Key Insights

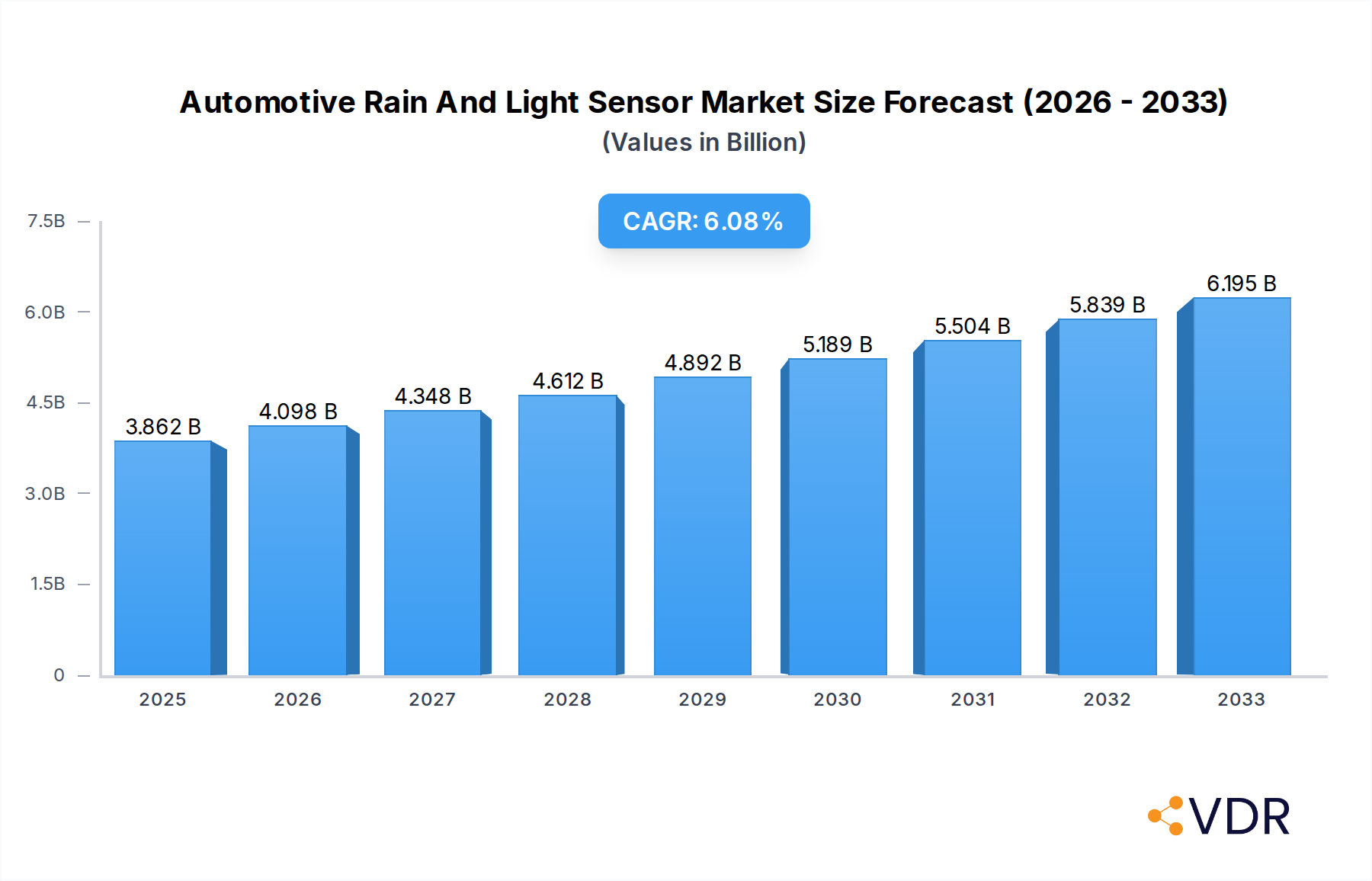

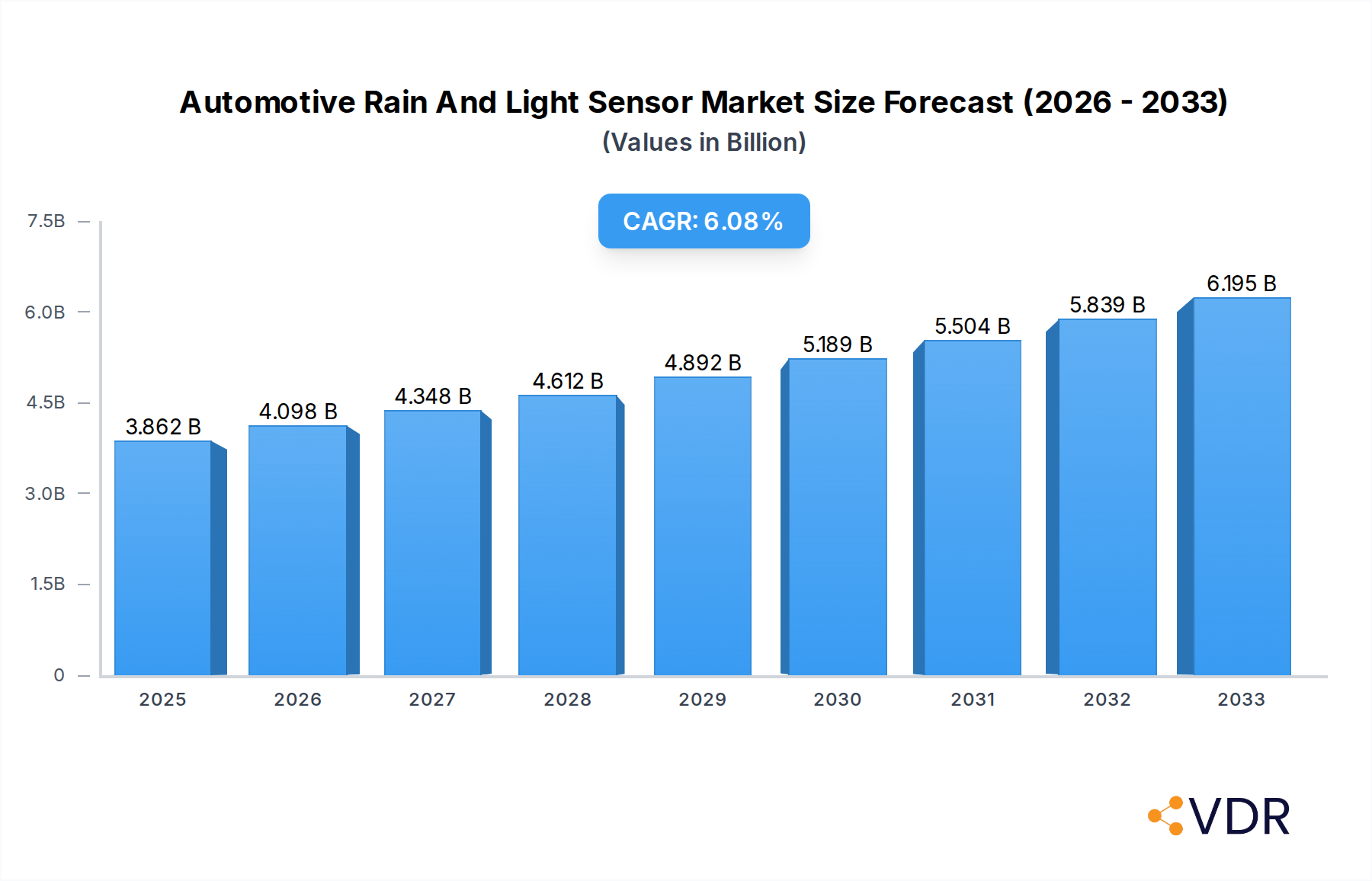

The global Automotive Rain and Light Sensor market is poised for significant expansion, projected to reach $3862 million by 2025 and demonstrating a robust Compound Annual Growth Rate (CAGR) of 6.2% from 2025 to 2033. This growth is primarily fueled by the increasing integration of advanced driver-assistance systems (ADAS) and the escalating demand for enhanced vehicle safety and convenience features. Modern vehicles are increasingly equipped with rain sensors to automate windshield wiper operation and light sensors to control headlights, improving visibility and reducing driver distraction in varying environmental conditions. This technological adoption is particularly pronounced in passenger cars, which represent a substantial segment of the market due to high production volumes and a growing consumer preference for premium, safety-conscious features. Furthermore, the commercial vehicle segment, including light commercial vehicles (LCVs) and heavy commercial vehicles (HCVs), is witnessing a steady rise in sensor adoption, driven by fleet operator demands for operational efficiency and compliance with evolving safety regulations.

Automotive Rain And Light Sensor Market Size (In Billion)

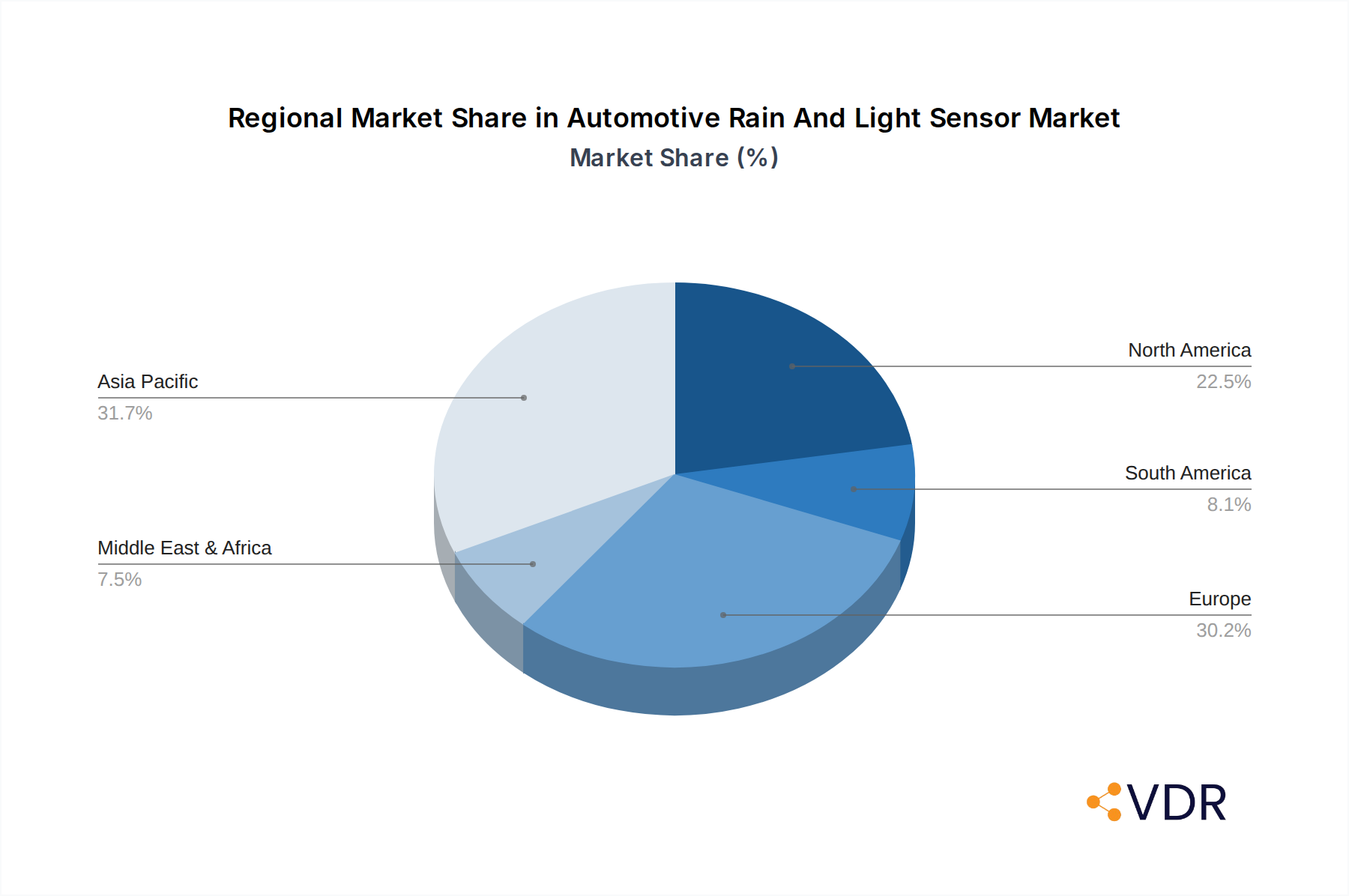

Emerging trends like the development of more sophisticated, multi-functional sensor arrays that combine rain and light detection, alongside other environmental sensing capabilities, are expected to further propel market growth. The increasing focus on autonomous driving technologies also necessitates highly reliable and accurate sensing systems, making rain and light sensors a critical component. While the market benefits from these advancements, certain restraints may temper its pace. These include the initial cost of sensor integration, particularly for budget-oriented vehicle models, and the ongoing need for recalibration or maintenance of these systems. However, declining component costs and advancements in manufacturing processes are likely to mitigate these challenges over the forecast period. Geographically, the Asia Pacific region, led by China and India, is expected to be a dominant force, driven by its massive automotive manufacturing base and growing consumer market. North America and Europe are also significant markets, owing to stringent safety standards and a high adoption rate of advanced vehicle technologies.

Automotive Rain And Light Sensor Company Market Share

Automotive Rain and Light Sensor Market: Comprehensive Growth Analysis & Future Outlook (2019-2033)

This report delivers an in-depth analysis of the global Automotive Rain and Light Sensor market, encompassing its dynamics, growth trajectories, regional dominance, product innovation, key drivers, emerging opportunities, and competitive landscape. With a study period spanning from 2019 to 2033, this comprehensive research provides critical insights for industry stakeholders. The base year for analysis is 2025, with a detailed forecast period from 2025 to 2033 and historical data from 2019 to 2024. This report will detail market size evolution, technological advancements, regulatory impacts, and competitive strategies, offering a robust foundation for strategic decision-making.

Automotive Rain And Light Sensor Market Dynamics & Structure

The Automotive Rain and Light Sensor market is characterized by moderate concentration, with a significant presence of established Tier-1 automotive suppliers and emerging Asian players. Technological innovation, particularly in sensor accuracy, integration capabilities, and cost reduction, serves as a primary driver. The increasing adoption of Advanced Driver-Assistance Systems (ADAS) and autonomous driving features is fueling demand for sophisticated rain and light sensing capabilities. Regulatory frameworks, such as mandates for automatic headlights and improved visibility for safety, are also indirectly influencing market growth. Competitive product substitutes are minimal, as these sensors fulfill distinct and essential functions within vehicle systems. End-user demographics are shifting towards a preference for vehicles with enhanced safety and convenience features, particularly among younger demographics and urban populations. Mergers and acquisitions (M&A) trends indicate consolidation among smaller players and strategic partnerships aimed at expanding product portfolios and market reach.

- Market Concentration: Moderate, with a mix of global Tier-1 suppliers and regional manufacturers.

- Technological Innovation Drivers: Enhanced accuracy, miniaturization, cost-effectiveness, AI integration for improved decision-making.

- Regulatory Frameworks: Indirect influence from ADAS mandates and vehicle safety standards.

- Competitive Product Substitutes: Limited, due to the specialized nature of sensor functions.

- End-User Demographics: Growing demand from younger, tech-savvy consumers and urban dwellers prioritizing safety and convenience.

- M&A Trends: Strategic acquisitions for technology integration and market expansion, with an estimated XX M&A deals in the historical period.

Automotive Rain And Light Sensor Growth Trends & Insights

The global Automotive Rain and Light Sensor market is poised for significant expansion, projected to witness a Compound Annual Growth Rate (CAGR) of XX% from 2025 to 2033. This robust growth is underpinned by several interconnected trends. The increasing penetration of passenger cars globally, especially in emerging economies, directly translates into a larger addressable market for these essential automotive components. Furthermore, the rising sophistication of vehicle features, driven by consumer demand for enhanced safety, comfort, and convenience, is a pivotal factor. Automatic headlight activation, adaptive lighting systems, and automatic wiper control are no longer considered luxury features but are becoming standard in a growing number of vehicle segments. The integration of rain and light sensors with other ADAS components, such as cameras and radar, is creating synergistic opportunities, enabling more advanced functionalities like intelligent windshield wiper control based on precipitation intensity and predictive lighting adjustments for enhanced visibility in diverse driving conditions.

Technological disruptions are also playing a crucial role. Advancements in sensor technology, including the development of more compact, power-efficient, and cost-effective solutions, are making these systems more accessible for integration across a wider range of vehicle models, including mid-range and compact cars. The evolution of optical sensors, incorporating machine learning algorithms for better environmental perception, is further enhancing their performance and reliability. Consumer behavior shifts are also contributing to the market's upward trajectory. There is a discernible increase in consumer awareness and expectation regarding vehicle safety features. As vehicles become more connected and intelligent, consumers are actively seeking out models equipped with advanced sensing technologies that contribute to a safer and more comfortable driving experience. This growing preference for smart automotive features acts as a direct catalyst for the adoption of rain and light sensors. The market penetration of these sensors is projected to reach XX% by 2033, a significant increase from the XX% in 2024.

The increasing complexity of automotive electronics and the demand for integrated solutions are also driving innovation in sensor packaging and connectivity. Manufacturers are focusing on developing sensors that are easily integrated into the vehicle's existing electrical architecture, reducing installation complexity and cost. The rising trend of vehicle electrification, while not directly impacting the core functionality of these sensors, is indirectly benefiting the market by increasing the overall technological sophistication of electric vehicles, which are often equipped with advanced features. The forecast suggests that the market size will grow from approximately $XX billion in 2025 to an estimated $XX billion by 2033, driven by these multifaceted trends.

Dominant Regions, Countries, or Segments in Automotive Rain And Light Sensor

The Passenger Car (PC) segment stands as the dominant force within the global Automotive Rain and Light Sensor market, accounting for an estimated XX% of the total market revenue in 2025. This dominance is primarily attributed to the sheer volume of passenger vehicles manufactured and sold worldwide. The growing middle class in emerging economies, coupled with increasing disposable incomes, fuels the demand for new passenger cars, consequently driving the adoption of advanced features like automatic rain and light sensors. The shift towards feature-rich vehicles as a standard offering in many markets further solidifies the Passenger Car segment's leadership.

Geographically, Asia Pacific is emerging as the most influential region, projected to account for approximately XX% of the global market share by 2033. This leadership is fueled by the region's robust automotive manufacturing base, particularly in China and India, which are the world's largest automotive markets. Favorable government policies promoting domestic manufacturing, coupled with significant investments in research and development by local and international automotive players, are key drivers. The increasing adoption of ADAS technologies in Chinese passenger vehicles, driven by both consumer demand and government initiatives for road safety, is a major growth accelerator.

Within Asia Pacific, China is the standout country, representing an estimated XX% of the regional market. The country's massive vehicle production, coupled with a rapidly expanding aftermarket for automotive electronics, positions it as a critical hub for rain and light sensor adoption. The government's emphasis on technological advancement in the automotive sector and the strong presence of indigenous sensor manufacturers like CETC Motor and Hirain are further bolstering China's dominance.

- Dominant Segment: Passenger Car (PC), driven by high production volumes and increasing feature mandates.

- Leading Region: Asia Pacific, owing to its vast manufacturing capabilities and growing consumer market.

- Key Country: China, with its immense vehicle production and strong domestic sensor industry.

- Drivers for PC Dominance: High vehicle sales, increasing adoption of convenience and safety features, regulatory push for ADAS.

- Drivers for Asia Pacific Leadership: Robust manufacturing ecosystem, growing middle class, supportive government policies, increasing R&D investments.

- Drivers for China's Dominance: Largest automotive market, rapid technological integration, significant domestic players, government support for innovation.

Automotive Rain And Light Sensor Product Landscape

Automotive rain and light sensors are witnessing continuous product innovation focused on enhanced performance and seamless integration. Modern sensors utilize advanced optical technologies to accurately detect precipitation intensity and ambient light levels, enabling features such as automatic windshield wipers and adaptive headlights. Innovations include smaller form factors for discreet integration, improved temperature and humidity resistance for increased durability, and the development of multi-functional sensors that combine rain and light sensing capabilities with other environmental perception tasks. The unique selling proposition lies in their ability to automate critical driving functions, thereby enhancing driver safety and comfort by adapting vehicle systems to changing environmental conditions without manual intervention. Technological advancements are also focusing on increasing the processing power within the sensor module, allowing for more intelligent data interpretation and faster response times.

Key Drivers, Barriers & Challenges in Automotive Rain And Light Sensor

Key Drivers:

- Increasing Adoption of ADAS: The growing integration of Advanced Driver-Assistance Systems (ADAS) in vehicles necessitates advanced sensing capabilities, with rain and light sensors being foundational components.

- Enhanced Vehicle Safety and Comfort: Consumer demand for improved driving experiences, prioritizing safety and convenience, directly fuels the adoption of these automated features.

- Technological Advancements: Continuous innovation in sensor technology, leading to more accurate, reliable, and cost-effective solutions, broadens market accessibility.

- Regulatory Mandates: Government regulations and safety standards promoting automatic lighting and improved visibility further drive demand.

- Growth in Automotive Production: Overall expansion of global automotive production, particularly in emerging markets, provides a larger installed base for these sensors.

Key Barriers & Challenges:

- Cost Sensitivity: While costs are decreasing, the initial investment for sensor integration can still be a barrier for some entry-level vehicle segments.

- Supply Chain Volatility: Global supply chain disruptions, particularly for electronic components, can impact production and availability.

- Integration Complexity: The need for seamless integration with existing vehicle electronics can pose technical challenges for some manufacturers.

- Competition from Lower-Cost Alternatives: While direct substitutes are limited, intense competition among sensor manufacturers can lead to price pressures.

- Consumer Awareness and Education: In some markets, a lack of full consumer understanding of the benefits can hinder adoption.

Emerging Opportunities in Automotive Rain And Light Sensor

Emerging opportunities in the Automotive Rain and Light Sensor market lie in the development of more sophisticated, integrated sensing solutions. The expansion of these sensors into next-generation autonomous driving systems, where they will play a crucial role in environmental perception and sensor fusion, presents a significant growth avenue. The development of smart windshields that incorporate these sensors directly into the glass offers a more streamlined and aesthetically pleasing integration. Furthermore, the growing demand for connected car features presents opportunities for sensors to contribute data to cloud-based platforms, enabling predictive maintenance and enhanced traffic management systems. Untapped markets in developing regions with improving automotive infrastructure also represent fertile ground for market expansion.

Growth Accelerators in the Automotive Rain And Light Sensor Industry

Growth accelerators for the Automotive Rain and Light Sensor industry are predominantly technology-driven and market-demand-fueled. The relentless pursuit of higher levels of vehicle automation, from Level 2+ to Level 4 autonomy, will significantly boost the requirement for highly accurate and redundant sensing systems. Strategic partnerships between sensor manufacturers and major automotive OEMs are crucial for co-development and faster integration of advanced sensor technologies into new vehicle platforms. Market expansion strategies focused on addressing the needs of emerging economies, where vehicle electrification and smart features are gaining traction, will also serve as significant growth catalysts. The increasing focus on in-cabin sensing capabilities, such as detecting driver distraction or fatigue, could also pave the way for integrated sensor solutions that extend beyond traditional rain and light detection.

Key Players Shaping the Automotive Rain And Light Sensor Market

- TRW

- Mitsubishi Motors

- Volkswagen

- Hella

- AUDI AG.

- BMW

- Kostal Group

- Panasonic

- Osram GmbH

- ROHM

- Sensata

- CETC Motor

- Hirain

- G-Pulse

- Startway

- Kenchuang

- Yichenglong

Notable Milestones in Automotive Rain And Light Sensor Sector

- 2019: Increased integration of multi-function sensors combining rain and light detection in premium passenger vehicles.

- 2020: Advancements in optical sensor technology leading to improved accuracy and reduced susceptibility to environmental interference.

- 2021: Growing adoption of rain-sensing technology in mid-range passenger vehicles, driven by feature democratization.

- 2022: Increased focus on cost reduction and miniaturization of sensor components to cater to a wider range of automotive segments.

- 2023: Significant R&D investment in developing AI-powered algorithms for enhanced sensor interpretation and predictive capabilities.

- 2024: Emergence of specialized sensor solutions for electric vehicles, focusing on integration with advanced battery management and energy-efficient lighting systems.

In-Depth Automotive Rain And Light Sensor Market Outlook

The future outlook for the Automotive Rain and Light Sensor market is exceptionally promising, driven by an unyielding demand for enhanced vehicle safety, comfort, and the relentless march towards autonomous driving. Growth accelerators such as the integration of these sensors into sophisticated ADAS suites, enabling proactive environmental adaptation and advanced driver assistance, will be paramount. The expansion of these sensing capabilities into emerging markets, coupled with the continuous drive for technological innovation that leads to more integrated and cost-effective solutions, will fuel sustained market expansion. Strategic alliances between key players and a proactive approach to evolving consumer preferences will be critical for capitalizing on the vast future potential and securing a competitive edge in this dynamic sector. The market is well-positioned for significant growth in the coming years.

Automotive Rain And Light Sensor Segmentation

-

1. Application

- 1.1. Passenger Car (PC)

- 1.2. Commercial Vehicle (LCV)

- 1.3. Heavy Commercial Vehicle (HCV)

-

2. Type

- 2.1. Rain Sensor

- 2.2. Light Sensor

Automotive Rain And Light Sensor Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Rain And Light Sensor Regional Market Share

Geographic Coverage of Automotive Rain And Light Sensor

Automotive Rain And Light Sensor REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Rain And Light Sensor Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Car (PC)

- 5.1.2. Commercial Vehicle (LCV)

- 5.1.3. Heavy Commercial Vehicle (HCV)

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Rain Sensor

- 5.2.2. Light Sensor

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automotive Rain And Light Sensor Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Car (PC)

- 6.1.2. Commercial Vehicle (LCV)

- 6.1.3. Heavy Commercial Vehicle (HCV)

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Rain Sensor

- 6.2.2. Light Sensor

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automotive Rain And Light Sensor Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Car (PC)

- 7.1.2. Commercial Vehicle (LCV)

- 7.1.3. Heavy Commercial Vehicle (HCV)

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Rain Sensor

- 7.2.2. Light Sensor

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive Rain And Light Sensor Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Car (PC)

- 8.1.2. Commercial Vehicle (LCV)

- 8.1.3. Heavy Commercial Vehicle (HCV)

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Rain Sensor

- 8.2.2. Light Sensor

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automotive Rain And Light Sensor Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Car (PC)

- 9.1.2. Commercial Vehicle (LCV)

- 9.1.3. Heavy Commercial Vehicle (HCV)

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Rain Sensor

- 9.2.2. Light Sensor

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automotive Rain And Light Sensor Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Car (PC)

- 10.1.2. Commercial Vehicle (LCV)

- 10.1.3. Heavy Commercial Vehicle (HCV)

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Rain Sensor

- 10.2.2. Light Sensor

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 TRW

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Mitsubishi Motors

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Volkswagen

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Hella

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 AUDI AG.

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 BMW

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Kostal Group

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Panasonic

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Osram GmbH

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 ROHM

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Sensata

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 CETC Motor

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Hirain

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 G-Pulse

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Startway

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Kenchuang

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Yichenglong

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 TRW

List of Figures

- Figure 1: Global Automotive Rain And Light Sensor Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Rain And Light Sensor Revenue (million), by Application 2025 & 2033

- Figure 3: North America Automotive Rain And Light Sensor Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Rain And Light Sensor Revenue (million), by Type 2025 & 2033

- Figure 5: North America Automotive Rain And Light Sensor Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Automotive Rain And Light Sensor Revenue (million), by Country 2025 & 2033

- Figure 7: North America Automotive Rain And Light Sensor Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Rain And Light Sensor Revenue (million), by Application 2025 & 2033

- Figure 9: South America Automotive Rain And Light Sensor Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Rain And Light Sensor Revenue (million), by Type 2025 & 2033

- Figure 11: South America Automotive Rain And Light Sensor Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Automotive Rain And Light Sensor Revenue (million), by Country 2025 & 2033

- Figure 13: South America Automotive Rain And Light Sensor Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Rain And Light Sensor Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Automotive Rain And Light Sensor Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Rain And Light Sensor Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Automotive Rain And Light Sensor Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Automotive Rain And Light Sensor Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Automotive Rain And Light Sensor Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Rain And Light Sensor Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Rain And Light Sensor Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Rain And Light Sensor Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Automotive Rain And Light Sensor Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Automotive Rain And Light Sensor Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Rain And Light Sensor Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Rain And Light Sensor Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Rain And Light Sensor Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Rain And Light Sensor Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Automotive Rain And Light Sensor Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Automotive Rain And Light Sensor Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Rain And Light Sensor Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Rain And Light Sensor Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Rain And Light Sensor Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Automotive Rain And Light Sensor Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Rain And Light Sensor Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Rain And Light Sensor Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Automotive Rain And Light Sensor Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Rain And Light Sensor Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Rain And Light Sensor Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Automotive Rain And Light Sensor Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Rain And Light Sensor Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Rain And Light Sensor Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Automotive Rain And Light Sensor Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Rain And Light Sensor Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Rain And Light Sensor Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Automotive Rain And Light Sensor Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Rain And Light Sensor Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Rain And Light Sensor Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Automotive Rain And Light Sensor Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Rain And Light Sensor Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Rain And Light Sensor?

The projected CAGR is approximately 6.2%.

2. Which companies are prominent players in the Automotive Rain And Light Sensor?

Key companies in the market include TRW, Mitsubishi Motors, Volkswagen, Hella, AUDI AG., BMW, Kostal Group, Panasonic, Osram GmbH, ROHM, Sensata, CETC Motor, Hirain, G-Pulse, Startway, Kenchuang, Yichenglong.

3. What are the main segments of the Automotive Rain And Light Sensor?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 3862 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Rain And Light Sensor," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Rain And Light Sensor report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Rain And Light Sensor?

To stay informed about further developments, trends, and reports in the Automotive Rain And Light Sensor, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence