Key Insights

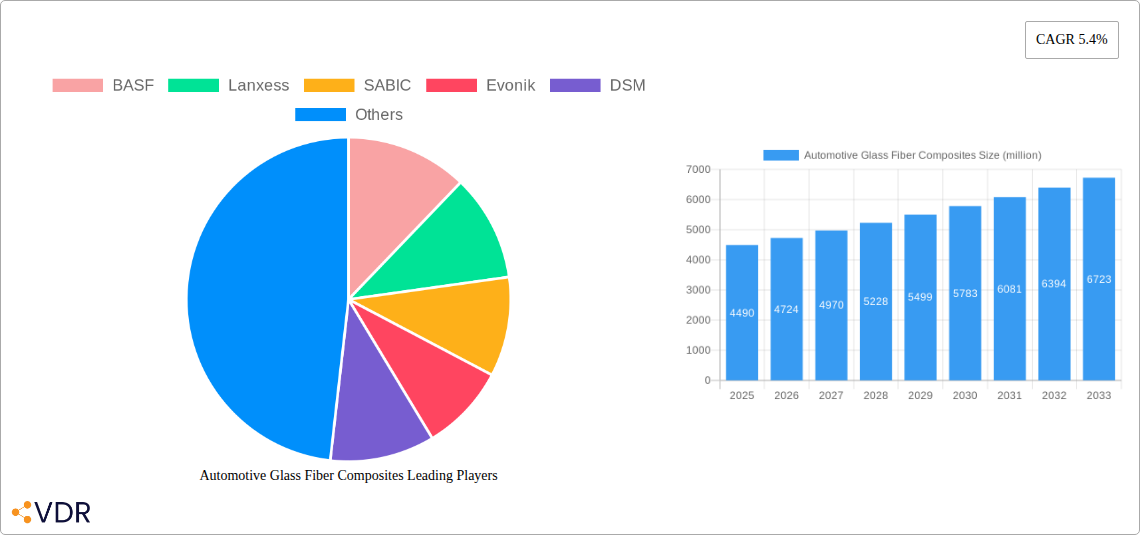

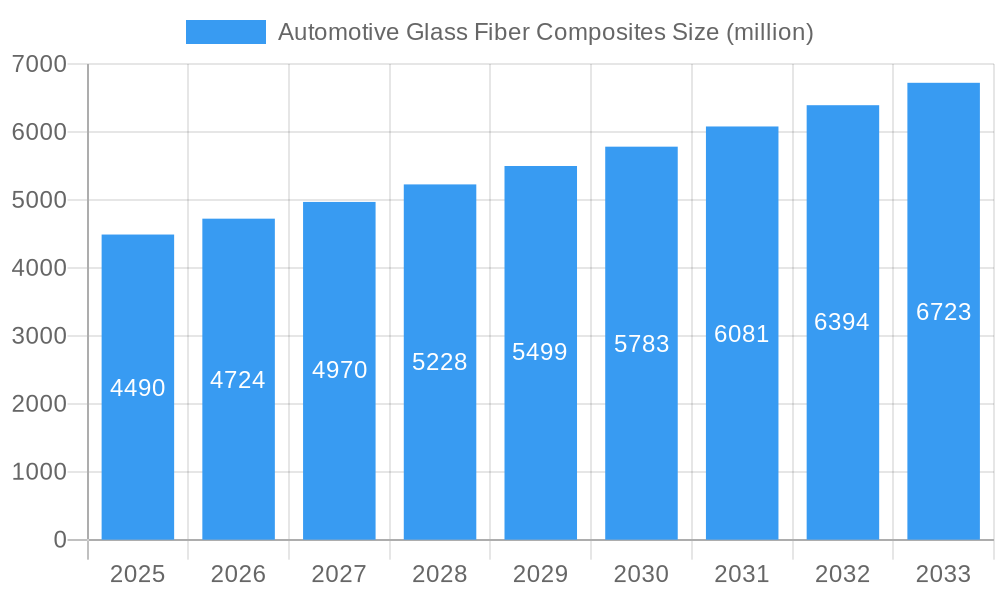

The global Automotive Glass Fiber Composites market is poised for significant expansion, projected to reach a substantial valuation in the coming years. The market, currently valued at approximately $4490 million in 2025, is expected to witness a Compound Annual Growth Rate (CAGR) of 5.4% throughout the forecast period of 2025-2033. This robust growth is primarily fueled by the increasing demand for lightweight and durable materials in the automotive industry, driven by stringent fuel efficiency regulations and the growing emphasis on reducing vehicle emissions. Manufacturers are increasingly adopting glass fiber composites as a viable alternative to traditional materials like steel and aluminum, owing to their superior strength-to-weight ratio, corrosion resistance, and design flexibility. Key applications spanning automotive body and roof panels, hoods, chassis components, and interior parts are witnessing a surge in composite integration, directly contributing to the market's upward trajectory.

Automotive Glass Fiber Composites Market Size (In Billion)

The market's expansion is further propelled by ongoing advancements in composite manufacturing technologies, leading to improved performance characteristics and cost-effectiveness. The Thermosetting Plastic Products segment, known for its excellent mechanical properties and thermal stability, is expected to maintain a strong market presence. Simultaneously, the Thermoplastic Plastic Products segment is gaining traction due to its recyclability and ease of processing. Geographically, Asia Pacific, led by China and India, is anticipated to be a dominant region, driven by its expanding automotive production and increasing adoption of advanced materials. North America and Europe also represent significant markets, supported by established automotive industries and a strong focus on sustainability initiatives. However, challenges such as the relatively higher initial investment costs for composite manufacturing infrastructure and the need for specialized handling and recycling processes may present some restraints to the market's growth, requiring strategic solutions from industry players.

Automotive Glass Fiber Composites Company Market Share

Automotive Glass Fiber Composites Market Report: Comprehensive Analysis & Future Outlook (2019-2033)

This in-depth report provides a definitive analysis of the global Automotive Glass Fiber Composites market, offering critical insights for stakeholders navigating this dynamic sector. Covering a comprehensive study period from 2019 to 2033, with a base year of 2025, this report meticulously dissects market drivers, growth trends, regional dominance, product innovation, and key players. We present quantitative and qualitative data, utilizing parent and child market segments to deliver unparalleled market intelligence. All values are presented in million units for clear industry comprehension.

Automotive Glass Fiber Composites Market Dynamics & Structure

The automotive glass fiber composites market is characterized by a moderately concentrated landscape, with key players investing heavily in technological advancements to enhance material performance, weight reduction, and cost-effectiveness. Innovation drivers include the relentless pursuit of fuel efficiency, the growing adoption of electric vehicles (EVs), and stringent regulatory frameworks aimed at reducing carbon emissions. The increasing demand for lighter yet robust automotive components across applications like automotive body & roof panels, automotive hood, automotive chassis, and interiors fuels this innovation. Competitive product substitutes, such as advanced high-strength steels and aluminum alloys, continue to challenge market penetration, necessitating continuous R&D in composite formulations and manufacturing processes. End-user demographics are shifting towards environmentally conscious consumers and an increasing global vehicle production output. Mergers and acquisitions (M&A) activity, while moderate, is strategic, focusing on expanding manufacturing capacity, acquiring advanced technologies, and consolidating market presence. Barriers to entry include high initial investment for advanced manufacturing facilities and the need for specialized expertise in composite design and production.

- Market Concentration: Moderately concentrated with significant presence of established chemical and materials companies.

- Technological Innovation Drivers:

- Lightweighting for fuel efficiency and EV range extension.

- Improved strength-to-weight ratios.

- Enhanced safety features through impact absorption.

- Development of sustainable and recyclable composite materials.

- Regulatory Frameworks: Increasing stringency in emissions standards globally, driving adoption of lightweight materials.

- Competitive Product Substitutes: Advanced High-Strength Steels (AHSS), aluminum alloys, and carbon fiber composites.

- End-User Demographics: Growing demand from emerging economies, increased preference for sustainable mobility solutions, and evolving consumer expectations for vehicle performance.

- M&A Trends: Strategic acquisitions to gain technological edge, expand product portfolios, and secure market share. Example: Acquisition of advanced composite manufacturers by larger chemical conglomerates.

Automotive Glass Fiber Composites Growth Trends & Insights

The global automotive glass fiber composites market is poised for significant expansion, driven by a confluence of technological advancements, evolving automotive design philosophies, and increasing regulatory pressures. The market size evolution is marked by a consistent upward trajectory, with projected substantial growth throughout the forecast period. Adoption rates of glass fiber composites are accelerating as automakers recognize their inherent advantages in reducing vehicle weight, thereby enhancing fuel efficiency and extending the range of electric vehicles. This shift is particularly pronounced in the passenger car segment, where the pursuit of optimal performance and sustainability is paramount. Technological disruptions are continuously reshaping the market, including advancements in resin systems, fiber weaving techniques, and automated manufacturing processes that improve production efficiency and component quality. These innovations address previous concerns regarding cost and scalability, making composites a more viable and attractive alternative to traditional materials.

Consumer behavior shifts, influenced by environmental consciousness and a desire for technologically advanced vehicles, are further propelling the demand for lighter, more fuel-efficient cars. This translates into a growing preference for components manufactured from advanced materials like glass fiber composites. The market penetration of these composites is expected to increase across a wider spectrum of automotive applications, moving beyond traditional components to more integrated structural parts. The ability of glass fiber composites to offer complex geometries and superior design flexibility also contributes to their increasing adoption, allowing for innovative vehicle designs and integrated functionalities. The forecast period will witness a sustained compound annual growth rate (CAGR) as the industry innovates and scales production. Specific metrics indicate a growing market penetration from an estimated 18% in 2025 to over 25% by 2033 for key structural applications. This sustained growth is underpinned by ongoing research and development efforts aimed at further reducing manufacturing costs and improving the recyclability of these advanced materials, making them a cornerstone of future automotive manufacturing.

Dominant Regions, Countries, or Segments in Automotive Glass Fiber Composites

The global automotive glass fiber composites market is experiencing dynamic growth, with significant regional and segment-specific contributions. Among the Applications, Automotive Body & Roof Panels stand out as the dominant segment, accounting for an estimated 35% of the market share in 2025. This dominance is fueled by the critical need for weight reduction in these large surface areas to enhance fuel efficiency and the electric vehicle range. The inherent strength and design flexibility of glass fiber composites make them ideal for creating sleek, aerodynamic, and structurally sound body and roof structures.

In terms of Types, Thermoplastic Plastic Products are increasingly gaining traction and are projected to experience a higher growth rate compared to Thermosetting Plastic Products. By 2025, Thermoplastic Plastic Products are expected to capture approximately 58% of the market share due to their advantageous properties such as recyclability, lower processing temperatures, and faster cycle times, making them more cost-effective for high-volume automotive production.

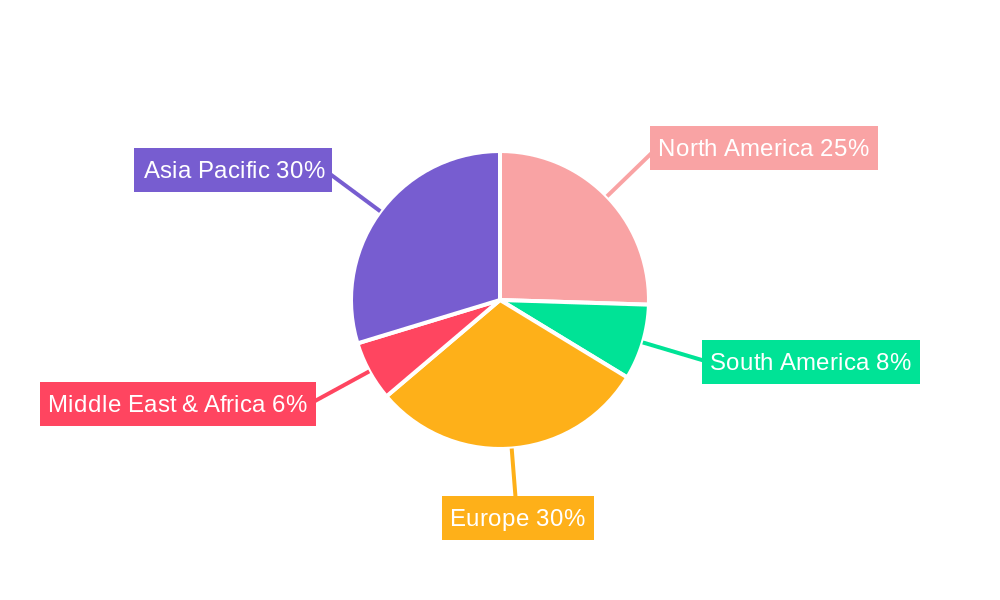

Geographically, Asia Pacific is emerging as the powerhouse of the automotive glass fiber composites market, driven by its status as the world's largest automotive manufacturing hub. Countries like China, Japan, and South Korea are leading the charge, with substantial investments in electric vehicle production and stringent government policies promoting the adoption of lightweight materials. China, in particular, is a dominant force, expected to contribute over 40% of the global demand by 2025, propelled by its massive domestic vehicle market and aggressive push towards electrification.

- Dominant Application Segment:

- Automotive Body & Roof Panels: Expected to hold approximately 35% market share in 2025.

- Key Drivers: Lightweighting for fuel efficiency and EV range, superior impact resistance, design flexibility for aerodynamics.

- Market Share Growth Potential: High due to increasing adoption in mainstream vehicle platforms.

- Automotive Body & Roof Panels: Expected to hold approximately 35% market share in 2025.

- Dominant Type Segment:

- Thermoplastic Plastic Products: Projected to hold approximately 58% market share in 2025, with higher growth potential.

- Key Drivers: Recyclability, faster manufacturing cycles, lower energy consumption during production, improved impact performance.

- Growth Potential: Significant, driven by cost-effectiveness and sustainability initiatives.

- Thermoplastic Plastic Products: Projected to hold approximately 58% market share in 2025, with higher growth potential.

- Dominant Region:

- Asia Pacific: Expected to lead the global market by a considerable margin.

- Key Drivers: Largest automotive production base, rapid EV adoption, supportive government policies and incentives for lightweight materials, growing middle-class population.

- Country-Specific Dominance: China leading in both production and consumption, followed by Japan and South Korea.

- Market Share: Estimated to account for over 40% of the global market by 2025.

- Asia Pacific: Expected to lead the global market by a considerable margin.

Automotive Glass Fiber Composites Product Landscape

The automotive glass fiber composites product landscape is characterized by continuous innovation in material science and manufacturing techniques. Products are engineered to offer enhanced mechanical properties, improved thermal resistance, and superior surface finish. Key innovations include high-strength glass fibers, advanced resin matrices (e.g., tailored epoxies and polyurethanes for thermosets, and high-performance polyamides and polycarbonates for thermoplastics), and innovative composite structures like organosheets and continuous fiber-reinforced thermoplastics. These materials are integral to creating lightweight yet robust components such as structural reinforcements, interior trim, and exterior panels, contributing to improved vehicle safety and performance. Unique selling propositions revolve around exceptional strength-to-weight ratios, corrosion resistance, and the ability to integrate multiple functions into a single component. Technological advancements are also focusing on developing fire-retardant composites and those with enhanced acoustic dampening properties.

Key Drivers, Barriers & Challenges in Automotive Glass Fiber Composites

The automotive glass fiber composites market is propelled by several key drivers. The paramount driver is the industry's relentless pursuit of lightweighting to enhance fuel efficiency and extend the range of electric vehicles, a crucial factor in meeting global emissions standards. Secondly, advancements in manufacturing technologies are making these composites more cost-competitive and scalable for mass production. Finally, growing environmental regulations and consumer demand for sustainable mobility are pushing automakers towards materials with a lower carbon footprint and improved recyclability.

However, the market also faces significant barriers and challenges. High manufacturing costs compared to traditional materials like steel remain a considerable restraint, particularly for entry-level vehicles. Recycling infrastructure and technologies for composites are still in their nascent stages, posing a challenge for end-of-life management. Furthermore, complex supply chains and the availability of skilled labor for specialized composite manufacturing processes can create bottlenecks. The impact of fluctuating raw material prices, particularly for resins, can also affect profitability.

Emerging Opportunities in Automotive Glass Fiber Composites

Emerging opportunities in the automotive glass fiber composites sector are substantial and diverse. The rapid growth of the electric vehicle (EV) market presents a significant avenue, as EVs heavily rely on lightweight materials for battery enclosure systems, body structures, and interior components to maximize range. The development of advanced recycling technologies for glass fiber composites, making them more circular and sustainable, will unlock new markets and appeal to environmentally conscious manufacturers and consumers. Furthermore, the exploration of bio-based resins and natural fibers in composite formulations offers a pathway towards greener automotive solutions. The increasing trend towards autonomous driving necessitates the integration of complex sensor housings and lightweight structural components, areas where composites excel.

Growth Accelerators in the Automotive Glass Fiber Composites Industry

Several key catalysts are accelerating the growth of the automotive glass fiber composites industry. Technological breakthroughs in resin systems and fiber reinforcement continue to enhance material performance, enabling their use in more demanding structural applications. Strategic partnerships and collaborations between material suppliers, automotive OEMs, and Tier-1 suppliers are crucial for co-development and faster market adoption. Furthermore, increased investment in research and development by major chemical and composites companies is driving innovation in areas like faster curing times, improved impact resistance, and enhanced recyclability. Market expansion strategies, including the development of new manufacturing techniques and the localization of production in key automotive hubs, are also playing a significant role in boosting growth.

Key Players Shaping the Automotive Glass Fiber Composites Market

- BASF

- Lanxess

- SABIC

- Evonik Industries AG

- DSM

- Avient Corporation

- DuPont

- DOMO Chemicals

- Hexion Inc.

- Celanese Corporation

- RTP Company

- Sumitomo Bakelite Co., Ltd.

- Lotte Chemical Corporation

- Daicel Corporation

- Kolon Industries, Inc.

- Denka Company Limited

- Kingfa Sci. & Tech. Co., Ltd.

Notable Milestones in Automotive Glass Fiber Composites Sector

- 2019: Launch of new generation of high-performance thermoplastic composites offering improved impact strength and recyclability.

- 2020: Increased R&D investment by major automotive OEMs in lightweight composite solutions for electric vehicles.

- 2021: Significant advancements in continuous fiber-reinforced thermoplastic manufacturing processes, enabling wider adoption in structural automotive parts.

- 2022: Growing focus on developing bio-based resins and recycled glass fibers for more sustainable composite solutions.

- 2023: Introduction of advanced composite materials for enhanced battery enclosure systems in electric vehicles.

- 2024: Strategic acquisitions and partnerships aimed at expanding production capacity for automotive-grade glass fiber composites.

In-Depth Automotive Glass Fiber Composites Market Outlook

The future outlook for the automotive glass fiber composites market is exceptionally promising, driven by the transformative shifts in the automotive industry. Growth accelerators like the ongoing electrification of vehicles, stringent global emissions regulations, and a rising consumer demand for sustainable and high-performance mobility solutions will continue to fuel market expansion. Strategic opportunities lie in further developing cost-effective manufacturing processes, enhancing the recyclability of composites to meet circular economy mandates, and expanding their application into increasingly complex and safety-critical structural components. The industry is well-positioned to become a cornerstone of modern vehicle design, contributing significantly to lighter, safer, and more environmentally friendly automobiles.

Automotive Glass Fiber Composites Segmentation

-

1. Application

- 1.1. Automotive Body & Roof Panels

- 1.2. Automotive Hood

- 1.3. Automotive Chassis

- 1.4. Interiors and Others

-

2. Types

- 2.1. Thermosetting Plastic Products

- 2.2. Thermoplastic Plastic Products

Automotive Glass Fiber Composites Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Glass Fiber Composites Regional Market Share

Geographic Coverage of Automotive Glass Fiber Composites

Automotive Glass Fiber Composites REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Automotive Body & Roof Panels

- 5.1.2. Automotive Hood

- 5.1.3. Automotive Chassis

- 5.1.4. Interiors and Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Thermosetting Plastic Products

- 5.2.2. Thermoplastic Plastic Products

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Automotive Glass Fiber Composites Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Automotive Body & Roof Panels

- 6.1.2. Automotive Hood

- 6.1.3. Automotive Chassis

- 6.1.4. Interiors and Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Thermosetting Plastic Products

- 6.2.2. Thermoplastic Plastic Products

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Automotive Glass Fiber Composites Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Automotive Body & Roof Panels

- 7.1.2. Automotive Hood

- 7.1.3. Automotive Chassis

- 7.1.4. Interiors and Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Thermosetting Plastic Products

- 7.2.2. Thermoplastic Plastic Products

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Automotive Glass Fiber Composites Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Automotive Body & Roof Panels

- 8.1.2. Automotive Hood

- 8.1.3. Automotive Chassis

- 8.1.4. Interiors and Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Thermosetting Plastic Products

- 8.2.2. Thermoplastic Plastic Products

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Automotive Glass Fiber Composites Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Automotive Body & Roof Panels

- 9.1.2. Automotive Hood

- 9.1.3. Automotive Chassis

- 9.1.4. Interiors and Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Thermosetting Plastic Products

- 9.2.2. Thermoplastic Plastic Products

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Automotive Glass Fiber Composites Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Automotive Body & Roof Panels

- 10.1.2. Automotive Hood

- 10.1.3. Automotive Chassis

- 10.1.4. Interiors and Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Thermosetting Plastic Products

- 10.2.2. Thermoplastic Plastic Products

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Automotive Glass Fiber Composites Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Automotive Body & Roof Panels

- 11.1.2. Automotive Hood

- 11.1.3. Automotive Chassis

- 11.1.4. Interiors and Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Thermosetting Plastic Products

- 11.2.2. Thermoplastic Plastic Products

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 BASF

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Lanxess

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 SABIC

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Evonik

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 DSM

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Avient

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 DuPont

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 DOMO Chemicals

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Hexion

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Celanese

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 RTP

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Sumitomo Bakelite

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Lotte Chemical

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Daicel

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Kolon

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Denka

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Kingfa

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.1 BASF

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Automotive Glass Fiber Composites Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Glass Fiber Composites Revenue (million), by Application 2025 & 2033

- Figure 3: North America Automotive Glass Fiber Composites Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Glass Fiber Composites Revenue (million), by Types 2025 & 2033

- Figure 5: North America Automotive Glass Fiber Composites Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automotive Glass Fiber Composites Revenue (million), by Country 2025 & 2033

- Figure 7: North America Automotive Glass Fiber Composites Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Glass Fiber Composites Revenue (million), by Application 2025 & 2033

- Figure 9: South America Automotive Glass Fiber Composites Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Glass Fiber Composites Revenue (million), by Types 2025 & 2033

- Figure 11: South America Automotive Glass Fiber Composites Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automotive Glass Fiber Composites Revenue (million), by Country 2025 & 2033

- Figure 13: South America Automotive Glass Fiber Composites Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Glass Fiber Composites Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Automotive Glass Fiber Composites Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Glass Fiber Composites Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Automotive Glass Fiber Composites Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automotive Glass Fiber Composites Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Automotive Glass Fiber Composites Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Glass Fiber Composites Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Glass Fiber Composites Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Glass Fiber Composites Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automotive Glass Fiber Composites Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automotive Glass Fiber Composites Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Glass Fiber Composites Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Glass Fiber Composites Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Glass Fiber Composites Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Glass Fiber Composites Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Automotive Glass Fiber Composites Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automotive Glass Fiber Composites Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Glass Fiber Composites Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Glass Fiber Composites Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Glass Fiber Composites Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Automotive Glass Fiber Composites Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Glass Fiber Composites Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Glass Fiber Composites Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Automotive Glass Fiber Composites Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Glass Fiber Composites Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Glass Fiber Composites Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Automotive Glass Fiber Composites Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Glass Fiber Composites Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Glass Fiber Composites Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Automotive Glass Fiber Composites Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Glass Fiber Composites Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Glass Fiber Composites Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Automotive Glass Fiber Composites Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Glass Fiber Composites Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Glass Fiber Composites Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Automotive Glass Fiber Composites Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Glass Fiber Composites Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Glass Fiber Composites?

The projected CAGR is approximately 5.4%.

2. Which companies are prominent players in the Automotive Glass Fiber Composites?

Key companies in the market include BASF, Lanxess, SABIC, Evonik, DSM, Avient, DuPont, DOMO Chemicals, Hexion, Celanese, RTP, Sumitomo Bakelite, Lotte Chemical, Daicel, Kolon, Denka, Kingfa.

3. What are the main segments of the Automotive Glass Fiber Composites?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 4490 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Glass Fiber Composites," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Glass Fiber Composites report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Glass Fiber Composites?

To stay informed about further developments, trends, and reports in the Automotive Glass Fiber Composites, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence