Key Insights

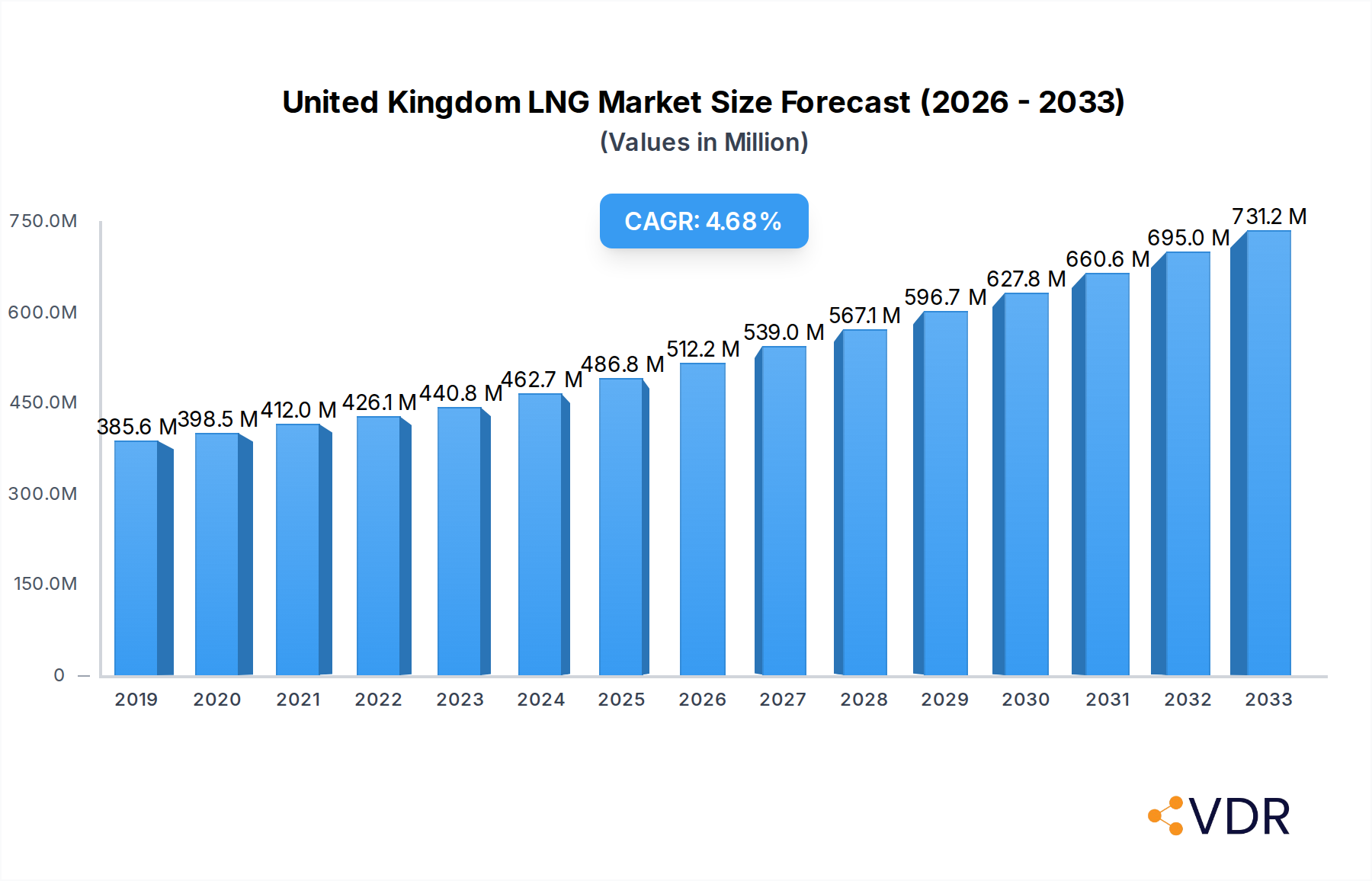

The United Kingdom's Liquefied Natural Gas (LNG) market is poised for robust growth, driven by increasing demand for cleaner energy alternatives and the nation's ongoing energy security initiatives. With a projected market size of USD 462.69 million in 2024, the sector is expected to expand at a Compound Annual Growth Rate (CAGR) of 5.1% from 2019 to 2033. This upward trajectory is significantly influenced by the critical role LNG plays in diversifying the UK's energy mix, reducing reliance on volatile global gas supplies, and meeting the stringent environmental regulations that favor lower-emission fuels. Key applications such as power generation are a primary demand driver, as utilities increasingly turn to natural gas as a transitional fuel for electricity production. The transportation sector also presents a growing opportunity, with the potential for LNG adoption in heavy-duty vehicles and maritime transport. Major players like Shell PLC, Électricité de France, and Bechtel Corporation are actively investing and developing infrastructure, indicating a strong confidence in the market's future potential.

United Kingdom LNG Market Market Size (In Million)

The UK LNG market is characterized by a dynamic interplay of drivers and restraints. While increasing environmental consciousness and government policies promoting decarbonization serve as strong growth catalysts, the market also faces challenges. High infrastructure costs associated with LNG terminals and regasification facilities, coupled with the volatility of global LNG prices, can act as significant restraints. Furthermore, the development and adoption of renewable energy sources, although a long-term goal, could eventually temper the demand for fossil fuels, including LNG. However, the strategic importance of LNG in ensuring energy security, especially in light of geopolitical uncertainties, is likely to sustain its relevance in the medium term. The market’s segmentation reveals a diversified application base, with power generation and transportation leading the charge, while a concentrated presence of major global and national companies suggests a competitive yet opportunity-rich landscape.

United Kingdom LNG Market Company Market Share

Comprehensive United Kingdom LNG Market Report: Dynamics, Trends, and Future Outlook (2019-2033)

This in-depth report offers a strategic analysis of the United Kingdom Liquefied Natural Gas (LNG) market, meticulously examining its dynamics, growth trajectory, key players, and future potential. Covering the historical period from 2019 to 2024, with a base year of 2025 and a forecast period extending to 2033, this report provides unparalleled insights for industry stakeholders seeking to navigate and capitalize on the evolving UK LNG landscape. Our analysis integrates high-traffic keywords such as "UK LNG market," "LNG import UK," "LNG terminal UK," "energy security UK," and "gas market UK," ensuring maximum search engine visibility. We delve into the parent and child market structures to provide a holistic understanding of market segmentation and interdependencies. All quantitative data is presented in million units.

United Kingdom LNG Market Market Dynamics & Structure

The United Kingdom LNG market is characterized by a moderate to high concentration, with a few key players dominating import infrastructure and supply. Technological innovation is largely driven by advancements in liquefaction and regasification technologies, enhancing efficiency and reducing environmental impact, crucial for meeting stringent UK environmental regulations. The regulatory framework is robust, influenced by EU energy directives (even post-Brexit, many remain influential) and national policies focused on energy security and decarbonization targets. Competitive product substitutes, primarily pipeline natural gas from Europe, exert significant influence, but the increasing volatility of these supplies enhances LNG's strategic importance. End-user demographics are shifting, with growing demand from power generation and an emerging interest in the transportation sector, particularly for heavy-duty vehicles. Mergers and Acquisitions (M&A) trends are influenced by the pursuit of integrated supply chains and market access.

- Market Concentration: Dominated by a few major terminal operators and large-scale buyers, but with increasing fragmentation in downstream distribution.

- Technological Innovation: Focus on enhanced cooling efficiency in liquefaction, advanced regasification techniques, and digital supply chain management.

- Regulatory Frameworks: Driven by energy security mandates, net-zero targets, and international trade agreements.

- Competitive Substitutes: European pipeline gas, but with growing LNG preference due to geopolitical uncertainties.

- End-User Demographics: Power generation remains the largest segment, with increasing potential in maritime and road transport.

- M&A Trends: Strategic acquisitions to secure import capacity and build diversified energy portfolios.

United Kingdom LNG Market Growth Trends & Insights

The United Kingdom LNG market is poised for significant expansion, driven by a confluence of factors including the nation's unwavering commitment to energy security, the strategic imperative to diversify gas supply away from single sources, and the increasing demand from key industrial and power generation sectors. The market size has demonstrated consistent growth over the historical period, reflecting the UK's reliance on imported natural gas. This growth is projected to accelerate in the forecast period, fueled by ongoing investments in LNG infrastructure and the adaptation of new technologies. Adoption rates for LNG are expected to climb, particularly as the nation seeks to reduce its carbon footprint through cleaner burning fuels in its power sector and explore nascent applications in the transportation industry. Technological disruptions are primarily centered around more efficient and environmentally friendly regasification processes and advancements in floating storage and regasification units (FSRUs), which offer flexibility and reduced capital expenditure. Consumer behavior shifts are becoming more pronounced, with a greater emphasis on reliable and sustainable energy sources, which LNG, when sourced responsibly, can help provide. The UK's strategic position as a major gas consumer, coupled with its advanced port infrastructure, solidifies its role as a critical hub for LNG imports. The projected Compound Annual Growth Rate (CAGR) for the UK LNG market is expected to be robust, reflecting these underlying trends and the ongoing geopolitical shifts that underscore the importance of flexible and secure energy supplies. Understanding these evolving dynamics is crucial for stakeholders seeking to capitalize on the opportunities within the United Kingdom's burgeoning LNG sector.

Dominant Regions, Countries, or Segments in United Kingdom LNG Market

The Power Generation segment is the undisputed driver of growth within the United Kingdom LNG market. This dominance is underpinned by several key factors, including the UK's ongoing transition away from coal-fired power plants, the intermittent nature of renewable energy sources like wind and solar, and the strategic role of natural gas as a flexible and reliable source of electricity generation. The UK government's energy policies, which prioritize decarbonization while ensuring grid stability, have cemented the importance of gas-fired power plants, which are often fueled by LNG imports.

- Power Generation Dominance:

- Energy Security: LNG provides a crucial buffer against supply disruptions from traditional pipeline sources, ensuring consistent power availability.

- Decarbonization Goals: Natural gas, while a fossil fuel, is a cleaner-burning alternative to coal, supporting interim emissions reduction targets.

- Grid Stability: Gas power plants offer rapid ramp-up and ramp-down capabilities, essential for balancing the grid with variable renewables.

- Infrastructure: The UK possesses significant gas-fired power generation capacity and strategically located LNG import terminals.

- Market Share: Power generation consistently accounts for over 60% of UK LNG consumption.

The Transportation segment is an emerging, yet rapidly growing, area for LNG adoption. While currently a smaller contributor, its potential is substantial, driven by the need for cleaner fuels in heavy-duty road transport and maritime shipping. The UK's ambition to achieve net-zero emissions extends to these sectors, making LNG an attractive option due to its lower particulate matter and sulfur dioxide emissions compared to diesel and heavy fuel oil. Government incentives and the development of dedicated LNG fueling infrastructure are key to unlocking this segment's potential.

- Transportation Growth Drivers:

- Environmental Regulations: Stricter emissions standards for road and maritime transport are pushing operators towards cleaner fuels.

- Cost-Effectiveness: LNG can offer competitive operational costs for long-haul trucking and shipping.

- Infrastructure Development: Investment in LNG fueling stations and bunkering facilities is gradually expanding.

- Dual-Fuel Technology: Advancements in engines capable of running on both LNG and other fuels are increasing flexibility.

Other Applications, encompassing industrial processes and the residential heating sector, represent a more mature but stable segment of the UK LNG market. While industrial demand for natural gas remains significant, the shift towards electrification and alternative heating solutions in the residential sector may temper its growth in the long term. However, LNG continues to play a vital role in providing a reliable energy source for various industrial operations where direct electrification is challenging or economically unfeasible.

- Other Applications Insights:

- Industrial Processes: Consistent demand from sectors like manufacturing and chemicals for process heat and feedstock.

- Residential Heating: While declining in new builds, it remains a crucial supply for existing infrastructure.

- LNG as Feedstock: Potential for growth in chemical production.

United Kingdom LNG Market Product Landscape

The United Kingdom LNG market's product landscape is primarily defined by its role as a versatile energy commodity. The core product is liquefied natural gas, a chilled form of natural gas that facilitates efficient transportation and storage. Innovations in this space are focused on improving the liquefaction process to reduce energy consumption and enhance safety. On the receiving end, advancements in regasification technologies, including the deployment of floating storage and regasification units (FSRUs), offer greater flexibility and scalability for the UK's import capacity. The performance metrics of LNG are measured by its energy content, purity, and environmental profile, with growing emphasis on its lower carbon footprint compared to other fossil fuels. Unique selling propositions include its inherent safety and its ability to provide energy security, mitigating reliance on single pipeline routes.

Key Drivers, Barriers & Challenges in United Kingdom LNG Market

Key Drivers: The United Kingdom LNG market is propelled by several critical factors. Energy security is paramount, especially in light of geopolitical instability impacting traditional gas supplies. The UK's strong commitment to decarbonization targets positions LNG as a transitional fuel, offering a cleaner alternative to coal and oil for power generation and industry. Furthermore, the development of advanced regasification technologies and the flexibility of FSRUs are enhancing import capabilities. Strategic investments in LNG infrastructure, including terminals and distribution networks, are also crucial growth catalysts.

Barriers & Challenges: Despite the drivers, the market faces significant barriers. The volatility of global LNG prices can impact its competitiveness against pipeline gas. High capital costs associated with developing and maintaining LNG infrastructure remain a challenge. Environmental concerns surrounding methane emissions during production and transportation, as well as the energy intensity of liquefaction, require continuous technological solutions. Regulatory hurdles and the complex permitting processes for new infrastructure projects can cause delays. Supply chain disruptions, as evidenced by recent global events, pose a persistent risk, impacting availability and price. Competition from renewable energy sources and the long-term shift towards a hydrogen economy present a future challenge to sustained LNG demand.

Emerging Opportunities in United Kingdom LNG Market

Emerging opportunities in the United Kingdom LNG market are diverse and promising. The maritime sector presents a significant untapped market for LNG as a bunker fuel, driven by stricter emissions regulations. The heavy-duty road transport sector is also a growing area for LNG adoption, offering cost savings and reduced emissions for logistics companies. Furthermore, the development of smaller-scale LNG infrastructure for regional distribution and industrial use can unlock new markets. Innovations in virtual pipeline solutions and the potential for bio-LNG integration offer pathways to further decarbonize the existing LNG value chain, enhancing its sustainability appeal and opening up new avenues for market growth.

Growth Accelerators in the United Kingdom LNG Market Industry

Several catalysts are accelerating the growth of the United Kingdom LNG market. Technological breakthroughs in liquefaction and regasification, leading to greater efficiency and lower costs, are a significant driver. Strategic partnerships between LNG suppliers, terminal operators, and end-users are crucial for optimizing supply chains and securing long-term contracts. Market expansion strategies, including the development of new import and distribution networks, are vital for increasing accessibility. The UK's robust demand for natural gas, coupled with its strategic geographical location and established trading relationships, provides a fertile ground for continued investment and growth in the LNG sector.

Key Players Shaping the United Kingdom LNG Market Market

- Shell PLC

- Électricité de France

- Dragon LNG

- Bechtel Corporation

- South Hook LNG Terminal Ltd

- Ramboll Group A/S

- Fluor Corporation

- Npower Limited

Notable Milestones in United Kingdom LNG Market Sector

- August 2022: Houston-based Delfin LNG signed a deal to supply LNG to a United Kingdom energy company that plans to construct a floating LNG export terminal off Louisiana's coast. This agreement involves Delfin LNG providing 1 million metric tons of LNG annually to Centrica, an energy company located in Windsor, England, which owns British Gas and Bord Gais Energy.

In-Depth United Kingdom LNG Market Market Outlook

The outlook for the United Kingdom LNG market remains exceptionally strong, driven by its indispensable role in ensuring national energy security and supporting the country's ambitious decarbonization agenda. Growth accelerators such as ongoing investment in state-of-the-art regasification facilities, including flexible FSRU solutions, will continue to bolster import capacity and responsiveness to market demands. Strategic partnerships are anticipated to deepen, fostering greater integration across the supply chain and unlocking efficiencies. The increasing adoption of LNG in the transportation sector, particularly for maritime and heavy-duty road freight, represents a significant growth frontier, aligned with stringent environmental regulations. Furthermore, the potential for blending with lower-carbon gases like bio-LNG will enhance the sustainability profile of the UK's LNG imports, positioning it as a vital component of a diversified and resilient energy future.

United Kingdom LNG Market Segmentation

-

1. Application

- 1.1. Power Generation

- 1.2. Transportation

- 1.3. Other Applications

United Kingdom LNG Market Segmentation By Geography

- 1. United Kingdom

United Kingdom LNG Market Regional Market Share

Geographic Coverage of United Kingdom LNG Market

United Kingdom LNG Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Power Generation

- 5.1.2. Transportation

- 5.1.3. Other Applications

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. United Kingdom

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. United Kingdom LNG Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Power Generation

- 6.1.2. Transportation

- 6.1.3. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Shell PLC

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Électricité de France

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Dragon LNG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Bechtel Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 South Hook LNG Terminal Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Ramboll Group A/S

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Fluor Corporation

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Npower Limited

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.1 Shell PLC

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United Kingdom LNG Market Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: United Kingdom LNG Market Share (%) by Company 2025

List of Tables

- Table 1: United Kingdom LNG Market Revenue million Forecast, by Application 2020 & 2033

- Table 2: United Kingdom LNG Market Revenue million Forecast, by Region 2020 & 2033

- Table 3: United Kingdom LNG Market Revenue million Forecast, by Application 2020 & 2033

- Table 4: United Kingdom LNG Market Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United Kingdom LNG Market?

The projected CAGR is approximately 5.1%.

2. Which companies are prominent players in the United Kingdom LNG Market?

Key companies in the market include Shell PLC, Électricité de France, Dragon LNG, Bechtel Corporation, South Hook LNG Terminal Ltd, Ramboll Group A/S, Fluor Corporation, Npower Limited.

3. What are the main segments of the United Kingdom LNG Market?

The market segments include Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 462.69 million as of 2022.

5. What are some drivers contributing to market growth?

Drivers; Restraints.

6. What are the notable trends driving market growth?

Transportation Segment to dominate the market during the forecast period..

7. Are there any restraints impacting market growth?

4.; Political Instability and Militant Attacks on Pipeline Infrastructure.

8. Can you provide examples of recent developments in the market?

In August 2022, Houston-based Delfin LNG signed a deal to supply LNG to a United Kingdom energy company that plans to construct a floating LNG export terminal off Louisiana's coast. This agreement involves Delfin LNG providing 1 million metric tons of LNG annually to Centrica, an energy company located in Windsor, England, which owns British Gas and Bord Gais Energy.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United Kingdom LNG Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United Kingdom LNG Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United Kingdom LNG Market?

To stay informed about further developments, trends, and reports in the United Kingdom LNG Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence