Key Insights

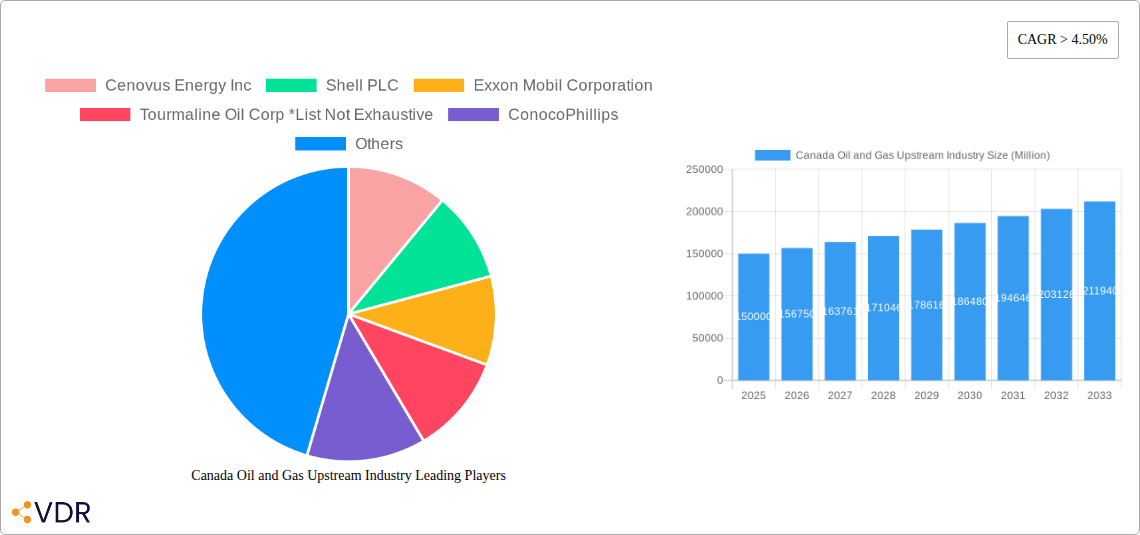

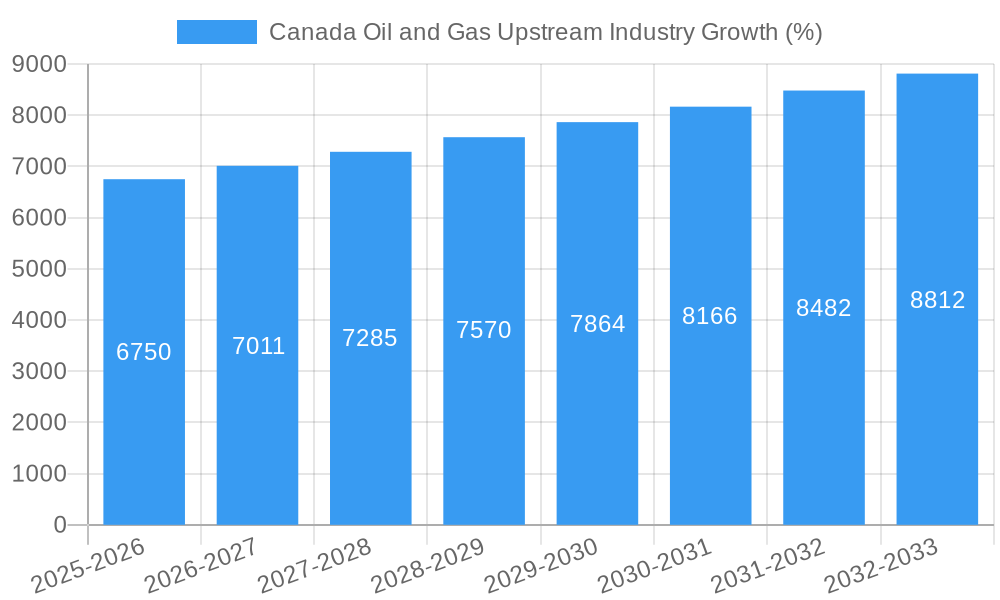

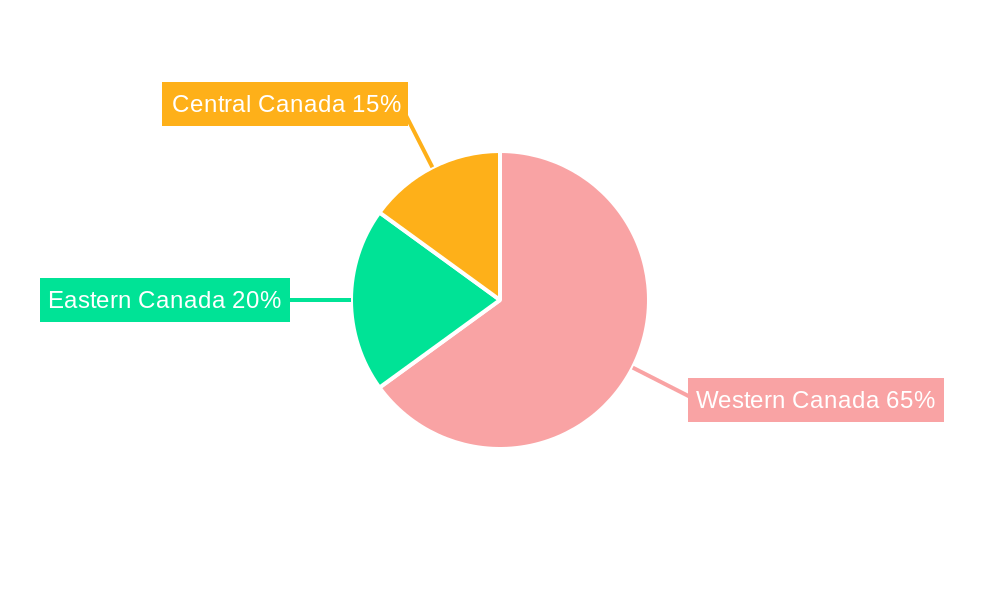

The Canadian oil and gas upstream industry, encompassing crude oil, natural gas, and condensate production, is experiencing robust growth, projected to maintain a Compound Annual Growth Rate (CAGR) exceeding 4.5% from 2025 to 2033. This expansion is driven by increasing global energy demand, particularly in the Asia-Pacific region, coupled with Canada's significant reserves and strategic geographic location. Key application segments such as transportation, power generation, and petrochemicals are fueling this growth, with industrial end-users representing the largest consumer base. While environmental regulations and fluctuating global oil prices present challenges, technological advancements in extraction and processing, along with government initiatives to support responsible resource development, are mitigating these restraints. The industry is segmented geographically, with Western Canada historically dominating production due to its substantial oil sands reserves. However, growth is expected across all regions – Eastern, Central, and Western Canada – driven by exploration in less developed areas and infrastructure improvements. Major players like Cenovus Energy, Shell, ExxonMobil, and ConocoPhillips are actively involved, shaping the competitive landscape through strategic investments and technological innovation.

The market size in 2025 is estimated at $150 billion (USD) based on typical industry valuations for similar markets with comparable CAGR projections. Given the 4.5% CAGR, we can project substantial growth over the forecast period. This growth, however, isn't uniform across all segments. While the industrial sector remains the dominant end-user, the residential and commercial segments are expected to experience faster growth rates driven by increased urbanization and infrastructure development. Similarly, natural gas production is likely to see accelerated growth compared to crude oil, driven by its increasing role in power generation and its relative environmental benefits compared to coal. The ongoing transition towards cleaner energy sources presents both challenges and opportunities, requiring the industry to adapt and invest in carbon capture and emission reduction technologies to sustain long-term growth and maintain its competitive position in the global energy market.

Canada Oil and Gas Upstream Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Canadian oil and gas upstream industry, encompassing market dynamics, growth trends, dominant segments, and key players. Covering the period from 2019 to 2033, with a base year of 2025, this report is an essential resource for industry professionals, investors, and strategic decision-makers. The report uses Million units (MM) for all value figures.

Canada Oil and Gas Upstream Industry Market Dynamics & Structure

This section analyzes the intricate structure of Canada's oil and gas upstream sector, focusing on market concentration, technological advancements, regulatory landscapes, competitive dynamics, and market trends. The analysis incorporates both quantitative data (market share, M&A activity) and qualitative insights (innovation barriers, regulatory impacts).

- Market Concentration: The Canadian upstream sector exhibits a moderately concentrated market structure, with major players like Cenovus Energy Inc, Shell PLC, Exxon Mobil Corporation, and Tourmaline Oil Corp holding significant market share. However, the presence of numerous smaller independent producers contributes to a dynamic competitive landscape. The market share of the top 5 companies is estimated at xx% in 2025.

- Technological Innovation: Technological advancements, such as enhanced oil recovery (EOR) techniques and digitalization, are driving efficiency improvements and boosting production. However, high initial investment costs and regulatory hurdles present significant barriers to widespread adoption.

- Regulatory Framework: Stringent environmental regulations and evolving climate policies significantly impact industry operations and investment decisions. The carbon tax and methane emission regulations are key factors influencing operational strategies and capital expenditure.

- Competitive Product Substitutes: The growing adoption of renewable energy sources presents a competitive challenge to the oil and gas industry, although natural gas is positioned as a transition fuel.

- M&A Activity: The historical period (2019-2024) witnessed xx M&A deals, primarily driven by consolidation efforts among smaller producers and strategic acquisitions by larger companies. This activity is expected to continue in the forecast period (2025-2033), albeit at a potentially moderated pace due to regulatory scrutiny and economic uncertainty. The total deal value in the historical period is estimated at xx MM.

- End-User Demographics: The primary end-users of crude oil and natural gas are the industrial, commercial, and residential sectors, with transportation being the most significant consumer of crude oil. Demand patterns vary based on economic activity and seasonal variations.

Canada Oil and Gas Upstream Industry Growth Trends & Insights

This section provides a detailed analysis of the historical and projected growth trajectory of the Canadian oil and gas upstream market, incorporating key macroeconomic factors, technological disruptions, and shifts in consumer behaviour. This analysis will incorporate data from various sources, including government reports, industry publications, and company filings. The analysis will explore factors such as shifting energy demand, the impact of government policies on investment, and advancements in exploration and production technologies. The report will also assess the future outlook for the market, factoring in uncertainty in commodity prices, global competition, and environmental concerns. The projected CAGR for the forecast period (2025-2033) is estimated at xx%. The market size in 2025 is predicted to be xx MM, increasing to xx MM by 2033.

Dominant Regions, Countries, or Segments in Canada Oil and Gas Upstream Industry

This section pinpoints the leading regions, countries, and segments within the Canadian oil and gas upstream industry driving growth. The analysis will focus on the relative contributions of different product types (crude oil, natural gas, condensate), application sectors (transportation, heating, power generation, petrochemicals), and end-user segments (industrial, commercial, residential).

- Dominant Segment: Alberta is the leading province for oil and gas production, followed by Saskatchewan and British Columbia. Crude oil currently represents the largest segment by revenue, followed by natural gas, while the transportation sector holds the most significant share in terms of oil consumption.

- Growth Drivers: Strong economic activity, robust industrial demand, and increasing natural gas exports are significant factors contributing to industry growth. Government incentives for oil sands development, however, are under increasing scrutiny due to environmental concerns.

Canada Oil and Gas Upstream Industry Product Landscape

The Canadian oil and gas upstream industry offers a range of products, including conventional and unconventional crude oil, natural gas, and natural gas liquids (NGLs). Technological advancements continue to enhance extraction efficiency and production quality. EOR techniques play a vital role in maximizing recovery from mature oil fields, while innovative drilling and completion methods enhance productivity in unconventional resources. The focus on reducing environmental impact is also shaping product development and market strategies.

Key Drivers, Barriers & Challenges in Canada Oil and Gas Upstream Industry

Key Drivers:

- Increasing global energy demand, particularly in emerging economies.

- Technological advancements enhancing exploration and production efficiency.

- Strategic partnerships and investments in new technologies.

Key Challenges and Restraints:

- Fluctuating commodity prices, creating uncertainty in investment decisions.

- Stringent environmental regulations, including carbon pricing mechanisms.

- Growing concerns regarding climate change and the transition to lower-carbon energy sources. This transition may reduce demand for fossil fuels in the longer term. The impact is estimated to be a xx% reduction in demand by 2033.

Emerging Opportunities in Canada Oil and Gas Upstream Industry

- Growing demand for natural gas as a transition fuel.

- Potential for carbon capture and storage (CCS) technology to mitigate environmental impact.

- Exploration and development of offshore oil and gas resources.

Growth Accelerators in the Canada Oil and Gas Upstream Industry

Technological breakthroughs, such as improved EOR techniques and automation, are key growth accelerators. Strategic partnerships and collaborations between energy companies and technology providers are crucial for unlocking innovation and accelerating industry growth. Expansion into new exploration areas and diversification into related sectors, such as renewable energy, also represent key growth strategies.

Key Players Shaping the Canada Oil and Gas Upstream Industry Market

- Cenovus Energy Inc

- Shell PLC

- Exxon Mobil Corporation

- Tourmaline Oil Corp

- ConocoPhillips

- Chevron Corporation

- TotalEnergies SE

- BP PLC

Notable Milestones in Canada Oil and Gas Upstream Industry Sector

- January 2021: Chevron Canada, Equinor Canada, and BHP Petroleum secured approvals for three offshore drilling projects in Newfoundland and Labrador.

In-Depth Canada Oil and Gas Upstream Industry Market Outlook

The Canadian oil and gas upstream industry faces a complex interplay of challenges and opportunities. While the transition to a lower-carbon economy presents significant headwinds, the ongoing demand for natural gas as a transition fuel and potential for carbon capture and storage technologies present opportunities for growth. Strategic investments in technology, operational efficiency, and sustainable practices will be crucial for long-term success in this evolving landscape. The market is projected to show moderate growth in the coming years, driven by increasing global energy demand and technological advancements. However, the pace of growth will depend heavily on the global energy transition and government regulations.

Canada Oil and Gas Upstream Industry Segmentation

- 1. Onshore

- 2. Offshore

Canada Oil and Gas Upstream Industry Segmentation By Geography

- 1. Canada

Canada Oil and Gas Upstream Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 4.50% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Declining Solar Panel Costs4.; Supportive Government Policies

- 3.3. Market Restrains

- 3.3.1. 4.; High Upfront Cost

- 3.4. Market Trends

- 3.4.1. Offshore Segment to Witness Significant Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Canada Oil and Gas Upstream Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Onshore

- 5.2. Market Analysis, Insights and Forecast - by Offshore

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Onshore

- 6. Eastern Canada Canada Oil and Gas Upstream Industry Analysis, Insights and Forecast, 2019-2031

- 7. Western Canada Canada Oil and Gas Upstream Industry Analysis, Insights and Forecast, 2019-2031

- 8. Central Canada Canada Oil and Gas Upstream Industry Analysis, Insights and Forecast, 2019-2031

- 9. Competitive Analysis

- 9.1. Market Share Analysis 2024

- 9.2. Company Profiles

- 9.2.1 Cenovus Energy Inc

- 9.2.1.1. Overview

- 9.2.1.2. Products

- 9.2.1.3. SWOT Analysis

- 9.2.1.4. Recent Developments

- 9.2.1.5. Financials (Based on Availability)

- 9.2.2 Shell PLC

- 9.2.2.1. Overview

- 9.2.2.2. Products

- 9.2.2.3. SWOT Analysis

- 9.2.2.4. Recent Developments

- 9.2.2.5. Financials (Based on Availability)

- 9.2.3 Exxon Mobil Corporation

- 9.2.3.1. Overview

- 9.2.3.2. Products

- 9.2.3.3. SWOT Analysis

- 9.2.3.4. Recent Developments

- 9.2.3.5. Financials (Based on Availability)

- 9.2.4 Tourmaline Oil Corp *List Not Exhaustive

- 9.2.4.1. Overview

- 9.2.4.2. Products

- 9.2.4.3. SWOT Analysis

- 9.2.4.4. Recent Developments

- 9.2.4.5. Financials (Based on Availability)

- 9.2.5 ConocoPhillips

- 9.2.5.1. Overview

- 9.2.5.2. Products

- 9.2.5.3. SWOT Analysis

- 9.2.5.4. Recent Developments

- 9.2.5.5. Financials (Based on Availability)

- 9.2.6 Chevron Corporation

- 9.2.6.1. Overview

- 9.2.6.2. Products

- 9.2.6.3. SWOT Analysis

- 9.2.6.4. Recent Developments

- 9.2.6.5. Financials (Based on Availability)

- 9.2.7 TotalEnergies SE

- 9.2.7.1. Overview

- 9.2.7.2. Products

- 9.2.7.3. SWOT Analysis

- 9.2.7.4. Recent Developments

- 9.2.7.5. Financials (Based on Availability)

- 9.2.8 BP PLC

- 9.2.8.1. Overview

- 9.2.8.2. Products

- 9.2.8.3. SWOT Analysis

- 9.2.8.4. Recent Developments

- 9.2.8.5. Financials (Based on Availability)

- 9.2.1 Cenovus Energy Inc

List of Figures

- Figure 1: Canada Oil and Gas Upstream Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Canada Oil and Gas Upstream Industry Share (%) by Company 2024

List of Tables

- Table 1: Canada Oil and Gas Upstream Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Canada Oil and Gas Upstream Industry Revenue Million Forecast, by Onshore 2019 & 2032

- Table 3: Canada Oil and Gas Upstream Industry Revenue Million Forecast, by Offshore 2019 & 2032

- Table 4: Canada Oil and Gas Upstream Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Canada Oil and Gas Upstream Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Eastern Canada Canada Oil and Gas Upstream Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Western Canada Canada Oil and Gas Upstream Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Central Canada Canada Oil and Gas Upstream Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Canada Oil and Gas Upstream Industry Revenue Million Forecast, by Onshore 2019 & 2032

- Table 10: Canada Oil and Gas Upstream Industry Revenue Million Forecast, by Offshore 2019 & 2032

- Table 11: Canada Oil and Gas Upstream Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Oil and Gas Upstream Industry?

The projected CAGR is approximately > 4.50%.

2. Which companies are prominent players in the Canada Oil and Gas Upstream Industry?

Key companies in the market include Cenovus Energy Inc, Shell PLC, Exxon Mobil Corporation, Tourmaline Oil Corp *List Not Exhaustive, ConocoPhillips, Chevron Corporation, TotalEnergies SE, BP PLC.

3. What are the main segments of the Canada Oil and Gas Upstream Industry?

The market segments include Onshore, Offshore.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Declining Solar Panel Costs4.; Supportive Government Policies.

6. What are the notable trends driving market growth?

Offshore Segment to Witness Significant Growth.

7. Are there any restraints impacting market growth?

4.; High Upfront Cost.

8. Can you provide examples of recent developments in the market?

In January 2021, Chevron Canada, Equinor Canada, and BHP Petroleum (New Ventures) secured approvals from the Environment and Climate Change Minister to conduct drilling at three offshore drilling projects east of St. John's, Newfoundland, and Labrador. The companies have proposed operating offshore platforms like ships and helicopters to conduct exploration drilling and well testing.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Oil and Gas Upstream Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Oil and Gas Upstream Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Oil and Gas Upstream Industry?

To stay informed about further developments, trends, and reports in the Canada Oil and Gas Upstream Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence