Key Insights

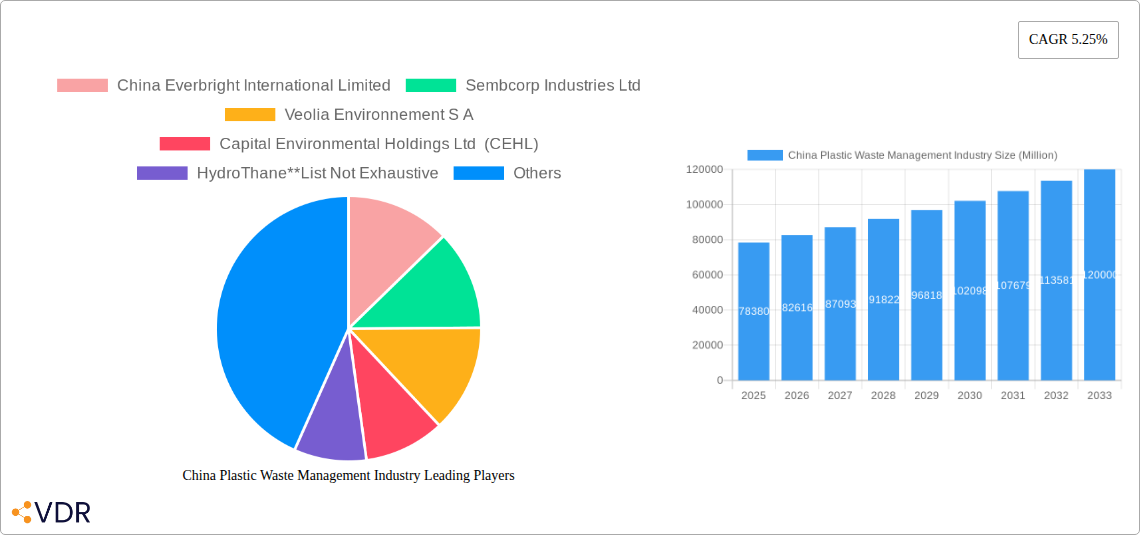

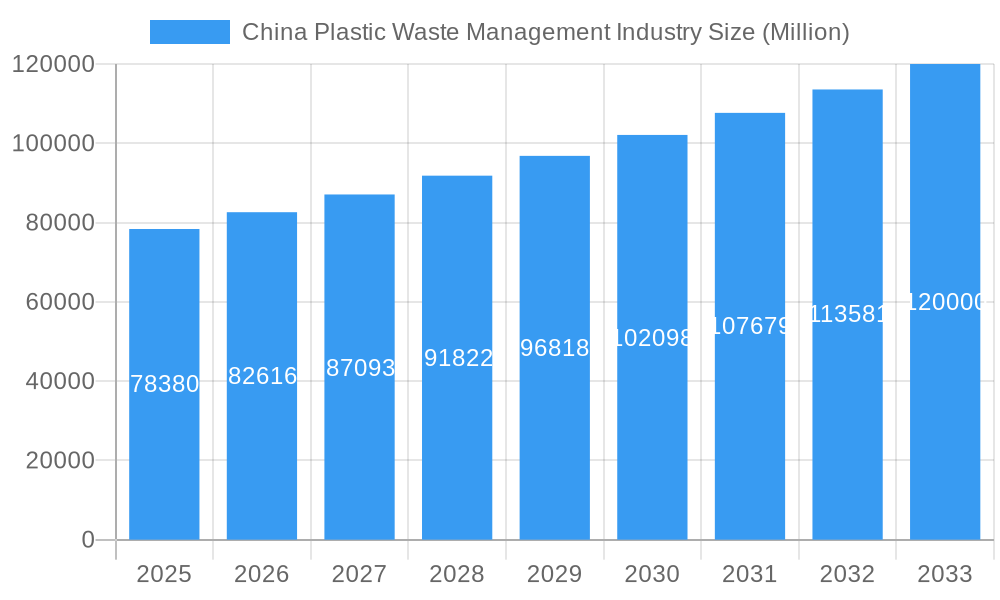

The China plastic waste management industry, valued at $78.38 billion in 2025, is projected to experience robust growth, driven by increasing environmental awareness, stringent government regulations aimed at reducing plastic pollution, and rising demand for recycled plastics. A Compound Annual Growth Rate (CAGR) of 5.25% from 2025 to 2033 indicates a significant expansion of the market, reaching an estimated value exceeding $120 billion by 2033. Key drivers include the implementation of the National Sword policy and subsequent focus on domestic waste management solutions, growing investments in advanced recycling technologies like chemical recycling and pyrolysis, and increasing adoption of Extended Producer Responsibility (EPR) schemes that incentivize plastic waste reduction and recycling. The industry is segmented by waste type (PET, HDPE, PVC, etc.), recycling methods (mechanical, chemical), and geographic location. Major players like China Everbright International Limited, Sembcorp Industries Ltd, and Veolia Environnement S.A. are actively investing in capacity expansion and technological advancements to capitalize on this growing market. However, challenges remain, including inconsistent waste collection and sorting infrastructure, a lack of standardized recycling processes across regions, and the need for further technological development to improve the efficiency and cost-effectiveness of recycling specific plastic types.

China Plastic Waste Management Industry Market Size (In Billion)

The growth trajectory of the China plastic waste management market is closely tied to China's overall economic development and its commitment to environmental sustainability. Further advancements in technology, coupled with supportive government policies, will likely accelerate market expansion. The increasing awareness among consumers about the environmental consequences of plastic waste is also expected to fuel demand for sustainable waste management solutions. While challenges exist, the long-term outlook for the industry remains positive, presenting significant opportunities for both domestic and international companies involved in waste collection, sorting, processing, and recycling technologies. The market is expected to see considerable consolidation as larger players acquire smaller companies to enhance their market share and technological capabilities.

China Plastic Waste Management Industry Company Market Share

China Plastic Waste Management Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the China plastic waste management industry, covering market dynamics, growth trends, key players, and future outlook. The study period spans 2019-2033, with 2025 serving as the base and estimated year. The forecast period is 2025-2033, and the historical period encompasses 2019-2024. This report is invaluable for industry professionals, investors, and policymakers seeking a clear understanding of this rapidly evolving sector. The parent market is Waste Management, and the child market is Plastic Waste Management. The total market size in 2025 is estimated at xx Million units.

China Plastic Waste Management Industry Market Dynamics & Structure

The China plastic waste management market exhibits a moderately concentrated structure, with several large players holding significant market share. Technological innovation, particularly in advanced recycling technologies like chemical recycling and pyrolysis, is a key driver. Stringent government regulations aimed at reducing plastic pollution and promoting circular economy principles are significantly shaping the market landscape. The emergence of biodegradable plastics and other competitive substitutes poses a challenge to traditional waste management approaches. End-user demographics, primarily driven by increasing urbanization and rising environmental awareness, are influencing demand. M&A activity in the sector has been moderate (xx deals in the last 5 years), with larger players consolidating their market positions.

- Market Concentration: Moderately concentrated, with top 5 players holding approximately xx% market share in 2025.

- Technological Innovation: Significant advancements in chemical recycling and AI-powered waste sorting driving efficiency gains.

- Regulatory Framework: Stringent regulations on plastic waste disposal and increasing emphasis on Extended Producer Responsibility (EPR) schemes.

- Competitive Substitutes: Biodegradable plastics and other sustainable packaging alternatives presenting competitive pressures.

- End-User Demographics: Growing urbanization and rising environmental awareness boosting demand for effective waste management solutions.

- M&A Trends: Moderate level of M&A activity, primarily focused on consolidation among larger companies.

China Plastic Waste Management Industry Growth Trends & Insights

The China plastic waste management market has witnessed robust growth over the past few years, driven by a combination of factors. The market size is projected to expand at a CAGR of xx% during the forecast period (2025-2033), reaching xx Million units by 2033. Increased adoption of advanced recycling technologies, coupled with government initiatives promoting circular economy principles, has fueled this growth. Shifting consumer behavior, particularly a rising preference for sustainable products, has also played a significant role. Technological disruptions, such as the development of AI-powered waste sorting systems, are further enhancing efficiency and reducing costs. Market penetration of advanced recycling technologies is expected to increase from xx% in 2025 to xx% by 2033.

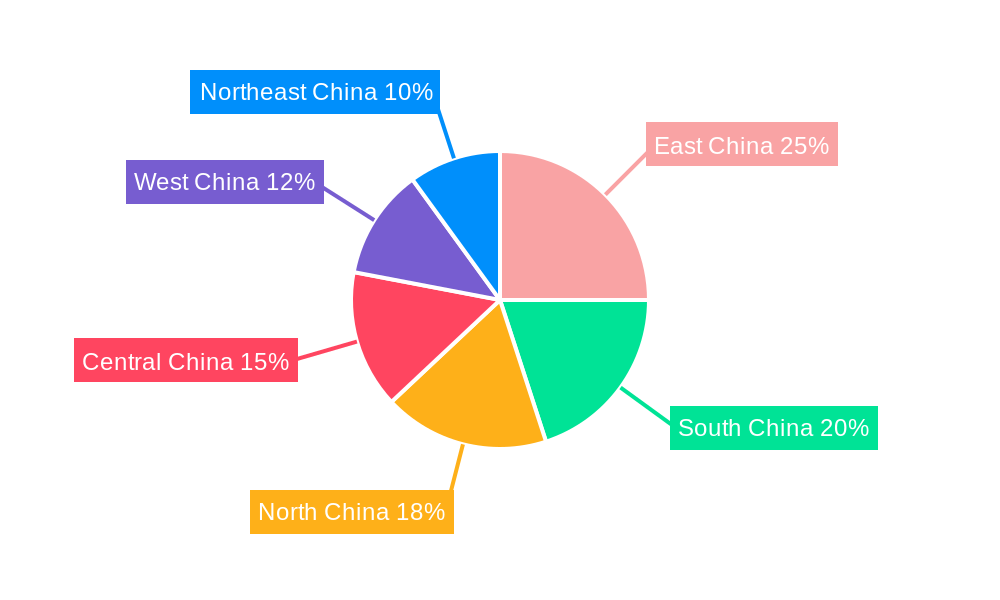

Dominant Regions, Countries, or Segments in China Plastic Waste Management Industry

Coastal provinces like Guangdong, Jiangsu, and Zhejiang are currently the dominant regions in the China plastic waste management market, due to higher population density, industrial activity, and established infrastructure. These regions have witnessed significant investments in waste management infrastructure and the adoption of advanced technologies. Government policies promoting waste segregation and recycling at the municipal level have further strengthened their position. The growth potential in less-developed regions, particularly in the western part of China, remains significant, however infrastructure development and capacity building are necessary.

- Key Drivers in Coastal Provinces: Higher population density, robust industrial activity, and established infrastructure.

- Government Support: Strong policy initiatives promoting waste segregation and recycling.

- Technological Adoption: Higher adoption rates of advanced waste management technologies.

- Growth Potential in Western Regions: Significant untapped potential, but requires infrastructure development and capacity building.

China Plastic Waste Management Industry Product Landscape

The product landscape is diversifying, with an increasing focus on advanced recycling technologies, such as chemical recycling and pyrolysis, which offer higher recovery rates and value-added products compared to traditional mechanical recycling. These technologies are gaining traction due to their ability to process a wider range of plastic waste streams. Innovations in waste sorting technologies, driven by advancements in AI and robotics, are significantly improving efficiency and reducing operational costs. The market also includes a range of services, from waste collection and transportation to processing and disposal.

Key Drivers, Barriers & Challenges in China Plastic Waste Management Industry

Key Drivers: Stringent government regulations, increasing environmental awareness, advancements in recycling technologies, and the growing need for sustainable waste management solutions.

Key Challenges: Inadequate infrastructure in certain regions, inconsistent waste segregation practices, high operating costs associated with advanced recycling technologies, and competition from informal waste management sectors. The lack of a comprehensive nationwide recycling system leads to inefficiencies and difficulties in tracking materials. This translates to a xx Million unit annual loss due to inadequate recycling practices.

Emerging Opportunities in China Plastic Waste Management Industry

Emerging opportunities include the growing demand for recycled plastic feedstock, expanding applications of recycled plastics in various industries, and the potential for developing innovative business models based on waste-to-energy technologies. The development of closed-loop recycling systems, which minimize material loss and maximize resource utilization, presents significant growth opportunities. The untapped potential of rural areas offers another promising avenue for expansion.

Growth Accelerators in the China Plastic Waste Management Industry Industry

Technological advancements, including the development of highly efficient recycling technologies and AI-powered waste sorting systems, will play a crucial role in accelerating market growth. Strategic partnerships between technology providers, waste management companies, and government agencies will facilitate the deployment of innovative solutions. Market expansion into underserved regions, coupled with capacity building initiatives, will also contribute to market growth.

Key Players Shaping the China Plastic Waste Management Industry Market

- China Everbright International Limited

- Sembcorp Industries Ltd

- Veolia Environnement S A

- Capital Environmental Holdings Ltd (CEHL)

- HydroThane

Notable Milestones in China Plastic Waste Management Industry Sector

- 2020: Introduction of stricter regulations on plastic waste disposal.

- 2021: Launch of several large-scale waste-to-energy projects.

- 2022: Significant investments in advanced recycling technologies.

- 2023: Several major M&A deals involving leading waste management companies.

In-Depth China Plastic Waste Management Industry Market Outlook

The future of the China plastic waste management industry is bright, driven by continued technological advancements, supportive government policies, and increasing environmental awareness. The market is poised for significant growth, offering substantial opportunities for companies involved in waste collection, processing, recycling, and disposal. Strategic partnerships, investments in innovative technologies, and expansion into new markets will be critical for success in this dynamic sector. The market is expected to see xx% growth in the coming decade.

China Plastic Waste Management Industry Segmentation

-

1. Waste type

- 1.1. Industrial waste

- 1.2. Municipal solid waste

- 1.3. Hazardous waste

- 1.4. E-waste

- 1.5. Plastic waste

- 1.6. Bio-medical waste

-

2. Disposal methods

- 2.1. Landfill

- 2.2. Incineration

- 2.3. Dismantling

- 2.4. Recycling

-

3. Type of ownership

- 3.1. Public

- 3.2. Private

- 3.3. Public - Private Patnership

China Plastic Waste Management Industry Segmentation By Geography

- 1. China

China Plastic Waste Management Industry Regional Market Share

Geographic Coverage of China Plastic Waste Management Industry

China Plastic Waste Management Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.25% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Waste type

- 5.1.1. Industrial waste

- 5.1.2. Municipal solid waste

- 5.1.3. Hazardous waste

- 5.1.4. E-waste

- 5.1.5. Plastic waste

- 5.1.6. Bio-medical waste

- 5.2. Market Analysis, Insights and Forecast - by Disposal methods

- 5.2.1. Landfill

- 5.2.2. Incineration

- 5.2.3. Dismantling

- 5.2.4. Recycling

- 5.3. Market Analysis, Insights and Forecast - by Type of ownership

- 5.3.1. Public

- 5.3.2. Private

- 5.3.3. Public - Private Patnership

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.1. Market Analysis, Insights and Forecast - by Waste type

- 6. China Plastic Waste Management Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Waste type

- 6.1.1. Industrial waste

- 6.1.2. Municipal solid waste

- 6.1.3. Hazardous waste

- 6.1.4. E-waste

- 6.1.5. Plastic waste

- 6.1.6. Bio-medical waste

- 6.2. Market Analysis, Insights and Forecast - by Disposal methods

- 6.2.1. Landfill

- 6.2.2. Incineration

- 6.2.3. Dismantling

- 6.2.4. Recycling

- 6.3. Market Analysis, Insights and Forecast - by Type of ownership

- 6.3.1. Public

- 6.3.2. Private

- 6.3.3. Public - Private Patnership

- 6.1. Market Analysis, Insights and Forecast - by Waste type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 China Everbright International Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Sembcorp Industries Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Veolia Environnement S A

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Capital Environmental Holdings Ltd (CEHL)

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 HydroThane**List Not Exhaustive

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.1 China Everbright International Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Plastic Waste Management Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: China Plastic Waste Management Industry Share (%) by Company 2025

List of Tables

- Table 1: China Plastic Waste Management Industry Revenue Million Forecast, by Waste type 2020 & 2033

- Table 2: China Plastic Waste Management Industry Volume Billion Forecast, by Waste type 2020 & 2033

- Table 3: China Plastic Waste Management Industry Revenue Million Forecast, by Disposal methods 2020 & 2033

- Table 4: China Plastic Waste Management Industry Volume Billion Forecast, by Disposal methods 2020 & 2033

- Table 5: China Plastic Waste Management Industry Revenue Million Forecast, by Type of ownership 2020 & 2033

- Table 6: China Plastic Waste Management Industry Volume Billion Forecast, by Type of ownership 2020 & 2033

- Table 7: China Plastic Waste Management Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: China Plastic Waste Management Industry Volume Billion Forecast, by Region 2020 & 2033

- Table 9: China Plastic Waste Management Industry Revenue Million Forecast, by Waste type 2020 & 2033

- Table 10: China Plastic Waste Management Industry Volume Billion Forecast, by Waste type 2020 & 2033

- Table 11: China Plastic Waste Management Industry Revenue Million Forecast, by Disposal methods 2020 & 2033

- Table 12: China Plastic Waste Management Industry Volume Billion Forecast, by Disposal methods 2020 & 2033

- Table 13: China Plastic Waste Management Industry Revenue Million Forecast, by Type of ownership 2020 & 2033

- Table 14: China Plastic Waste Management Industry Volume Billion Forecast, by Type of ownership 2020 & 2033

- Table 15: China Plastic Waste Management Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: China Plastic Waste Management Industry Volume Billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Plastic Waste Management Industry?

The projected CAGR is approximately 5.25%.

2. Which companies are prominent players in the China Plastic Waste Management Industry?

Key companies in the market include China Everbright International Limited, Sembcorp Industries Ltd, Veolia Environnement S A, Capital Environmental Holdings Ltd (CEHL), HydroThane**List Not Exhaustive.

3. What are the main segments of the China Plastic Waste Management Industry?

The market segments include Waste type, Disposal methods, Type of ownership.

4. Can you provide details about the market size?

The market size is estimated to be USD 78.38 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Spotlight on the China e-waste generation and its effective management.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Plastic Waste Management Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Plastic Waste Management Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Plastic Waste Management Industry?

To stay informed about further developments, trends, and reports in the China Plastic Waste Management Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence