Key Insights

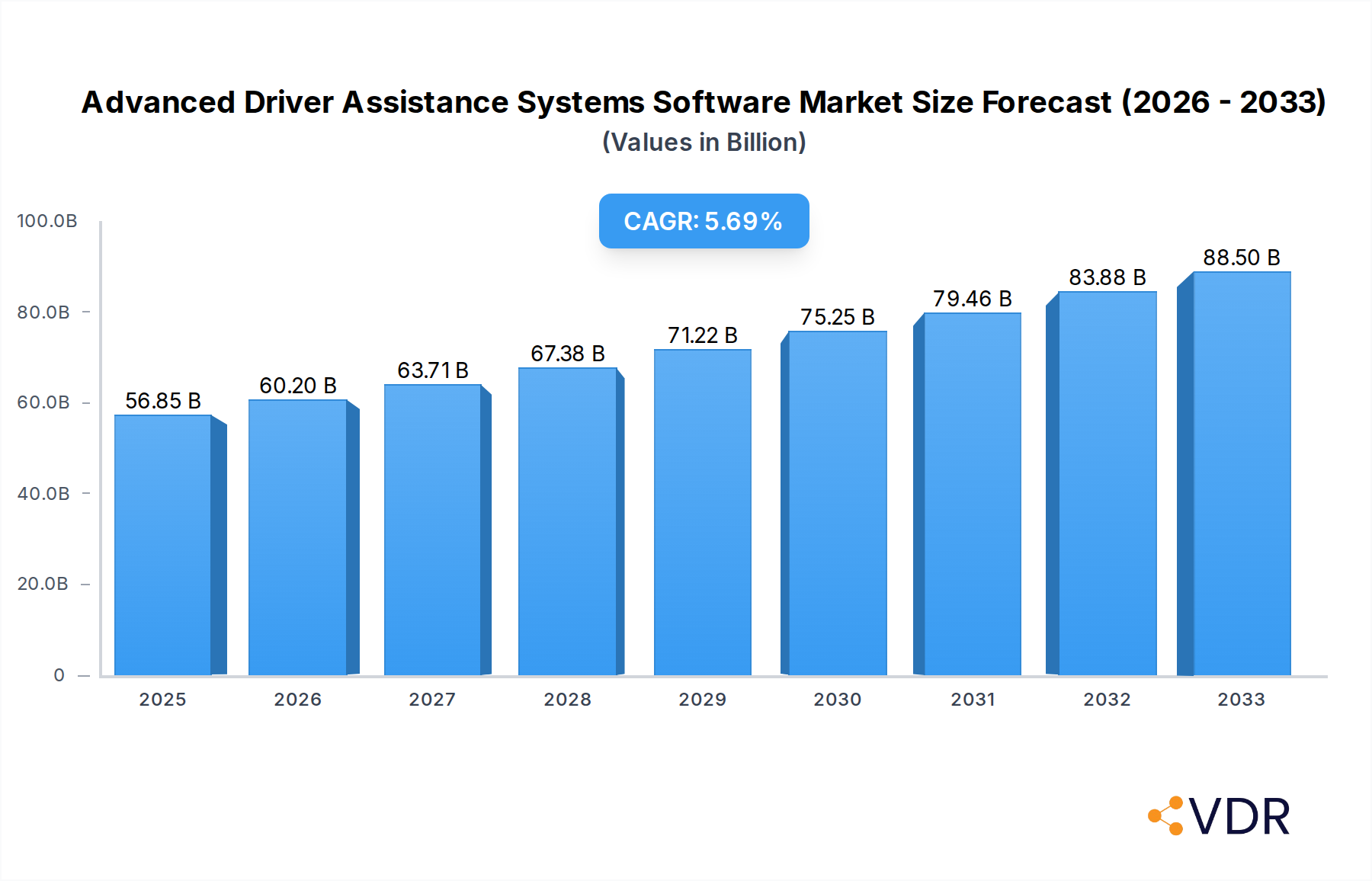

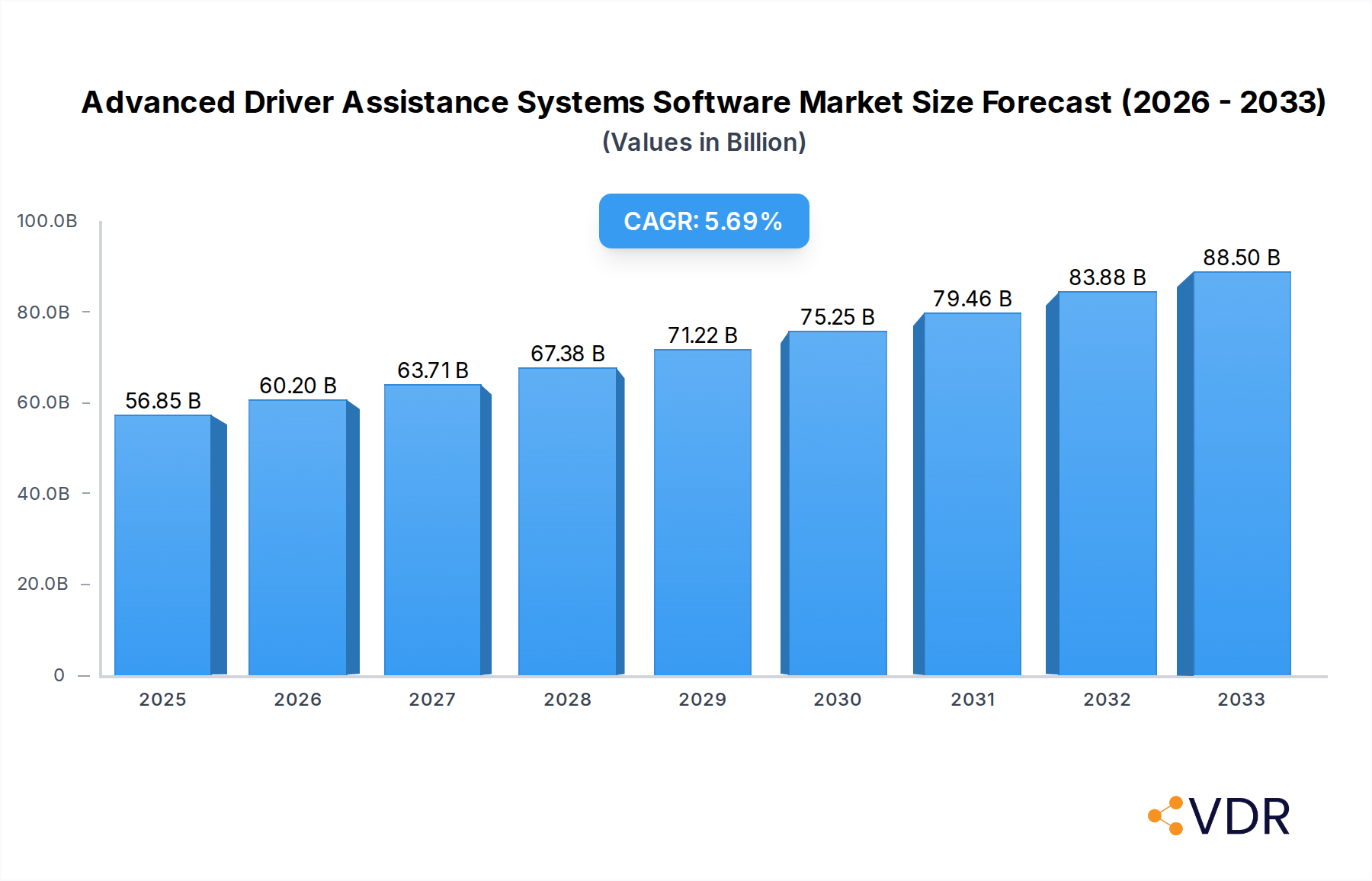

The global market for Advanced Driver Assistance Systems (ADAS) software is poised for substantial growth, driven by increasing consumer demand for enhanced safety features and regulatory mandates pushing for safer vehicles. With a current market size estimated at 56,850 million USD in 2025, the sector is projected to expand at a robust Compound Annual Growth Rate (CAGR) of 5.9% through 2033. This upward trajectory is fueled by critical drivers such as the relentless pursuit of accident reduction, the integration of AI and machine learning for more sophisticated ADAS functionalities, and the accelerating adoption of autonomous driving technologies. The passenger car segment is expected to lead this expansion, owing to the high volume of vehicle production and consumer preference for advanced safety suites. Furthermore, the growing complexity of vehicle electronics and the need for seamless integration of various ADAS components are pushing the market towards cloud-based and web-based software solutions, offering scalability, over-the-air updates, and advanced data analytics capabilities.

Advanced Driver Assistance Systems Software Market Size (In Billion)

The market is characterized by a dynamic competitive landscape with key players like Continental Automotive, Harman, and Intellias investing heavily in research and development to offer innovative ADAS software solutions. Emerging trends include the development of sophisticated sensor fusion algorithms, enhanced human-machine interface (HMI) for better driver interaction, and the increasing use of sophisticated AI for predictive safety. However, the market also faces restraints such as the high cost of implementation and integration for certain ADAS features, potential cybersecurity vulnerabilities in connected vehicle systems, and the need for extensive validation and testing to ensure reliability. Despite these challenges, the overarching trend towards a safer and more automated driving experience, coupled with supportive government initiatives and technological advancements, is expected to propel the ADAS software market to new heights in the coming years.

Advanced Driver Assistance Systems Software Company Market Share

Advanced Driver Assistance Systems Software Market Dynamics & Structure

The Advanced Driver Assistance Systems (ADAS) software market is characterized by a moderately concentrated landscape, driven by relentless technological innovation and evolving regulatory frameworks. Key innovation drivers include the pursuit of enhanced vehicle safety, the escalating demand for autonomous driving capabilities, and the integration of AI and machine learning for sophisticated perception and decision-making. Stricter safety mandates globally, particularly in Europe and North America, are pushing automakers to adopt ADAS features, thereby fueling market growth. Competitive product substitutes, though nascent, include advanced aftermarket solutions and the potential for integrated vehicle platforms that consolidate ADAS functionalities. End-user demographics show a growing preference among tech-savvy consumers and fleet operators for vehicles equipped with advanced safety and convenience features. Mergers & Acquisitions (M&A) are a significant trend, with major automotive suppliers and technology companies acquiring specialized ADAS software firms to bolster their portfolios and gain market share. For instance, M&A deal volumes have seen a consistent increase, with an estimated XX deals in the historical period. Innovation barriers include the high cost of R&D, the need for extensive validation and testing to ensure functional safety, and the complexities of cybersecurity threats.

- Market Concentration: Moderately concentrated, with leading players holding significant market share but ample room for specialized and emerging companies.

- Technological Innovation Drivers: AI/ML integration, sensor fusion, V2X communication, over-the-air (OTA) updates, and advanced perception algorithms.

- Regulatory Frameworks: Euro NCAP, NHTSA New Car Assessment Program (NCAP), UNECE regulations pushing for mandatory ADAS features.

- Competitive Product Substitutes: Aftermarket ADAS solutions, advanced infotainment systems with integrated safety features.

- End-User Demographics: Younger, tech-oriented car buyers, commercial fleet operators seeking cost reduction through safety, aging populations prioritizing independence.

- M&A Trends: Strategic acquisitions by Tier 1 suppliers and tech giants to secure IP, talent, and market access.

Advanced Driver Assistance Systems Software Growth Trends & Insights

The global Advanced Driver Assistance Systems (ADAS) software market is poised for substantial expansion, projected to grow from an estimated XX million units in the historical period to over XXX million units by 2033. This robust growth trajectory is underpinned by a confluence of factors, including escalating consumer demand for enhanced vehicle safety, stringent governmental regulations mandating ADAS adoption, and the relentless pace of technological advancements. The base year of 2025 serves as a critical benchmark, with the market estimated to reach XX million units, showcasing the immediate momentum. The forecast period (2025–2033) anticipates a compound annual growth rate (CAGR) of approximately XX%, driven by the increasing penetration of advanced ADAS features across all vehicle segments, from passenger cars to heavy commercial vehicles.

Technological disruptions are at the forefront of this market evolution. The integration of artificial intelligence (AI) and machine learning (ML) algorithms is revolutionizing the capabilities of ADAS, enabling more sophisticated object detection, predictive analysis, and decision-making. Sensor fusion, which combines data from multiple sensors like cameras, radar, and lidar, is becoming increasingly critical for accurate environmental perception. Furthermore, the development of cloud-based and web-based ADAS solutions is facilitating over-the-air (OTA) updates, continuous improvement of software functionalities, and enhanced data analytics for performance optimization.

Consumer behavior is also undergoing a significant shift. As awareness of ADAS benefits, such as collision avoidance, adaptive cruise control, and lane-keeping assist, grows, so does the willingness of consumers to pay for these features. This escalating demand is a primary catalyst for automakers to integrate more advanced ADAS functionalities as standard or optional equipment. The pursuit of higher levels of vehicle automation, from Level 2 (partial automation) to Level 3 (conditional automation) and beyond, is directly reliant on the advancement and widespread adoption of sophisticated ADAS software. The market penetration of ADAS software is expected to surge, moving from an estimated XX% in 2025 to over XX% by 2033, indicating a profound transformation in the automotive landscape.

The transition towards software-defined vehicles further accelerates this trend. Automakers are increasingly viewing vehicle functionality as being driven by software rather than hardware, making ADAS software a core component of vehicle architecture. This shift fosters a more agile development environment, allowing for quicker deployment of new features and functionalities, thus enhancing the overall user experience and safety. The increasing complexity and interconnectedness of vehicle systems necessitate robust and scalable ADAS software solutions, which are becoming a key differentiator for automotive manufacturers.

Dominant Regions, Countries, or Segments in Advanced Driver Assistance Systems Software

The Advanced Driver Assistance Systems (ADAS) software market is experiencing significant growth, with the Passenger Car segment emerging as the dominant force, driven by a confluence of factors that highlight its exceptional market share and growth potential. In 2025, the Passenger Car segment is estimated to account for a substantial XX% of the total ADAS software market. This dominance is attributed to several key drivers, including widespread consumer demand for enhanced safety and convenience features in personal vehicles, coupled with the increasing affordability of ADAS technologies as production scales up. Major economies in North America and Europe, along with rapidly developing Asian markets, are witnessing high adoption rates due to favorable economic policies and robust infrastructure supporting advanced automotive technologies.

Within the Application segment, Passenger Cars are characterized by a high propensity for feature adoption. This is further bolstered by stringent safety regulations and high consumer awareness campaigns that emphasize the life-saving capabilities of ADAS. For example, in North America, the National Highway Traffic Safety Administration (NHTSA) and its New Car Assessment Program (NCAP) have consistently pushed for the inclusion of advanced safety features, directly impacting the Passenger Car segment's growth. Similarly, Europe’s Euro NCAP ratings heavily influence consumer choices, prioritizing vehicles equipped with comprehensive ADAS suites. The market share of ADAS software within the Passenger Car segment is projected to reach XX% by 2033, indicating sustained and strong demand.

In terms of Type, Cloud-based ADAS software is rapidly gaining traction and is expected to become a pivotal segment, complementing the dominance of Passenger Cars. While Web-based solutions have established a strong foundation, Cloud-based platforms offer unparalleled scalability, data processing capabilities, and the potential for continuous over-the-air (OTA) updates. This allows for real-time adaptation of ADAS functionalities to evolving driving conditions and user preferences. The market share for Cloud-based ADAS software is anticipated to grow from XX% in 2025 to an impressive XX% by 2033. The ability of cloud solutions to handle vast amounts of data generated by sensors and facilitate advanced AI-driven decision-making makes them indispensable for future ADAS development, particularly for autonomous driving functionalities.

Economic policies in key automotive manufacturing hubs are also contributing to the dominance of these segments. Government incentives for electric and connected vehicles often include provisions that encourage the adoption of advanced safety features, directly benefiting the Passenger Car segment. Furthermore, investments in smart city infrastructure and V2X (Vehicle-to-Everything) communication are creating an ecosystem where advanced ADAS software can operate more effectively, further solidifying the position of Passenger Cars and the adoption of Cloud-based solutions. The growth potential is further amplified by the increasing average selling price of vehicles due to the integration of these sophisticated software systems, translating into higher revenue streams for ADAS software providers.

Advanced Driver Assistance Systems Software Product Landscape

The ADAS software product landscape is defined by continuous innovation focused on enhancing vehicle safety, driver comfort, and the foundational capabilities for autonomous driving. Key product innovations include advanced sensor fusion algorithms that seamlessly integrate data from cameras, radar, lidar, and ultrasonic sensors for a comprehensive 360-degree environmental understanding. AI-powered perception systems are enabling real-time object recognition, classification, and tracking with unprecedented accuracy. Performance metrics are continually being pushed, with reductions in latency for critical decision-making processes and improvements in the reliability and robustness of ADAS functions under diverse weather and lighting conditions. Unique selling propositions often lie in the software's ability to provide a highly personalized and adaptive driving experience, alongside its adherence to stringent functional safety standards (e.g., ISO 26262).

Key Drivers, Barriers & Challenges in Advanced Driver Assistance Systems Software

Key Drivers: The ADAS software market is propelled by escalating consumer demand for enhanced safety, stringent global safety regulations (e.g., NCAP ratings), and the ongoing pursuit of autonomous driving capabilities. Technological advancements in AI, machine learning, and sensor technology are enabling more sophisticated and reliable ADAS features. Automakers are also leveraging ADAS as a key differentiator and a pathway to future mobility services.

Barriers & Challenges: High development and validation costs, coupled with the need for extensive testing to ensure functional safety and cybersecurity, present significant barriers. Regulatory hurdles and the patchwork of international standards can slow down global deployment. Supply chain disruptions for critical hardware components and the increasing complexity of software integration within vehicle architectures are also major challenges. Furthermore, consumer trust and acceptance of ADAS technologies, particularly those with higher levels of automation, require continuous education and demonstration of reliability. The estimated impact of these challenges on market growth is approximately XX%.

Emerging Opportunities in Advanced Driver Assistance Systems Software

Emerging opportunities lie in the expansion of ADAS capabilities beyond traditional safety features to include predictive maintenance and proactive driver coaching powered by AI. The growing interest in subscription-based software models for ADAS features presents a new revenue stream for providers. Furthermore, the integration of ADAS software with smart city infrastructure and V2X communication networks opens avenues for enhanced traffic management and cooperative driving scenarios. Untapped markets in developing economies, where basic safety features are still a significant selling point, also represent substantial growth potential.

Growth Accelerators in the Advanced Driver Assistance Systems Industry

Key growth accelerators in the ADAS software industry include significant investments in R&D by automotive OEMs and Tier 1 suppliers, fostering rapid innovation. Strategic partnerships between automotive companies and technology firms are crucial for integrating cutting-edge AI and software solutions. The increasing adoption of Over-The-Air (OTA) updates allows for continuous improvement and feature enhancement of ADAS software post-purchase, driving customer satisfaction and ongoing revenue. Furthermore, the development of standardized software architectures and development platforms is streamlining the integration process and reducing time-to-market for new ADAS functionalities.

Key Players Shaping the Advanced Driver Assistance Systems Software Market

- Electrobit

- ADASENS Automotive GmbH

- Intellias

- Continental Automotive

- FAAR Industry

- Harman

- AISIN Group

- Green Hills

- Wabco

Notable Milestones in Advanced Driver Assistance Systems Software Sector

- 2022/09: Electrobit launches a new software suite for automotive cybersecurity, enhancing ADAS system protection against threats.

- 2021/04: Continental Automotive announces significant advancements in its lidar technology, crucial for next-generation ADAS.

- 2020/11: Intellias develops an AI-powered perception system that improves object detection accuracy in adverse weather conditions.

- 2019/07: AISIN Group announces strategic partnerships to bolster its ADAS software development capabilities.

In-Depth Advanced Driver Assistance Systems Software Market Outlook

The ADAS software market outlook is exceptionally positive, driven by ongoing technological breakthroughs and an expanding ecosystem of interconnected automotive systems. The relentless pursuit of higher levels of driving automation, coupled with a strong emphasis on consumer safety and regulatory mandates, will continue to fuel demand for sophisticated ADAS software. Strategic collaborations between software developers, automotive manufacturers, and sensor providers will be instrumental in accelerating the pace of innovation. The increasing adoption of software-defined vehicles signifies a fundamental shift, positioning ADAS software as a core enabler of future automotive experiences and a significant contributor to revenue growth and market expansion.

Advanced Driver Assistance Systems Software Segmentation

-

1. Application

- 1.1. Passenger Car

- 1.2. LCV

- 1.3. HCV

-

2. Type

- 2.1. Cloud-based

- 2.2. Web-based

Advanced Driver Assistance Systems Software Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

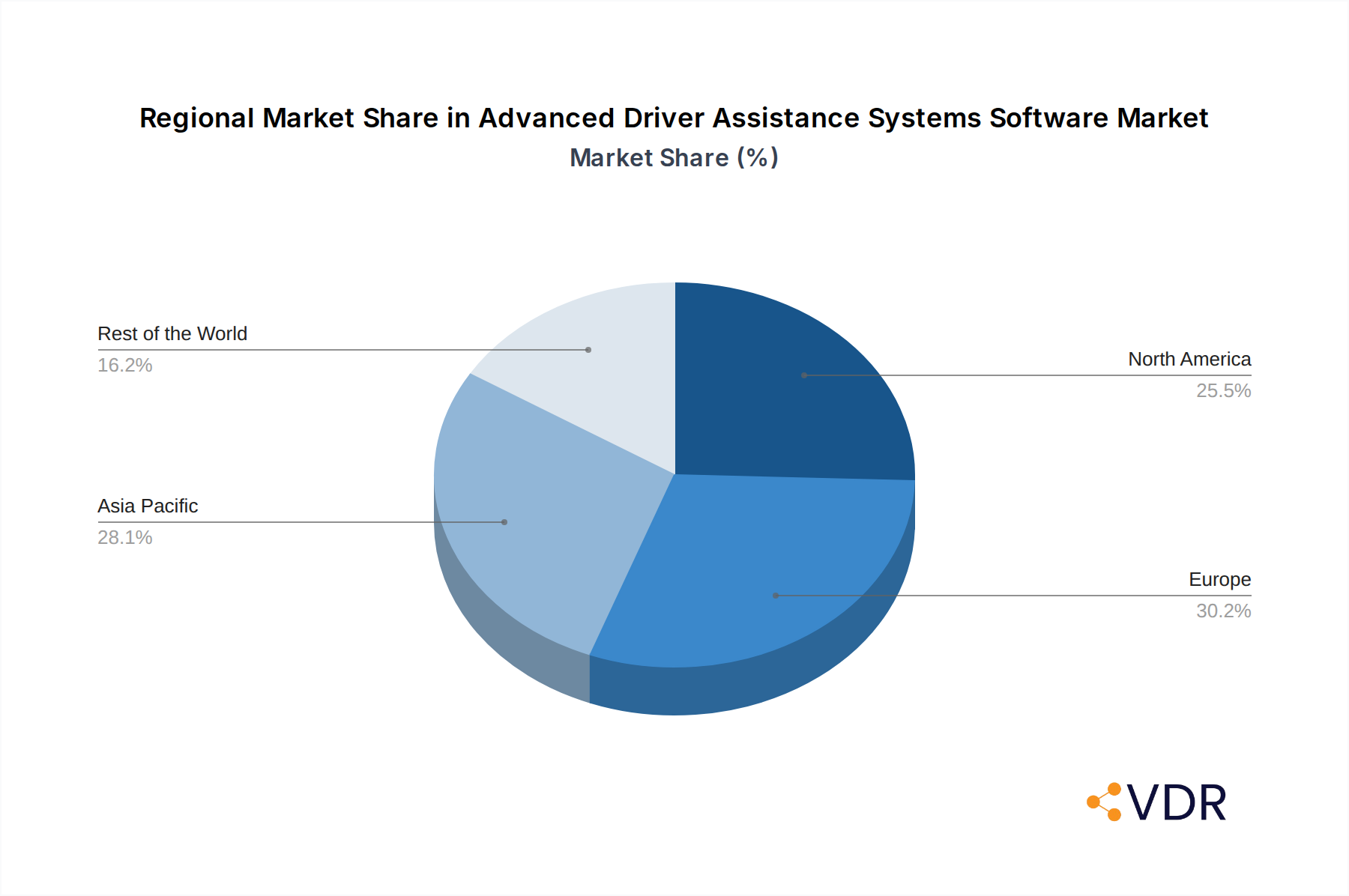

Advanced Driver Assistance Systems Software Regional Market Share

Geographic Coverage of Advanced Driver Assistance Systems Software

Advanced Driver Assistance Systems Software REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Advanced Driver Assistance Systems Software Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Car

- 5.1.2. LCV

- 5.1.3. HCV

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Cloud-based

- 5.2.2. Web-based

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Advanced Driver Assistance Systems Software Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Car

- 6.1.2. LCV

- 6.1.3. HCV

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Cloud-based

- 6.2.2. Web-based

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Advanced Driver Assistance Systems Software Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Car

- 7.1.2. LCV

- 7.1.3. HCV

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Cloud-based

- 7.2.2. Web-based

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Advanced Driver Assistance Systems Software Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Car

- 8.1.2. LCV

- 8.1.3. HCV

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Cloud-based

- 8.2.2. Web-based

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Advanced Driver Assistance Systems Software Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Car

- 9.1.2. LCV

- 9.1.3. HCV

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Cloud-based

- 9.2.2. Web-based

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Advanced Driver Assistance Systems Software Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Car

- 10.1.2. LCV

- 10.1.3. HCV

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Cloud-based

- 10.2.2. Web-based

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Electrobit

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 ADASENS Automotive GmbH

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Intellias

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Continental Automotive

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 FAAR Industry

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Harman

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 AISIN Group

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Green Hills

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Wabco

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 Electrobit

List of Figures

- Figure 1: Global Advanced Driver Assistance Systems Software Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Advanced Driver Assistance Systems Software Revenue (million), by Application 2025 & 2033

- Figure 3: North America Advanced Driver Assistance Systems Software Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Advanced Driver Assistance Systems Software Revenue (million), by Type 2025 & 2033

- Figure 5: North America Advanced Driver Assistance Systems Software Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Advanced Driver Assistance Systems Software Revenue (million), by Country 2025 & 2033

- Figure 7: North America Advanced Driver Assistance Systems Software Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Advanced Driver Assistance Systems Software Revenue (million), by Application 2025 & 2033

- Figure 9: South America Advanced Driver Assistance Systems Software Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Advanced Driver Assistance Systems Software Revenue (million), by Type 2025 & 2033

- Figure 11: South America Advanced Driver Assistance Systems Software Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Advanced Driver Assistance Systems Software Revenue (million), by Country 2025 & 2033

- Figure 13: South America Advanced Driver Assistance Systems Software Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Advanced Driver Assistance Systems Software Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Advanced Driver Assistance Systems Software Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Advanced Driver Assistance Systems Software Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Advanced Driver Assistance Systems Software Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Advanced Driver Assistance Systems Software Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Advanced Driver Assistance Systems Software Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Advanced Driver Assistance Systems Software Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Advanced Driver Assistance Systems Software Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Advanced Driver Assistance Systems Software Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Advanced Driver Assistance Systems Software Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Advanced Driver Assistance Systems Software Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Advanced Driver Assistance Systems Software Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Advanced Driver Assistance Systems Software Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Advanced Driver Assistance Systems Software Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Advanced Driver Assistance Systems Software Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Advanced Driver Assistance Systems Software Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Advanced Driver Assistance Systems Software Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Advanced Driver Assistance Systems Software Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Advanced Driver Assistance Systems Software Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Advanced Driver Assistance Systems Software Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Advanced Driver Assistance Systems Software Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Advanced Driver Assistance Systems Software Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Advanced Driver Assistance Systems Software Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Advanced Driver Assistance Systems Software Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Advanced Driver Assistance Systems Software Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Advanced Driver Assistance Systems Software Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Advanced Driver Assistance Systems Software Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Advanced Driver Assistance Systems Software Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Advanced Driver Assistance Systems Software Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Advanced Driver Assistance Systems Software Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Advanced Driver Assistance Systems Software Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Advanced Driver Assistance Systems Software Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Advanced Driver Assistance Systems Software Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Advanced Driver Assistance Systems Software Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Advanced Driver Assistance Systems Software Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Advanced Driver Assistance Systems Software Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Advanced Driver Assistance Systems Software Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Advanced Driver Assistance Systems Software?

The projected CAGR is approximately 5.9%.

2. Which companies are prominent players in the Advanced Driver Assistance Systems Software?

Key companies in the market include Electrobit, ADASENS Automotive GmbH, Intellias, Continental Automotive, FAAR Industry, Harman, AISIN Group, Green Hills, Wabco.

3. What are the main segments of the Advanced Driver Assistance Systems Software?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 56850 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Advanced Driver Assistance Systems Software," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Advanced Driver Assistance Systems Software report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Advanced Driver Assistance Systems Software?

To stay informed about further developments, trends, and reports in the Advanced Driver Assistance Systems Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence