Key Insights

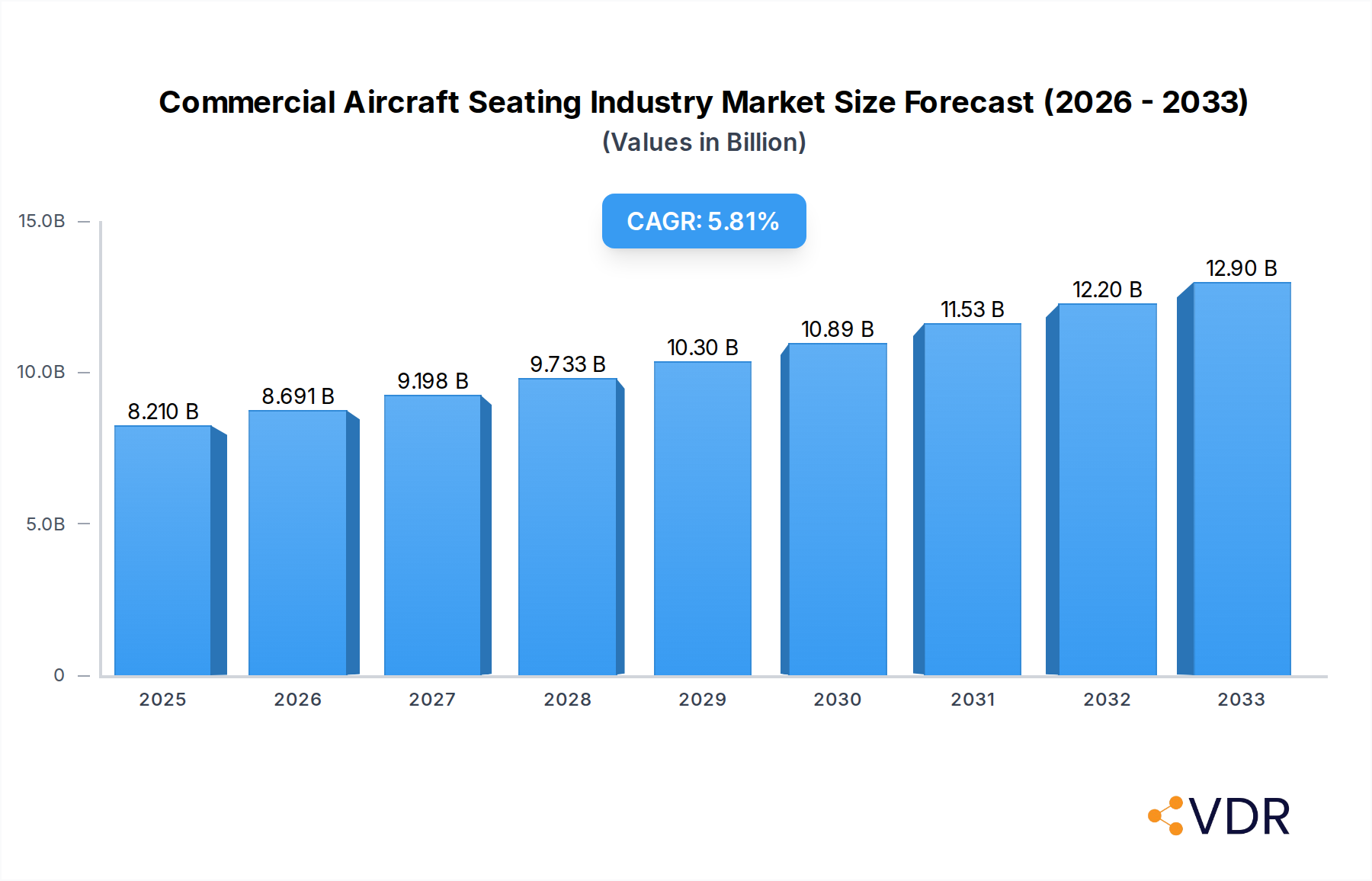

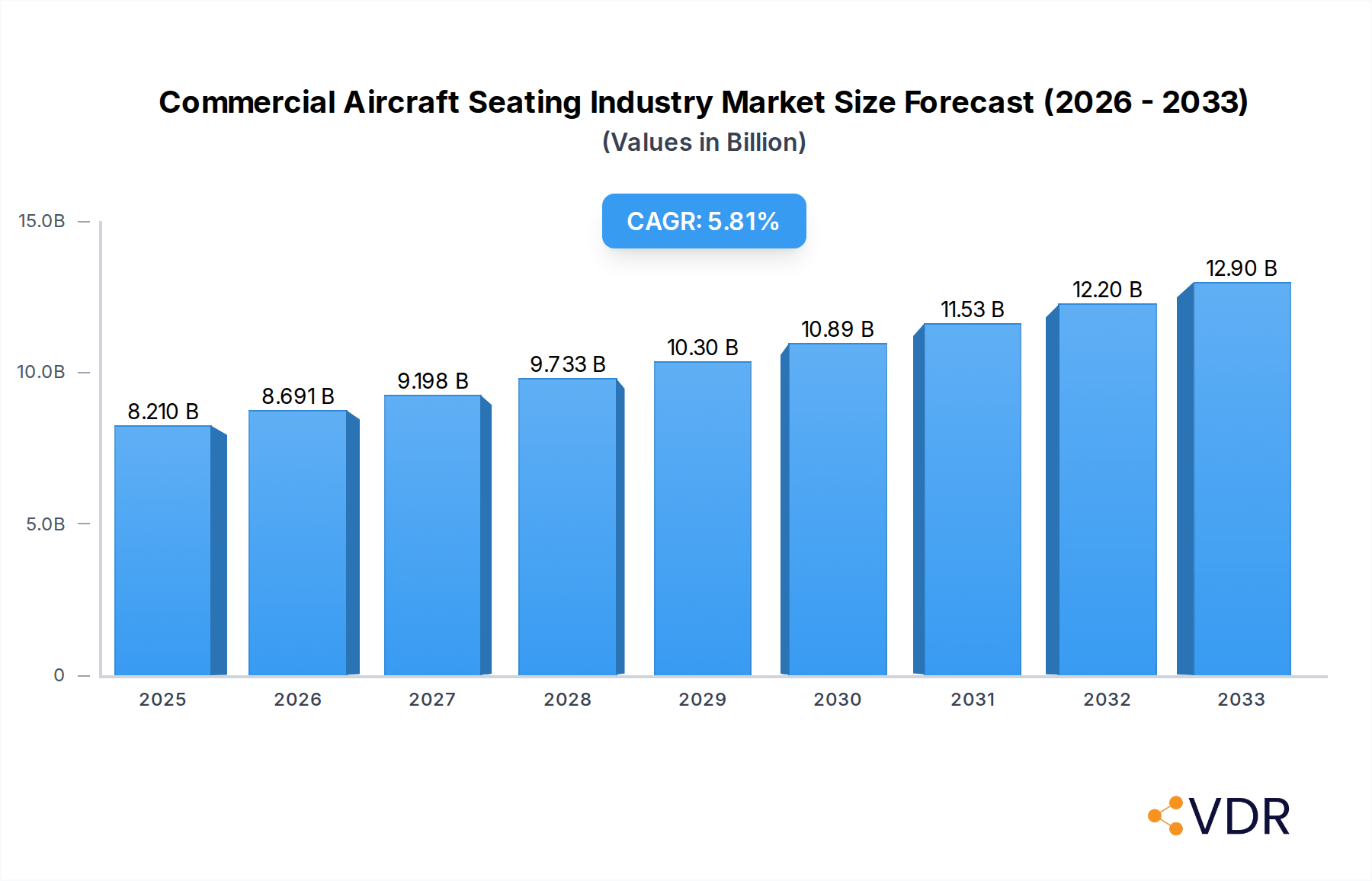

The Commercial Aircraft Seating Industry is poised for significant expansion, with a projected market size of USD 8.21 billion in 2025. This growth is driven by a confluence of factors including the sustained demand for air travel, the ongoing fleet modernization initiatives by airlines, and the increasing passenger focus on comfort and in-flight experience. As airlines strive to differentiate themselves, investments in advanced, lightweight, and ergonomically superior seating solutions are becoming paramount. The industry is also witnessing a strong emphasis on sustainability, with manufacturers developing seats using recycled materials and prioritizing fuel efficiency through weight reduction. This creates a dynamic market where innovation in material science, design, and integrated technology will be crucial for success. The projected CAGR of 5.94% underscores the industry's robust recovery and its continued importance in the aviation ecosystem.

Commercial Aircraft Seating Industry Market Size (In Billion)

The competitive landscape is characterized by the presence of established players and emerging innovators, all vying to capture market share through product differentiation and strategic partnerships. Key growth drivers include the expanding global aviation infrastructure, particularly in emerging economies, and the anticipated surge in air passenger traffic post-pandemic. While the industry benefits from these positive trends, it also faces certain restraints. These include the high cost of research and development for cutting-edge seating technologies, the stringent regulatory environment for aviation safety and certification, and potential supply chain disruptions. Nevertheless, the industry's resilience and adaptability, coupled with the persistent demand for air travel, suggest a promising outlook for commercial aircraft seating manufacturers. The forecast period of 2025-2033 indicates a sustained upward trajectory, with ample opportunities for companies that can deliver on innovation, cost-effectiveness, and passenger satisfaction.

Commercial Aircraft Seating Industry Company Market Share

Commercial Aircraft Seating Industry: Market Dynamics, Growth Trends, and Future Outlook (2019-2033)

This comprehensive report delves into the dynamic commercial aircraft seating market, offering an in-depth analysis of its structure, growth trajectories, key players, and future potential. Covering the period from 2019 to 2033, with a base and estimated year of 2025, this study provides invaluable insights for stakeholders seeking to navigate the evolving landscape of aircraft interiors. Explore parent and child market dynamics, understand crucial industry developments, and identify lucrative opportunities within this vital aerospace sector.

Commercial Aircraft Seating Industry Market Dynamics & Structure

The global commercial aircraft seating market is characterized by a moderate level of concentration, with a few dominant players controlling a significant portion of the market share. Technological innovation acts as a primary driver, with manufacturers continuously investing in lighter materials, enhanced ergonomics, and integrated in-flight entertainment systems to meet evolving airline demands and passenger expectations for comfort and connectivity. Regulatory frameworks, primarily driven by safety standards and cabin configuration mandates from aviation authorities like the FAA and EASA, also shape product development and market entry. Competitive product substitutes, while limited within the core seating segment, can emerge from advancements in cabin modularity and flexible interior designs. End-user demographics, particularly the growth of premium economy and business class offerings driven by a rising global middle class and a desire for enhanced travel experiences, significantly influence product demand. Mergers and acquisitions (M&A) have been a strategic tool for consolidation and market expansion, allowing companies to broaden their product portfolios and geographical reach. For instance, the integration of STELIA Aerospace into Airbus Atlantic signifies a major consolidation within the child market of aerostructures and cabin components.

- Market Concentration: Dominated by key players like Collins Aerospace, Safran, and Recaro Group.

- Technological Innovation Drivers: Focus on weight reduction (e.g., carbon fiber composites), improved passenger comfort, and integration of smart cabin technologies.

- Regulatory Frameworks: Stringent safety certifications (e.g., EASA Part 21, FAA FARs) and cabin density regulations impact design and manufacturing.

- Competitive Product Substitutes: Evolution of cabin interior modularity and in-flight entertainment systems can indirectly impact seating demand.

- End-User Demographics: Growing demand for premium economy and first-class seating driven by increased disposable income and evolving travel preferences.

- M&A Trends: Strategic acquisitions to gain market share, expand product lines, and enhance technological capabilities. For example, the Adient Aerospace acquisition by Collins Aerospace aimed to bolster their offerings in the parent market of aircraft interiors.

Commercial Aircraft Seating Industry Growth Trends & Insights

The commercial aircraft seating industry is projected to experience robust growth throughout the forecast period, driven by a confluence of factors including the gradual recovery and expansion of global air travel, a sustained demand for fleet modernization, and the increasing introduction of new aircraft models. The market size is anticipated to expand significantly, moving from an estimated XX billion units in 2025 to reach a projected XX billion units by 2033, reflecting a Compound Annual Growth Rate (CAGR) of approximately XX%. Adoption rates for advanced seating solutions, such as those offering enhanced comfort, improved fuel efficiency through weight reduction, and integrated digital features, are on an upward trajectory. Technological disruptions, including advancements in 3D printing for customizable components and the development of bio-based or recycled materials for sustainable seating, are poised to reshape the industry. Consumer behavior shifts are also playing a pivotal role; passengers are increasingly valuing comfort and personalized experiences, leading to a greater demand for premium cabin classes and innovative seating configurations that maximize space and functionality. This evolving passenger expectation fuels the development of next-generation seating solutions. The increasing focus on sustainability in aviation is also driving demand for lighter and more eco-friendly seating materials and designs. Furthermore, the introduction of new aircraft variants and the ongoing need for cabin retrofits to meet these evolving passenger demands will continue to stimulate market growth. The child market of premium economy seating, in particular, is witnessing accelerated adoption rates as airlines seek to differentiate their offerings and cater to a growing segment of travelers willing to pay for enhanced comfort. The parent market of overall aircraft interiors is thus seeing a significant uplift from these specialized seating innovations.

Dominant Regions, Countries, or Segments in Commercial Aircraft Seating Industry

The Narrowbody aircraft segment is currently the dominant force driving growth within the commercial aircraft seating industry. This segment, encompassing popular aircraft families like the Airbus A320neo and Boeing 737 MAX, constitutes the largest portion of global airline fleets due to their versatility for short-to-medium haul routes, making them the workhorses of commercial aviation. The sheer volume of narrowbody aircraft manufactured and operated worldwide directly translates into a higher demand for seating solutions. Countries with a strong manufacturing base in aerospace and significant airline operations, such as the United States, Europe (particularly Germany, France, and the UK), and Asia-Pacific (led by China and Singapore), are pivotal in this segment's growth. The economic policies in these regions, which often support domestic aerospace manufacturing and airline expansion, further bolster demand. Infrastructure development, including the expansion of airports and air traffic control capabilities, also indirectly fuels the need for new aircraft and, consequently, new seating. The market share held by narrowbody seating solutions is substantial, estimated to be around XX% of the total aircraft seating market. Growth potential in this segment remains exceptionally high, fueled by ongoing fleet expansions and the continuous retirement of older narrowbody aircraft, necessitating replacement seating.

- Dominant Segment: Narrowbody Aircraft.

- Key Drivers: High volume of narrowbody aircraft production and operation, demand for fleet modernization, and efficiency in short-to-medium haul travel.

- Leading Countries/Regions: United States, Europe (Germany, France, UK), Asia-Pacific (China, Singapore).

- Market Share: Narrowbody seating accounts for an estimated XX% of the global aircraft seating market.

- Growth Potential: Strong, driven by new aircraft orders, fleet replacements, and airline growth in emerging markets.

- Impact of Economic Policies: Government support for aerospace manufacturing and airline subsidies in key regions stimulate demand.

- Infrastructure Influence: Airport expansion and air traffic management improvements facilitate increased flight operations, requiring more aircraft and seating.

The Widebody aircraft segment, while smaller in volume compared to narrowbodies, represents a significant and growing market for premium and innovative seating solutions. Airlines are increasingly investing in upgrading their widebody fleets to enhance passenger experience on long-haul routes, driving demand for sophisticated business class and first-class suites, as well as comfortable premium economy options. This trend is particularly pronounced in regions with burgeoning long-haul travel markets. The market share for widebody seating, while currently at around XX%, is expected to witness a steady increase. The child market of premium cabin seating within the widebody segment is a key area of focus for manufacturers.

- Significant Segment: Widebody Aircraft.

- Key Drivers: Demand for enhanced passenger experience on long-haul flights, growth in premium cabin classes, and fleet modernization for long-haul carriers.

- Market Share: Approximately XX%, with strong growth potential in premium segments.

- Growth Potential: High, driven by increasing demand for comfort and luxury in long-haul travel.

Commercial Aircraft Seating Industry Product Landscape

The commercial aircraft seating industry is witnessing a rapid evolution in its product landscape, driven by a relentless pursuit of enhanced passenger comfort, weight reduction, and integrated technology. Innovations are focused on lighter, stronger materials such as advanced composites, leading to improved fuel efficiency and reduced environmental impact. Ergonomic designs are becoming more sophisticated, offering greater adjustability and support to cater to diverse passenger needs. Unique selling propositions revolve around personalized comfort features, such as customizable lumbar support, advanced recline mechanisms, and integrated personal electronic device holders. Technological advancements include the seamless integration of in-flight entertainment (IFE) systems, USB charging ports, and even Wi-Fi connectivity directly into the seat architecture. The child market of specialized seating, like premium economy and business class suites, is at the forefront of these product innovations.

Key Drivers, Barriers & Challenges in Commercial Aircraft Seating Industry

The commercial aircraft seating industry is propelled by several key drivers, including the continuous demand for fleet modernization driven by airlines seeking fuel efficiency and passenger comfort, and the growing preference for premium travel experiences, particularly in the child market of premium economy and business class seating. Technological advancements in lightweight materials and smart cabin integration also act as significant growth catalysts. The increasing global demand for air travel, especially in emerging economies, further fuels market expansion.

Conversely, the industry faces substantial barriers and challenges. Supply chain disruptions, as evidenced by recent global events, can significantly impact production timelines and costs. Stringent and evolving regulatory frameworks require continuous investment in R&D and certification processes. High capital expenditure for manufacturing facilities and the long lead times for product development and approval also present considerable hurdles. Intense competition among established players and the threat of new entrants with disruptive technologies contribute to market pressures. The need to balance cost-effectiveness with advanced features for airlines remains a persistent challenge.

Emerging Opportunities in Commercial Aircraft Seating Industry

Emerging opportunities in the commercial aircraft seating industry lie in the development of sustainable and eco-friendly seating solutions, utilizing recycled materials and advanced manufacturing techniques like 3D printing for reduced waste and optimized designs. The growing demand for personalized cabin experiences presents a significant opportunity for manufacturers to offer highly customizable seating configurations catering to specific airline needs and passenger preferences, particularly within the child market of premium cabins. Furthermore, the integration of advanced connectivity and smart cabin technologies, beyond basic IFE, into seating, such as biometric passenger recognition and predictive maintenance sensors, offers a fertile ground for innovation and value creation. Untapped markets in regions with rapidly expanding air travel infrastructure also present significant growth potential.

Growth Accelerators in the Commercial Aircraft Seating Industry Industry

Several catalysts are accelerating the growth of the commercial aircraft seating industry. Technological breakthroughs in material science, leading to lighter, stronger, and more sustainable seating components, are a primary accelerator. Strategic partnerships between seating manufacturers, airlines, and technology providers are fostering innovation and co-creation of next-generation cabin interiors, especially within the child market of specialized seating. Market expansion strategies, such as entering emerging economies with growing air travel demand and focusing on retrofit programs for existing fleets, are also significant growth engines. The continuous drive for differentiation by airlines, leading to investments in superior passenger comfort and amenities, further fuels demand for advanced seating solutions.

Key Players Shaping the Commercial Aircraft Seating Industry Market

- Expliseat

- Safran

- Recaro Group

- STELIA Aerospace (Airbus Atlantic Merginac)

- Thompson Aero Seating

- Jamco Corporation

- Adient Aerospace

- Collins Aerospace

- ZIM Aircraft Seating Gmb

- B/E Aerospace (now Collins Aerospace)

Notable Milestones in Commercial Aircraft Seating Industry Sector

- July 2022: ZIM Aircraft Seating agreed to supply premium economy seats for Air New Zealand's Boeing 787-9 Dreamliner fleet.

- June 2022: STELIA Aerospace and AERQ collaborated on Cabin Digital Signage integration of OPERA seats for the A320neo family.

- June 2022: Recaro Aircraft Seating was selected by KLM Royal Dutch Airlines (KLM), Transavia France, and Netherlands-based Transavia Airlines to outfit new Airbus aircraft with economy class seats.

In-Depth Commercial Aircraft Seating Industry Market Outlook

The commercial aircraft seating industry is poised for a period of sustained expansion, driven by the enduring demand for air travel and the imperative for airlines to enhance passenger experience. Future market potential is significant, with ongoing fleet renewal programs and the introduction of new aircraft models creating continuous opportunities. Strategic opportunities abound in the development of advanced, lightweight, and sustainable seating solutions, alongside the integration of cutting-edge digital and connectivity features. The child market of premium and specialized seating, in particular, is expected to witness substantial growth as airlines differentiate their offerings. Collaboration between key industry players and a focus on innovation will be crucial for navigating the evolving market landscape and capitalizing on future growth prospects.

Commercial Aircraft Seating Industry Segmentation

-

1. Aircraft Type

- 1.1. Narrowbody

- 1.2. Widebody

Commercial Aircraft Seating Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

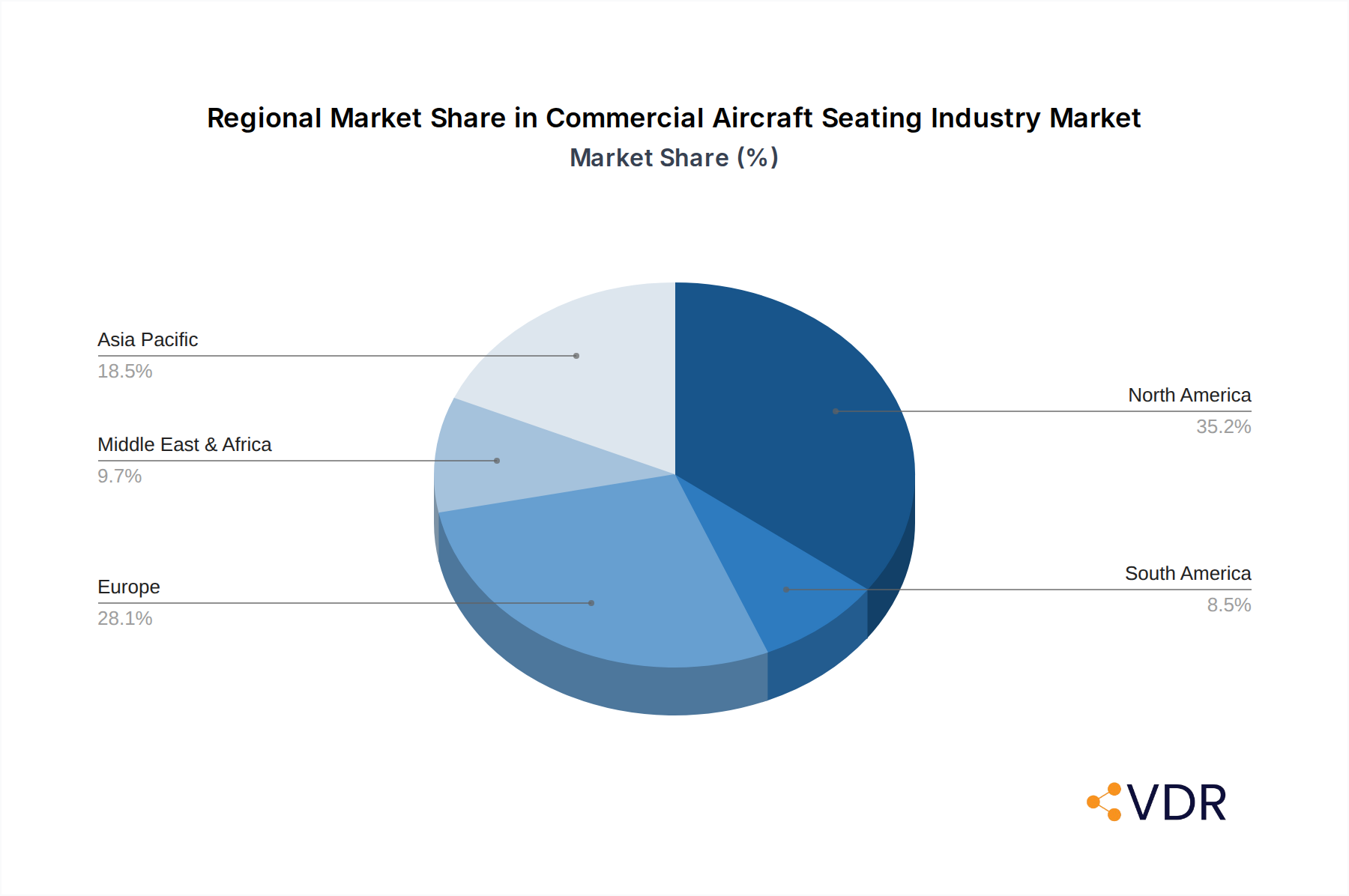

Commercial Aircraft Seating Industry Regional Market Share

Geographic Coverage of Commercial Aircraft Seating Industry

Commercial Aircraft Seating Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.94% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Commercial Aircraft Seating Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 5.1.1. Narrowbody

- 5.1.2. Widebody

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. South America

- 5.2.3. Europe

- 5.2.4. Middle East & Africa

- 5.2.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 6. North America Commercial Aircraft Seating Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 6.1.1. Narrowbody

- 6.1.2. Widebody

- 6.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 7. South America Commercial Aircraft Seating Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 7.1.1. Narrowbody

- 7.1.2. Widebody

- 7.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 8. Europe Commercial Aircraft Seating Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 8.1.1. Narrowbody

- 8.1.2. Widebody

- 8.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 9. Middle East & Africa Commercial Aircraft Seating Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 9.1.1. Narrowbody

- 9.1.2. Widebody

- 9.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 10. Asia Pacific Commercial Aircraft Seating Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 10.1.1. Narrowbody

- 10.1.2. Widebody

- 10.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Expliseat

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Safran

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Recaro Group

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 STELIA Aerospace (Airbus Atlantic Merginac)

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Thompson Aero Seating

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Jamco Corporation

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Adient Aerospace

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Collins Aerospace

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 ZIM Aircraft Seating Gmb

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 Expliseat

List of Figures

- Figure 1: Global Commercial Aircraft Seating Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Commercial Aircraft Seating Industry Revenue (billion), by Aircraft Type 2025 & 2033

- Figure 3: North America Commercial Aircraft Seating Industry Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 4: North America Commercial Aircraft Seating Industry Revenue (billion), by Country 2025 & 2033

- Figure 5: North America Commercial Aircraft Seating Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: South America Commercial Aircraft Seating Industry Revenue (billion), by Aircraft Type 2025 & 2033

- Figure 7: South America Commercial Aircraft Seating Industry Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 8: South America Commercial Aircraft Seating Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: South America Commercial Aircraft Seating Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Commercial Aircraft Seating Industry Revenue (billion), by Aircraft Type 2025 & 2033

- Figure 11: Europe Commercial Aircraft Seating Industry Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 12: Europe Commercial Aircraft Seating Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Commercial Aircraft Seating Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Middle East & Africa Commercial Aircraft Seating Industry Revenue (billion), by Aircraft Type 2025 & 2033

- Figure 15: Middle East & Africa Commercial Aircraft Seating Industry Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 16: Middle East & Africa Commercial Aircraft Seating Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Middle East & Africa Commercial Aircraft Seating Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Commercial Aircraft Seating Industry Revenue (billion), by Aircraft Type 2025 & 2033

- Figure 19: Asia Pacific Commercial Aircraft Seating Industry Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 20: Asia Pacific Commercial Aircraft Seating Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Asia Pacific Commercial Aircraft Seating Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Commercial Aircraft Seating Industry Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 2: Global Commercial Aircraft Seating Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global Commercial Aircraft Seating Industry Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 4: Global Commercial Aircraft Seating Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: United States Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Canada Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: Mexico Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Global Commercial Aircraft Seating Industry Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 9: Global Commercial Aircraft Seating Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Brazil Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Argentina Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Rest of South America Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Global Commercial Aircraft Seating Industry Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 14: Global Commercial Aircraft Seating Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United Kingdom Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Germany Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: France Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Italy Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Spain Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Russia Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Benelux Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Nordics Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Rest of Europe Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Global Commercial Aircraft Seating Industry Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 25: Global Commercial Aircraft Seating Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 26: Turkey Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Israel Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: GCC Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: North Africa Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: South Africa Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of Middle East & Africa Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global Commercial Aircraft Seating Industry Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 33: Global Commercial Aircraft Seating Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 34: China Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: India Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Japan Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: South Korea Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: ASEAN Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Oceania Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Rest of Asia Pacific Commercial Aircraft Seating Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Commercial Aircraft Seating Industry?

The projected CAGR is approximately 5.94%.

2. Which companies are prominent players in the Commercial Aircraft Seating Industry?

Key companies in the market include Expliseat, Safran, Recaro Group, STELIA Aerospace (Airbus Atlantic Merginac), Thompson Aero Seating, Jamco Corporation, Adient Aerospace, Collins Aerospace, ZIM Aircraft Seating Gmb.

3. What are the main segments of the Commercial Aircraft Seating Industry?

The market segments include Aircraft Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.21 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

July 2022: ZIM Aircraft Seating agreed to supply premium economy seats for Air New Zealand's Boeing 787-9 Dreamliner fleet.June 2022: STELIA Aerospace and AERQ to collaborate on Cabin Digital Signage integration of OPERA seats for the A320neo family.June 2022: Recaro Aircraft Seating was selected by KLM Royal Dutch Airlines (KLM), Transavia France, and Netherlands-based Transavia Airlines to outfit new Airbus aircraft with economy class seats.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Commercial Aircraft Seating Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Commercial Aircraft Seating Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Commercial Aircraft Seating Industry?

To stay informed about further developments, trends, and reports in the Commercial Aircraft Seating Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence