Key Insights

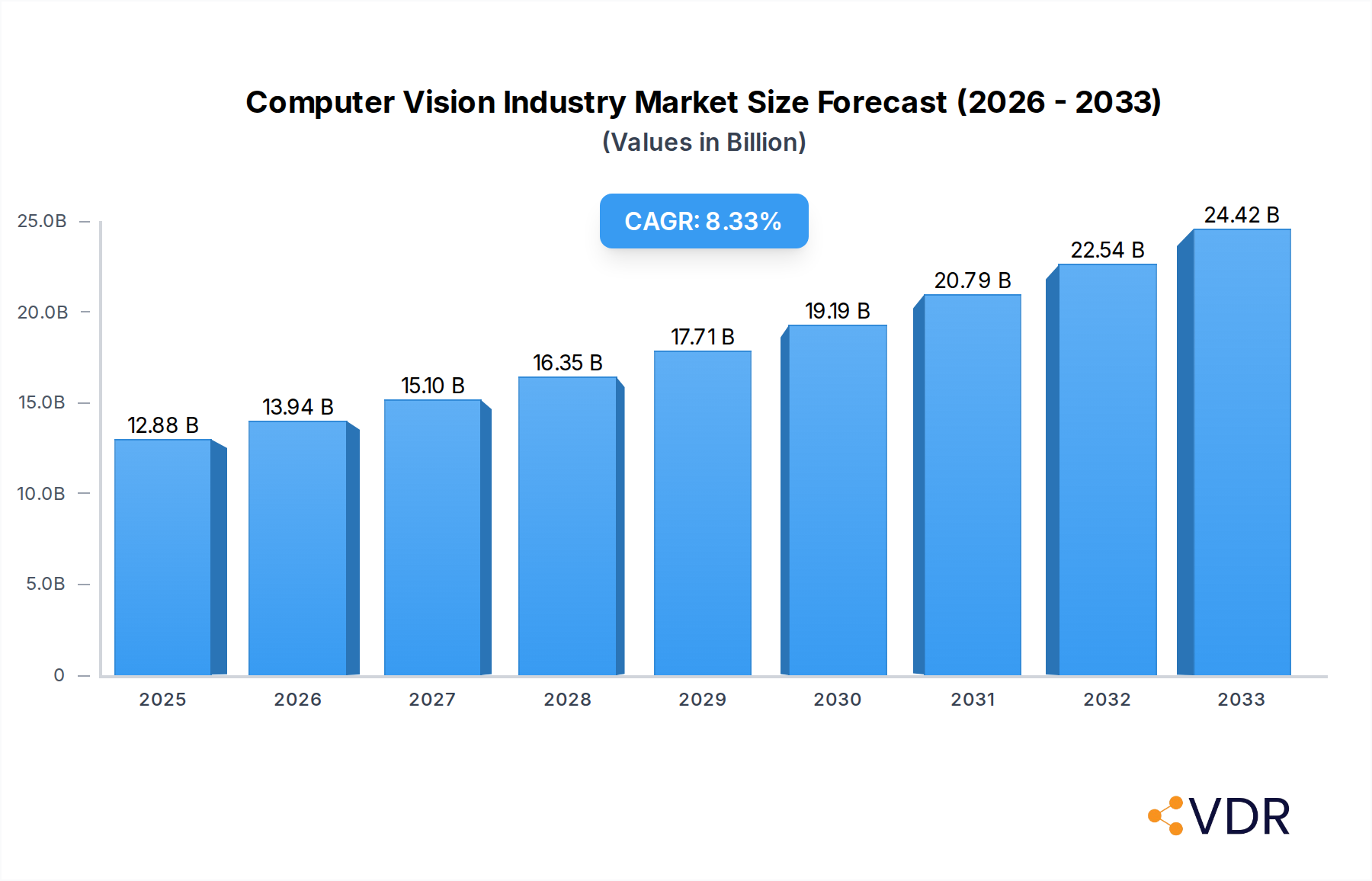

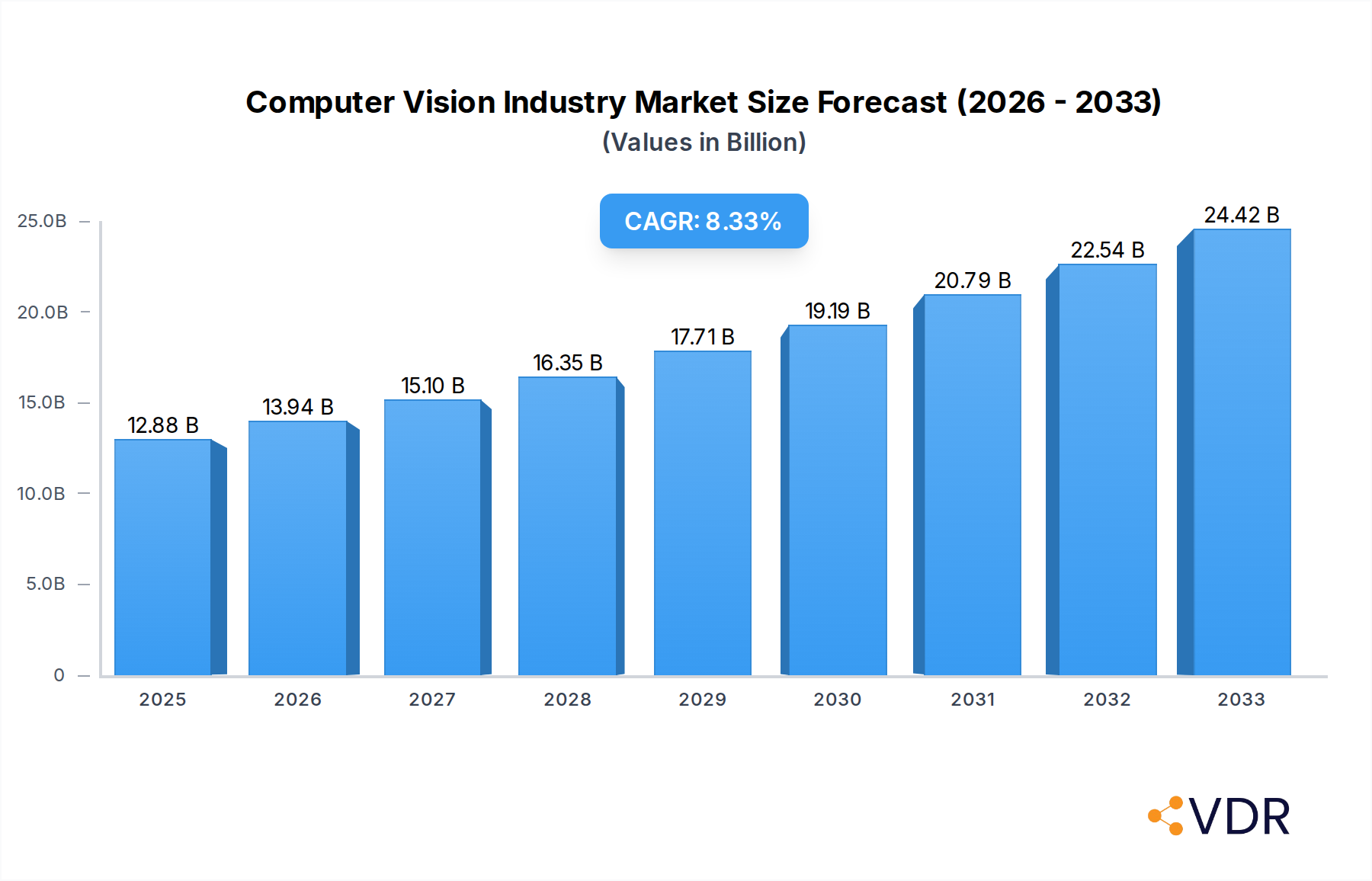

The global computer vision market is experiencing robust expansion, projected to reach an impressive USD 12.88 Billion by 2025, with a Compound Annual Growth Rate (CAGR) of 8.32% during the forecast period of 2025-2033. This significant growth is propelled by the escalating demand for automation across diverse industries, driven by the need for enhanced efficiency, precision, and quality control. The automotive sector, in particular, is a major contributor, leveraging computer vision for advanced driver-assistance systems (ADAS) and autonomous driving technologies. Similarly, the healthcare and pharmaceutical industries are increasingly adopting these technologies for medical imaging analysis, robotic surgery, and drug discovery. The logistics and retail sectors are also witnessing a surge in computer vision applications for inventory management, supply chain optimization, and enhanced customer experiences through smart retail solutions.

Computer Vision Industry Market Size (In Billion)

The market's trajectory is further bolstered by rapid advancements in artificial intelligence (AI) and machine learning (ML) algorithms, which are making computer vision systems more sophisticated and capable. The increasing accessibility and decreasing cost of hardware components like high-resolution cameras and powerful processors are also facilitating wider adoption. Smart camera-based systems are gaining traction due to their integrated processing capabilities, offering more streamlined deployment. However, challenges such as the high initial investment cost for sophisticated systems and concerns regarding data privacy and security may temper the growth in certain segments. Geographically, North America and Europe are leading the market, driven by strong technological infrastructure and early adoption rates, while the Asia Pacific region, with its burgeoning manufacturing base and increasing digitalization, presents substantial growth opportunities.

Computer Vision Industry Company Market Share

Unlocking the Future: Comprehensive Computer Vision Industry Report (2019-2033)

Gain unparalleled insights into the dynamic computer vision market with our in-depth report, covering the period from 2019 to 2033. This essential resource delves into the intricacies of machine vision technology, AI vision systems, and industrial automation, providing a 360-degree view for industry professionals, investors, and strategists. Discover the evolving landscape of image recognition, object detection, and deep learning in vision, driven by advancements in hardware and sophisticated software solutions. Analyze the impact of key players like Cognex Corporation, Keyence Corporation, and Sony Group Corporation, and understand their strategies in shaping the future of automated visual inspection and intelligent data capture.

This report offers a granular analysis of the computer vision industry size, market share, and growth projections, with all values presented in Million units. We dissect the computer vision market trends, including the proliferation of smart cameras and the increasing demand for PC-based vision systems. Explore the critical role of computer vision in manufacturing, automotive applications, and the burgeoning healthcare AI sector. With a forecast period extending to 2033, this report is your definitive guide to navigating the opportunities and challenges within this rapidly expanding technological domain.

Computer Vision Industry Market Dynamics & Structure

The computer vision industry is characterized by a moderately concentrated market structure, with a mix of large conglomerates and specialized players driving innovation. Key influencers like Keyence Corporation, Cognex Corporation, and Omron Corporation hold significant market sway, complemented by specialized providers such as MVTec Software GmbH and IDS Imaging Development Systems GmbH. Technological innovation is a primary driver, fueled by continuous advancements in AI algorithms, deep learning models, and sensor technology, enabling more sophisticated image processing and pattern recognition. The regulatory framework, particularly concerning data privacy and AI ethics, is evolving and will increasingly shape deployment strategies for computer vision solutions.

- Market Concentration: Dominated by a few large corporations, but with significant room for niche players and emerging technologies.

- Technological Innovation Drivers: Advancements in AI, machine learning, neural networks, and hardware miniaturization are crucial.

- Regulatory Frameworks: Data privacy (e.g., GDPR), AI ethics, and industry-specific compliance standards are becoming paramount.

- Competitive Product Substitutes: While direct substitutes are few, advancements in alternative automation technologies and manual inspection processes represent indirect competition.

- End-User Demographics: A broad spectrum of industries, from high-volume manufacturing to specialized healthcare, are adopting computer vision.

- M&A Trends: Strategic acquisitions by larger firms to acquire cutting-edge technology and expand market reach are prevalent. For instance, Atlas Copco's acquisition of Isra Vision AG underscores this trend.

Computer Vision Industry Growth Trends & Insights

The computer vision industry is poised for exponential growth, projected to expand from an estimated USD 15,700 million in 2025 to a substantial USD 47,500 million by 2033, exhibiting a compound annual growth rate (CAGR) of approximately 14.7%. This robust expansion is driven by the escalating adoption of machine vision systems across diverse end-user industries seeking enhanced automation, quality control, and data analytics. The historical period (2019-2024) saw consistent growth, laying the groundwork for accelerated adoption in the forecast period. The base year of 2025 serves as a pivotal point, with significant investments in R&D and the proliferation of AI-powered vision solutions.

Consumer behavior shifts, particularly the demand for greater product quality and traceability in sectors like food and beverage and healthcare, are directly translating into increased reliance on computer vision applications. Technological disruptions, including the development of more powerful and cost-effective cameras, optics, and illumination systems, along with advancements in software platforms, are democratizing access to these sophisticated technologies. The integration of edge AI and cloud-based computer vision is further enhancing performance and scalability, enabling real-time processing and intelligent decision-making. The increasing sophistication of AI vision is enabling applications far beyond simple inspection, moving towards predictive maintenance, robotic guidance, and augmented reality interfaces. This sustained upward trajectory is indicative of computer vision becoming an indispensable component of modern industrial and commercial operations.

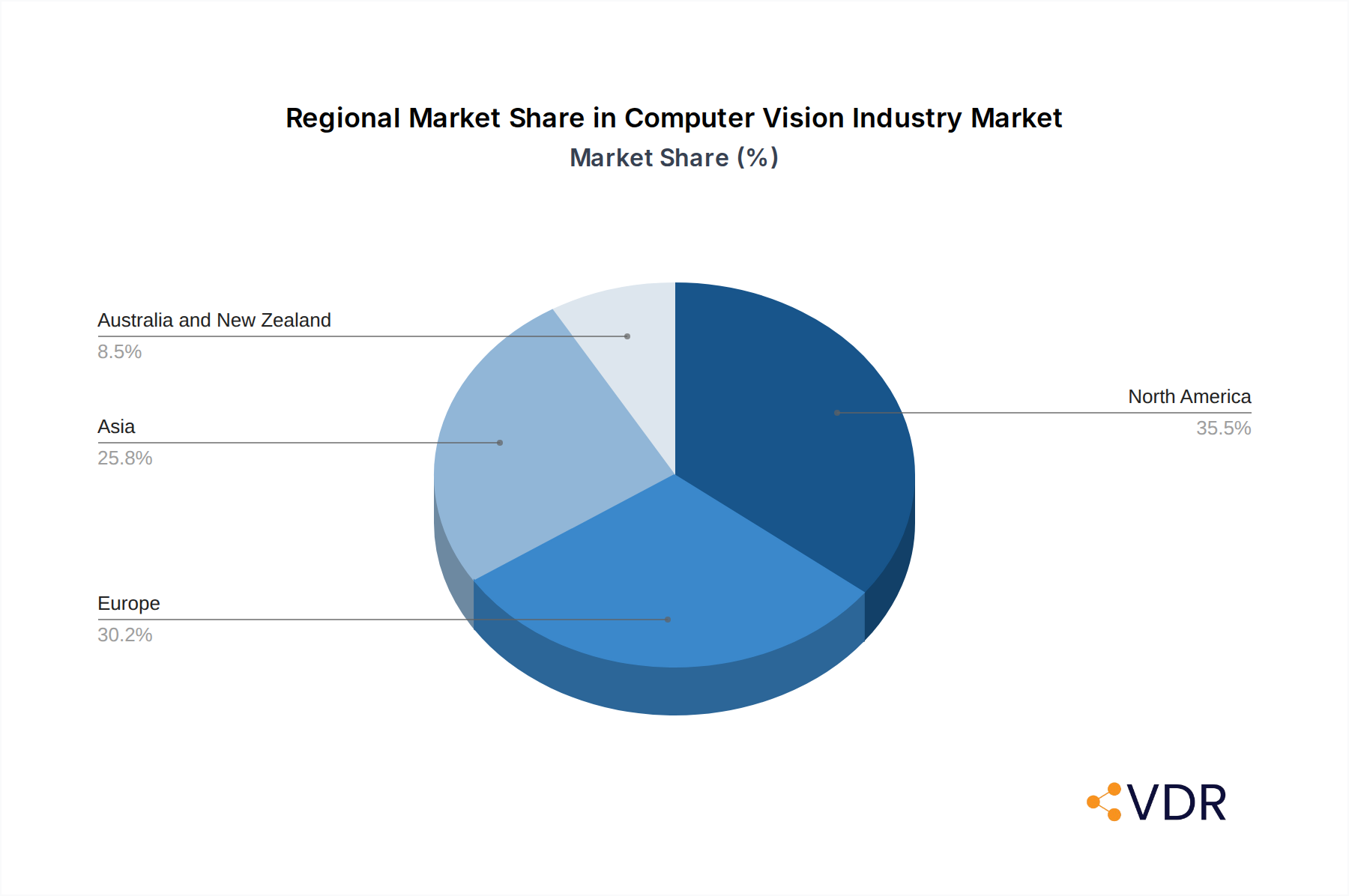

Dominant Regions, Countries, or Segments in Computer Vision Industry

The computer vision industry's dominance is currently observed in regions and segments characterized by advanced manufacturing capabilities, significant R&D investments, and a high degree of automation. North America, particularly the United States, and Europe, led by Germany, are leading the charge. Asia-Pacific, driven by countries like China, Japan, and South Korea, is emerging as a powerhouse, fueled by its vast manufacturing base and rapid technological adoption. The Electronics and Semiconductors sector stands out as a dominant end-user industry, with stringent quality control requirements and the need for precision inspection driving high demand for computer vision solutions.

- Dominant End-User Industry: Electronics and Semiconductors, driven by the need for microscopic defect detection and high-throughput inspection.

- Leading Component Segment: Hardware, with Vision Systems and Cameras forming the core, followed by essential Optics and Illumination Systems.

- Dominant Product Type: PC-based vision systems currently lead due to their flexibility and processing power, though Smart Camera-based systems are rapidly gaining traction for embedded applications.

- Key Driver: Economic Policies: Government initiatives supporting Industry 4.0, automation, and technological innovation foster market growth.

- Key Driver: Infrastructure: Robust industrial infrastructure and advanced research facilities facilitate the development and deployment of computer vision.

- Market Share & Growth Potential: The Electronics and Semiconductors segment holds a significant market share and is projected to maintain high growth due to continuous innovation and miniaturization in the electronics industry.

Computer Vision Industry Product Landscape

The computer vision industry is continuously evolving with cutting-edge product innovations. Key offerings include advanced vision systems capable of complex defect detection, high-speed cameras for capturing intricate details, and sophisticated optics and illumination systems designed for optimal image quality under diverse conditions. Software solutions leverage AI and deep learning for enhanced pattern recognition, object detection, and image analysis. Notable product developments, such as Keyence Corporation's VS series smart cameras with advanced lens control, exemplify the trend towards more adaptable and user-friendly machine vision technology. These advancements are tailored for specific applications, from meticulous inspection in healthcare and pharmaceutical to quality assurance in food and beverage and precision guidance in robotics.

Key Drivers, Barriers & Challenges in Computer Vision Industry

The computer vision industry is propelled by several key drivers, including the relentless pursuit of increased efficiency and accuracy in industrial processes, the growing demand for automation across various sectors, and the continuous advancements in AI and deep learning, which enhance the capabilities of vision systems. The integration of edge computing and the decreasing cost of powerful hardware also contribute significantly.

However, the industry faces considerable barriers and challenges. High initial implementation costs can deter smaller enterprises. The need for specialized expertise for deployment and maintenance, alongside concerns about data security and privacy, present ongoing hurdles. Furthermore, the complexity of integrating computer vision solutions into existing legacy systems and the ongoing need for algorithm refinement to adapt to ever-changing environments also pose significant challenges. Supply chain disruptions affecting component availability, particularly for specialized sensors and processors, can also impact growth.

Emerging Opportunities in Computer Vision Industry

Emerging opportunities in the computer vision industry are vast and diverse. The expansion of AI in healthcare for diagnostics and robotic surgery, the application of computer vision in retail for inventory management and personalized customer experiences, and the integration of autonomous driving technology are prime examples. The burgeoning field of augmented reality (AR) and virtual reality (VR), powered by advanced visual processing, opens new avenues for training, design, and entertainment. Furthermore, the application of machine vision in agriculture for crop monitoring and yield optimization represents a significant untapped market. The development of more generalized AI models will further democratize these applications.

Growth Accelerators in the Computer Vision Industry Industry

Several factors are acting as significant growth accelerators for the computer vision industry. Technological breakthroughs in areas like neuromorphic computing and explainable AI are poised to enhance system performance and trustworthiness. Strategic partnerships, such as the collaboration between Basler AG and MVTec Software GmbH with Siemens, are crucial for streamlining integration and expanding market reach. Furthermore, global market expansion strategies, targeting developing economies with growing industrial bases, will drive demand. The increasing availability of large, labeled datasets for training AI models is also accelerating the development and deployment of more sophisticated computer vision solutions.

Key Players Shaping the Computer Vision Industry Market

- Keyence Corporation

- IDS Imaging Development Systems GmbH (Paul Hartmann AG)

- MVTec Software GmbH

- National Instruments Corporation (Emerson)

- Cognex Corporation

- Teledyne DALSA (Teledyne Technologies Company)

- Isra Vision AG (Atlas Copco Group)

- Omron Corporation

- Toshiba Corporation

- Sony Group Corporation

Notable Milestones in Computer Vision Industry Sector

- November 2023: Basler AG and MVTec Software GmbH partnered with Siemens to bring machine vision solutions directly to customers’ machines and systems, enabling seamless integration of machine vision apps into automation technology and reducing complexity.

- October 2023: Keyence Corporation launched its new line of smart camera vision systems, the VS series, featuring sophisticated lens control technology that optimizes the management of 19 lenses in an IP67 camera, allowing adaptability to various imaging needs with a single model.

In-Depth Computer Vision Industry Market Outlook

The computer vision industry is on an upward trajectory, driven by pervasive digital transformation and the relentless pursuit of enhanced automation and intelligence. Future market potential is immense, with advancements in AI vision enabling applications that were once confined to science fiction. Strategic opportunities lie in deeper integration with robotics, the development of predictive maintenance solutions, and the expansion of computer vision in logistics and retail for optimized supply chains and personalized customer experiences. The continued evolution of smart cameras and edge AI will democratize access to powerful visual intelligence, making it an indispensable technology across nearly every sector. The industry is set for sustained, robust growth as businesses worldwide recognize the critical value of visual data in driving efficiency and innovation.

Computer Vision Industry Segmentation

-

1. Component

-

1.1. Hardware

- 1.1.1. Vision Systems

- 1.1.2. Cameras

- 1.1.3. Optics and Illumination Systems

- 1.1.4. Frame Grabbers

- 1.1.5. Other Types of Hardware

- 1.2. Software

-

1.1. Hardware

-

2. Product

- 2.1. PC-based

- 2.2. Smart Camera-based

-

3. End-user Industry

- 3.1. Food and Beverage

- 3.2. Healthcare and Pharmaceutical

- 3.3. Logistics and Retail

- 3.4. Automotive

- 3.5. Electronics and Semiconductors

- 3.6. Other End-user Industries

Computer Vision Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

-

3. Asia

- 3.1. China

- 3.2. Japan

- 3.3. South Korea

- 3.4. India

- 4. Australia and New Zealand

Computer Vision Industry Regional Market Share

Geographic Coverage of Computer Vision Industry

Computer Vision Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.32% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Hardware

- 5.1.1.1. Vision Systems

- 5.1.1.2. Cameras

- 5.1.1.3. Optics and Illumination Systems

- 5.1.1.4. Frame Grabbers

- 5.1.1.5. Other Types of Hardware

- 5.1.2. Software

- 5.1.1. Hardware

- 5.2. Market Analysis, Insights and Forecast - by Product

- 5.2.1. PC-based

- 5.2.2. Smart Camera-based

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Food and Beverage

- 5.3.2. Healthcare and Pharmaceutical

- 5.3.3. Logistics and Retail

- 5.3.4. Automotive

- 5.3.5. Electronics and Semiconductors

- 5.3.6. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia

- 5.4.4. Australia and New Zealand

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Global Computer Vision Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Hardware

- 6.1.1.1. Vision Systems

- 6.1.1.2. Cameras

- 6.1.1.3. Optics and Illumination Systems

- 6.1.1.4. Frame Grabbers

- 6.1.1.5. Other Types of Hardware

- 6.1.2. Software

- 6.1.1. Hardware

- 6.2. Market Analysis, Insights and Forecast - by Product

- 6.2.1. PC-based

- 6.2.2. Smart Camera-based

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Food and Beverage

- 6.3.2. Healthcare and Pharmaceutical

- 6.3.3. Logistics and Retail

- 6.3.4. Automotive

- 6.3.5. Electronics and Semiconductors

- 6.3.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. North America Computer Vision Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Component

- 7.1.1. Hardware

- 7.1.1.1. Vision Systems

- 7.1.1.2. Cameras

- 7.1.1.3. Optics and Illumination Systems

- 7.1.1.4. Frame Grabbers

- 7.1.1.5. Other Types of Hardware

- 7.1.2. Software

- 7.1.1. Hardware

- 7.2. Market Analysis, Insights and Forecast - by Product

- 7.2.1. PC-based

- 7.2.2. Smart Camera-based

- 7.3. Market Analysis, Insights and Forecast - by End-user Industry

- 7.3.1. Food and Beverage

- 7.3.2. Healthcare and Pharmaceutical

- 7.3.3. Logistics and Retail

- 7.3.4. Automotive

- 7.3.5. Electronics and Semiconductors

- 7.3.6. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Component

- 8. Europe Computer Vision Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Component

- 8.1.1. Hardware

- 8.1.1.1. Vision Systems

- 8.1.1.2. Cameras

- 8.1.1.3. Optics and Illumination Systems

- 8.1.1.4. Frame Grabbers

- 8.1.1.5. Other Types of Hardware

- 8.1.2. Software

- 8.1.1. Hardware

- 8.2. Market Analysis, Insights and Forecast - by Product

- 8.2.1. PC-based

- 8.2.2. Smart Camera-based

- 8.3. Market Analysis, Insights and Forecast - by End-user Industry

- 8.3.1. Food and Beverage

- 8.3.2. Healthcare and Pharmaceutical

- 8.3.3. Logistics and Retail

- 8.3.4. Automotive

- 8.3.5. Electronics and Semiconductors

- 8.3.6. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Component

- 9. Asia Computer Vision Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Component

- 9.1.1. Hardware

- 9.1.1.1. Vision Systems

- 9.1.1.2. Cameras

- 9.1.1.3. Optics and Illumination Systems

- 9.1.1.4. Frame Grabbers

- 9.1.1.5. Other Types of Hardware

- 9.1.2. Software

- 9.1.1. Hardware

- 9.2. Market Analysis, Insights and Forecast - by Product

- 9.2.1. PC-based

- 9.2.2. Smart Camera-based

- 9.3. Market Analysis, Insights and Forecast - by End-user Industry

- 9.3.1. Food and Beverage

- 9.3.2. Healthcare and Pharmaceutical

- 9.3.3. Logistics and Retail

- 9.3.4. Automotive

- 9.3.5. Electronics and Semiconductors

- 9.3.6. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Component

- 10. Australia and New Zealand Computer Vision Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Component

- 10.1.1. Hardware

- 10.1.1.1. Vision Systems

- 10.1.1.2. Cameras

- 10.1.1.3. Optics and Illumination Systems

- 10.1.1.4. Frame Grabbers

- 10.1.1.5. Other Types of Hardware

- 10.1.2. Software

- 10.1.1. Hardware

- 10.2. Market Analysis, Insights and Forecast - by Product

- 10.2.1. PC-based

- 10.2.2. Smart Camera-based

- 10.3. Market Analysis, Insights and Forecast - by End-user Industry

- 10.3.1. Food and Beverage

- 10.3.2. Healthcare and Pharmaceutical

- 10.3.3. Logistics and Retail

- 10.3.4. Automotive

- 10.3.5. Electronics and Semiconductors

- 10.3.6. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Component

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Keyence Corporation

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 IDS Imaging Development Systems GmbH (Paul Hartmann AG)

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 MVTec Software GmbH

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 National Instruments Corporation (Emerson)

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Cognex Corporation

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Teledyne DALSA (Teledyne Technologies Company)

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Isra Vision AG (Atlas Copco Group)

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Omron Corporation

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Toshiba Corporation

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Sony Group Corporation

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 Keyence Corporation

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Computer Vision Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Computer Vision Industry Revenue (Million), by Component 2025 & 2033

- Figure 3: North America Computer Vision Industry Revenue Share (%), by Component 2025 & 2033

- Figure 4: North America Computer Vision Industry Revenue (Million), by Product 2025 & 2033

- Figure 5: North America Computer Vision Industry Revenue Share (%), by Product 2025 & 2033

- Figure 6: North America Computer Vision Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 7: North America Computer Vision Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 8: North America Computer Vision Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Computer Vision Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Computer Vision Industry Revenue (Million), by Component 2025 & 2033

- Figure 11: Europe Computer Vision Industry Revenue Share (%), by Component 2025 & 2033

- Figure 12: Europe Computer Vision Industry Revenue (Million), by Product 2025 & 2033

- Figure 13: Europe Computer Vision Industry Revenue Share (%), by Product 2025 & 2033

- Figure 14: Europe Computer Vision Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 15: Europe Computer Vision Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 16: Europe Computer Vision Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Computer Vision Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Computer Vision Industry Revenue (Million), by Component 2025 & 2033

- Figure 19: Asia Computer Vision Industry Revenue Share (%), by Component 2025 & 2033

- Figure 20: Asia Computer Vision Industry Revenue (Million), by Product 2025 & 2033

- Figure 21: Asia Computer Vision Industry Revenue Share (%), by Product 2025 & 2033

- Figure 22: Asia Computer Vision Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 23: Asia Computer Vision Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Asia Computer Vision Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Computer Vision Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Australia and New Zealand Computer Vision Industry Revenue (Million), by Component 2025 & 2033

- Figure 27: Australia and New Zealand Computer Vision Industry Revenue Share (%), by Component 2025 & 2033

- Figure 28: Australia and New Zealand Computer Vision Industry Revenue (Million), by Product 2025 & 2033

- Figure 29: Australia and New Zealand Computer Vision Industry Revenue Share (%), by Product 2025 & 2033

- Figure 30: Australia and New Zealand Computer Vision Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 31: Australia and New Zealand Computer Vision Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 32: Australia and New Zealand Computer Vision Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Australia and New Zealand Computer Vision Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Computer Vision Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 2: Global Computer Vision Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 3: Global Computer Vision Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 4: Global Computer Vision Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Computer Vision Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 6: Global Computer Vision Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 7: Global Computer Vision Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 8: Global Computer Vision Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States Computer Vision Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada Computer Vision Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Global Computer Vision Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 12: Global Computer Vision Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 13: Global Computer Vision Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 14: Global Computer Vision Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 15: Germany Computer Vision Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: United Kingdom Computer Vision Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: France Computer Vision Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Italy Computer Vision Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Spain Computer Vision Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Global Computer Vision Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 21: Global Computer Vision Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 22: Global Computer Vision Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 23: Global Computer Vision Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: China Computer Vision Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Japan Computer Vision Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: South Korea Computer Vision Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: India Computer Vision Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Global Computer Vision Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 29: Global Computer Vision Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 30: Global Computer Vision Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 31: Global Computer Vision Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Computer Vision Industry?

The projected CAGR is approximately 8.32%.

2. Which companies are prominent players in the Computer Vision Industry?

Key companies in the market include Keyence Corporation, IDS Imaging Development Systems GmbH (Paul Hartmann AG), MVTec Software GmbH, National Instruments Corporation (Emerson), Cognex Corporation, Teledyne DALSA (Teledyne Technologies Company), Isra Vision AG (Atlas Copco Group), Omron Corporation, Toshiba Corporation, Sony Group Corporation.

3. What are the main segments of the Computer Vision Industry?

The market segments include Component, Product, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.88 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Need for Quality Inspections; Increasing Demand for Vision-guided Robotic Systems.

6. What are the notable trends driving market growth?

Cameras to be the Largest Hardware Segment.

7. Are there any restraints impacting market growth?

Scarcity of Flexible Machine Vision Solutions.

8. Can you provide examples of recent developments in the market?

November 2023: Basler AG and MVTec Software GmbH partnered with Siemens to bring machine vision solutions directly to customers’ machines and systems. The new partnerships between Basler AG and Siemens enable customers to integrate machine vision apps directly into their automation technology. Siemens’ experience with industrial automation and digitization, combined with MVTec’s expertise in machine vision, reduces the complexity for customers. It significantly reduces the barrier to entry for machine vision solutions.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Computer Vision Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Computer Vision Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Computer Vision Industry?

To stay informed about further developments, trends, and reports in the Computer Vision Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence