Key Insights

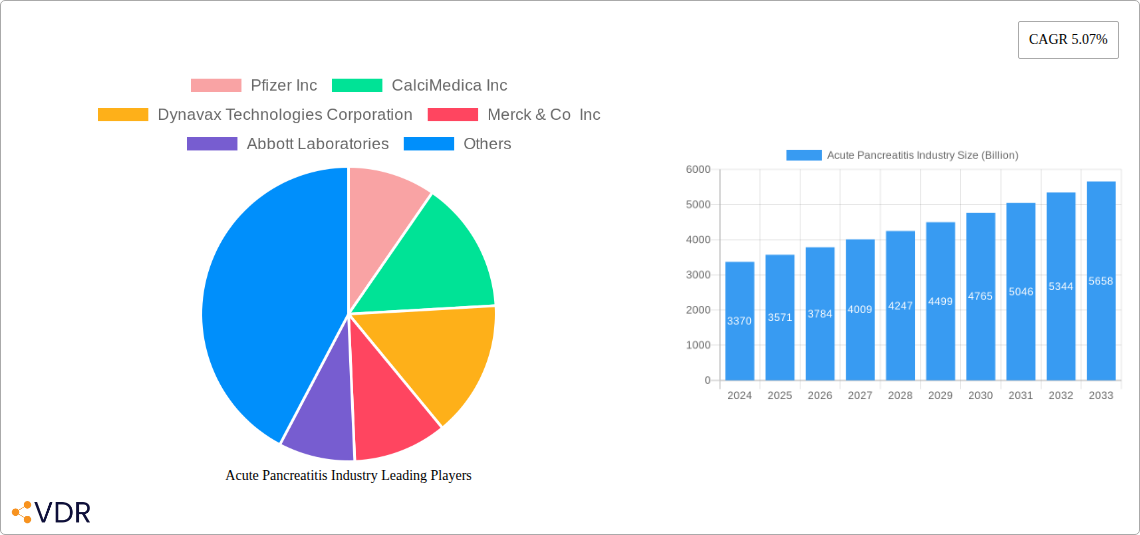

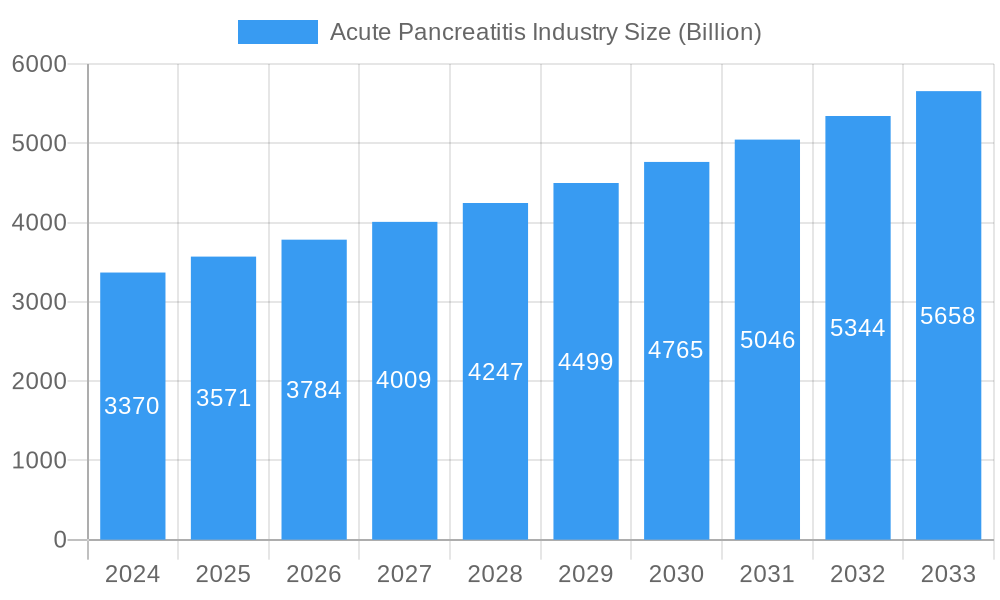

The global Acute Pancreatitis market is poised for significant expansion, with a current market size of USD 3.37 billion in 2024. Projections indicate a robust Compound Annual Growth Rate (CAGR) of 5.8% from 2025 to 2033, underscoring a period of sustained development and increasing demand for effective treatment solutions. This growth is primarily fueled by a confluence of factors, including the rising global incidence of pancreatitis driven by lifestyle changes such as poor dietary habits and alcohol consumption, alongside an aging population that is more susceptible to chronic conditions. Advancements in diagnostic tools, leading to earlier and more accurate detection of acute pancreatitis, also contribute to market momentum. Furthermore, an increasing focus on minimally invasive treatment modalities and the development of novel therapeutic agents are expected to drive market penetration and adoption, creating a dynamic environment for stakeholders.

Acute Pancreatitis Industry Market Size (In Billion)

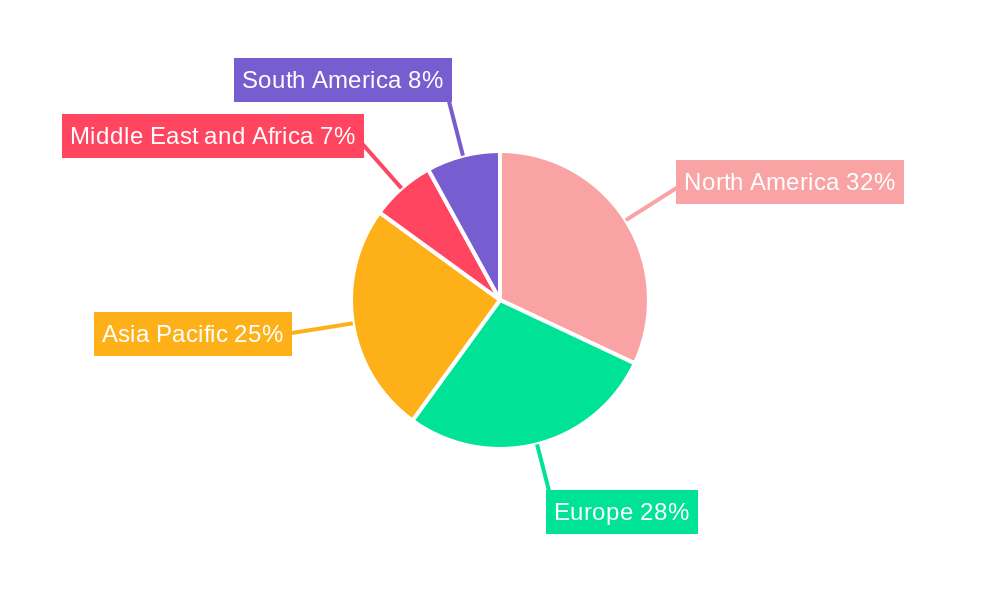

The market landscape for acute pancreatitis is characterized by a diverse range of treatment approaches and a broad spectrum of end-users. Drug-based therapies, encompassing analgesics and antibiotics, represent a foundational segment. However, the market is witnessing a growing prominence of device-based therapies, such as intravenous fluids and endoscopic procedures, which offer more targeted interventions and potentially faster recovery times. Nutritional support plays a crucial role in patient management, while surgical interventions and antioxidant treatments, though perhaps less frequent, remain vital for severe cases. Hospitals and clinics are the primary end-users, demanding sophisticated diagnostic and treatment technologies. Key industry players like Pfizer Inc., Abbott Laboratories, and Merck & Co. Inc. are actively engaged in research and development, introducing innovative products and expanding their market reach across major regions including North America, Europe, and Asia Pacific, indicating a competitive yet opportunity-rich environment.

Acute Pancreatitis Industry Company Market Share

Report Description: Acute Pancreatitis Industry Analysis 2024-2033

This comprehensive report offers an in-depth analysis of the Acute Pancreatitis Industry, providing critical insights into market dynamics, growth trends, and future opportunities. Spanning the study period of 2019–2033, with a base year of 2025, this report leverages extensive data from 2019–2024 to present a robust forecast for the market. Focusing on high-traffic keywords such as acute pancreatitis treatment, pancreatitis drugs, pancreatitis devices, hospital acquired pancreatitis, pancreatitis management, and pancreatitis therapeutics, this analysis is designed to maximize search engine visibility and engage industry professionals, including researchers, clinicians, pharmaceutical manufacturers, medical device companies, and investors. We delve into both the parent and child markets, offering a granular view of the landscape. All monetary values are presented in billions of U.S. dollars.

Acute Pancreatitis Industry Market Dynamics & Structure

The acute pancreatitis market exhibits a moderately concentrated structure, driven by a blend of established pharmaceutical giants and emerging biopharmaceutical innovators. Technological innovation in drug discovery and medical device development remains a primary driver, with significant investment flowing into novel therapeutic approaches targeting the underlying mechanisms of pancreatic inflammation and necrosis. The pancreatitis drug market is particularly dynamic, with ongoing research into more effective analgesics and antibiotics to manage complications. Regulatory frameworks, primarily governed by bodies like the FDA and EMA, play a crucial role in dictating product approval pathways and market access, influencing the speed of innovation and adoption. Competitive product substitutes are evolving, with advancements in less invasive pancreatitis device therapies posing a challenge to traditional surgical interventions. End-user demographics are shifting, with an aging global population and rising incidence of metabolic diseases contributing to an increased patient pool seeking acute pancreatitis management solutions. Mergers and Acquisitions (M&A) trends are indicative of strategic consolidation, with larger companies acquiring promising smaller firms to bolster their pancreatitis therapeutics pipelines.

- Market Concentration: Dominated by a mix of large pharmaceutical companies and specialized biotechs, indicating potential for both competition and collaboration.

- Technological Innovation: Driven by advancements in understanding pancreatic pathophysiology, leading to new drug targets and improved delivery systems for pancreatitis treatment.

- Regulatory Landscape: Stringent approval processes are in place, influencing R&D investments and time-to-market for new pancreatitis drugs.

- Competitive Substitutes: The rise of advanced pancreatitis devices and supportive care offers alternatives to traditional treatments.

- End-User Demographics: Increasing prevalence of risk factors like gallstones and alcohol abuse, alongside an aging population, is expanding the patient base for pancreatitis management.

- M&A Activity: Key players are actively engaging in strategic acquisitions to expand their product portfolios and secure market position in the acute pancreatitis market.

Acute Pancreatitis Industry Growth Trends & Insights

The acute pancreatitis industry is poised for significant expansion, driven by a confluence of factors that underscore its growing importance in global healthcare. Market size evolution has been steady, with a projected Compound Annual Growth Rate (CAGR) of approximately 6.5% from the base year 2025 through 2033. This growth is propelled by an increasing incidence of acute pancreatitis globally, attributed to lifestyle changes, rising rates of obesity, and improved diagnostic capabilities leading to earlier detection. Adoption rates of novel pancreatitis treatments are accelerating as clinical evidence supporting their efficacy and safety solidifies, particularly for drug-based therapies and advanced medical devices. Technological disruptions are a key theme, with significant progress in understanding the inflammatory cascade and developing targeted therapies. For instance, the development of novel protease inhibitors and anti-inflammatory agents is transforming the therapeutic landscape beyond basic symptom management.

Consumer behavior shifts are also influencing the market. Patients are increasingly seeking minimally invasive procedures and personalized treatment plans, favoring device-based therapy options like continuous intravenous fluid administration and endoscopic interventions over more aggressive surgical approaches where appropriate. This trend is supported by healthcare providers who are prioritizing early intervention and multidisciplinary care to mitigate complications and reduce mortality rates associated with severe acute pancreatitis. The pancreatitis drug market, in particular, is experiencing innovation in the development of agents that can modulate the inflammatory response, reduce pancreatic necrosis, and prevent systemic complications. The pancreatitis device market is witnessing advancements in fluid management systems and imaging technologies that aid in diagnosis and treatment guidance. The forecast period from 2025 to 2033 is expected to see sustained market penetration of these advanced solutions, leading to improved patient outcomes and a more robust acute pancreatitis therapeutics ecosystem. The market size in the base year 2025 is estimated to be approximately $18.5 billion, projected to reach $31.2 billion by 2033.

Dominant Regions, Countries, or Segments in Acute Pancreatitis Industry

The acute pancreatitis industry is experiencing robust growth across various regions and segments, with North America and Europe currently leading the market due to established healthcare infrastructures, high healthcare expenditure, and a strong presence of leading pharmaceutical and medical device companies. The drug-based therapy segment, particularly analgesics and antibiotics for managing pain and preventing infections, dominates the treatment type landscape, reflecting the immediate needs in acute pancreatitis care. However, device-based therapy, encompassing critical interventions like intravenous fluids for resuscitation and endoscopic procedures for managing complications such as pseudocysts, is experiencing rapid expansion, driven by technological advancements and a preference for less invasive approaches. The nutritional support segment is also crucial, ensuring adequate caloric intake and preventing malnutrition in patients with severe pancreatitis.

Within end-users, hospitals represent the largest market share, as they are equipped to handle the complex critical care requirements of acute pancreatitis patients, including intensive care units (ICUs) and specialized surgical teams. Clinics also play a role, particularly in outpatient management of mild cases and follow-up care. The other end-users category, which includes specialized treatment centers and long-term care facilities, is also gaining traction as the management of chronic pancreatitis sequelae becomes more sophisticated. The market growth in these segments is underpinned by several key drivers. In North America, extensive R&D investments, favorable reimbursement policies, and a high prevalence of risk factors such as gallstones and alcohol abuse contribute to market dominance. Europe mirrors these trends with advanced healthcare systems and a commitment to adopting innovative pancreatitis treatments. Emerging economies in Asia-Pacific are expected to exhibit the highest growth potential due to increasing healthcare access, a rising incidence of metabolic diseases, and growing awareness of acute pancreatitis. Economic policies supporting healthcare infrastructure development and technological adoption are critical in these regions.

- Dominant Region: North America and Europe, driven by advanced healthcare systems and R&D investments.

- Leading Segment (Treatment Type): Drug-Based Therapy (Analgesics, Antibiotics), followed by Device-Based Therapy.

- Key Drivers (Treatment Type): Need for pain and infection control, advancements in fluid management, and minimally invasive procedures.

- Dominant End-User: Hospitals, due to the critical care requirements of acute pancreatitis.

- Growth Potential: Asia-Pacific is projected to be the fastest-growing region due to expanding healthcare access and rising disease prevalence.

- Influencing Factors: Economic policies, healthcare infrastructure development, and technological adoption rates.

Acute Pancreatitis Industry Product Landscape

The acute pancreatitis industry product landscape is characterized by a diverse range of pharmaceuticals, medical devices, and supportive care solutions designed to manage pain, reduce inflammation, prevent complications, and support recovery. Key product innovations include novel analgesics offering improved pain relief with fewer side effects, and advanced antibiotics specifically targeting the pathogens most commonly associated with pancreatic infections. In the device-based therapy arena, sophisticated intravenous fluid management systems ensure optimal hydration and organ perfusion, while minimally invasive endoscopic tools facilitate the drainage of pseudocysts and removal of gallstones, significantly reducing the need for traditional surgery. Nutritional support products, ranging from specialized enteral feeding formulas to parenteral nutrition solutions, are crucial for maintaining patient well-being. The ongoing development of targeted antioxidant treatments and immunomodulatory agents represents a frontier in preventing pancreatic necrosis and systemic inflammatory response.

Key Drivers, Barriers & Challenges in Acute Pancreatitis Industry

The acute pancreatitis industry is propelled by several key drivers. The increasing global incidence of acute pancreatitis, fueled by lifestyle factors such as poor diet and high alcohol consumption, directly expands the patient pool. Advancements in medical technology and drug discovery are leading to more effective pancreatitis treatments, improving patient outcomes and driving market growth. Enhanced diagnostic capabilities allow for earlier and more accurate identification of the condition, facilitating timely intervention.

Conversely, the industry faces significant barriers and challenges. The high cost of advanced medical devices and novel drug therapies can limit accessibility, particularly in resource-constrained regions. Complex regulatory approval processes for new pancreatitis drugs and devices can prolong development timelines and increase R&D expenses. The lack of a definitive cure for severe acute pancreatitis and the persistent risk of complications and mortality remain major challenges, necessitating ongoing research and development.

- Key Drivers:

- Rising global incidence of acute pancreatitis.

- Technological advancements in drug and device development.

- Improved diagnostic accuracy and early detection.

- Growing demand for minimally invasive pancreatitis treatments.

- Barriers & Challenges:

- High cost of advanced therapies and devices.

- Stringent regulatory pathways.

- Complex disease pathophysiology and risk of complications.

- Limited market penetration in developing economies.

- Shortage of skilled healthcare professionals in specialized care.

Emerging Opportunities in Acute Pancreatitis Industry

Emerging opportunities in the acute pancreatitis industry are largely centered around personalized medicine and the development of novel therapeutic targets. Research into the microbiome's role in pancreatitis offers potential for innovative treatment strategies. The increasing adoption of telehealth and remote monitoring solutions presents opportunities for better patient management and follow-up care, especially for chronic pancreatitis patients. Furthermore, a growing focus on preventative strategies, including public health initiatives and early intervention for high-risk individuals, could reshape the market. The development of biomarkers for predicting disease severity and guiding treatment decisions also represents a significant untapped market.

Growth Accelerators in the Acute Pancreatitis Industry Industry

Several catalysts are accelerating long-term growth in the acute pancreatitis industry. Technological breakthroughs in understanding pancreatic injury mechanisms are paving the way for targeted therapies with improved efficacy. Strategic partnerships between pharmaceutical companies, medical device manufacturers, and research institutions are fostering innovation and accelerating product development. Market expansion strategies, particularly into emerging economies with growing healthcare needs, are opening new avenues for revenue generation. The increasing emphasis on value-based healthcare is also encouraging the development of cost-effective and outcome-driven pancreatitis management solutions.

Key Players Shaping the Acute Pancreatitis Industry Market

- Pfizer Inc

- CalciMedica Inc

- Dynavax Technologies Corporation

- Merck & Co Inc

- Abbott Laboratories

- Fresenius SE & Co KGaA

- GlaxoSmithKline

- Baxter International Inc

- SCM Lifescience

- B Braun SE

- Olympus Corporation

Notable Milestones in Acute Pancreatitis Industry Sector

- December 2022: CalciMedica, Inc. is conducting a Phase II clinical dose-ranging study of Auxora in patients with acute pancreatitis and accompanying systemic inflammatory response syndrome, indicating promising development in novel therapeutic agents.

- March 2022: AcelRx Pharmaceuticals, Inc. presented comparative data between two different dialysis circuit anticoagulants, Nafamostat and citrate anticoagulation (RCA), in pediatric patients undergoing continuous renal replacement therapy (CRRT). Nafamostat is a serine protease inhibitor used to treat acute pancreatitis, highlighting its continued relevance and evaluation in critical care settings.

In-Depth Acute Pancreatitis Industry Market Outlook

The future outlook for the acute pancreatitis industry is exceptionally promising, driven by persistent growth accelerators. Continued investment in research and development, particularly in the areas of regenerative medicine and targeted anti-inflammatory therapies, will unlock new avenues for treatment. Strategic collaborations and potential mergers will further consolidate market expertise and resource allocation, leading to accelerated innovation. The expansion into underserved geographical markets, coupled with increasing healthcare expenditure in these regions, will broaden the reach of advanced pancreatitis treatments. Moreover, the growing emphasis on patient-centric care and preventative measures presents a significant opportunity to improve global health outcomes and reduce the burden of acute pancreatitis. The market is anticipated to witness substantial growth, driven by unmet clinical needs and a robust pipeline of innovative pancreatitis therapeutics and devices.

Acute Pancreatitis Industry Segmentation

-

1. Treatment Type

-

1.1. Drug -Based Therapy

- 1.1.1. Analgesics

- 1.1.2. Anitibiotics

-

1.2. Device-Based Therapy

- 1.2.1. Intravenous Fluids

- 1.2.2. Endoscop

- 1.3. Nutritional Support

- 1.4. Others (Surgery, Antioxidant Treatment)

-

1.1. Drug -Based Therapy

-

2. End Users

- 2.1. Hospitals

- 2.2. Clinics

- 2.3. Other End-Users

Acute Pancreatitis Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Acute Pancreatitis Industry Regional Market Share

Geographic Coverage of Acute Pancreatitis Industry

Acute Pancreatitis Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Treatment Type

- 5.1.1. Drug -Based Therapy

- 5.1.1.1. Analgesics

- 5.1.1.2. Anitibiotics

- 5.1.2. Device-Based Therapy

- 5.1.2.1. Intravenous Fluids

- 5.1.2.2. Endoscop

- 5.1.3. Nutritional Support

- 5.1.4. Others (Surgery, Antioxidant Treatment)

- 5.1.1. Drug -Based Therapy

- 5.2. Market Analysis, Insights and Forecast - by End Users

- 5.2.1. Hospitals

- 5.2.2. Clinics

- 5.2.3. Other End-Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Treatment Type

- 6. Global Acute Pancreatitis Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Treatment Type

- 6.1.1. Drug -Based Therapy

- 6.1.1.1. Analgesics

- 6.1.1.2. Anitibiotics

- 6.1.2. Device-Based Therapy

- 6.1.2.1. Intravenous Fluids

- 6.1.2.2. Endoscop

- 6.1.3. Nutritional Support

- 6.1.4. Others (Surgery, Antioxidant Treatment)

- 6.1.1. Drug -Based Therapy

- 6.2. Market Analysis, Insights and Forecast - by End Users

- 6.2.1. Hospitals

- 6.2.2. Clinics

- 6.2.3. Other End-Users

- 6.1. Market Analysis, Insights and Forecast - by Treatment Type

- 7. North America Acute Pancreatitis Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Treatment Type

- 7.1.1. Drug -Based Therapy

- 7.1.1.1. Analgesics

- 7.1.1.2. Anitibiotics

- 7.1.2. Device-Based Therapy

- 7.1.2.1. Intravenous Fluids

- 7.1.2.2. Endoscop

- 7.1.3. Nutritional Support

- 7.1.4. Others (Surgery, Antioxidant Treatment)

- 7.1.1. Drug -Based Therapy

- 7.2. Market Analysis, Insights and Forecast - by End Users

- 7.2.1. Hospitals

- 7.2.2. Clinics

- 7.2.3. Other End-Users

- 7.1. Market Analysis, Insights and Forecast - by Treatment Type

- 8. Europe Acute Pancreatitis Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Treatment Type

- 8.1.1. Drug -Based Therapy

- 8.1.1.1. Analgesics

- 8.1.1.2. Anitibiotics

- 8.1.2. Device-Based Therapy

- 8.1.2.1. Intravenous Fluids

- 8.1.2.2. Endoscop

- 8.1.3. Nutritional Support

- 8.1.4. Others (Surgery, Antioxidant Treatment)

- 8.1.1. Drug -Based Therapy

- 8.2. Market Analysis, Insights and Forecast - by End Users

- 8.2.1. Hospitals

- 8.2.2. Clinics

- 8.2.3. Other End-Users

- 8.1. Market Analysis, Insights and Forecast - by Treatment Type

- 9. Asia Pacific Acute Pancreatitis Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Treatment Type

- 9.1.1. Drug -Based Therapy

- 9.1.1.1. Analgesics

- 9.1.1.2. Anitibiotics

- 9.1.2. Device-Based Therapy

- 9.1.2.1. Intravenous Fluids

- 9.1.2.2. Endoscop

- 9.1.3. Nutritional Support

- 9.1.4. Others (Surgery, Antioxidant Treatment)

- 9.1.1. Drug -Based Therapy

- 9.2. Market Analysis, Insights and Forecast - by End Users

- 9.2.1. Hospitals

- 9.2.2. Clinics

- 9.2.3. Other End-Users

- 9.1. Market Analysis, Insights and Forecast - by Treatment Type

- 10. Middle East and Africa Acute Pancreatitis Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Treatment Type

- 10.1.1. Drug -Based Therapy

- 10.1.1.1. Analgesics

- 10.1.1.2. Anitibiotics

- 10.1.2. Device-Based Therapy

- 10.1.2.1. Intravenous Fluids

- 10.1.2.2. Endoscop

- 10.1.3. Nutritional Support

- 10.1.4. Others (Surgery, Antioxidant Treatment)

- 10.1.1. Drug -Based Therapy

- 10.2. Market Analysis, Insights and Forecast - by End Users

- 10.2.1. Hospitals

- 10.2.2. Clinics

- 10.2.3. Other End-Users

- 10.1. Market Analysis, Insights and Forecast - by Treatment Type

- 11. South America Acute Pancreatitis Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Treatment Type

- 11.1.1. Drug -Based Therapy

- 11.1.1.1. Analgesics

- 11.1.1.2. Anitibiotics

- 11.1.2. Device-Based Therapy

- 11.1.2.1. Intravenous Fluids

- 11.1.2.2. Endoscop

- 11.1.3. Nutritional Support

- 11.1.4. Others (Surgery, Antioxidant Treatment)

- 11.1.1. Drug -Based Therapy

- 11.2. Market Analysis, Insights and Forecast - by End Users

- 11.2.1. Hospitals

- 11.2.2. Clinics

- 11.2.3. Other End-Users

- 11.1. Market Analysis, Insights and Forecast - by Treatment Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Pfizer Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 CalciMedica Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Dynavax Technologies Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Merck & Co Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Abbott Laboratories

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Fresenius SE & Co KGaA

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 GlaxoSmithKline

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Baxter International Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 SCM Lifescience*List Not Exhaustive

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 B Braun SE

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Olympus Corporation

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Pfizer Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Acute Pancreatitis Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Acute Pancreatitis Industry Revenue (billion), by Treatment Type 2025 & 2033

- Figure 3: North America Acute Pancreatitis Industry Revenue Share (%), by Treatment Type 2025 & 2033

- Figure 4: North America Acute Pancreatitis Industry Revenue (billion), by End Users 2025 & 2033

- Figure 5: North America Acute Pancreatitis Industry Revenue Share (%), by End Users 2025 & 2033

- Figure 6: North America Acute Pancreatitis Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Acute Pancreatitis Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Acute Pancreatitis Industry Revenue (billion), by Treatment Type 2025 & 2033

- Figure 9: Europe Acute Pancreatitis Industry Revenue Share (%), by Treatment Type 2025 & 2033

- Figure 10: Europe Acute Pancreatitis Industry Revenue (billion), by End Users 2025 & 2033

- Figure 11: Europe Acute Pancreatitis Industry Revenue Share (%), by End Users 2025 & 2033

- Figure 12: Europe Acute Pancreatitis Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Acute Pancreatitis Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Acute Pancreatitis Industry Revenue (billion), by Treatment Type 2025 & 2033

- Figure 15: Asia Pacific Acute Pancreatitis Industry Revenue Share (%), by Treatment Type 2025 & 2033

- Figure 16: Asia Pacific Acute Pancreatitis Industry Revenue (billion), by End Users 2025 & 2033

- Figure 17: Asia Pacific Acute Pancreatitis Industry Revenue Share (%), by End Users 2025 & 2033

- Figure 18: Asia Pacific Acute Pancreatitis Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Acute Pancreatitis Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East and Africa Acute Pancreatitis Industry Revenue (billion), by Treatment Type 2025 & 2033

- Figure 21: Middle East and Africa Acute Pancreatitis Industry Revenue Share (%), by Treatment Type 2025 & 2033

- Figure 22: Middle East and Africa Acute Pancreatitis Industry Revenue (billion), by End Users 2025 & 2033

- Figure 23: Middle East and Africa Acute Pancreatitis Industry Revenue Share (%), by End Users 2025 & 2033

- Figure 24: Middle East and Africa Acute Pancreatitis Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East and Africa Acute Pancreatitis Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Acute Pancreatitis Industry Revenue (billion), by Treatment Type 2025 & 2033

- Figure 27: South America Acute Pancreatitis Industry Revenue Share (%), by Treatment Type 2025 & 2033

- Figure 28: South America Acute Pancreatitis Industry Revenue (billion), by End Users 2025 & 2033

- Figure 29: South America Acute Pancreatitis Industry Revenue Share (%), by End Users 2025 & 2033

- Figure 30: South America Acute Pancreatitis Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: South America Acute Pancreatitis Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Acute Pancreatitis Industry Revenue billion Forecast, by Treatment Type 2020 & 2033

- Table 2: Global Acute Pancreatitis Industry Revenue billion Forecast, by End Users 2020 & 2033

- Table 3: Global Acute Pancreatitis Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Acute Pancreatitis Industry Revenue billion Forecast, by Treatment Type 2020 & 2033

- Table 5: Global Acute Pancreatitis Industry Revenue billion Forecast, by End Users 2020 & 2033

- Table 6: Global Acute Pancreatitis Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Acute Pancreatitis Industry Revenue billion Forecast, by Treatment Type 2020 & 2033

- Table 11: Global Acute Pancreatitis Industry Revenue billion Forecast, by End Users 2020 & 2033

- Table 12: Global Acute Pancreatitis Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Germany Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: France Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Italy Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Spain Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Global Acute Pancreatitis Industry Revenue billion Forecast, by Treatment Type 2020 & 2033

- Table 20: Global Acute Pancreatitis Industry Revenue billion Forecast, by End Users 2020 & 2033

- Table 21: Global Acute Pancreatitis Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 22: China Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Japan Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: India Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Australia Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: South Korea Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Acute Pancreatitis Industry Revenue billion Forecast, by Treatment Type 2020 & 2033

- Table 29: Global Acute Pancreatitis Industry Revenue billion Forecast, by End Users 2020 & 2033

- Table 30: Global Acute Pancreatitis Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 31: GCC Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: South Africa Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Rest of Middle East and Africa Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Global Acute Pancreatitis Industry Revenue billion Forecast, by Treatment Type 2020 & 2033

- Table 35: Global Acute Pancreatitis Industry Revenue billion Forecast, by End Users 2020 & 2033

- Table 36: Global Acute Pancreatitis Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 37: Brazil Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Argentina Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Rest of South America Acute Pancreatitis Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Acute Pancreatitis Industry?

The projected CAGR is approximately 5.8%.

2. Which companies are prominent players in the Acute Pancreatitis Industry?

Key companies in the market include Pfizer Inc, CalciMedica Inc, Dynavax Technologies Corporation, Merck & Co Inc, Abbott Laboratories, Fresenius SE & Co KGaA, GlaxoSmithKline, Baxter International Inc, SCM Lifescience*List Not Exhaustive, B Braun SE, Olympus Corporation.

3. What are the main segments of the Acute Pancreatitis Industry?

The market segments include Treatment Type, End Users.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.37 billion as of 2022.

5. What are some drivers contributing to market growth?

Increase in Incident Cases of Gallstone and Obesity; Ongoing Research and Development Activities for the Disease.

6. What are the notable trends driving market growth?

Intravenous Fluids Segment is Expected to Grow Over the Forecast Period.

7. Are there any restraints impacting market growth?

Poor Reimbursement policies & High cost of treatment; Stringent Regulatory standards.

8. Can you provide examples of recent developments in the market?

December 2022: CalciMedica, Inc. is conducting a Phase II clinical dose-ranging study of Auxora in patients with acute pancreatitis and accompanying systemic inflammatory response syndrome.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Acute Pancreatitis Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Acute Pancreatitis Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Acute Pancreatitis Industry?

To stay informed about further developments, trends, and reports in the Acute Pancreatitis Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence