Key Insights

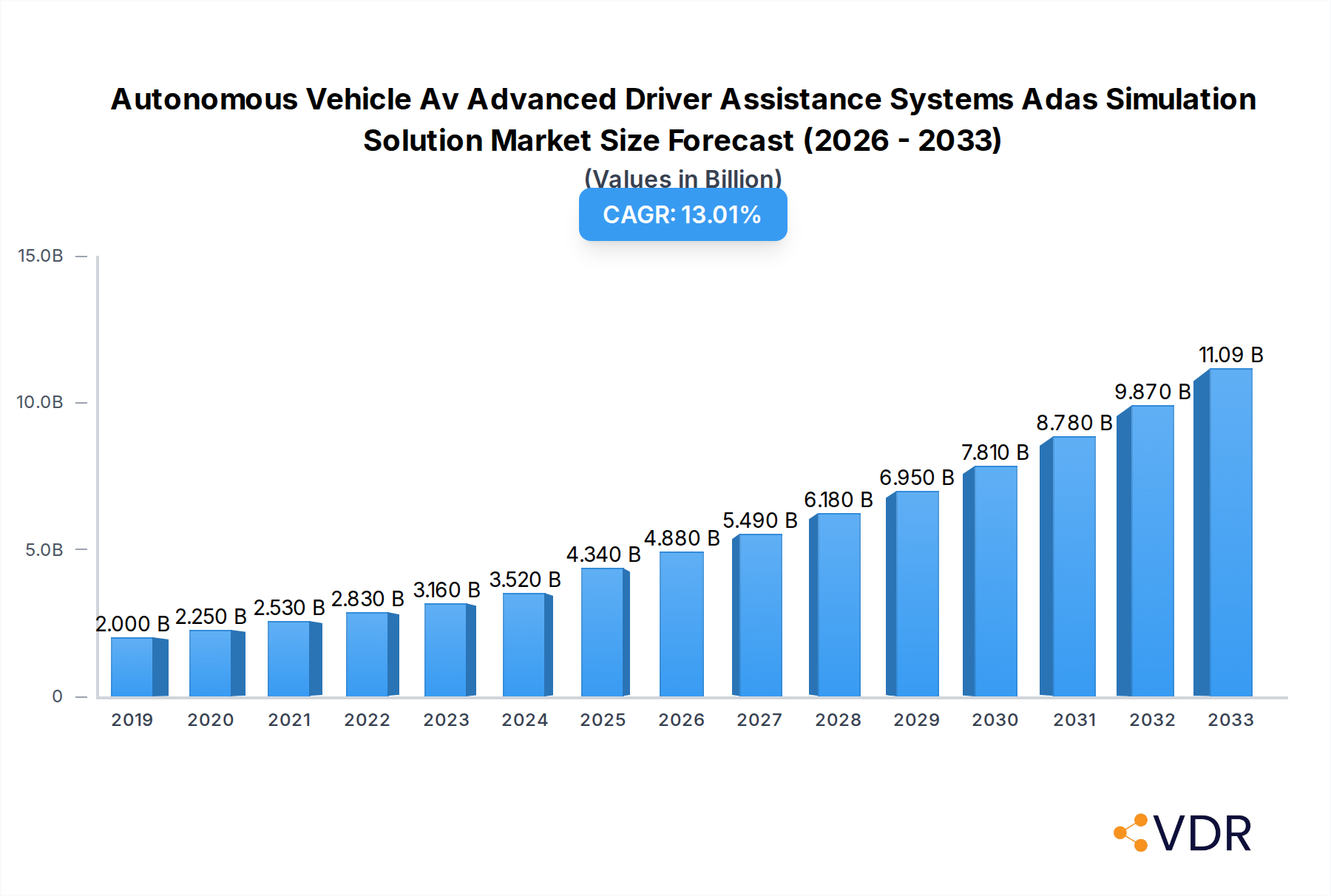

The global market for Autonomous Vehicle (AV) and Advanced Driver Assistance Systems (ADAS) simulation solutions is poised for significant expansion, projected to reach an estimated USD 4340 million by 2025, and is anticipated to grow at a robust Compound Annual Growth Rate (CAGR) of 12.5% through 2033. This escalating demand is primarily fueled by the relentless pursuit of enhanced vehicle safety and the rapid advancement of autonomous driving technologies. Key drivers include the increasing regulatory pressure for safer vehicles, the growing consumer acceptance of ADAS features, and the substantial investments in research and development by automotive manufacturers and technology providers. Simulation plays a critical role in accelerating the development and validation of complex AV and ADAS systems, offering a cost-effective and efficient alternative to extensive real-world testing. The market's trajectory is further bolstered by the growing sophistication of simulation tools, enabling more realistic and comprehensive testing scenarios, from basic lane-keeping assist to complex urban autonomous driving. The industry's focus on data-driven development and the need to train AI algorithms for perception, prediction, and planning are also substantial contributors to the market's upward trend.

Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Market Size (In Billion)

The market's dynamism is characterized by a strong emphasis on innovation and the development of sophisticated simulation platforms. Leading companies are investing heavily in creating virtual environments that accurately replicate real-world driving conditions, including diverse weather, lighting, and traffic scenarios, as well as edge cases that are difficult to encounter in physical testing. This allows for the rapid iteration and refinement of AV and ADAS algorithms, significantly reducing development cycles and costs. Emerging trends include the integration of AI and machine learning within simulation environments to generate realistic sensor data and to train and test perception systems more effectively. Furthermore, the rise of Hardware-in-the-Loop (HiL) and Software-in-the-Loop (SiL) testing methodologies are integral to ensuring the reliability and safety of these advanced automotive systems. While the market shows immense promise, potential restraints include the high initial investment in sophisticated simulation infrastructure and the need for skilled personnel to operate and manage these complex systems. However, the overarching need for robust validation and the increasing complexity of autonomous driving functionalities are expected to outweigh these challenges, driving continued market growth.

Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Company Market Share

Autonomous Vehicle AV Advanced Driver Assistance Systems (ADAS) Simulation Solution Market Dynamics & Structure

The Autonomous Vehicle (AV) and Advanced Driver Assistance Systems (ADAS) simulation solution market is characterized by a moderate to high concentration, with key players like Siemens, Dassault Systèmes, ANSYS, Inc., and Altair Engineering Inc. dominating the landscape. Technological innovation is the primary driver, fueled by the relentless pursuit of higher levels of vehicle autonomy and the critical need for robust, cost-effective testing methodologies. Regulatory frameworks, while still evolving, are increasingly mandating safety validation, pushing adoption of advanced simulation tools. Competitive product substitutes, primarily physical testing, are being challenged by the efficiency and scalability of simulation. End-user demographics span automobile manufacturers, autonomous driving technology companies, ADAS technology providers, and a growing segment of research institutions and Tier 1 suppliers. Mergers and acquisitions (M&A) are active, driven by the need for consolidated offerings and expanded capabilities. Recent M&A activity has seen significant investments in companies specializing in sensor simulation, scenario generation, and AI-driven validation, reflecting the industry's drive towards comprehensive digital twins for AV development. The complexity of AV systems necessitates integrated simulation platforms, leading to strategic alliances and acquisitions aimed at bridging hardware-in-the-loop (HiL) and software-in-the-loop (SiL) capabilities.

- Market Concentration: Moderate to High, driven by the specialized nature of the technology.

- Technological Innovation Drivers: Increasing complexity of AV/ADAS features, stringent safety regulations, cost reduction imperatives, and the need for rapid development cycles.

- Regulatory Frameworks: Growing mandates for safety validation of ADAS and AV systems, influencing testing requirements.

- Competitive Product Substitutes: Physical testing, while still relevant, faces limitations in terms of scalability, cost, and repeatability compared to simulation.

- End-User Demographics: Automobile Manufacturers, Autonomous Driving Technology Companies, ADAS Technology Providers, Research Institutions, Tier 1 Suppliers.

- M&A Trends: Active consolidation, with focus on sensor fusion simulation, AI-driven testing, and end-to-end validation solutions.

Autonomous Vehicle AV Advanced Driver Assistance Systems (ADAS) Simulation Solution Growth Trends & Insights

The global Autonomous Vehicle (AV) and Advanced Driver Assistance Systems (ADAS) simulation solution market is poised for substantial expansion, driven by the accelerating development and deployment of autonomous driving technologies. The market size, estimated to be approximately $3,200 million in 2025, is projected to reach an impressive $8,500 million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 13.5% during the forecast period of 2025–2033. This robust growth is underpinned by several critical factors. Firstly, the increasing complexity of automotive safety regulations worldwide necessitates rigorous and comprehensive testing of ADAS and AV functionalities, which can only be efficiently achieved through advanced simulation. The shift from traditional physical testing to virtual validation is gaining momentum due to its cost-effectiveness, speed, and ability to simulate rare or hazardous scenarios that are difficult or impossible to replicate in the real world.

Secondly, the rapid advancements in artificial intelligence (AI) and machine learning (ML) are significantly enhancing the capabilities of simulation solutions, enabling more realistic environmental modeling, sensor simulation, and scenario generation. This technological disruption allows for the validation of increasingly sophisticated AI-driven driving algorithms, a core component of autonomous systems. Furthermore, the evolving consumer demand for enhanced safety features and the convenience offered by semi-autonomous and fully autonomous driving capabilities are creating a strong pull for the underlying ADAS technologies, subsequently driving the demand for their simulation counterparts.

The adoption rates of simulation solutions are also on an upward trajectory across the automotive value chain. Automobile manufacturers are increasingly integrating simulation into their R&D pipelines, while dedicated autonomous driving technology companies and ADAS technology providers are relying heavily on these tools for algorithm development, validation, and certification. The market penetration of simulation solutions is expected to deepen as the industry moves towards higher levels of autonomy (Level 3, 4, and 5). Consumer behavior shifts, influenced by increasing awareness of safety technologies and the desire for advanced in-car experiences, are indirectly fueling this demand. The market is also witnessing a growing trend towards cloud-based simulation platforms, offering greater scalability, accessibility, and collaborative development environments, further accelerating market growth. The convergence of HiL and SiL methodologies within comprehensive simulation frameworks is also a significant trend, providing a more holistic validation approach.

Dominant Regions, Countries, or Segments in Autonomous Vehicle AV Advanced Driver Assistance Systems (ADAS) Simulation Solution

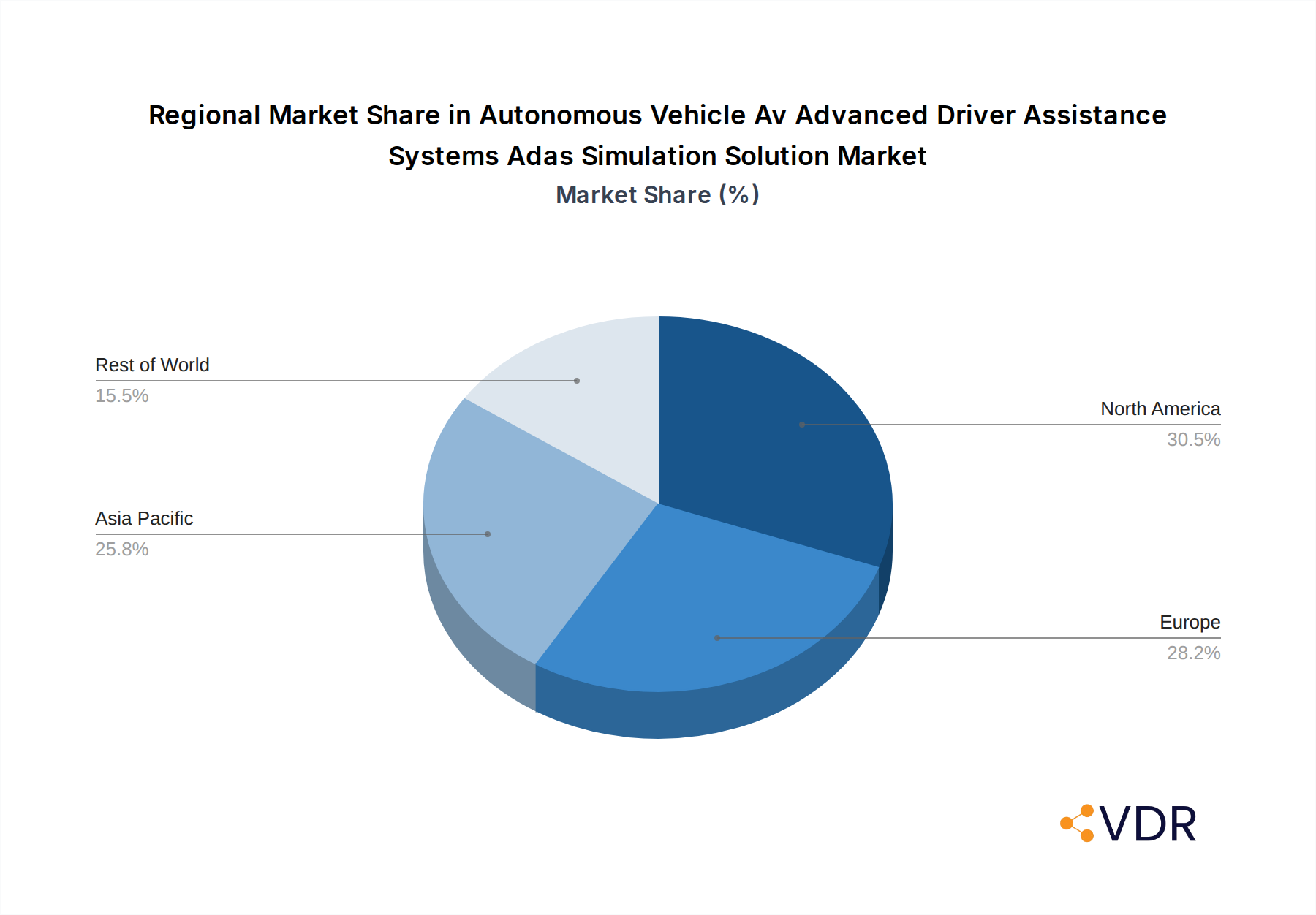

The global Autonomous Vehicle (AV) and Advanced Driver Assistance Systems (ADAS) simulation solution market is experiencing significant growth across various regions, with North America and Europe emerging as the dominant forces, closely followed by Asia Pacific. This regional dominance is primarily driven by a confluence of factors including robust automotive industries, substantial investments in R&D for autonomous driving, stringent regulatory frameworks demanding advanced safety validation, and a high concentration of leading automotive manufacturers and technology providers.

In North America, the United States stands out due to its pioneering role in autonomous vehicle development and testing. Government initiatives supporting AV research and deployment, coupled with substantial private sector investment from major automotive OEMs and tech giants like Google and Amazon Web Services, Inc., create a fertile ground for simulation solutions. The presence of key players such as Applied Intuition, Inc., and a strong ecosystem of ADAS technology providers further solidify its leadership. The application segment of Autonomous Driving Technology Companies is a significant driver in this region, heavily relying on advanced simulation for their cutting-edge development. The Software-in-the-Loop (SiL) type of simulation is particularly prominent here, enabling rapid iteration and validation of complex software algorithms.

Europe, with its strong automotive heritage and stringent safety standards like Euro NCAP, is another powerhouse. Countries like Germany, France, and the UK are home to major automotive manufacturers (e.g., Robert Bosch GmbH) and specialized simulation providers (e.g., VI-grade GmbH, AB Dynamics plc (rFpro)). The emphasis on safety and the increasing regulatory push for ADAS feature deployment are key growth catalysts. The Automobile Manufacturers segment is the primary consumer of simulation solutions in Europe, leveraging them for their extensive vehicle development programs. Similar to North America, the adoption of Software-in-the-Loop (SiL) is high, complemented by increasing adoption of Hardware-in-the-Loop (HiL) for integrating real ECUs into the simulation environment.

Asia Pacific, particularly China, is rapidly emerging as a critical market. The Chinese government's ambitious plans for autonomous vehicle development and smart city initiatives, along with massive investments in electric vehicle (EV) technology, are fueling a significant surge in demand for simulation solutions. The country's large automotive market and a growing number of domestic AV startups and ADAS technology providers are key contributors to this growth. While North America and Europe currently lead in terms of market share, Asia Pacific is expected to witness the fastest growth rate in the coming years, driven by increasing adoption and a dynamic technological landscape. The ADAS Technology Providers segment is experiencing rapid expansion here, seeking efficient validation tools. Both SiL and HiL are seeing accelerated adoption as the region catches up on advanced simulation methodologies.

Autonomous Vehicle AV Advanced Driver Assistance Systems (ADAS) Simulation Solution Product Landscape

The product landscape for Autonomous Vehicle (AV) and Advanced Driver Assistance Systems (ADAS) simulation solutions is characterized by sophisticated platforms offering comprehensive digital environments for virtual testing. These solutions focus on highly accurate sensor modeling (e.g., radar, lidar, camera), realistic environmental rendering, and complex traffic scenario generation. Key innovations include the integration of AI and machine learning for intelligent scenario creation and anomaly detection, as well as advanced physics-based modeling for precise vehicle dynamics and sensor response simulation. Performance metrics are centered on the fidelity of the simulation, the speed of execution, the scalability of testing, and the ability to seamlessly integrate with existing development workflows, including Hardware-in-the-Loop (HiL) and Software-in-the-Loop (SiL) testing. Unique selling propositions often lie in the extensibility of the platforms, the depth of their scenario libraries, and their validation capabilities for a wide range of ADAS features and autonomous driving functions.

Key Drivers, Barriers & Challenges in Autonomous Vehicle AV Advanced Driver Assistance Systems (ADAS) Simulation Solution

Key Drivers:

- Increasingly Complex ADAS and AV Systems: The growing sophistication of features requires extensive and repeatable testing.

- Stringent Safety Regulations: Mandates for safety validation necessitate robust and efficient testing methodologies.

- Cost and Time Efficiency: Simulation offers a significant reduction in costs and development time compared to physical testing.

- Ability to Simulate Rare and Hazardous Scenarios: Virtual environments allow for testing of critical edge cases that are difficult to reproduce in reality.

- Advancements in AI and Machine Learning: Enhancing the realism and intelligence of simulation platforms.

Barriers & Challenges:

- High Initial Investment: Sophisticated simulation software and hardware can require substantial upfront costs.

- Talent Gap: A shortage of skilled professionals with expertise in simulation and AV development.

- Validation and Correlation with Real-World Data: Ensuring simulation models accurately reflect real-world performance remains a challenge, particularly for complex sensor interactions.

- Cybersecurity Concerns: Protecting sensitive simulation data and intellectual property.

- Interoperability and Standardization: Lack of universal standards can create integration challenges between different simulation tools and hardware.

- Supply Chain Issues: Availability of specialized hardware components for HiL systems can sometimes pose a challenge.

- Regulatory Uncertainty: Evolving regulations can necessitate frequent updates to simulation methodologies.

Emerging Opportunities in Autonomous Vehicle AV Advanced Driver Assistance Systems (ADAS) Simulation Solution

Emerging opportunities lie in the expansion of cloud-based simulation platforms, offering enhanced scalability and collaborative development environments, making advanced simulation accessible to a broader range of companies. The development of digital twin technology for continuous validation throughout the vehicle lifecycle presents a significant avenue for growth. Furthermore, the increasing demand for simulation solutions for specific ADAS applications like driver monitoring systems, advanced parking assist, and pedestrian detection, as well as the growing interest in simulating sensor fusion algorithms and the impact of environmental factors (weather, lighting) on sensor performance, represent untapped market potential. The integration of AI for automated test case generation and scenario discovery is another promising area.

Growth Accelerators in the Autonomous Vehicle AV Advanced Driver Assistance Systems (ADAS) Simulation Solution Industry

Long-term growth in the AV/ADAS simulation market is being accelerated by breakthroughs in real-time rendering technologies, enabling more photorealistic and immersive virtual environments. Strategic partnerships between simulation providers, automotive OEMs, and sensor manufacturers are crucial for developing integrated and comprehensive validation solutions. The expansion of simulation capabilities to cover emerging areas like vehicle-to-everything (V2X) communication testing and cybersecurity threat simulation is also a key accelerator. Furthermore, market expansion into developing economies with growing automotive sectors and increasing focus on vehicle safety will drive sustained growth. The growing reliance on SiL for software validation and the increasing adoption of HiL for hardware integration are critical accelerators in the current landscape.

Key Players Shaping the Autonomous Vehicle AV Advanced Driver Assistance Systems (ADAS) Simulation Solution Market

- Siemens

- Dassault Systèmes

- ANSYS, Inc.

- Altair Engineering Inc.

- VI-grade GmbH

- Realtime Technologies

- Applied Intuition, Inc.

- Konrad Technologies (KT)

- EMERSON (N1)

- Claytex Services Ltd

- Keysight Technologies

- Amazon Web Services, Inc.

- Robert Bosch GmbH

- PTV Planning Transport Traffic GmbH

- Hexagon

- AB Dynamics plc (rFpro)

Notable Milestones in Autonomous Vehicle AV Advanced Driver Assistance Systems (ADAS) Simulation Solution Sector

- 2023: Introduction of advanced AI-driven scenario generation tools by Applied Intuition, Inc., enabling testing of millions of scenarios in days.

- 2023: Siemens announces enhanced integration of its Vires VTD simulation platform with its Simcenter suite, offering a more comprehensive digital twin for AV development.

- 2022: ANSYS releases upgraded sensor simulation capabilities, featuring enhanced fidelity for lidar and radar modeling to improve autonomous system validation.

- 2022: Dassault Systèmes expands its 3DEXPERIENCE platform with new simulation capabilities for complex AV perception systems.

- 2021: Altair Engineering Inc. acquires Inflemy, a specialist in autonomous driving simulation, to strengthen its offering in scenario generation and validation.

- 2021: VI-grade GmbH launches its Teleoperation Module for its driving simulators, enabling remote control and testing of autonomous vehicles.

- 2020: Keysight Technologies introduces new HiL testing solutions tailored for ADAS ECU validation, focusing on signal integrity and functional safety.

- 2019: Google's Waymo expands its simulation efforts, leveraging extensive real-world driving data to train and validate its autonomous driving system.

In-Depth Autonomous Vehicle AV Advanced Driver Assistance Systems (ADAS) Simulation Solution Market Outlook

The outlook for the AV/ADAS simulation solution market remains exceptionally strong, driven by the indispensable role of simulation in accelerating the safe and efficient development of autonomous vehicles. Key growth accelerators like advancements in AI for intelligent scenario generation and validation, coupled with the increasing adoption of cloud-based simulation platforms for enhanced accessibility and collaboration, will continue to fuel market expansion. Strategic partnerships and acquisitions will remain pivotal in consolidating offerings and addressing the end-to-end validation needs of the industry. The ongoing evolution of regulatory landscapes, alongside escalating consumer demand for advanced safety features, will further solidify the market's trajectory. The focus on HiL and SiL integration within comprehensive digital twin frameworks will be a significant strategic opportunity for players to capture market share and drive innovation in the highly dynamic autonomous driving ecosystem.

Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Segmentation

-

1. Application

- 1.1. Automobile Manufacturers

- 1.2. Autonomous Driving Technology Companies

- 1.3. ADAS Technology Providers

- 1.4. Others

-

2. Type

- 2.1. Hardware In The Loop (HiL)

- 2.2. Software In The Loop (SiL)

Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Regional Market Share

Geographic Coverage of Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution

Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Automobile Manufacturers

- 5.1.2. Autonomous Driving Technology Companies

- 5.1.3. ADAS Technology Providers

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Hardware In The Loop (HiL)

- 5.2.2. Software In The Loop (SiL)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Automobile Manufacturers

- 6.1.2. Autonomous Driving Technology Companies

- 6.1.3. ADAS Technology Providers

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Hardware In The Loop (HiL)

- 6.2.2. Software In The Loop (SiL)

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Automobile Manufacturers

- 7.1.2. Autonomous Driving Technology Companies

- 7.1.3. ADAS Technology Providers

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Hardware In The Loop (HiL)

- 7.2.2. Software In The Loop (SiL)

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Automobile Manufacturers

- 8.1.2. Autonomous Driving Technology Companies

- 8.1.3. ADAS Technology Providers

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Hardware In The Loop (HiL)

- 8.2.2. Software In The Loop (SiL)

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Automobile Manufacturers

- 9.1.2. Autonomous Driving Technology Companies

- 9.1.3. ADAS Technology Providers

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Hardware In The Loop (HiL)

- 9.2.2. Software In The Loop (SiL)

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Automobile Manufacturers

- 10.1.2. Autonomous Driving Technology Companies

- 10.1.3. ADAS Technology Providers

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Hardware In The Loop (HiL)

- 10.2.2. Software In The Loop (SiL)

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Siemens

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Dassault Systèmes

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 ANSYS Inc

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Altair Engineering Inc

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 VI-grade GmbH -

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Realtime Technologies

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Applied Intuition Inc.

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Google

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Konrad Technologies (KT)

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 EMERSON (N1)

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Claytex Services Ltd

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Keysight Technologies

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Amazon Web Services Inc.

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Robert Bosch GmbH

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 PTV Planning Transport Traffic GmbH

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Hexagon

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 AB Dynamics plc (rFpro)

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 Siemens

List of Figures

- Figure 1: Global Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million), by Application 2025 & 2033

- Figure 3: North America Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million), by Type 2025 & 2033

- Figure 5: North America Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million), by Country 2025 & 2033

- Figure 7: North America Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million), by Application 2025 & 2033

- Figure 9: South America Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million), by Type 2025 & 2033

- Figure 11: South America Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million), by Country 2025 & 2033

- Figure 13: South America Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution?

The projected CAGR is approximately 12.5%.

2. Which companies are prominent players in the Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution?

Key companies in the market include Siemens, Dassault Systèmes, ANSYS, Inc, Altair Engineering Inc, VI-grade GmbH -, Realtime Technologies, Applied Intuition, Inc., Google, Konrad Technologies (KT), EMERSON (N1), Claytex Services Ltd, Keysight Technologies, Amazon Web Services, Inc., Robert Bosch GmbH, PTV Planning Transport Traffic GmbH, Hexagon, AB Dynamics plc (rFpro).

3. What are the main segments of the Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 4340 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution?

To stay informed about further developments, trends, and reports in the Autonomous Vehicle Av Advanced Driver Assistance Systems Adas Simulation Solution, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence