Key Insights

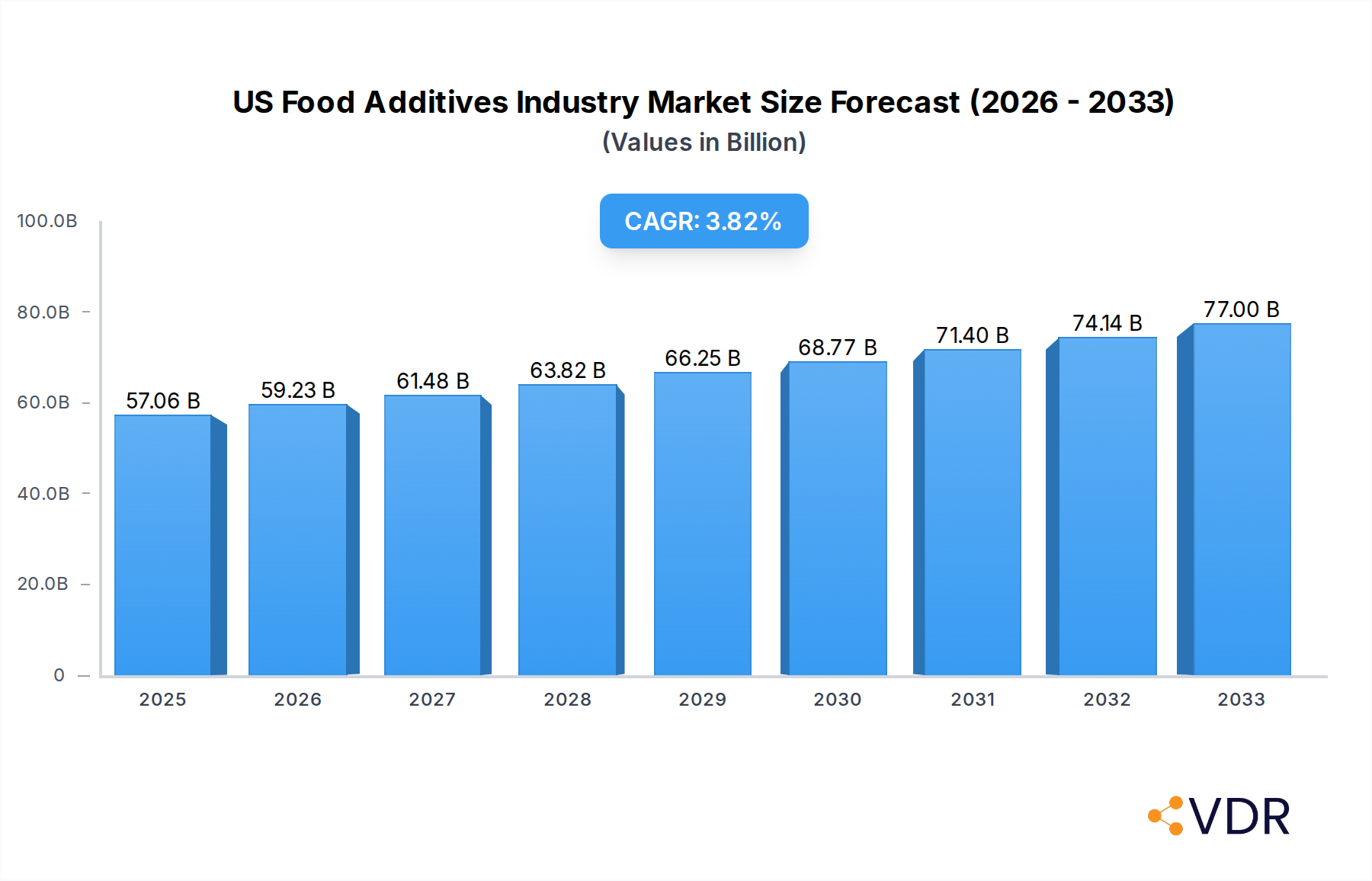

The US food additives market is poised for steady growth, driven by evolving consumer preferences for processed foods and beverages that offer enhanced shelf-life, improved texture, and desirable flavors. With an estimated market size of $57.06 billion in 2025, the industry is projected to expand at a Compound Annual Growth Rate (CAGR) of 3.8% through 2033. This growth is underpinned by a robust demand for a diverse range of additives, including preservatives that extend product freshness, sweeteners and sugar substitutes catering to the health-conscious population, and emulsifiers that improve product stability and appearance. Key applications span across confectionery, bakery products, dairy and frozen foods, and beverages, reflecting the broad integration of food additives into everyday consumer goods. Leading players such as DuPont-Danisco, Cargill Incorporated, and Novozymes are instrumental in shaping market trends through innovation and product development.

US Food Additives Industry Market Size (In Billion)

The market's expansion is further supported by an increasing focus on natural and clean-label ingredients, creating opportunities for bio-based and naturally derived food additives. However, the industry faces challenges related to stringent regulatory frameworks governing the use of certain additives and growing consumer skepticism towards artificial ingredients. Despite these hurdles, the ongoing innovation in food technology, coupled with the demand for convenience and indulgence, will continue to fuel the market's trajectory. The Asia Pacific region is expected to witness the highest growth, but North America, with its established food processing industry and significant consumer spending, will remain a dominant force. The market is dynamic, with companies continuously adapting to consumer demands for healthier, safer, and more appealing food products.

US Food Additives Industry Company Market Share

US Food Additives Industry: Market Dynamics & Structure Report Description

This comprehensive report dives deep into the US Food Additives Industry, a dynamic sector projected to reach significant growth. Analyze the intricate market structure, identifying key players like DuPont-Danisco, Cargill Incorporated, Novozymes, Kerry Inc, Archer Daniels Midland Company, Koninklijke DSM N V, Corbion NV, and Tate & Lyle. Understand the competitive landscape, technological innovation drivers, and evolving regulatory frameworks that shape the market for preservatives, sweeteners, sugar substitutes, emulsifiers, anti-caking agents, enzymes, hydrocolloids, food flavors and enhancers, food colorants, and acidulants. Explore the parent market of food ingredients and its influence on the child market of specialized additives.

- Market Concentration & Competitive Landscape: Uncover the degree of competition among major and emerging players in the US food additives market.

- Technological Innovation Drivers: Examine the role of R&D and emerging technologies in developing novel and sustainable food additive solutions.

- Regulatory Frameworks: Understand the impact of FDA regulations and evolving consumer safety standards on product development and market access.

- Competitive Product Substitutes: Analyze the availability and impact of alternative ingredients and technologies influencing consumer choices.

- End-User Demographics: Gain insights into how changing consumer preferences, such as demand for clean label and plant-based options, are reshaping the industry.

- M&A Trends: Track key merger and acquisition activities, including the recent acquisition of Tate & Lyle by Symrise in 2021, and their implications for market consolidation and innovation.

- Market Size & Value: Quantify the market size, with the US food additives market valued at an estimated $XX billion in the base year of 2025, and project its trajectory through 2033.

US Food Additives Industry Growth Trends & Insights

The US Food Additives Industry is poised for robust growth, driven by evolving consumer demands and technological advancements. This report utilizes advanced analytical tools to deliver a detailed 600-word analysis of market size evolution from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033. Delve into the adoption rates of innovative additives, particularly plant-based food additives as highlighted by DuPont-Danisco's investment in 2023. Understand the profound impact of technological disruptions, such as advancements in enzyme technology and fermentation processes, on the production and functionality of food additives. Analyze significant shifts in consumer behavior, including the increasing preference for clean label additives, exemplified by Cargill's 2022 launch of preservative-free options, and the growing demand for natural and sustainable ingredients across all application segments including confectionery, bakery products, dairy & frozen food, beverages, meat, poultry, and sea food. Quantify market penetration of key additive types and project the Compound Annual Growth Rate (CAGR) for the forecast period, providing crucial insights for strategic decision-making. Explore the interplay between the parent market for broad food ingredients and the specialized child market for high-performance food additives, understanding how innovations in one sphere influence the other.

Dominant Regions, Countries, or Segments in US Food Additives Industry

This section of the report meticulously identifies and analyzes the dominant forces within the US Food Additives Industry. It pinpoints the leading region, country, or specific segment driving market growth, offering a detailed 600-word examination. With a keen focus on the Type segments—including Preservatives, Sweetener, Sugar Substitutes, Emulsifier, Anti-Caking Agents, Enzymes, Hydrocolloids, Food Flavors and Enhancers, Food Colorants, and Acidulants—and the diverse Application segments such as Confectionery, Bakery Products, Dairy & Frozen Food, Beverages, Meat, Poultry, and Sea Food, and Others, this analysis highlights the most lucrative areas. Key drivers such as economic policies influencing food production, robust infrastructure supporting manufacturing and distribution, and evolving consumer preferences for specific product attributes are thoroughly investigated. The dominance of specific additive types, like hydrocolloids for texture modification or preservatives for extended shelf-life, is explained through their market share and growth potential, supported by data from the historical period (2019–2024) and projections for the forecast period (2025–2033). The report provides an in-depth look at why certain segments, such as Beverages or Bakery Products, are exhibiting higher demand for food additives, factoring in market size and growth trajectory.

US Food Additives Industry Product Landscape

The US Food Additives Industry is characterized by a vibrant product landscape driven by constant innovation and an increasing focus on functionality and consumer appeal. Companies are actively developing novel solutions within the Type segments, ranging from advanced preservatives that extend shelf-life without compromising taste to innovative sweeteners and sugar substitutes catering to health-conscious consumers. Significant advancements are also observed in enzymes for improved processing efficiency and in hydrocolloids for enhanced texture and stability across various applications. The demand for natural food colorants and food flavors and enhancers is on the rise, reflecting a broader trend towards cleaner labels. Performance metrics such as efficacy, stability, cost-effectiveness, and natural origin are key differentiators, influencing adoption rates in confectionery, bakery products, dairy & frozen food, beverages, meat, poultry, and sea food. Technological breakthroughs, including biotechnology and precision fermentation, are enabling the creation of specialized additives with unique selling propositions.

Key Drivers, Barriers & Challenges in US Food Additives Industry

The US Food Additives Industry is propelled by several key drivers and simultaneously faces significant barriers and challenges.

Key Drivers:

- Growing Demand for Processed and Packaged Foods: Increased consumption of convenient and ready-to-eat meals fuels the demand for additives that enhance shelf-life, texture, and flavor.

- Consumer Preference for Clean Label and Natural Ingredients: A strong shift towards minimally processed foods with recognizable ingredients is driving innovation in natural preservatives, colors, and flavors.

- Technological Advancements: Innovations in biotechnology, fermentation, and extraction processes are leading to the development of more effective, sustainable, and diverse food additives.

- Health and Wellness Trends: The rising awareness of health issues like obesity and diabetes is boosting the demand for sugar substitutes and low-calorie additives.

- Regulatory Support for Food Safety: Stringent food safety regulations necessitate the use of specific additives to prevent spoilage and ensure consumer health, creating a consistent market need.

Barriers & Challenges:

- Negative Consumer Perception and "Free-From" Trends: Public apprehension about artificial additives, often fueled by misinformation, can lead to a demand for "free-from" products, posing a challenge for traditional additive manufacturers. This has resulted in a market value impact of approximately $XX billion in lost revenue for certain synthetic additives.

- Complex Regulatory Landscape and Approval Processes: Navigating the intricate and evolving regulatory framework for food additives, including GRAS (Generally Recognized As Safe) status and specific regional approvals, can be time-consuming and costly, creating a barrier to market entry for smaller players.

- Supply Chain Volatility and Cost Fluctuations: Global supply chain disruptions and the fluctuating costs of raw materials, especially for natural additives, can impact production costs and product availability.

- Intense Competition and Price Sensitivity: The market is highly competitive, with significant price pressure from both large multinational corporations and smaller niche players, especially in bulk commodity additives.

- Development of Innovative Alternatives: The continuous emergence of novel food processing techniques and ingredient substitutes can displace the need for traditional additives, requiring constant adaptation from additive manufacturers.

Emerging Opportunities in US Food Additives Industry

The US Food Additives Industry presents a wealth of emerging opportunities driven by evolving consumer demands and technological frontiers. The escalating preference for plant-based food additives, as underscored by significant investments from major players like DuPont-Danisco, opens vast avenues for innovation in ingredients derived from sustainable sources. There is a growing demand for functional additives that offer health benefits beyond preservation and taste enhancement, such as gut-friendly prebiotics and probiotics integrated into dairy & frozen food and confectionery. The rise of personalized nutrition creates opportunities for specialized additives tailored to specific dietary needs and preferences. Furthermore, advancements in encapsulation technologies offer new ways to deliver flavors, colors, and nutrients more effectively and stably, particularly in beverages and bakery products. The "circular economy" concept is also creating opportunities for upcycling food byproducts into valuable additives, aligning with sustainability goals.

Growth Accelerators in the US Food Additives Industry Industry

Several critical factors are acting as growth accelerators for the US Food Additives Industry. Technological breakthroughs in areas like synthetic biology and precision fermentation are enabling the development of novel, high-performance, and sustainable additives at a lower cost. Strategic partnerships and collaborations between ingredient suppliers, food manufacturers, and research institutions are fostering innovation and speeding up product development cycles. Market expansion strategies, including the penetration into untapped application segments like meat, poultry, and sea food with advanced preservation and texturizing solutions, are significantly boosting growth. The increasing global demand for fortified and functional foods, driven by health and wellness trends, is a major catalyst, encouraging the development of additives that contribute to nutritional enhancement. Furthermore, evolving consumer demand for ethically sourced and environmentally friendly products is pushing the adoption of natural and plant-based additives, creating a strong market pull.

Key Players Shaping the US Food Additives Industry Market

- DuPont-Danisco

- Cargill Incorporated

- Novozymes

- Kerry Inc

- Archer Daniels Midland Company

- Koninklijke DSM N V

- Corbion NV

- Tate & Lyle

Notable Milestones in US Food Additives Industry Sector

- 2021 (Specific Month Unknown): Acquisition of Tate & Lyle by Symrise, a significant consolidation event that reshaped the competitive landscape and portfolio offerings within the food additives sector.

- 2022 (Specific Month Unknown): Launch of new preservative-free, clean label additives by Cargill, signaling a strong market response to consumer demand for natural and transparent ingredients, impacting the preservatives segment and wider application segments.

- 2023 (Specific Month Unknown): Investment in plant-based food additives by DuPont-Danisco, highlighting a strategic focus on sustainability and the growing market for vegan and vegetarian food ingredients across confectionery, bakery products, dairy & frozen food, beverages, and meat, poultry, and sea food.

In-Depth US Food Additives Industry Market Outlook

The US Food Additives Industry is set for sustained and accelerated growth, with future market potential driven by a confluence of strategic opportunities. The ongoing consumer-led demand for clean label, natural, and plant-based food additives will continue to be a primary growth engine, pushing innovation in food flavors and enhancers, food colorants, and sweeteners. Advancements in biotechnology and enzymatic processing will unlock new possibilities for producing highly functional and sustainable additives, impacting all application segments. Strategic partnerships and mergers, such as the Tate & Lyle acquisition by Symrise, will continue to shape the market by fostering consolidation and expanding product portfolios. The increasing focus on health and wellness will drive demand for specialized additives that support nutritional enhancement and address dietary concerns, particularly in dairy & frozen food and beverages. Furthermore, the industry's ability to adapt to evolving regulatory landscapes and leverage innovations in processing and delivery systems will be crucial for capitalizing on the vast potential within the parent market for food ingredients and the specialized child market for high-performance additives.

US Food Additives Industry Segmentation

-

1. Type

- 1.1. Preservatives

- 1.2. Sweetener

- 1.3. Sugar Substitutes

- 1.4. Emulsifier

- 1.5. Anti-Caking Agents

- 1.6. Enzymes

- 1.7. Hydrocolloids

- 1.8. Food Flavors and Enhancers

- 1.9. Food Colorants

- 1.10. Acidulants

-

2. Application

- 2.1. Confectionery

- 2.2. Bakery Products

- 2.3. Dairy & Frozen Food

- 2.4. Beverages

- 2.5. Meat, Poultry, and Sea Food

- 2.6. Others

US Food Additives Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

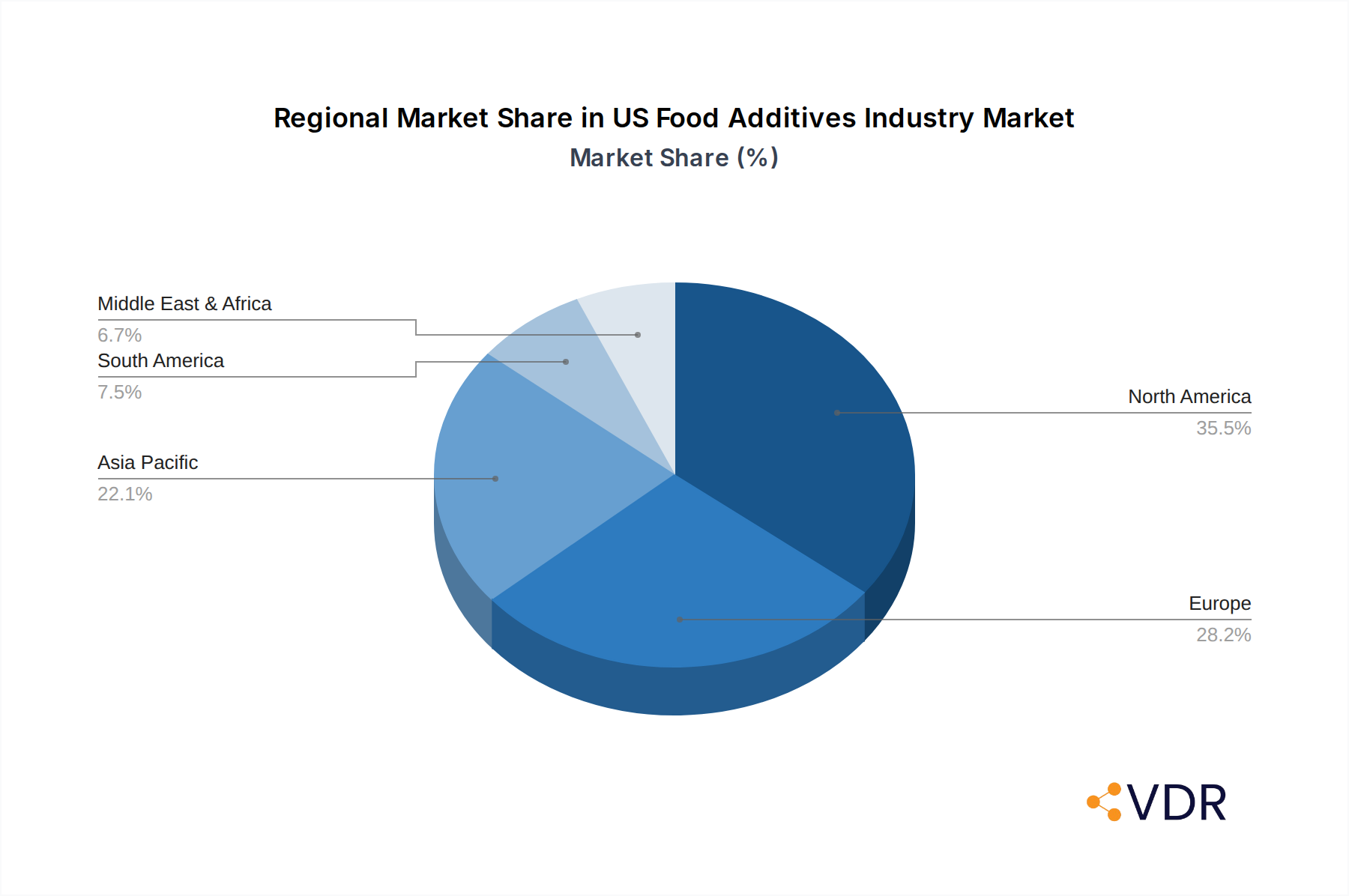

US Food Additives Industry Regional Market Share

Geographic Coverage of US Food Additives Industry

US Food Additives Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Preservatives

- 5.1.2. Sweetener

- 5.1.3. Sugar Substitutes

- 5.1.4. Emulsifier

- 5.1.5. Anti-Caking Agents

- 5.1.6. Enzymes

- 5.1.7. Hydrocolloids

- 5.1.8. Food Flavors and Enhancers

- 5.1.9. Food Colorants

- 5.1.10. Acidulants

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Confectionery

- 5.2.2. Bakery Products

- 5.2.3. Dairy & Frozen Food

- 5.2.4. Beverages

- 5.2.5. Meat, Poultry, and Sea Food

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global US Food Additives Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Preservatives

- 6.1.2. Sweetener

- 6.1.3. Sugar Substitutes

- 6.1.4. Emulsifier

- 6.1.5. Anti-Caking Agents

- 6.1.6. Enzymes

- 6.1.7. Hydrocolloids

- 6.1.8. Food Flavors and Enhancers

- 6.1.9. Food Colorants

- 6.1.10. Acidulants

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Confectionery

- 6.2.2. Bakery Products

- 6.2.3. Dairy & Frozen Food

- 6.2.4. Beverages

- 6.2.5. Meat, Poultry, and Sea Food

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America US Food Additives Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Preservatives

- 7.1.2. Sweetener

- 7.1.3. Sugar Substitutes

- 7.1.4. Emulsifier

- 7.1.5. Anti-Caking Agents

- 7.1.6. Enzymes

- 7.1.7. Hydrocolloids

- 7.1.8. Food Flavors and Enhancers

- 7.1.9. Food Colorants

- 7.1.10. Acidulants

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Confectionery

- 7.2.2. Bakery Products

- 7.2.3. Dairy & Frozen Food

- 7.2.4. Beverages

- 7.2.5. Meat, Poultry, and Sea Food

- 7.2.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. South America US Food Additives Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Preservatives

- 8.1.2. Sweetener

- 8.1.3. Sugar Substitutes

- 8.1.4. Emulsifier

- 8.1.5. Anti-Caking Agents

- 8.1.6. Enzymes

- 8.1.7. Hydrocolloids

- 8.1.8. Food Flavors and Enhancers

- 8.1.9. Food Colorants

- 8.1.10. Acidulants

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Confectionery

- 8.2.2. Bakery Products

- 8.2.3. Dairy & Frozen Food

- 8.2.4. Beverages

- 8.2.5. Meat, Poultry, and Sea Food

- 8.2.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe US Food Additives Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Preservatives

- 9.1.2. Sweetener

- 9.1.3. Sugar Substitutes

- 9.1.4. Emulsifier

- 9.1.5. Anti-Caking Agents

- 9.1.6. Enzymes

- 9.1.7. Hydrocolloids

- 9.1.8. Food Flavors and Enhancers

- 9.1.9. Food Colorants

- 9.1.10. Acidulants

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Confectionery

- 9.2.2. Bakery Products

- 9.2.3. Dairy & Frozen Food

- 9.2.4. Beverages

- 9.2.5. Meat, Poultry, and Sea Food

- 9.2.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East & Africa US Food Additives Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Preservatives

- 10.1.2. Sweetener

- 10.1.3. Sugar Substitutes

- 10.1.4. Emulsifier

- 10.1.5. Anti-Caking Agents

- 10.1.6. Enzymes

- 10.1.7. Hydrocolloids

- 10.1.8. Food Flavors and Enhancers

- 10.1.9. Food Colorants

- 10.1.10. Acidulants

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Confectionery

- 10.2.2. Bakery Products

- 10.2.3. Dairy & Frozen Food

- 10.2.4. Beverages

- 10.2.5. Meat, Poultry, and Sea Food

- 10.2.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Asia Pacific US Food Additives Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Preservatives

- 11.1.2. Sweetener

- 11.1.3. Sugar Substitutes

- 11.1.4. Emulsifier

- 11.1.5. Anti-Caking Agents

- 11.1.6. Enzymes

- 11.1.7. Hydrocolloids

- 11.1.8. Food Flavors and Enhancers

- 11.1.9. Food Colorants

- 11.1.10. Acidulants

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Confectionery

- 11.2.2. Bakery Products

- 11.2.3. Dairy & Frozen Food

- 11.2.4. Beverages

- 11.2.5. Meat, Poultry, and Sea Food

- 11.2.6. Others

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Dupont- Danisco

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Cargill Incorporated

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Novozymes

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Kerry Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Archer Daniels Midland Company

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Koninklijke DSM N V

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Corbion NV

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Tate & Lyle

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.1 Dupont- Danisco

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global US Food Additives Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America US Food Additives Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America US Food Additives Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America US Food Additives Industry Revenue (billion), by Application 2025 & 2033

- Figure 5: North America US Food Additives Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America US Food Additives Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America US Food Additives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America US Food Additives Industry Revenue (billion), by Type 2025 & 2033

- Figure 9: South America US Food Additives Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: South America US Food Additives Industry Revenue (billion), by Application 2025 & 2033

- Figure 11: South America US Food Additives Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: South America US Food Additives Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: South America US Food Additives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe US Food Additives Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Europe US Food Additives Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Europe US Food Additives Industry Revenue (billion), by Application 2025 & 2033

- Figure 17: Europe US Food Additives Industry Revenue Share (%), by Application 2025 & 2033

- Figure 18: Europe US Food Additives Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe US Food Additives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa US Food Additives Industry Revenue (billion), by Type 2025 & 2033

- Figure 21: Middle East & Africa US Food Additives Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Middle East & Africa US Food Additives Industry Revenue (billion), by Application 2025 & 2033

- Figure 23: Middle East & Africa US Food Additives Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: Middle East & Africa US Food Additives Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa US Food Additives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific US Food Additives Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: Asia Pacific US Food Additives Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Asia Pacific US Food Additives Industry Revenue (billion), by Application 2025 & 2033

- Figure 29: Asia Pacific US Food Additives Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Asia Pacific US Food Additives Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific US Food Additives Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global US Food Additives Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global US Food Additives Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Global US Food Additives Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global US Food Additives Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global US Food Additives Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Global US Food Additives Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global US Food Additives Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Global US Food Additives Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 12: Global US Food Additives Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global US Food Additives Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 17: Global US Food Additives Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 18: Global US Food Additives Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global US Food Additives Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 29: Global US Food Additives Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 30: Global US Food Additives Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global US Food Additives Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 38: Global US Food Additives Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 39: Global US Food Additives Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific US Food Additives Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the US Food Additives Industry?

The projected CAGR is approximately 5.9%.

2. Which companies are prominent players in the US Food Additives Industry?

Key companies in the market include Dupont- Danisco, Cargill Incorporated, Novozymes, Kerry Inc, Archer Daniels Midland Company, Koninklijke DSM N V, Corbion NV, Tate & Lyle.

3. What are the main segments of the US Food Additives Industry?

The market segments include Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 17.8 billion as of 2022.

5. What are some drivers contributing to market growth?

Wide Applications and Functionality; Demand For Gluten-Free Products.

6. What are the notable trends driving market growth?

Growing Demand for Retail Food.

7. Are there any restraints impacting market growth?

Easy Availability of Economically Feasible Alternatives.

8. Can you provide examples of recent developments in the market?

1. Acquisition of Tate & Lyle by Symrise in 2021 2. Launch of new preservative-free, clean label additives by Cargill in 2022 3. Investment in plant-based food additives by DuPont-Danisco in 2023

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "US Food Additives Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the US Food Additives Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the US Food Additives Industry?

To stay informed about further developments, trends, and reports in the US Food Additives Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence