Key Insights

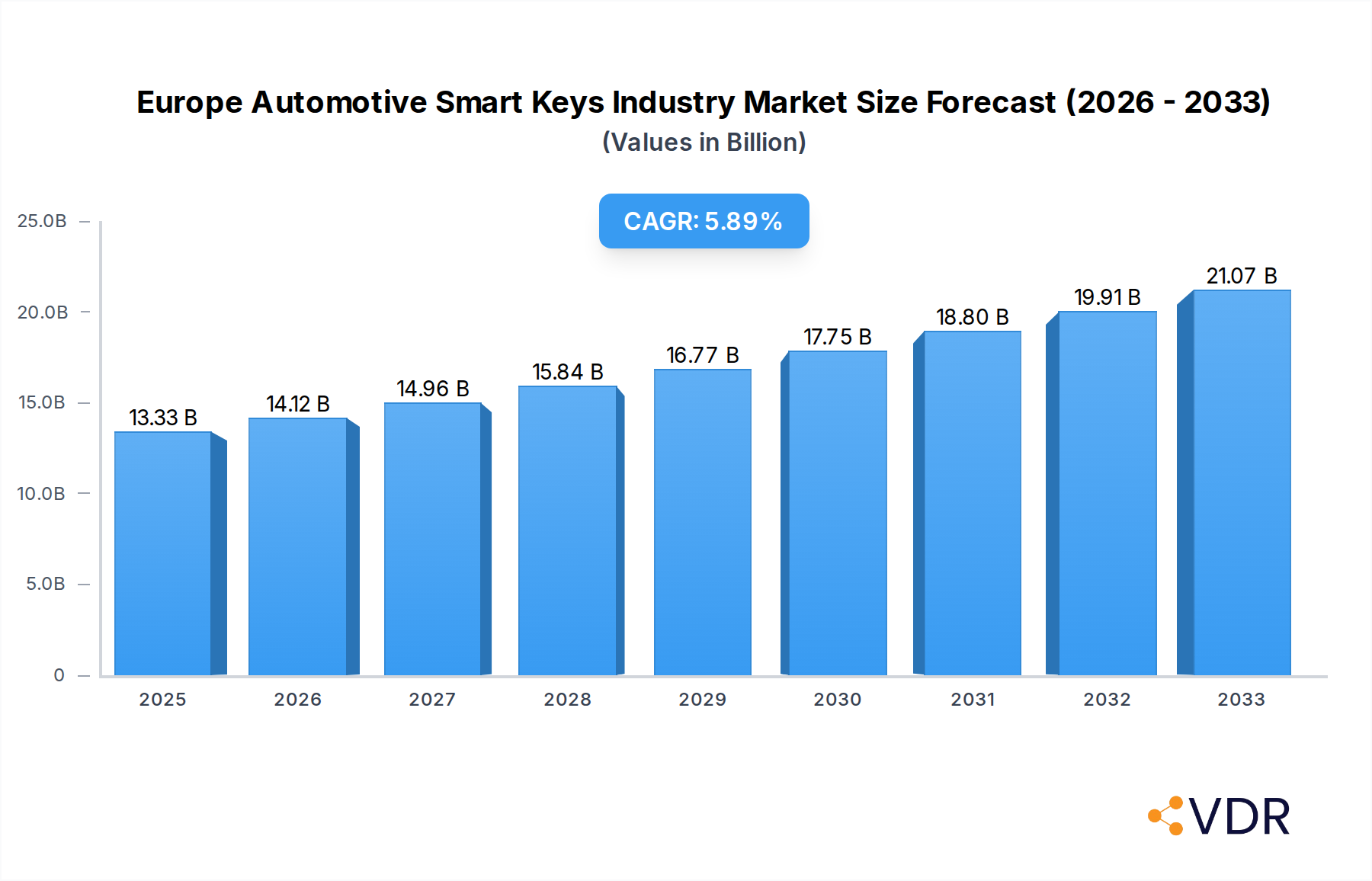

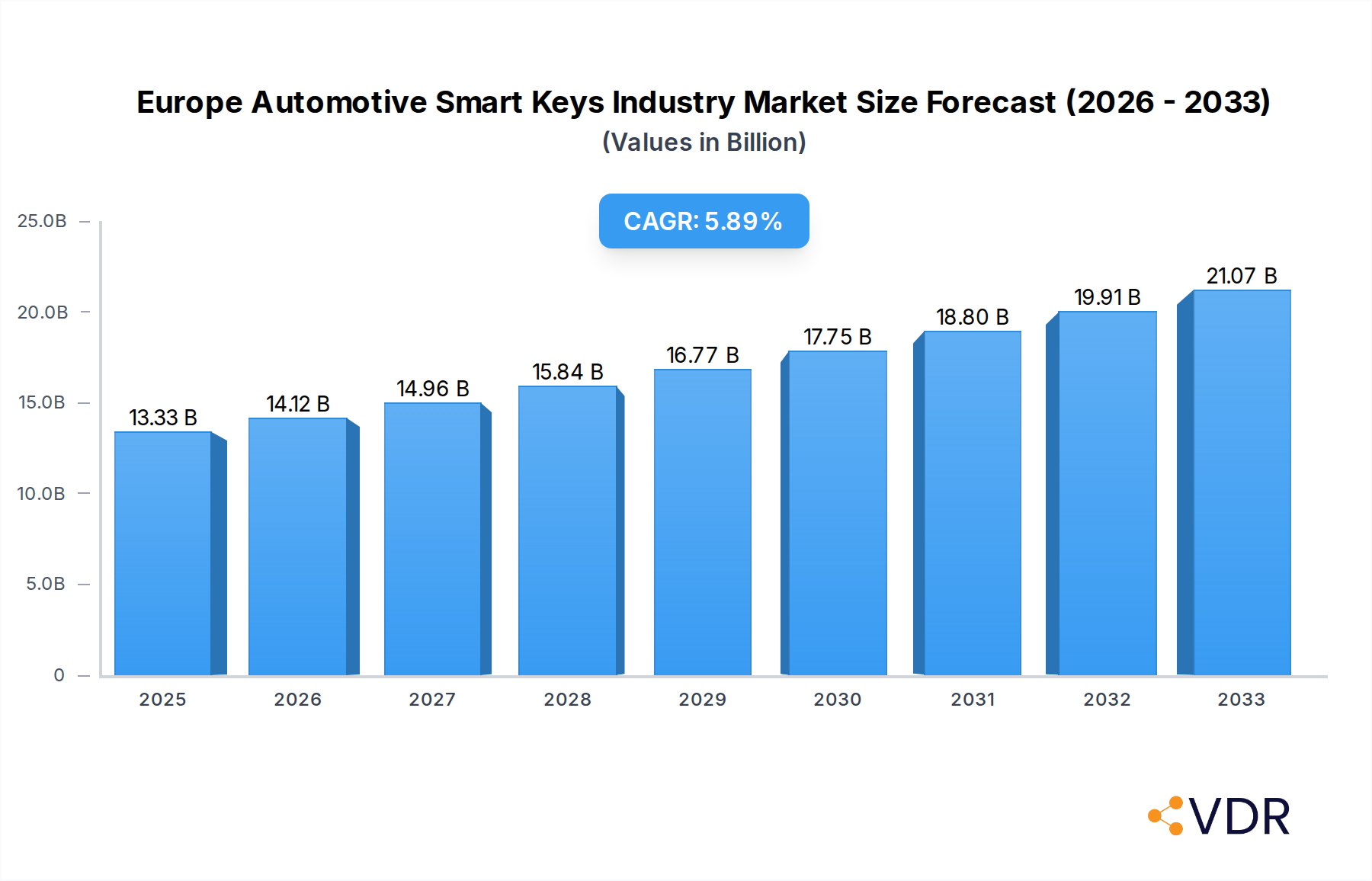

The Europe Automotive Smart Keys Industry is poised for significant expansion, driven by an increasing consumer demand for enhanced vehicle security, convenience, and advanced functionalities. With an estimated market size of USD 13.33 billion in 2025, the industry is projected to grow at a Compound Annual Growth Rate (CAGR) of 6% during the forecast period of 2025-2033. This robust growth is primarily fueled by the rising adoption of sophisticated vehicle access systems, including Remote Keyless Entry (RKE) and Passive Keyless Entry (PKE) technologies. The increasing integration of these smart key features as original equipment manufacturer (OEM) offerings in new vehicle models across Europe, coupled with a growing aftermarket segment seeking to upgrade existing vehicles, underscores the market's dynamism. Major players like Denso Corporation, Hyundai Mobis, and Continental AG are at the forefront, investing heavily in research and development to introduce innovative solutions that cater to evolving consumer preferences for seamless and secure vehicle interaction.

Europe Automotive Smart Keys Industry Market Size (In Billion)

The market's trajectory is further shaped by several key trends. The growing proliferation of multi-function smart keys, which integrate features such as engine start-stop, trunk opening, and even vehicle personalization, is a significant driver. Moreover, the ongoing technological advancements in vehicle connectivity and the increasing prevalence of electric vehicles (EVs) are creating new opportunities for smart key systems that can interact with mobile devices and offer advanced battery management features. While the market enjoys strong growth prospects, potential restraints include the high cost of advanced smart key technologies, which can impact adoption rates in certain segments, and concerns around cybersecurity vulnerabilities that necessitate robust encryption and authentication protocols. Nevertheless, the overarching trend towards smart and connected mobility in Europe, coupled with stringent automotive safety regulations, is expected to sustain the industry's upward momentum.

Europe Automotive Smart Keys Industry Company Market Share

Europe Automotive Smart Keys Industry Market Dynamics & Structure

The Europe Automotive Smart Keys industry is characterized by a moderately concentrated market, with leading players investing heavily in technological innovation. The rapid evolution of vehicle connectivity and the increasing consumer demand for enhanced convenience and security are primary drivers. Regulatory frameworks, particularly concerning cybersecurity and data privacy, are influencing product development and market entry. Competitive product substitutes, such as smartphone-based vehicle access, are emerging, pushing smart key manufacturers to innovate further. End-user demographics are shifting towards younger, tech-savvy consumers who prioritize integrated digital experiences within their vehicles. Mergers and acquisitions (M&A) activity is observed as companies seek to expand their technology portfolios and market reach.

- Market Concentration: Dominated by a few key global players, with significant contributions from European-based manufacturers.

- Technological Innovation Drivers: Increasing demand for enhanced vehicle security, seamless user experience, and integration with connected car ecosystems.

- Regulatory Frameworks: Stringent EU regulations on cybersecurity, data protection, and vehicle safety standards are shaping product design and compliance.

- Competitive Product Substitutes: Rise of smartphone integration for vehicle access, forcing smart key providers to offer superior functionality and security.

- End-User Demographics: Growing preference for advanced features and a willingness to pay a premium for convenience among affluent and younger car owners.

- M&A Trends: Strategic acquisitions aimed at bolstering technological capabilities in areas like NFC, Bluetooth Low Energy, and biometrics.

Europe Automotive Smart Keys Industry Growth Trends & Insights

The Europe Automotive Smart Keys industry is poised for robust growth, driven by an increasing adoption of advanced vehicle features and a rising demand for enhanced security and convenience. The market size is projected to witness a significant expansion from an estimated xx billion units in 2025 to xx billion units by 2033, exhibiting a compound annual growth rate (CAGR) of approximately xx% during the forecast period. This growth is underpinned by the steady penetration of smart key systems across various vehicle segments, from luxury and premium cars to increasingly sophisticated mid-range models. Technological disruptions are a constant feature, with advancements in Passive Keyless Entry (PKE) systems, enhanced anti-theft measures, and the integration of biometric authentication transforming the user experience. Consumer behavior is shifting towards a demand for seamless and integrated digital solutions, where the vehicle key becomes an extension of their digital identity. This trend is further fueled by the growing popularity of connected car services, which rely on secure and reliable access mechanisms. The base year of 2025 marks a pivotal point, with significant investments in R&D and the rollout of next-generation smart key technologies expected to accelerate market penetration. The historical period from 2019 to 2024 has laid the groundwork, showcasing consistent growth as manufacturers integrated these systems into a wider array of vehicles. The estimated year of 2025 reflects the current market standing, with a clear trajectory towards substantial future expansion. The study period, spanning from 2019 to 2033, encompasses this entire growth arc, providing a comprehensive view of the industry's evolution.

Dominant Regions, Countries, or Segments in Europe Automotive Smart Keys Industry

Within the Europe Automotive Smart Keys industry, Germany consistently emerges as a dominant country, primarily driven by its strong automotive manufacturing base and its role as a hub for technological innovation. The significant presence of leading automotive OEMs and Tier-1 suppliers in Germany fosters a dynamic environment for the adoption and development of advanced smart key technologies. This dominance is further reinforced by a robust aftermarket segment catering to the extensive existing vehicle parc.

Passive Keyless Entry (PKE) technology stands out as the most dominant segment in terms of market share and adoption rates. PKE systems offer superior convenience by allowing users to unlock and start their vehicles without physically interacting with the key. This seamless experience aligns perfectly with evolving consumer expectations for effortless vehicle access and operation. The widespread integration of PKE across various vehicle classes, from mainstream to premium, fuels its market leadership.

The OEM (Original Equipment Manufacturer) installation type commands a larger share of the market. This is attributable to the fact that smart key systems are increasingly becoming standard features in new vehicle production lines. Automakers are prioritizing these advanced security and convenience features to differentiate their offerings and meet consumer demand. While the aftermarket segment is growing, the sheer volume of new vehicle sales equipped with factory-installed smart keys solidifies the OEM segment's dominance.

Dominant Country: Germany

- Key Drivers: High concentration of automotive OEMs and Tier-1 suppliers, leading automotive R&D, strong consumer demand for advanced vehicle features, and a significant vehicle parc driving aftermarket sales.

- Market Share: Estimated to hold over xx% of the European smart key market value.

- Growth Potential: Continued innovation and strong integration with evolving automotive technologies.

Dominant Technology Type: Passive Keyless Entry (PKE)

- Key Drivers: Superior user convenience, enhanced security features, seamless integration with vehicle systems, and widespread adoption in new vehicle models.

- Market Penetration: Expected to be present in over xx% of new passenger vehicles sold in Europe by 2025.

- Growth Potential: Ongoing advancements in range, security protocols, and integration with digital vehicle access solutions.

Dominant Installation Type: OEM (Original Equipment Manufacturer)

- Key Drivers: Standard fitment in new vehicles, integration with vehicle's electronic architecture, economies of scale in production, and supplier relationships with automotive manufacturers.

- Market Share: Accounts for approximately xx% of the total smart key market value.

- Growth Potential: Continued demand for integrated solutions in new vehicle production.

Europe Automotive Smart Keys Industry Product Landscape

The Europe Automotive Smart Keys industry is witnessing a surge in sophisticated product innovations aimed at enhancing security, convenience, and user experience. Manufacturers are focusing on developing multi-function smart keys that integrate advanced features beyond basic locking and unlocking. This includes capabilities like remote engine start, vehicle location services, and integration with smartphone applications for digital key functionalities. Performance metrics such as enhanced signal range, improved battery life, and robust encryption for anti-theft measures are key differentiators. Unique selling propositions often revolve around seamless integration with in-car infotainment systems and advanced security protocols that prevent relay attacks. Technological advancements are pushing towards miniaturization, increased durability, and the incorporation of biometric authentication for personalized access.

Key Drivers, Barriers & Challenges in Europe Automotive Smart Keys Industry

Key Drivers:

- Growing Consumer Demand for Convenience and Security: The desire for effortless vehicle access and advanced anti-theft features is a primary market propellant.

- Advancements in Vehicle Connectivity and Infotainment Systems: Integration of smart keys with connected car platforms enhances functionality and user experience.

- Increasing Production of Premium and Luxury Vehicles: These segments often feature smart keys as standard, driving adoption rates.

- Technological Innovations: Development of more secure, reliable, and feature-rich smart key systems, including biometric authentication and NFC integration.

Barriers & Challenges:

- High Development and Manufacturing Costs: Implementing advanced technologies can lead to higher initial investment for manufacturers and potentially higher costs for consumers.

- Cybersecurity Threats and Vulnerabilities: The risk of hacking and relay attacks necessitates continuous investment in security enhancements, posing a significant challenge.

- Regulatory Compliance and Standardization: Navigating diverse and evolving automotive regulations across different European countries can be complex.

- Supply Chain Disruptions: Global supply chain issues can impact the availability of critical components, affecting production timelines and costs.

- Competition from Smartphone-Based Access: The growing adoption of digital keys via smartphones presents a competitive alternative.

Emerging Opportunities in Europe Automotive Smart Keys Industry

Emerging opportunities lie in the further development of digital key solutions that seamlessly integrate with smartphone ecosystems, offering consumers a versatile and secure alternative to traditional fobs. The increasing adoption of biometric authentication (fingerprint or facial recognition) on smart keys provides an enhanced layer of security and personalization. Opportunities also exist in developing energy-efficient smart keys with longer battery life and exploring vehicle-to-everything (V2X) communication capabilities for smart keys, enabling advanced safety and convenience features. Furthermore, the growing demand for shared mobility services presents an avenue for innovative smart key management solutions that facilitate easy and secure vehicle access for multiple users.

Growth Accelerators in the Europe Automotive Smart Keys Industry Industry

The long-term growth of the Europe Automotive Smart Keys industry is being significantly accelerated by several key factors. Technological breakthroughs in areas like ultra-wideband (UWB) technology are enabling more precise and secure location tracking for keyless entry, minimizing vulnerability to relay attacks. Strategic partnerships between smart key manufacturers, automotive OEMs, and technology providers are fostering integrated solutions and faster innovation cycles. Market expansion strategies, including the increasing adoption of smart keys in mid-range vehicle segments and the growing importance of the automotive aftermarket for retrofitting and upgrades, are also key growth accelerators. The continued push towards electrification and autonomous driving will further necessitate advanced and secure key management systems.

Key Players Shaping the Europe Automotive Smart Keys Industry Market

- Denso Corporation

- Tokai Rika Co Ltd

- Hyundai Mobis

- Silca Group

- Huf Hulsbeck & Furst GmbH & Co KG

- HELLA GmbH & Co KGaA

- Continental AG

- ALPHA Corporation

- Valeo SA

- Robert Bosch GmbH

- ZF Friedrichshafen AG

Notable Milestones in Europe Automotive Smart Keys Industry Sector

- 2019: Increased adoption of multi-function smart keys with integrated remote start and vehicle locator features in new vehicle models.

- 2020: Significant advancements in Passive Keyless Entry (PKE) security protocols to combat relay attacks, with widespread industry adoption.

- 2021: Growing integration of NFC (Near Field Communication) technology for smartphone-based vehicle access as a supplementary or primary key solution.

- 2022: Introduction of enhanced cybersecurity measures and encryption standards across major smart key manufacturers to address growing digital threats.

- 2023: Expansion of biometric authentication features (e.g., fingerprint scanners) in premium vehicle smart keys for added security and personalization.

- 2024: Increased focus on developing ultra-wideband (UWB) technology for more precise and secure keyless entry and vehicle location capabilities.

- 2025 (Estimated): Anticipated wider availability of integrated digital key platforms that allow seamless smartphone control of vehicle access and functions.

In-Depth Europe Automotive Smart Keys Industry Market Outlook

The Europe Automotive Smart Keys industry is projected for sustained and robust growth, propelled by an ongoing drive for enhanced vehicle security and user convenience. The integration of sophisticated technologies, such as ultra-wideband (UWB) for precise localization and advanced biometric authentication, will redefine the user experience and bolster security against sophisticated threats. Strategic collaborations between smart key manufacturers and automotive giants will accelerate the development and deployment of next-generation digital key solutions, seamlessly blending physical and digital access. As the automotive sector continues its transition towards electrification and autonomous driving, the demand for secure and integrated smart key systems will only intensify, creating a fertile ground for innovation and market expansion in the years to come.

Europe Automotive Smart Keys Industry Segmentation

-

1. Application Type

- 1.1. Single Function

- 1.2. Multi-function

-

2. Technology Type

- 2.1. Remote Keyless Entry

- 2.2. Passive Keyless Entry

-

3. Installation Type

- 3.1. OEM

- 3.2. Aftermarket

Europe Automotive Smart Keys Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

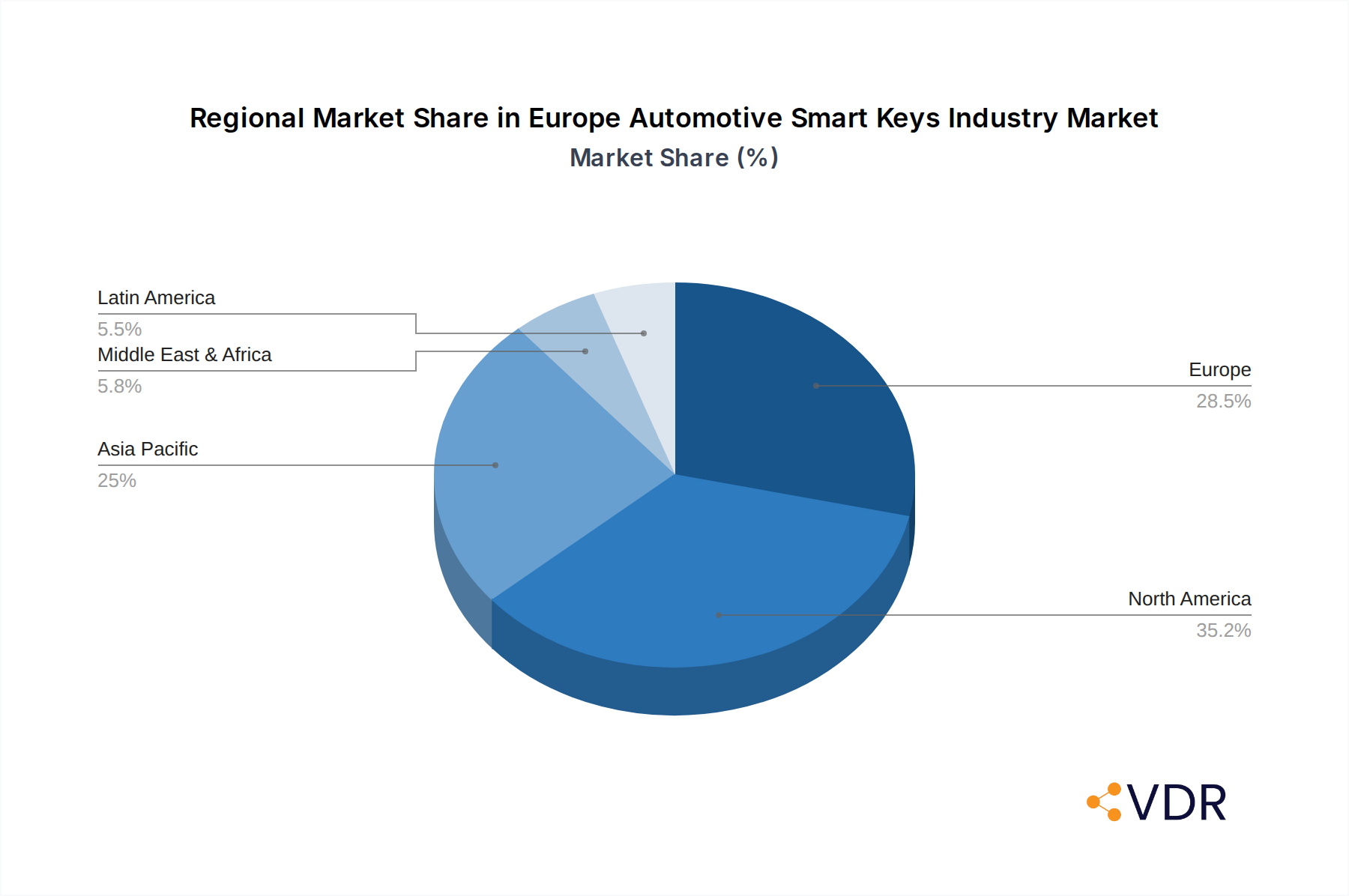

Europe Automotive Smart Keys Industry Regional Market Share

Geographic Coverage of Europe Automotive Smart Keys Industry

Europe Automotive Smart Keys Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application Type

- 5.1.1. Single Function

- 5.1.2. Multi-function

- 5.2. Market Analysis, Insights and Forecast - by Technology Type

- 5.2.1. Remote Keyless Entry

- 5.2.2. Passive Keyless Entry

- 5.3. Market Analysis, Insights and Forecast - by Installation Type

- 5.3.1. OEM

- 5.3.2. Aftermarket

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Application Type

- 6. Europe Automotive Smart Keys Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application Type

- 6.1.1. Single Function

- 6.1.2. Multi-function

- 6.2. Market Analysis, Insights and Forecast - by Technology Type

- 6.2.1. Remote Keyless Entry

- 6.2.2. Passive Keyless Entry

- 6.3. Market Analysis, Insights and Forecast - by Installation Type

- 6.3.1. OEM

- 6.3.2. Aftermarket

- 6.1. Market Analysis, Insights and Forecast - by Application Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Denso Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Tokai Rika Co Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Hyundai Mobis

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Silca Group

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Huf Hulsbeck & Furst GmbH & Co KG

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 HELLA GmbH & Co KGaA

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Continental AG

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 ALPHA Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Valeo SA

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Robert Bosch Gmb

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 ZF Friedrichshafen AG

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Denso Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Automotive Smart Keys Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Automotive Smart Keys Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Automotive Smart Keys Industry Revenue billion Forecast, by Application Type 2020 & 2033

- Table 2: Europe Automotive Smart Keys Industry Revenue billion Forecast, by Technology Type 2020 & 2033

- Table 3: Europe Automotive Smart Keys Industry Revenue billion Forecast, by Installation Type 2020 & 2033

- Table 4: Europe Automotive Smart Keys Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Europe Automotive Smart Keys Industry Revenue billion Forecast, by Application Type 2020 & 2033

- Table 6: Europe Automotive Smart Keys Industry Revenue billion Forecast, by Technology Type 2020 & 2033

- Table 7: Europe Automotive Smart Keys Industry Revenue billion Forecast, by Installation Type 2020 & 2033

- Table 8: Europe Automotive Smart Keys Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United Kingdom Europe Automotive Smart Keys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Germany Europe Automotive Smart Keys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: France Europe Automotive Smart Keys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Italy Europe Automotive Smart Keys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Spain Europe Automotive Smart Keys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Netherlands Europe Automotive Smart Keys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Belgium Europe Automotive Smart Keys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Sweden Europe Automotive Smart Keys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Norway Europe Automotive Smart Keys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Poland Europe Automotive Smart Keys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Denmark Europe Automotive Smart Keys Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Automotive Smart Keys Industry?

The projected CAGR is approximately 6%.

2. Which companies are prominent players in the Europe Automotive Smart Keys Industry?

Key companies in the market include Denso Corporation, Tokai Rika Co Ltd, Hyundai Mobis, Silca Group, Huf Hulsbeck & Furst GmbH & Co KG, HELLA GmbH & Co KGaA, Continental AG, ALPHA Corporation, Valeo SA, Robert Bosch Gmb, ZF Friedrichshafen AG.

3. What are the main segments of the Europe Automotive Smart Keys Industry?

The market segments include Application Type, Technology Type, Installation Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 13.33 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand of Electric Vehicles Is Likely To Drive The Market Growth.

6. What are the notable trends driving market growth?

Security Risks is Hindering the Market Growth..

7. Are there any restraints impacting market growth?

Lack of Skilled Labors Is Anticipated To Restrain The market Growth.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Automotive Smart Keys Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Automotive Smart Keys Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Automotive Smart Keys Industry?

To stay informed about further developments, trends, and reports in the Europe Automotive Smart Keys Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence