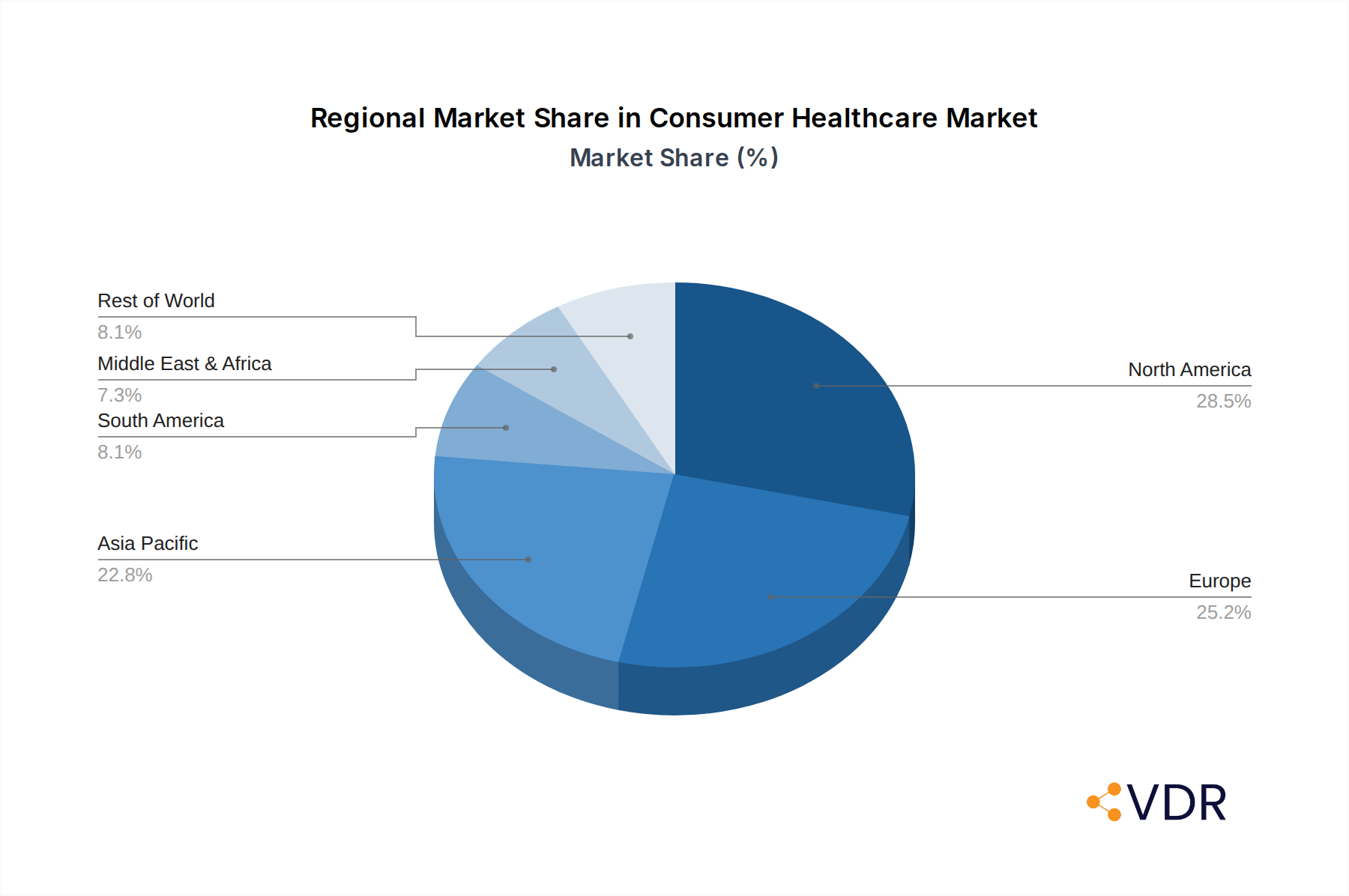

Dominant Regions, Countries, or Segments in Consumer Healthcare

North America currently holds a dominant position in the global consumer healthcare market, driven by high disposable incomes, advanced healthcare infrastructure, and a well-established culture of self-care. The United States, as the largest market within this region, contributes significantly to the growth of OTC Pharmaceuticals and Dietary Supplements segments. In the estimated year 2025, North America is expected to account for over 30% of the global market revenue. The dominance is further amplified by strong economic policies that support market innovation and consumer spending on health and wellness products. Key drivers include extensive retail pharmacy networks and a burgeoning online pharmacy sector, facilitated by robust logistics and widespread internet penetration.

- Dominant Region: North America, with the United States as the leading country.

- Leading Segments: OTC Pharmaceuticals and Dietary Supplements are the primary growth engines.

- Key Drivers:

- Economic Policies: Favorable reimbursement policies for OTC products and supportive regulations for dietary supplements.

- Infrastructure: Extensive network of retail pharmacies and well-developed e-commerce platforms for online sales.

- Consumer Behavior: High awareness of preventive healthcare and a strong inclination towards self-medication and nutritional supplements.

- Aging Population: Increasing prevalence of age-related conditions driving demand for health-promoting products.

- Market Share & Growth Potential: North America is expected to maintain its leading position throughout the forecast period, with an estimated market share of 32-35% by 2033. The Dietary Supplements segment is projected to witness a CAGR of approximately 5.2%, while OTC Pharmaceuticals will grow at around 4.0%.

Consumer Healthcare Product Landscape

The consumer healthcare product landscape is characterized by a continuous stream of innovations focused on enhanced efficacy, convenience, and personalized consumer needs. OTC pharmaceuticals are witnessing advancements in formulations for faster symptom relief and improved patient compliance. Dietary supplements are evolving beyond basic vitamins and minerals to include specialized formulations targeting specific health concerns like gut health, cognitive function, and immune support, with a growing emphasis on bioavailable ingredients and sustainable sourcing. The application in Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy segments dictates product development, with online channels increasingly featuring direct-to-consumer (DTC) personalized health kits and subscription services. Unique selling propositions often revolve around scientifically backed claims, natural ingredients, and user-friendly packaging.

Key Drivers, Barriers & Challenges in Consumer Healthcare

Key Drivers: The consumer healthcare market is propelled by several key drivers, including rising global health consciousness, an increasing prevalence of chronic diseases, and a growing preference for self-care. Technological advancements in product development, such as novel drug delivery systems and personalized nutrition formulations, are also significant catalysts. Favorable government initiatives promoting preventive healthcare and the accessibility of over-the-counter (OTC) medications further fuel market expansion.

Key Barriers & Challenges: Despite robust growth, the industry faces significant challenges. Stringent regulatory hurdles and the lengthy approval processes for new products can impede market entry. Intense competition from both established players and emerging brands, coupled with pricing pressures, poses a constant challenge. Supply chain disruptions, geopolitical uncertainties, and increasing consumer demand for evidence-based claims require continuous adaptation and investment in research and development. The estimated impact of regulatory delays can add 12-18 months to product launch timelines.

Emerging Opportunities in Consumer Healthcare

Emerging opportunities in consumer healthcare are primarily concentrated in personalized health solutions, digital therapeutics, and the burgeoning wellness tourism sector. The growing demand for customized dietary supplements, tailored to individual genetic profiles and lifestyle needs, presents a significant untapped market. The integration of AI and wearable technology for proactive health monitoring and management opens avenues for innovative digital therapeutics. Furthermore, the increasing consumer focus on holistic well-being is creating opportunities for integrated health and wellness programs that combine nutrition, fitness, and mental health support, particularly in regions with rising disposable incomes and a growing middle class.

Growth Accelerators in the Consumer Healthcare Industry

Growth in the consumer healthcare industry is significantly accelerated by ongoing technological breakthroughs in product formulation and delivery. The expansion of e-commerce and digital platforms is providing unprecedented access to a global consumer base, breaking down geographical barriers. Strategic partnerships between pharmaceutical companies, technology providers, and research institutions are fostering rapid innovation and the development of novel health solutions. Market expansion strategies, including penetration into emerging economies and the introduction of specialized product lines catering to niche health needs, are also playing a crucial role in driving sustained growth and increasing market penetration rates.

Key Players Shaping the Consumer Healthcare Market

- Johnson & Johnson

- Bayer Healthcare

- GlaxoSmithKline

- Sanofi

- Pfizer

- Boehringer Ingelheim

- Abbott Laboratories

- Merck

- Nestle

- Novartis

- Procter & Gamble

- Amway

- Danone

- BASF

- DSM

- Mylan

- Herbalife

- Kellogg

- American Health

- Sun Pharma

- Takeda Pharmaceuticals

- Teva Pharmaceuticals

- Taisho Pharmaceuticals

- Mitsubishi Tanabe Pharma

Notable Milestones in Consumer Healthcare Sector

- 2019 Q3: GlaxoSmithKline and Pfizer complete the merger of their consumer healthcare businesses to form Haleon.

- 2020 Q1: Reckitt Benckiser launches Durex Invisible Extra Thin condoms, emphasizing enhanced intimacy.

- 2021 Q2: Abbott Laboratories introduces its latest FreeStyle Libre continuous glucose monitoring system, improving diabetes management.

- 2022 Q4: Bayer AG divests its Blackmores stake, signaling a strategic shift in its consumer health portfolio.

- 2023 Q1: Sanofi invests in a new digital health platform focused on chronic disease management.

In-Depth Consumer Healthcare Market Outlook

The future outlook for the consumer healthcare market is exceptionally bright, driven by a confluence of powerful growth accelerators. Continued innovation in personalized nutrition, the rapid adoption of digital health solutions, and an unwavering global focus on preventative healthcare will shape the market's trajectory. Strategic partnerships and market expansion into underserved regions will unlock significant new revenue streams. The increasing consumer demand for scientifically validated, convenient, and sustainable health products positions the industry for sustained, robust growth, with an estimated market value projected to exceed $750 billion units by the end of the forecast period.

Consumer Healthcare Segmentation

-

1. Application

- 1.1. Hospital Pharmacy

- 1.2. Retail Pharmacy

- 1.3. Online Pharmacy

-

2. Type

- 2.1. OTC Pharmaceuticals

- 2.2. Dietary Supplements

Consumer Healthcare Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Consumer Healthcare Regional Market Share

Geographic Coverage of Consumer Healthcare

Consumer Healthcare REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 19.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Consumer Healthcare Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital Pharmacy

- 5.1.2. Retail Pharmacy

- 5.1.3. Online Pharmacy

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. OTC Pharmaceuticals

- 5.2.2. Dietary Supplements

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Consumer Healthcare Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital Pharmacy

- 6.1.2. Retail Pharmacy

- 6.1.3. Online Pharmacy

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. OTC Pharmaceuticals

- 6.2.2. Dietary Supplements

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Consumer Healthcare Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital Pharmacy

- 7.1.2. Retail Pharmacy

- 7.1.3. Online Pharmacy

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. OTC Pharmaceuticals

- 7.2.2. Dietary Supplements

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Consumer Healthcare Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital Pharmacy

- 8.1.2. Retail Pharmacy

- 8.1.3. Online Pharmacy

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. OTC Pharmaceuticals

- 8.2.2. Dietary Supplements

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Consumer Healthcare Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital Pharmacy

- 9.1.2. Retail Pharmacy

- 9.1.3. Online Pharmacy

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. OTC Pharmaceuticals

- 9.2.2. Dietary Supplements

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Consumer Healthcare Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital Pharmacy

- 10.1.2. Retail Pharmacy

- 10.1.3. Online Pharmacy

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. OTC Pharmaceuticals

- 10.2.2. Dietary Supplements

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Johnson & Johnson

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Bayer Healthcare

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 GlaxoSmithKline

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Sanofi

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Pfizer

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Boehringer Ingelheim

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Abbott Laboratories

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Merck

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Nestle

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Novartis

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Procter & Gamble

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Amway

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Danone

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 BASF

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 DSM

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Mylan

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Herbalife

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Kellogg

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 American Health

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Sun Pharma

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Takeda Pharmaceuticals

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 Teva Pharmaceuticals

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Taisho Pharmaceuticals

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Mitsubishi Tanabe Pharma

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.1 Johnson & Johnson

List of Figures

- Figure 1: Global Consumer Healthcare Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Consumer Healthcare Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Consumer Healthcare Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Consumer Healthcare Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Consumer Healthcare Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Consumer Healthcare Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Consumer Healthcare Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Consumer Healthcare Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Consumer Healthcare Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Consumer Healthcare Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Consumer Healthcare Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Consumer Healthcare Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Consumer Healthcare Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Consumer Healthcare Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Consumer Healthcare Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Consumer Healthcare Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Consumer Healthcare Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Consumer Healthcare Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Consumer Healthcare Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Consumer Healthcare Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Consumer Healthcare Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Consumer Healthcare Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Consumer Healthcare Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Consumer Healthcare Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Consumer Healthcare Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Consumer Healthcare Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Consumer Healthcare Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Consumer Healthcare Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Consumer Healthcare Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Consumer Healthcare Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Consumer Healthcare Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Consumer Healthcare Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Consumer Healthcare Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Consumer Healthcare Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Consumer Healthcare Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Consumer Healthcare Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Consumer Healthcare Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Consumer Healthcare Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Consumer Healthcare Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Consumer Healthcare Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Consumer Healthcare Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Consumer Healthcare Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Consumer Healthcare Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Consumer Healthcare Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Consumer Healthcare Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Consumer Healthcare Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Consumer Healthcare Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Consumer Healthcare Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Consumer Healthcare Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Consumer Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Consumer Healthcare?

The projected CAGR is approximately 19.9%.

2. Which companies are prominent players in the Consumer Healthcare?

Key companies in the market include Johnson & Johnson, Bayer Healthcare, GlaxoSmithKline, Sanofi, Pfizer, Boehringer Ingelheim, Abbott Laboratories, Merck, Nestle, Novartis, Procter & Gamble, Amway, Danone, BASF, DSM, Mylan, Herbalife, Kellogg, American Health, Sun Pharma, Takeda Pharmaceuticals, Teva Pharmaceuticals, Taisho Pharmaceuticals, Mitsubishi Tanabe Pharma.

3. What are the main segments of the Consumer Healthcare?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Consumer Healthcare," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Consumer Healthcare report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Consumer Healthcare?

To stay informed about further developments, trends, and reports in the Consumer Healthcare, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence