Key Insights

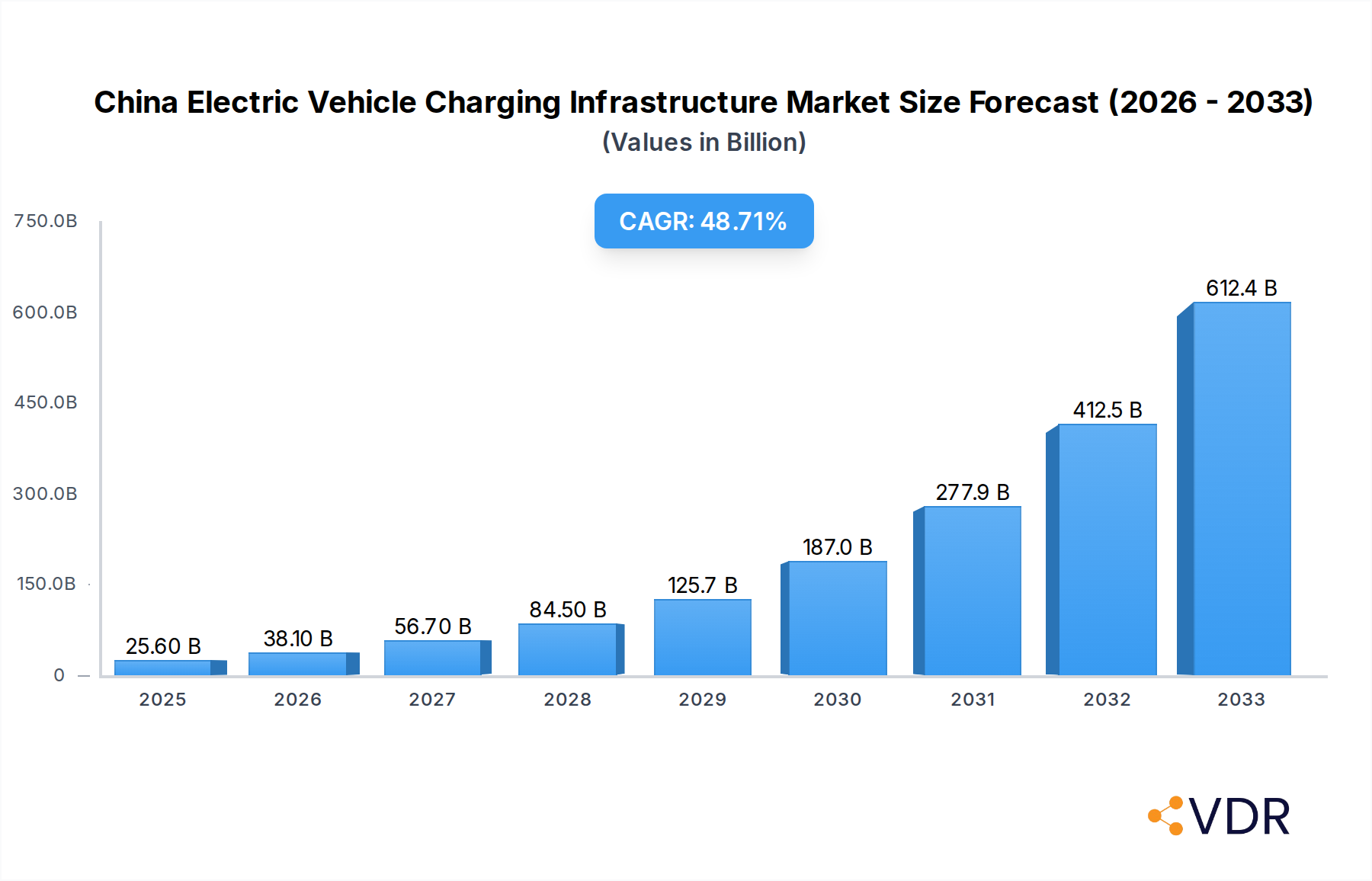

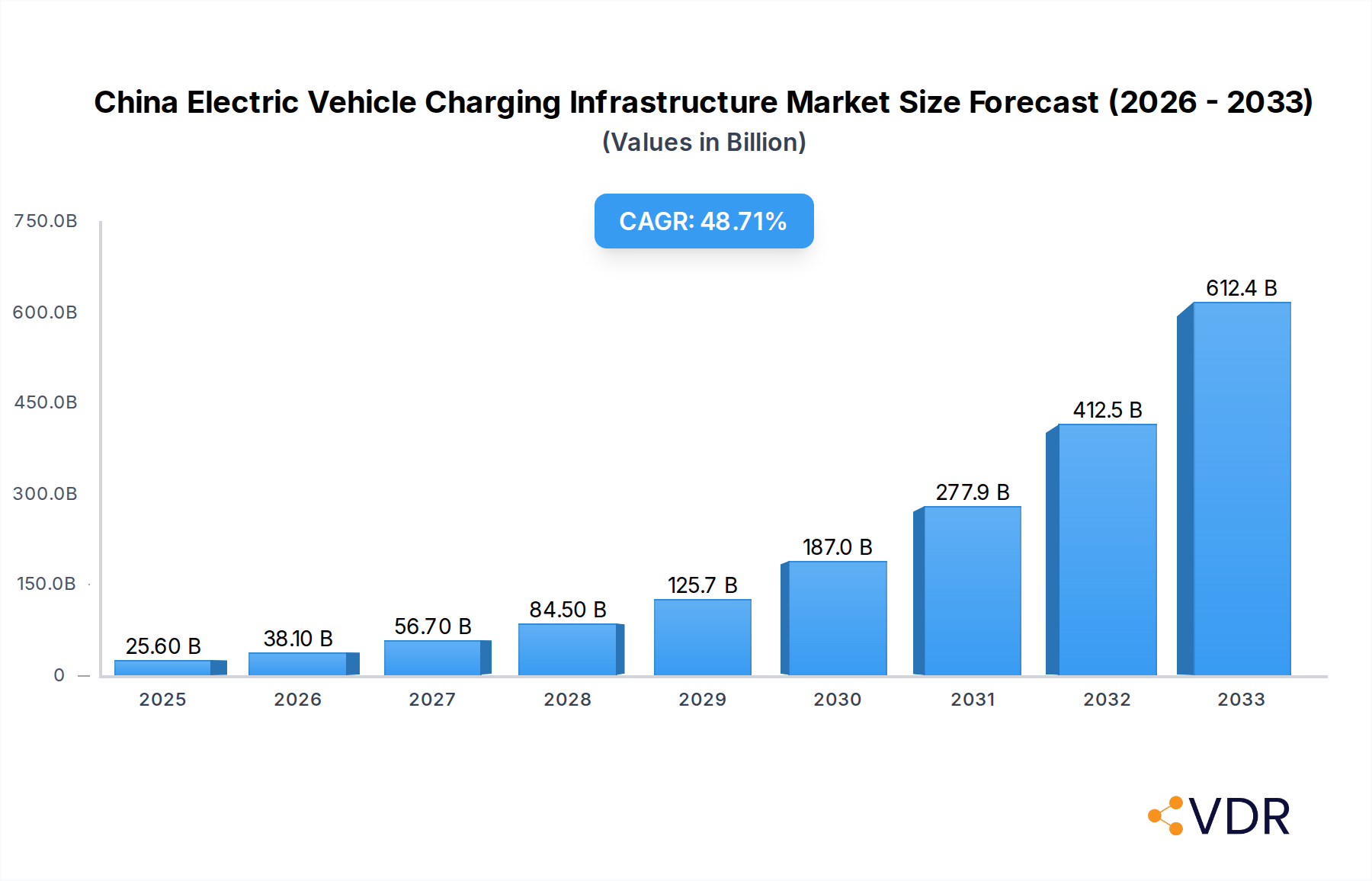

The China Electric Vehicle (EV) Charging Infrastructure Market is poised for explosive growth, projected to reach a market size of $25.6 billion in 2025, driven by an unprecedented CAGR of 48.56% throughout the forecast period. This remarkable expansion is primarily fueled by the nation's aggressive push towards electric mobility, supported by strong government policies, substantial subsidies, and a rapidly growing EV user base. The burgeoning demand for both passenger and commercial EVs necessitates a corresponding surge in charging solutions, making charging stations the linchpin of China's sustainable transportation ecosystem. Key drivers include technological advancements in charging speed and efficiency, the increasing adoption of smart charging solutions, and the expansion of grid capacity to support widespread EV charging. The market's segmentation reveals a dynamic landscape with both Alternating Current (AC) and Direct Current (DC) charging stations playing crucial roles, catering to diverse user needs across private and public infrastructures.

China Electric Vehicle Charging Infrastructure Market Market Size (In Billion)

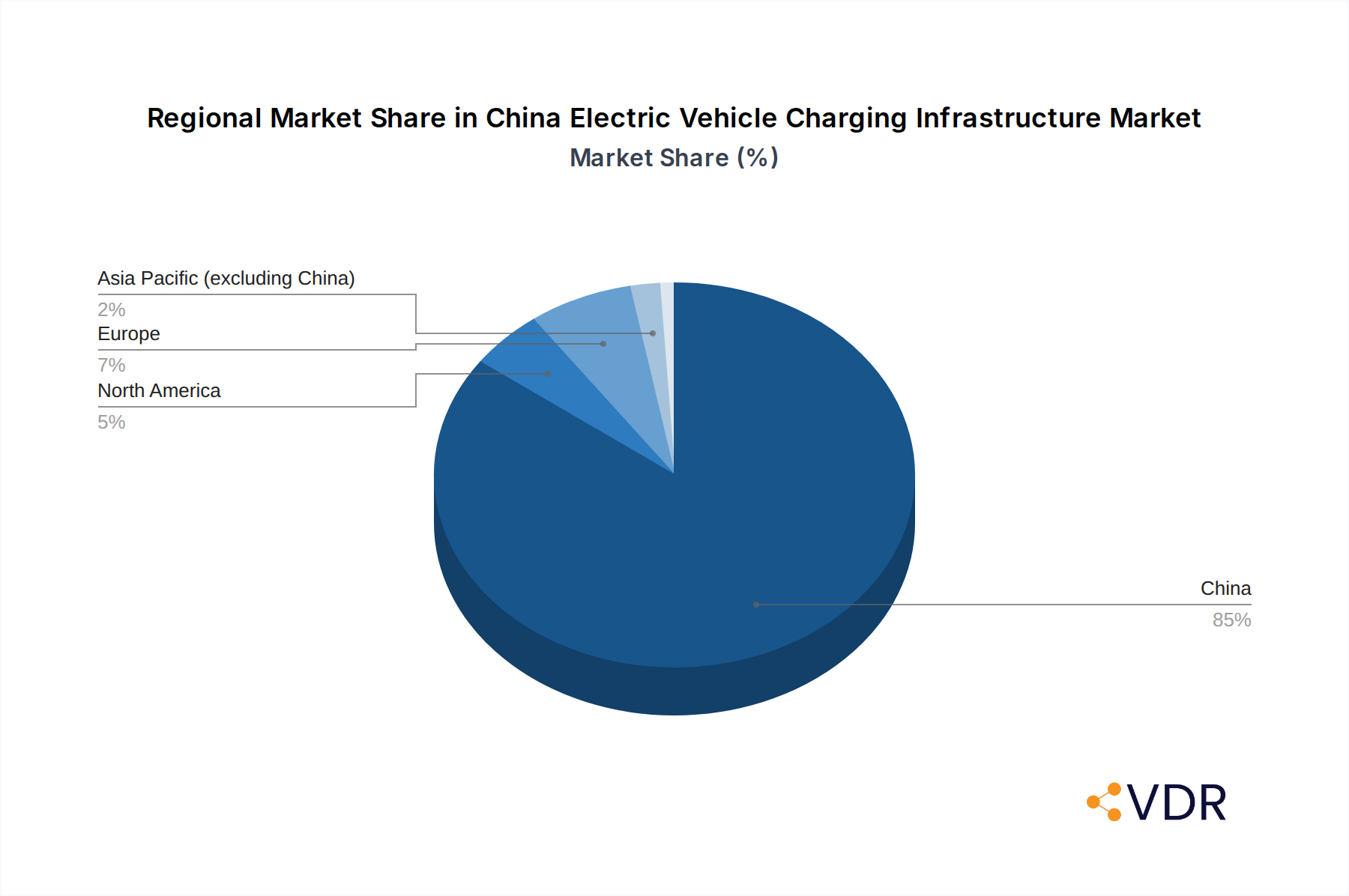

The sheer scale of China's automotive market, combined with its leadership in EV production and adoption, positions it as the dominant force in the global EV charging infrastructure arena. The market is characterized by intense competition among a multitude of players, from established state-owned enterprises like State Grid Corporation of China and Southern Power Grid to innovative private companies such as TELD, TGood, and Starcharge. The strategic expansion of charging networks, both in urban centers and along major transportation routes, is a critical trend. While the rapid growth presents immense opportunities, challenges such as ensuring grid stability, standardizing charging protocols, and addressing the upfront investment costs for infrastructure deployment remain areas of focus. Nonetheless, the overwhelming momentum towards electrification, underscored by the robust CAGR, suggests that China will continue to lead the world in EV charging infrastructure development and deployment for the foreseeable future.

China Electric Vehicle Charging Infrastructure Market Company Market Share

China Electric Vehicle Charging Infrastructure Market: Comprehensive Market Analysis & Future Outlook (2019-2033)

Report Description:

Dive deep into the booming China Electric Vehicle (EV) Charging Infrastructure Market with this definitive analysis. Covering the extensive 2019–2033 period, with a base year of 2025, this report offers unparalleled insights into market dynamics, growth trends, competitive landscapes, and future opportunities. As China solidifies its position as a global leader in EV adoption, understanding its robust charging ecosystem is paramount. This report dissects the market by Charging Station Type (AC and DC), Vehicle Type (Passenger and Commercial), and User Application (Private and Public Infrastructure), providing a granular view of demand and expansion.

With an estimated market size projected to reach $XX billion by 2033, driven by supportive government policies, technological advancements, and escalating consumer demand for sustainable mobility, this research is essential for stakeholders seeking to capitalize on this dynamic sector. We analyze the strategic moves of key players like EV Power, YKC, State Grid Corporation of China, Eichong, TELD, TGood, Evking, Wancheng Wanchong, Starcharge, SAIC Motor, Potevio, Southern Power Grid, ShenZhen Carenergy Net, Hooenergy, and Winland, alongside industry developments such as PetroChina's acquisition of Potevio New Energy Co Ltd. Uncover the future trajectory of China's EV charging network and identify key growth accelerators, barriers, and emerging opportunities.

China Electric Vehicle Charging Infrastructure Market Market Dynamics & Structure

The China EV Charging Infrastructure Market is characterized by rapid expansion and increasing sophistication, driven by a strong interplay of technological innovation and robust regulatory support. Market concentration is gradually evolving, with dominant state-owned enterprises and a growing number of private players vying for market share. Technological innovation is a key differentiator, focusing on faster charging speeds, enhanced grid integration, and the development of smart charging solutions. Regulatory frameworks, including national targets for EV adoption and charging station deployment, provide a consistent and favorable environment for investment. Competitive product substitutes are minimal, as the fundamental need for charging infrastructure is essential for EV operation. End-user demographics are diverse, ranging from individual car owners to fleet operators and public transportation providers, each with distinct charging needs. Mergers and acquisitions (M&A) are becoming increasingly prevalent as companies seek to consolidate their market positions and expand their service offerings. For instance, the acquisition of Potevio by PetroChina underscores the strategic importance of the EV charging market for established energy giants.

- Market Concentration: Evolving landscape with both large state-owned entities and agile private sector players.

- Technological Innovation Drivers: Focus on faster charging (DC), smart grid integration, V2G capabilities, and user-friendly interfaces.

- Regulatory Frameworks: Government mandates for EV sales and charging point deployment, subsidies, and standardization initiatives.

- Competitive Product Substitutes: Limited direct substitutes, as charging is an intrinsic requirement for EVs.

- End-User Demographics: Diverse, including individual consumers, corporate fleets, ride-sharing services, and public transit.

- M&A Trends: Increasing consolidation and strategic partnerships to gain market share and technological capabilities.

China Electric Vehicle Charging Infrastructure Market Growth Trends & Insights

The China Electric Vehicle Charging Infrastructure Market is experiencing exponential growth, fueled by a confluence of powerful market drivers. The overarching trend is the dramatic increase in EV adoption rates across the nation, directly translating into a burgeoning demand for accessible and efficient charging solutions. As of the base year 2025, the market is projected to reach an estimated $XX billion, a significant leap from historical figures and a strong indicator of future potential. This growth is further propelled by continuous technological disruptions in charging hardware and software, leading to faster charging times, enhanced grid stability, and more integrated user experiences. Consumer behavior is rapidly shifting towards electric mobility, with increased awareness of environmental benefits, lower running costs, and the expanding availability of EV models. The government's ambitious targets for NEV penetration and its sustained investment in charging infrastructure development form the bedrock of this expansion.

The compound annual growth rate (CAGR) for the forecast period of 2025–2033 is expected to remain robust, driven by ongoing urbanization and the strategic placement of charging facilities in both urban centers and along major transportation arteries, including expressways. Insights from the June 2023 development, where China successfully installed 18,590 charging stations across highways, highlight the scale of infrastructure expansion. Furthermore, the identification of 27,000 parking spots reserved for charging stations underscores a proactive approach to overcoming range anxiety and facilitating widespread EV usage. The average market penetration of EVs, closely tied to charging infrastructure availability, is projected to climb significantly, creating a virtuous cycle of demand and supply. Key segments, such as DC Charging Stations for rapid replenishment and Public Infrastructure for convenience, are witnessing accelerated development. The focus on passenger vehicles continues to dominate, but the increasing electrification of commercial fleets presents a substantial secondary growth avenue. The market's trajectory is marked by a steady increase in the number of charging points, from XX million in 2019 to an estimated XX million by 2033, reflecting a critical expansion of the charging network. This sustained growth is indicative of a maturing market that is moving beyond initial adoption challenges to widespread integration.

Dominant Regions, Countries, or Segments in China Electric Vehicle Charging Infrastructure Market

Within the expansive China Electric Vehicle Charging Infrastructure Market, several regions, countries, and segments are demonstrating exceptional leadership and driving overall growth. While the entire nation is a key market, Eastern China consistently emerges as a dominant region. This dominance is attributed to a confluence of factors including a high concentration of major metropolitan areas like Shanghai and Beijing, a higher per capita income leading to greater EV purchasing power, and a more mature and proactive approach to adopting new technologies and sustainable infrastructure. The presence of major economic hubs fosters a robust demand for both Passenger Vehicles and Commercial Vehicles, necessitating a comprehensive charging network.

- Dominant Region: Eastern China

- Key Drivers: High population density, strong economic development, significant EV adoption rates, and advanced urban planning initiatives.

- Market Share: Eastern China accounts for an estimated XX% of the national charging infrastructure market share, with cities like Shanghai and Hangzhou leading in per capita charging points.

- Growth Potential: Continued investment in smart grid technology and the expansion of charging facilities in emerging smart cities within the region.

Segment-wise analysis reveals the crucial role of Direct Current (DC) Charging Stations. While Alternating Current (AC) charging remains prevalent for residential and overnight charging, the demand for faster charging solutions, particularly in public spaces and along highways, is rapidly propelling the growth of DC charging. This is directly linked to the increasing range of EVs and the need for quick top-ups during longer journeys or for commercial vehicle operations.

- Dominant Segment (Charging Station Type): Direct Current (DC) Charging Station

- Key Drivers: Faster charging times crucial for convenience and reducing range anxiety, supporting the operational efficiency of commercial fleets, and government incentives for high-power charging infrastructure.

- Market Share: DC charging stations are projected to capture an increasing share, estimated at XX% of the total charging points by 2033, driven by technological advancements and consumer preference for speed.

- Growth Potential: Expansion along expressways and in high-traffic urban areas, as well as integration with renewable energy sources to power these stations.

The Private Infrastructure segment, encompassing charging solutions installed at residential complexes and workplaces, is also a significant growth engine. However, the sheer scale of government-led deployment and the critical need for widespread public access make Public Infrastructure a segment with immense and sustained growth potential. The Chinese government's commitment to building a ubiquitous charging network ensures that public charging stations will continue to be a focal point of development, serving a broad spectrum of users.

- Dominant Segment (User Application): Public Infrastructure

- Key Drivers: Government mandates for widespread accessibility, support for public transportation and ride-sharing fleets, and the need to alleviate range anxiety for a larger population.

- Market Share: Public charging infrastructure is expected to represent a significant portion of the market, with an estimated XX% of total charging points by 2033, reflecting a sustained national effort.

- Growth Potential: Continued deployment in urban centers, highway service areas, and commercial districts, with an increasing emphasis on smart features and grid integration.

In terms of Vehicle Type, Passenger Vehicles remain the primary driver of charging infrastructure demand due to their sheer volume in the EV market. However, the electrification of logistics and public transport is steadily increasing the importance of charging solutions for Commercial Vehicles, presenting a significant growth opportunity for specialized charging infrastructure.

China Electric Vehicle Charging Infrastructure Market Product Landscape

The product landscape within the China Electric Vehicle Charging Infrastructure Market is rapidly innovating, focusing on enhancing user experience and operational efficiency. Key product developments include the proliferation of high-power DC fast chargers, capable of delivering significant range in minutes, and the integration of smart charging technologies that optimize energy consumption and grid load. Furthermore, manufacturers are focusing on modular designs for easier maintenance and scalability, as well as the development of integrated payment and management systems for seamless operation. The performance metrics of charging stations are continuously improving, with higher charging speeds, greater reliability, and enhanced safety features becoming standard. Unique selling propositions often revolve around the speed of charging, the intelligence of the charging management system, and the overall cost-effectiveness for operators and end-users.

Key Drivers, Barriers & Challenges in China Electric Vehicle Charging Infrastructure Market

The rapid expansion of China's EV charging infrastructure is propelled by several key drivers. Foremost among these is the strong and consistent governmental support, manifested through ambitious national targets for EV adoption and dedicated policies for charging infrastructure development. Technological advancements in battery technology and charging hardware are also critical, enabling faster, more efficient, and more affordable charging solutions. The growing consumer demand for EVs, driven by environmental consciousness, government incentives, and decreasing operational costs, further fuels the need for robust charging networks. Economic factors, such as the declining cost of renewable energy, also contribute to the viability and sustainability of charging infrastructure.

- Key Drivers:

- Government Policies and Targets for NEV Adoption.

- Technological Advancements in Charging Speed and Efficiency.

- Increasing Consumer Demand for Electric Vehicles.

- Economic Viability with Declining Renewable Energy Costs.

However, the market faces significant barriers and challenges. The substantial upfront investment required for deploying widespread charging infrastructure remains a hurdle, particularly for remote or less populated areas. Grid capacity limitations in certain regions can constrain the deployment of high-power charging stations and impact grid stability. Regulatory complexities and evolving standards can also create uncertainty for investors and operators. Supply chain issues for critical components can lead to delays and increased costs, while intense competition among a growing number of players can impact profitability. Furthermore, the need for widespread public acceptance and education regarding EV charging etiquette and availability continues to be an ongoing effort.

- Key Barriers & Challenges:

- High Capital Investment for Infrastructure Deployment.

- Grid Capacity and Stability Concerns.

- Evolving Regulatory Landscape and Standardization Issues.

- Supply Chain Volatility for Components.

- Intense Market Competition.

- Public Awareness and Behavioral Adoption.

Emerging Opportunities in China Electric Vehicle Charging Infrastructure Market

Emerging opportunities in the China EV Charging Infrastructure Market lie in several key areas. The integration of charging infrastructure with renewable energy sources, such as solar and wind power, presents a significant opportunity for sustainable and cost-effective charging. The development of Vehicle-to-Grid (V2G) technology, allowing EVs to feed power back into the grid, opens up new revenue streams and enhances grid flexibility. Furthermore, the expansion of charging networks into less developed rural areas and along less-traveled highways represents a significant untapped market. Innovative business models, such as battery swapping stations and subscription-based charging services, are also gaining traction, catering to diverse user needs and preferences. The increasing adoption of autonomous vehicles will also necessitate new charging solutions tailored for unmanned operation.

Growth Accelerators in the China Electric Vehicle Charging Infrastructure Market Industry

Several catalysts are accelerating the long-term growth of the China Electric Vehicle Charging Infrastructure Market. Continuous technological breakthroughs in battery technology, leading to longer EV ranges and faster charging times, directly reduce range anxiety and encourage EV adoption. Strategic partnerships between charging infrastructure providers, automakers, and energy companies are crucial for expanding reach and integrating charging solutions into the broader energy ecosystem. Market expansion strategies, including the development of intelligent charging networks that incorporate AI for predictive maintenance and optimized energy management, are further enhancing the efficiency and attractiveness of EV ownership. The ongoing commitment to building smart cities with integrated sustainable transportation solutions will also provide a continuous impetus for charging infrastructure development.

Key Players Shaping the China Electric Vehicle Charging Infrastructure Market Market

- EV Power

- YKC

- State Grid Corporation of China

- Eichong

- TELD

- TGood

- Evking

- Wancheng Wanchong

- Starcharge

- SAIC Motor

- Potevio

- Southern Power Grid

- ShenZhen Carenergy Net

- Hooenergy

- Winland

Notable Milestones in China Electric Vehicle Charging Infrastructure Market Sector

- September 2023: PetroChina acquired Potevio New Energy Co Ltd, signaling a major strategic move by an oil and gas giant to establish a strong presence in China's burgeoning EV charging market. By the end of 2021, Potevio had already established itself with 50,000 charging points across over 50 cities, demonstrating significant operational capacity.

- June 2023: The Chinese government announced its continued commitment to expanding charging facilities along national expressways for new energy vehicles (NEVs). Authorities reported the successful installation of 18,590 charging stations on highways and identified 27,000 parking spots exclusively for EV charging stations nationwide, underscoring a significant infrastructure build-out.

- November 2022: Audi launched its premium charging stations in China as part of its "Vorsprung 2030 China Strategy." By the close of 2022, 20 stations were operational in major cities like Beijing, Shanghai, Guangzhou, and Shenzhen, with plans for further expansion to more cities and locations.

In-Depth China Electric Vehicle Charging Infrastructure Market Market Outlook

The future outlook for the China Electric Vehicle Charging Infrastructure Market is exceptionally promising, characterized by sustained growth and significant strategic evolution. The continued commitment from both government and private sectors to electrify transportation ensures a robust pipeline of investment in charging infrastructure. Growth accelerators such as advancements in battery technology leading to longer ranges and faster charging, coupled with the increasing integration of smart grid technologies and renewable energy sources, will further enhance the appeal and efficiency of EV ownership. Emerging opportunities in areas like V2G technology and expansion into rural markets present substantial untapped potential. Strategic partnerships and innovative business models will play a pivotal role in shaping a more connected, intelligent, and sustainable charging ecosystem, solidifying China's position as a global leader in electric mobility.

China Electric Vehicle Charging Infrastructure Market Segmentation

-

1. Charging Station Type

- 1.1. Alternating Current (AC) Charging Station

- 1.2. Direct Current (DC) Charging Station

-

2. Vehicle Type

- 2.1. Passenger Vehicles

- 2.2. Commercial Vehicles

-

3. User Application

- 3.1. Private Infrastructure

- 3.2. Public Infrastructure

China Electric Vehicle Charging Infrastructure Market Segmentation By Geography

- 1. China

China Electric Vehicle Charging Infrastructure Market Regional Market Share

Geographic Coverage of China Electric Vehicle Charging Infrastructure Market

China Electric Vehicle Charging Infrastructure Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 48.56% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Charging Station Type

- 5.1.1. Alternating Current (AC) Charging Station

- 5.1.2. Direct Current (DC) Charging Station

- 5.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.2.1. Passenger Vehicles

- 5.2.2. Commercial Vehicles

- 5.3. Market Analysis, Insights and Forecast - by User Application

- 5.3.1. Private Infrastructure

- 5.3.2. Public Infrastructure

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.1. Market Analysis, Insights and Forecast - by Charging Station Type

- 6. China Electric Vehicle Charging Infrastructure Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Charging Station Type

- 6.1.1. Alternating Current (AC) Charging Station

- 6.1.2. Direct Current (DC) Charging Station

- 6.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.2.1. Passenger Vehicles

- 6.2.2. Commercial Vehicles

- 6.3. Market Analysis, Insights and Forecast - by User Application

- 6.3.1. Private Infrastructure

- 6.3.2. Public Infrastructure

- 6.1. Market Analysis, Insights and Forecast - by Charging Station Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 EV Power

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 YKC

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 State Grid Corporation of China

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Eichong

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 TELD

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 TGood

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Evking

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Wancheng Wanchong

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Starcharge

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 SAIC Motor

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Potevio

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Southern Power Grid

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 ShenZhen Carenergy Net

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Hooenergy

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Winland

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.1 EV Power

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Electric Vehicle Charging Infrastructure Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: China Electric Vehicle Charging Infrastructure Market Share (%) by Company 2025

List of Tables

- Table 1: China Electric Vehicle Charging Infrastructure Market Revenue billion Forecast, by Charging Station Type 2020 & 2033

- Table 2: China Electric Vehicle Charging Infrastructure Market Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 3: China Electric Vehicle Charging Infrastructure Market Revenue billion Forecast, by User Application 2020 & 2033

- Table 4: China Electric Vehicle Charging Infrastructure Market Revenue billion Forecast, by Region 2020 & 2033

- Table 5: China Electric Vehicle Charging Infrastructure Market Revenue billion Forecast, by Charging Station Type 2020 & 2033

- Table 6: China Electric Vehicle Charging Infrastructure Market Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 7: China Electric Vehicle Charging Infrastructure Market Revenue billion Forecast, by User Application 2020 & 2033

- Table 8: China Electric Vehicle Charging Infrastructure Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Electric Vehicle Charging Infrastructure Market?

The projected CAGR is approximately 48.56%.

2. Which companies are prominent players in the China Electric Vehicle Charging Infrastructure Market?

Key companies in the market include EV Power, YKC, State Grid Corporation of China, Eichong, TELD, TGood, Evking, Wancheng Wanchong, Starcharge, SAIC Motor, Potevio, Southern Power Grid, ShenZhen Carenergy Net, Hooenergy, Winland.

3. What are the main segments of the China Electric Vehicle Charging Infrastructure Market?

The market segments include Charging Station Type, Vehicle Type, User Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 25.6 billion as of 2022.

5. What are some drivers contributing to market growth?

Favorable Government Initiatives to Support the Growth of Electric Vehicle Charging Infrastructure.

6. What are the notable trends driving market growth?

Public Charging Stations are Expected to Gain Prominent Share in the Market During the Forecast Period.

7. Are there any restraints impacting market growth?

Supply Shortages in Building Electric Vehicle Charging Stations.

8. Can you provide examples of recent developments in the market?

September 2023: PetroChina, a leading oil and gas company based out of China, announced its acquisition of an electric vehicle (EV) charging firm, Potevio New Energy Co Ltd. It is to establish its brand presence in the electric vehicle charging market across China. It was estimated that by the end of 2021, Potevio operated 50,000 charging points in more than 50 Chinese cities.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Electric Vehicle Charging Infrastructure Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Electric Vehicle Charging Infrastructure Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Electric Vehicle Charging Infrastructure Market?

To stay informed about further developments, trends, and reports in the China Electric Vehicle Charging Infrastructure Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence