Key Insights

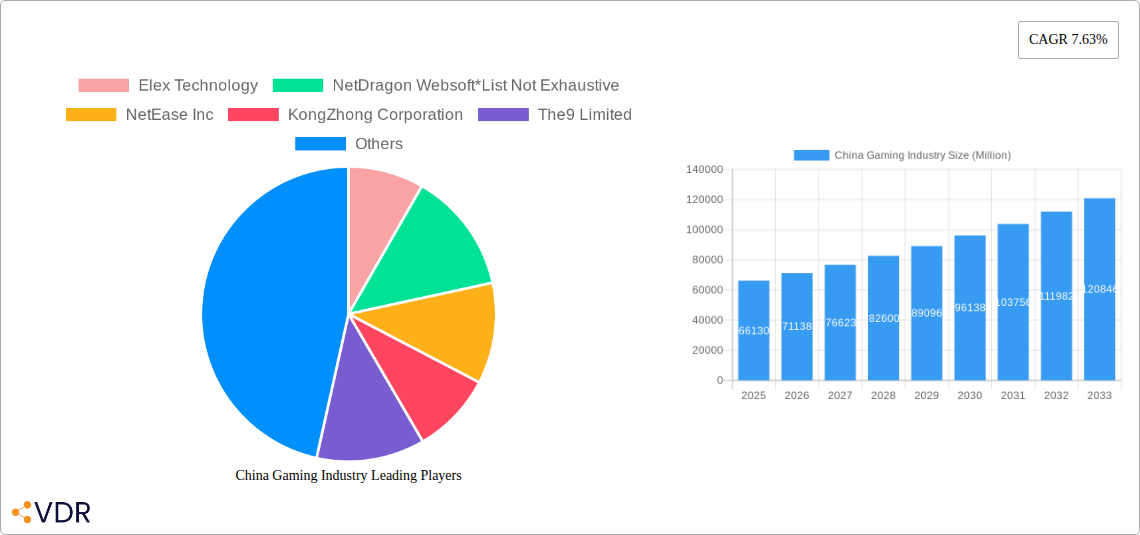

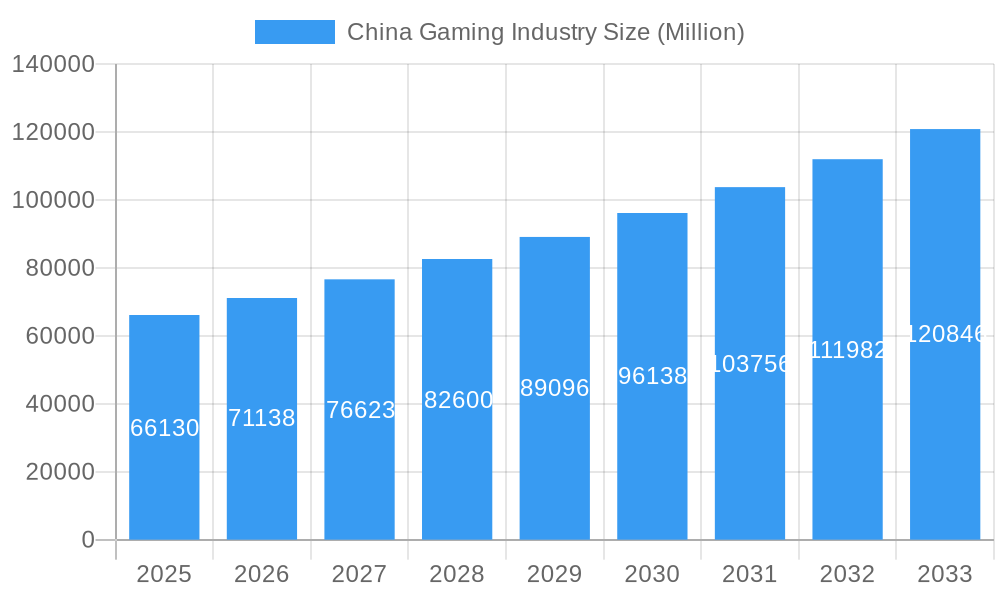

The China gaming market, a powerhouse in the global gaming industry, is projected to maintain robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 7.63% from 2025 to 2033. In 2025, the market size reached $66.13 billion USD. This expansion is fueled by several key drivers. Firstly, the increasing penetration of smartphones and readily available high-speed internet access significantly broadens the player base, particularly amongst younger demographics. Secondly, the continuous evolution of gaming technology, including advancements in graphics, virtual reality (VR), and augmented reality (AR), offers immersive and engaging experiences, driving demand for premium titles. Furthermore, the rising popularity of esports and the integration of gaming into broader social and entertainment culture fuels the market's growth. While government regulations and concerns regarding gaming addiction pose potential restraints, the overall market outlook remains optimistic, driven by a passionate player base and the continuous innovation within the industry. Key market segments, including PC, console, and mobile gaming, all contribute to this dynamic market. Competition among leading companies such as Tencent Holdings, NetEase Inc., and others fosters innovation and expands the range of available games.

China Gaming Industry Market Size (In Billion)

The future of the China gaming market is likely to witness a continued shift towards mobile gaming, given the widespread adoption of smartphones. However, the PC and console segments will remain significant contributors, particularly as technological advancements cater to increasingly sophisticated gaming preferences. Strategic partnerships between game developers and technology companies are expected to enhance the gaming experience and expand market reach. Moreover, diversification into new genres and game formats will be critical for sustained growth. The ongoing evolution of regulatory frameworks will undoubtedly impact the trajectory of the market, necessitating continuous adaptation by industry players. Despite potential challenges, the underlying trends suggest a positive outlook for the China gaming market in the coming years, with continued expansion and increased competition shaping its future landscape.

China Gaming Industry Company Market Share

China Gaming Industry Market Report: 2019-2033

This comprehensive report provides a deep dive into the dynamic China gaming industry, analyzing market trends, key players, and future growth prospects. With a focus on parent and child markets, this report is an essential resource for industry professionals, investors, and strategic decision-makers. The study period covers 2019-2033, with 2025 as the base and estimated year, and a forecast period of 2025-2033.

China Gaming Industry Market Dynamics & Structure

This section analyzes the intricate structure of the China gaming market, encompassing market concentration, technological advancements, regulatory landscapes, competitive dynamics, and evolving end-user demographics. The analysis also considers the impact of mergers and acquisitions (M&A) activities. The Chinese gaming market, valued at xx million in 2024, is characterized by a high degree of concentration amongst a few dominant players. However, smaller independent studios contribute significantly to innovation.

- Market Concentration: Top 5 players hold approximately xx% market share (2024).

- Technological Innovation: Rapid advancements in 5G, AI, and cloud gaming are driving immersive experiences and new game formats. Barriers to entry include high development costs and the need for robust infrastructure.

- Regulatory Framework: Government regulations significantly impact market dynamics. The recent easing of restrictions has opened new opportunities. However, ongoing compliance requirements remain crucial.

- Competitive Product Substitutes: Streaming services and other entertainment options present competitive pressures.

- End-User Demographics: The market caters to a diverse age range, with mobile gaming particularly popular among younger demographics.

- M&A Trends: The industry witnesses significant M&A activity, with larger players acquiring smaller studios to expand their portfolios and technological capabilities. XX major M&A deals were recorded in 2024.

China Gaming Industry Growth Trends & Insights

This section presents a comprehensive analysis of the China gaming market's growth trajectory, encompassing market size evolution, adoption rates, technological disruptions, and evolving consumer preferences. Utilizing robust data analysis and forecasting methodologies, the report provides key insights into past performance and projected future growth.

The Chinese gaming market experienced substantial growth from 2019 to 2024, driven by increasing smartphone penetration, rising disposable incomes, and the expanding popularity of mobile gaming. The market size is projected to reach xx million by 2033, with a Compound Annual Growth Rate (CAGR) of xx%. This growth is fueled by the increasing adoption of advanced technologies, such as augmented reality (AR) and virtual reality (VR), and the shifting preferences of gamers towards more immersive and interactive experiences.

Dominant Regions, Countries, or Segments in China Gaming Industry

This section identifies the leading regions, countries, or segments within the China gaming market that are driving the overall growth. The analysis focuses on market share, growth potential, and key factors contributing to the dominance of specific segments. The analysis is particularly insightful given the diverse nature of the market, with variations in platform preferences across different geographic regions and demographic groups.

- Mobile Games: This segment dominates the market, accounting for approximately xx% of the total revenue in 2024. Key drivers include high smartphone penetration and the convenience of mobile gaming.

- PC Games: This segment maintains a significant share, fueled by the popularity of esports and the dedicated PC gaming community.

- Console Games: While smaller than mobile and PC, console gaming is experiencing growth, driven by increasing availability of consoles and the rising popularity of global gaming titles in China.

The coastal regions of China, particularly the eastern and southern provinces, demonstrate stronger market growth due to higher disposable incomes and advanced technological infrastructure. Government support for digital infrastructure further stimulates growth in these regions.

China Gaming Industry Product Landscape

The China gaming market boasts a diverse product landscape featuring a wide array of gaming titles, from massively multiplayer online role-playing games (MMORPGs) to casual mobile games. Innovation in game design, graphics, and user experience is a key driver of market growth. The integration of advanced technologies, such as artificial intelligence (AI) and cloud computing, is enhancing the gaming experience. This dynamic market continues to witness the emergence of new game genres and formats, fueled by technological advancements and evolving consumer preferences.

Key Drivers, Barriers & Challenges in China Gaming Industry

Key Drivers:

- Technological advancements: 5G, AI, cloud gaming, and improved graphics are enhancing the gaming experience.

- Rising disposable incomes: Increased spending power fuels higher gaming expenditure.

- Government support: Relaxation of regulations and investments in digital infrastructure are positive catalysts.

Challenges:

- Regulatory hurdles: Stringent regulations and licensing processes can limit market expansion.

- Intense competition: The highly competitive landscape necessitates continuous innovation and marketing efforts.

- Piracy: Illegal game downloads affect revenue streams for developers and publishers.

Emerging Opportunities in China Gaming Industry

- Expansion into untapped markets: Reaching rural areas and less-penetrated demographic segments presents significant growth potential.

- Innovation in game genres: Developing new and unique gaming experiences to capture diverse player interests.

- Leveraging esports: Capitalizing on the growth of esports and developing associated revenue streams.

Growth Accelerators in the China Gaming Industry Industry

The long-term growth of the China gaming industry is expected to be fueled by several key factors. Continuous technological innovations, strategic partnerships between developers and technology companies, and expansion into international markets will propel market growth. The increasing adoption of cloud gaming technology will further expand access to gaming experiences, particularly in regions with limited internet infrastructure.

Key Players Shaping the China Gaming Industry Market

- Elex Technology

- NetDragon Websoft

- NetEase Inc

- KongZhong Corporation

- The9 Limited

- 37 Interactive Entertainment

- Perfect World Games

- Tencent Holdings

- Beijing Kunlun Technology Co Ltd

- Shanda Games

Notable Milestones in China Gaming Industry Sector

- September 2022: Tencent Holdings and NetEase receive approval to launch new paid games, signaling a relaxation of regulatory restrictions. Seventy-three online games (including 69 mobile games) were granted publishing licenses.

- August 2022: NetEase Inc. acquires Quantic Dream SA, strengthening its game development capabilities and portfolio.

In-Depth China Gaming Industry Market Outlook

The future of the China gaming market appears bright, with sustained growth anticipated throughout the forecast period. The continuous development and adoption of new technologies, coupled with strategic expansions and market diversification, will drive further growth. The market is poised to benefit from increasing smartphone penetration, rising disposable incomes, and the evolving preferences of gamers towards richer and more immersive experiences. Strategic partnerships and investments in innovative technologies will be critical in shaping the future of the industry.

China Gaming Industry Segmentation

- 1. China Gaming Market Sizing & Forecast

- 2. Gamers Population in China

- 3. Gamers Population Age and Gender

-

4. Market Segmentation Platform

- 4.1. PC Games

- 4.2. Console Games

- 4.3. Mobile Games

- 5. PC Games

- 6. Console Games

- 7. Mobile Games

- 8. Top 20 Android Games & Apps in China

- 9. Top 20 iOS Games & Apps in China

- 10. Suspension of Gaming Licenses in China

- 11. Foreign Companies Share in Chinese Gaming Industry

China Gaming Industry Segmentation By Geography

- 1. China

China Gaming Industry Regional Market Share

Geographic Coverage of China Gaming Industry

China Gaming Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.63% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by China Gaming Market Sizing & Forecast

- 5.2. Market Analysis, Insights and Forecast - by Gamers Population in China

- 5.3. Market Analysis, Insights and Forecast - by Gamers Population Age and Gender

- 5.4. Market Analysis, Insights and Forecast - by Market Segmentation Platform

- 5.4.1. PC Games

- 5.4.2. Console Games

- 5.4.3. Mobile Games

- 5.5. Market Analysis, Insights and Forecast - by PC Games

- 5.6. Market Analysis, Insights and Forecast - by Console Games

- 5.7. Market Analysis, Insights and Forecast - by Mobile Games

- 5.8. Market Analysis, Insights and Forecast - by Top 20 Android Games & Apps in China

- 5.9. Market Analysis, Insights and Forecast - by Top 20 iOS Games & Apps in China

- 5.10. Market Analysis, Insights and Forecast - by Suspension of Gaming Licenses in China

- 5.11. Market Analysis, Insights and Forecast - by Foreign Companies Share in Chinese Gaming Industry

- 5.12. Market Analysis, Insights and Forecast - by Region

- 5.12.1. China

- 6. China Gaming Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by China Gaming Market Sizing & Forecast

- 6.2. Market Analysis, Insights and Forecast - by Gamers Population in China

- 6.3. Market Analysis, Insights and Forecast - by Gamers Population Age and Gender

- 6.4. Market Analysis, Insights and Forecast - by Market Segmentation Platform

- 6.4.1. PC Games

- 6.4.2. Console Games

- 6.4.3. Mobile Games

- 6.5. Market Analysis, Insights and Forecast - by PC Games

- 6.6. Market Analysis, Insights and Forecast - by Console Games

- 6.7. Market Analysis, Insights and Forecast - by Mobile Games

- 6.8. Market Analysis, Insights and Forecast - by Top 20 Android Games & Apps in China

- 6.9. Market Analysis, Insights and Forecast - by Top 20 iOS Games & Apps in China

- 6.10. Market Analysis, Insights and Forecast - by Suspension of Gaming Licenses in China

- 6.11. Market Analysis, Insights and Forecast - by Foreign Companies Share in Chinese Gaming Industry

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Elex Technology

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 NetDragon Websoft*List Not Exhaustive

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 NetEase Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 KongZhong Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 The9 Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 37 Interactive Entertainment

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Perfect World Games

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Tencent Holdings

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Beijing Kunlun Technology Co Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Shanda Games

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Elex Technology

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Gaming Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: China Gaming Industry Share (%) by Company 2025

List of Tables

- Table 1: China Gaming Industry Revenue Million Forecast, by China Gaming Market Sizing & Forecast 2020 & 2033

- Table 2: China Gaming Industry Revenue Million Forecast, by Gamers Population in China 2020 & 2033

- Table 3: China Gaming Industry Revenue Million Forecast, by Gamers Population Age and Gender 2020 & 2033

- Table 4: China Gaming Industry Revenue Million Forecast, by Market Segmentation Platform 2020 & 2033

- Table 5: China Gaming Industry Revenue Million Forecast, by PC Games 2020 & 2033

- Table 6: China Gaming Industry Revenue Million Forecast, by Console Games 2020 & 2033

- Table 7: China Gaming Industry Revenue Million Forecast, by Mobile Games 2020 & 2033

- Table 8: China Gaming Industry Revenue Million Forecast, by Top 20 Android Games & Apps in China 2020 & 2033

- Table 9: China Gaming Industry Revenue Million Forecast, by Top 20 iOS Games & Apps in China 2020 & 2033

- Table 10: China Gaming Industry Revenue Million Forecast, by Suspension of Gaming Licenses in China 2020 & 2033

- Table 11: China Gaming Industry Revenue Million Forecast, by Foreign Companies Share in Chinese Gaming Industry 2020 & 2033

- Table 12: China Gaming Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 13: China Gaming Industry Revenue Million Forecast, by China Gaming Market Sizing & Forecast 2020 & 2033

- Table 14: China Gaming Industry Revenue Million Forecast, by Gamers Population in China 2020 & 2033

- Table 15: China Gaming Industry Revenue Million Forecast, by Gamers Population Age and Gender 2020 & 2033

- Table 16: China Gaming Industry Revenue Million Forecast, by Market Segmentation Platform 2020 & 2033

- Table 17: China Gaming Industry Revenue Million Forecast, by PC Games 2020 & 2033

- Table 18: China Gaming Industry Revenue Million Forecast, by Console Games 2020 & 2033

- Table 19: China Gaming Industry Revenue Million Forecast, by Mobile Games 2020 & 2033

- Table 20: China Gaming Industry Revenue Million Forecast, by Top 20 Android Games & Apps in China 2020 & 2033

- Table 21: China Gaming Industry Revenue Million Forecast, by Top 20 iOS Games & Apps in China 2020 & 2033

- Table 22: China Gaming Industry Revenue Million Forecast, by Suspension of Gaming Licenses in China 2020 & 2033

- Table 23: China Gaming Industry Revenue Million Forecast, by Foreign Companies Share in Chinese Gaming Industry 2020 & 2033

- Table 24: China Gaming Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Gaming Industry?

The projected CAGR is approximately 7.63%.

2. Which companies are prominent players in the China Gaming Industry?

Key companies in the market include Elex Technology, NetDragon Websoft*List Not Exhaustive, NetEase Inc, KongZhong Corporation, The9 Limited, 37 Interactive Entertainment, Perfect World Games, Tencent Holdings, Beijing Kunlun Technology Co Ltd, Shanda Games.

3. What are the main segments of the China Gaming Industry?

The market segments include China Gaming Market Sizing & Forecast, Gamers Population in China, Gamers Population Age and Gender, Market Segmentation Platform, PC Games, Console Games, Mobile Games, Top 20 Android Games & Apps in China, Top 20 iOS Games & Apps in China, Suspension of Gaming Licenses in China, Foreign Companies Share in Chinese Gaming Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 66.13 Million as of 2022.

5. What are some drivers contributing to market growth?

Rapid Advancement in Technological Developments.

6. What are the notable trends driving market growth?

Mobile Games Occupies the Largest Market Share.

7. Are there any restraints impacting market growth?

Fluctuating Government Regulations Regarding Gaming Industry.

8. Can you provide examples of recent developments in the market?

September 2022: Tencent Holdings and NetEase, two of China's largest video game companies, got approval to launch new paid games for the first time since July last year, indicating Beijing's relaxation of a two-year crackdown on the tech sector. Seventy-three online games, including 69 mobile games, were given publishing licenses by the National Press and Publication Administration. Licenses were also granted to CMGE Technology Group., Leiting, XD Inc, and Zhong Qing Bao.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Gaming Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Gaming Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Gaming Industry?

To stay informed about further developments, trends, and reports in the China Gaming Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence