Key Insights

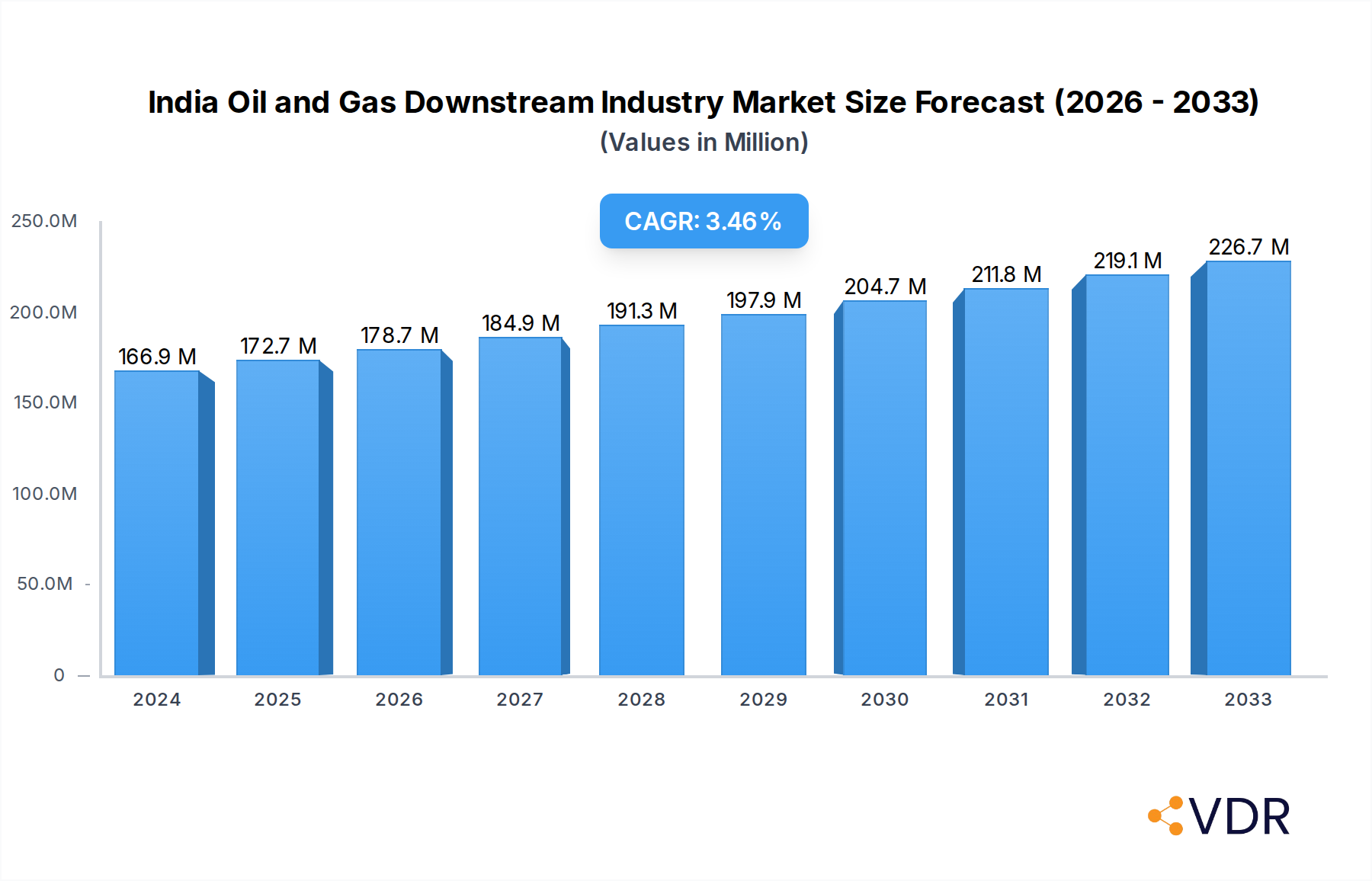

The India Oil and Gas Downstream Industry is poised for significant expansion, driven by robust demand for refined products and petrochemicals. In 2024, the market size is estimated at $166.93 million, with a projected Compound Annual Growth Rate (CAGR) of 3.5% through to 2033. This growth is primarily fueled by increasing per capita consumption of energy, a burgeoning automotive sector, and the expanding manufacturing base that relies heavily on petrochemical derivatives. Government initiatives aimed at boosting refining capacity and promoting the use of cleaner fuels further underpin this positive outlook. The downstream segment, encompassing refining and petrochemicals, plays a crucial role in India's energy security and economic development, transforming crude oil into a wide array of essential products. The interplay of these factors indicates a dynamic and evolving market landscape.

India Oil and Gas Downstream Industry Market Size (In Million)

Key drivers for this expansion include the continuous growth in demand for transportation fuels like petrol and diesel, alongside a surge in the consumption of petrochemicals used in plastics, synthetic fibers, and fertilizers, which are integral to various industries including packaging, textiles, and agriculture. While the market benefits from strong domestic demand and supportive government policies, potential restraints such as fluctuating crude oil prices and the increasing global focus on renewable energy sources present challenges. However, the significant investments being made by major players like Indian Oil Corporation, Bharat Petroleum Corporation Limited, and Reliance Industries Limited in upgrading existing facilities and developing new petrochemical complexes are expected to mitigate these challenges and solidify India's position in the global downstream oil and gas sector.

India Oil and Gas Downstream Industry Company Market Share

India Oil and Gas Downstream Industry Market Dynamics & Structure

The Indian oil and gas downstream industry, a critical pillar of the nation's economy, is characterized by a dynamic interplay of market concentration, technological advancements, and evolving regulatory landscapes. While dominated by public sector undertakings (PSUs) like Indian Oil Corporation Limited (IOCL), Bharat Petroleum Corporation Limited (BPCL), and Hindustan Petroleum Corporation Limited (HPCL), private players such as Reliance Industries Limited (RIL) and Nayara Energy Limited are increasingly influencing market dynamics. The sector's structure is defined by its integrated value chain, encompassing refining, petrochemicals, and marketing.

Market Concentration & Key Players:

- Dominant PSUs: IOCL, BPCL, HPCL collectively hold a significant market share in refining and fuel retailing, driven by extensive infrastructure and established distribution networks.

- Private Sector Influence: RIL’s Jamnagar refinery, one of the world’s largest, and its growing petrochemical ventures, alongside Nayara Energy’s retail expansion, are reshaping competitive intensity.

- Petrochemical Expansion: Companies like Haldia Petrochemicals Ltd (HPL) and GAIL (India) Limited are central to the burgeoning petrochemical segment, catering to diverse industrial demands.

Technological Innovation Drivers:

- Refinery Modernization: Investments in upgrading existing refineries to produce cleaner fuels (e.g., BS-VI compliant fuels) and enhance operational efficiency are paramount.

- Petrochemical Integration: Advancements in catalysis, process optimization, and development of high-value specialty chemicals are key innovation areas.

- Digitalization & Automation: The adoption of Industry 4.0 technologies, including AI, IoT, and advanced analytics, is crucial for improving safety, productivity, and predictive maintenance.

Regulatory Frameworks:

- Energy Transition Policies: Government initiatives promoting renewable energy and electric mobility are indirectly influencing demand patterns for traditional fuels.

- Environmental Regulations: Stringent emission norms and mandates for biofuel blending (e.g., Ethanol Blending Programme) are shaping product specifications and investment priorities.

- Pricing Reforms: De-regulation of fuel prices in certain segments has increased market competition and necessitated greater operational efficiency.

Competitive Product Substitutes:

- Electric Vehicles (EVs): The growing adoption of EVs poses a long-term substitute for gasoline and diesel in the transportation sector.

- Renewable Energy Sources: Solar and wind power are increasingly substituting fossil fuels in power generation.

- Biofuels: Ethanol and biodiesel are being blended with conventional fuels, acting as partial substitutes.

End-User Demographics:

- Transportation Sector: The largest consumer of refined products, with demand influenced by economic growth, urbanization, and vehicle ownership.

- Industrial Sector: Petrochemicals are crucial inputs for a wide array of industries, including plastics, textiles, and construction.

- Residential & Commercial: Liquefied Petroleum Gas (LPG) remains a key cooking fuel, with increasing penetration in rural areas.

Mergers & Acquisitions (M&A) Trends:

- Consolidation: While large-scale M&A is less frequent among major players, strategic acquisitions of smaller entities or stakes in joint ventures are observed to expand market reach or acquire new technologies.

- Joint Ventures: Partnerships, including those with international players like Oman Oil Company, are common for large-scale projects, technology transfer, and market access.

- Focus on Value Chain Integration: M&A activities often aim to strengthen integration across refining, marketing, and petrochemical segments to maximize synergies.

India Oil and Gas Downstream Industry Growth Trends & Insights

The Indian oil and gas downstream industry is poised for substantial growth, propelled by robust economic expansion, increasing energy demands, and strategic government initiatives. The market size evolution over the study period (2019–2033) reveals a consistent upward trajectory, with the base year of 2025 serving as a pivotal point for current market valuations and the subsequent forecast period (2025–2033) indicating accelerated expansion. Historical data from 2019–2024 provides the foundational understanding of past performance and sets the stage for future projections. The Compound Annual Growth Rate (CAGR) is anticipated to remain strong, driven by factors such as a growing middle class with rising disposable incomes, increased urbanization leading to higher transportation fuel consumption, and the burgeoning industrial sector’s demand for petrochemical products.

Technological disruptions are playing a transformative role. The industry is witnessing significant investments in upgrading refining capacities to meet stringent environmental norms, such as the phased rollout of BS-VI compliant fuels. This not only enhances fuel quality but also necessitates adoption of advanced refining technologies. In the petrochemical segment, innovation is geared towards developing higher-value specialty chemicals and polymers, catering to sophisticated end-user industries like automotive, packaging, and construction. The adoption rates for these advanced technologies are steadily increasing as companies recognize their importance for competitiveness and sustainability. Consumer behavior shifts are also noteworthy. While demand for traditional fuels continues to grow, there's an increasing awareness and gradual shift towards cleaner energy alternatives and fuels with lower emissions. This is reflected in the government's push for ethanol blending and the growing interest in electric mobility, which, while a long-term substitute, influences strategic planning for the downstream sector. The expansion of petrochemical applications into new areas, such as advanced materials for infrastructure and consumer goods, further solidifies its growth trajectory. The integration of digital technologies, including AI and IoT, for operational efficiency, predictive maintenance, and supply chain optimization, is another key trend enhancing market penetration and efficiency. The overarching narrative is one of sustained demand, technological evolution, and adaptation to evolving energy landscapes, ensuring the continued relevance and growth of India's oil and gas downstream sector.

Dominant Regions, Countries, or Segments in India Oil and Gas Downstream Industry

Within the multifaceted Indian oil and gas downstream industry, the Refineries: Market Overview segment emerges as a dominant force, underpinning the entire value chain and dictating the availability of critical feedstocks for downstream petrochemical production. India’s strategic imperative to achieve energy security and reduce import dependence has led to significant investments in refining capacity over the historical period (2019-2024) and the base year of 2025. This segment is characterized by colossal infrastructure, complex technological processes, and a direct link to the transportation and industrial sectors, making it the primary engine of downstream industry growth.

Key Drivers for Refinery Dominance:

- Surging Domestic Demand: India's rapidly expanding economy and a growing population are fueling an insatiable appetite for transportation fuels like gasoline, diesel, and aviation turbine fuel. The transportation sector remains the largest consumer of refined products, and with increasing vehicle ownership and economic activity, the demand for these fuels is projected to escalate significantly throughout the forecast period (2025-2033). This sustained demand provides a solid foundation for refinery operations.

- Government Policy Support & Energy Security: The Indian government has consistently prioritized strengthening its refining infrastructure to reduce reliance on imported refined products and enhance national energy security. Policies aimed at self-sufficiency and the continuous modernization of refineries to meet evolving fuel quality standards (e.g., BS-VI) underscore the strategic importance of this segment. Economic policies favoring domestic manufacturing and energy independence directly benefit the refining sector by ensuring consistent investment and operational support.

- Strategic Location & Infrastructure: Major refining complexes are strategically located near coastlines for efficient crude oil import and product export, or close to major consumption hubs. Significant investments in infrastructure such as pipelines, port facilities, and storage terminals further enhance the operational efficiency and reach of refineries. The presence of integrated refinery and petrochemical complexes, such as those operated by Reliance Industries Limited and Indian Oil Corporation Limited, maximizes value creation and operational synergies.

- Petrochemical Feedstock Integration: Refineries serve as the primary source of naphtha, liquefied petroleum gas (LPG), and other feedstocks essential for the Petrochemical Pants: Market Overview segment. This symbiotic relationship means that the growth and operational efficiency of refineries directly translate into the availability and cost-competitiveness of petrochemical products. Companies like Indian Oil Corporation Limited and Bharat Petroleum Corporation Limited are actively expanding their petrochemical capacities alongside their refining operations, demonstrating the inherent link and mutual growth potential.

- Technological Advancements & Modernization: Continuous investments in upgrading refinery technologies to improve yield, enhance product quality, and reduce environmental impact are crucial. The adoption of advanced catalytic processes, energy-efficient technologies, and digital solutions are driving operational excellence and profitability. This commitment to technological advancement ensures that Indian refineries remain competitive on a global scale.

- Market Share & Growth Potential: The sheer scale of operations and the critical role of refineries in supplying essential fuels give them a commanding market share. While other segments are growing, the foundational need for refined products ensures that refineries will continue to be the bedrock of the downstream industry. Their growth potential is intrinsically linked to overall economic growth and energy demand, which are robust in India.

The Petrochemical Pants: Market Overview segment, while not as foundational as refining, is rapidly gaining prominence and is a significant growth driver. The increasing demand from sectors like packaging, textiles, automotive, and construction for polymers, synthetic fibers, and other chemical derivatives is propelling its expansion. Companies like Reliance Industries Limited, Haldia Petrochemicals Ltd, and GAIL (India) Limited are at the forefront of this segment, investing in new capacities and developing a wider range of specialty petrochemicals.

Key Drivers for Petrochemical Growth:

- Expanding End-User Industries: The "Make in India" initiative and the growth of sectors such as automotive manufacturing, construction, consumer durables, and packaging are creating substantial demand for petrochemical products. The increasing purchasing power of the Indian populace also fuels demand for consumer goods that utilize petrochemical derivatives.

- Import Substitution: India is a significant importer of certain petrochemicals. There is a strong policy push and market opportunity to substitute these imports with domestically produced chemicals, thereby improving the trade balance and fostering local manufacturing.

- Value Addition & Diversification: Companies are increasingly focusing on moving up the value chain by producing higher-margin specialty chemicals and performance polymers, rather than just basic olefins and polyolefins. This diversification strategy enhances profitability and resilience.

- Feedstock Availability: The integrated nature of many Indian refining complexes ensures a reliable and cost-effective supply of essential feedstocks like naphtha and natural gas for petrochemical production. This integration provides a competitive advantage.

- Government Incentives: The government’s Production Linked Incentive (PLI) schemes for various manufacturing sectors, including chemicals and petrochemicals, are acting as significant growth accelerators. These incentives encourage investment in new capacities and the development of advanced products.

While refineries hold the foundational dominance due to their role in producing essential fuels, the petrochemical segment is the fastest-growing and holds immense potential for value creation and diversification, making both segments critical to the overall health and expansion of India's oil and gas downstream industry.

India Oil and Gas Downstream Industry Product Landscape

The product landscape of the Indian oil and gas downstream industry is predominantly defined by a range of fuels and a diverse array of petrochemical derivatives. In the refining segment, the primary products include gasoline, diesel, jet fuel, kerosene, and liquefied petroleum gas (LPG), all adhering to increasingly stringent environmental standards like BS-VI. Beyond these fuels, refineries also produce petrochemical feedstocks such as naphtha and reformate. The petrochemical segment contributes a wide spectrum of polymers like polyethylene (PE), polypropylene (PP), and polyvinyl chloride (PVC), essential for packaging, automotive components, and construction. Additionally, the industry produces synthetic fibers, solvents, and specialty chemicals catering to niche applications. Technological advancements are continuously enhancing the performance and environmental profile of these products, with a focus on higher energy efficiency and reduced emissions.

Key Drivers, Barriers & Challenges in India Oil and Gas Downstream Industry

Key Drivers:

- Robust Economic Growth: India's sustained economic expansion directly translates to higher energy consumption across transportation, industrial, and residential sectors, fueling demand for refined products and petrochemicals.

- Increasing Urbanization & Population: A growing urban population leads to a greater need for transportation, increased use of packaged goods, and higher demand for fuels like LPG.

- Government Policies & Initiatives: Policies promoting domestic manufacturing, energy security, and infrastructure development, alongside schemes like the Ethanol Blending Programme, act as significant catalysts.

- Technological Advancements: Investments in refinery modernization, development of cleaner fuels, and innovation in petrochemical product applications enhance competitiveness and market reach.

- Petrochemical Demand from End-User Industries: The burgeoning growth of sectors such as automotive, construction, packaging, and textiles creates substantial demand for petrochemical derivatives.

Barriers & Challenges:

- Price Volatility of Crude Oil: Fluctuations in global crude oil prices directly impact refining margins and feedstock costs, creating financial uncertainty.

- Competition from Renewable Energy & EVs: The long-term transition to cleaner energy sources and the rise of electric vehicles pose a disruptive threat to traditional fuel demand.

- Regulatory Hurdles & Policy Uncertainty: Evolving environmental regulations, complex approval processes, and potential policy shifts can create operational challenges and investment risks.

- Infrastructure Bottlenecks: Despite improvements, logistical challenges related to pipelines, port capacity, and storage can hinder efficient product distribution.

- Global Competition & Overcapacity: The international market for refined products and petrochemicals is highly competitive, with potential overcapacity in certain regions impacting pricing.

- Skilled Workforce Requirements: The sophisticated nature of modern refineries and petrochemical plants demands a highly skilled workforce, posing a challenge in talent acquisition and retention.

Emerging Opportunities in India Oil and Gas Downstream Industry

Emerging opportunities lie in the expansion of specialty petrochemicals, catering to high-growth sectors like advanced materials, pharmaceuticals, and electronics. The increasing focus on a circular economy presents avenues for investment in plastic recycling technologies and the development of biodegradable polymers. Furthermore, the drive towards decarbonization offers opportunities in developing and deploying carbon capture, utilization, and storage (CCUS) technologies within refineries and petrochemical complexes. Enhanced integration of renewable energy sources within downstream operations for power generation also represents a significant opportunity to reduce operational carbon footprints. The development of hydrogen as a clean fuel source also presents a future growth area for downstream players.

Growth Accelerators in the India Oil and Gas Downstream Industry Industry

The long-term growth of the India oil and gas downstream industry will be significantly accelerated by the strategic expansion of refining capacities to meet projected demand, coupled with aggressive investments in petrochemical integration to capture higher value. The government's continued push for indigenous manufacturing and its support through initiatives like Production Linked Incentives (PLI) for chemical and petrochemical sectors will be crucial. Furthermore, the adoption of advanced digital technologies for operational efficiency, predictive maintenance, and supply chain optimization will unlock significant cost savings and productivity gains. Partnerships and joint ventures, both domestic and international, will facilitate technology transfer and access to global best practices, fostering innovation and market expansion. The focus on developing and producing niche, high-value specialty chemicals will also be a key accelerator, diversifying revenue streams and enhancing profitability.

Key Players Shaping the India Oil and Gas Downstream Industry Market

- Indian Oil Corporation Limited

- Bharat Petroleum Corporation Limited

- Hindustan Petroleum Corporation Limited

- Reliance Industries Limited

- GAIL (India) Limited

- Nayara Energy Limited

- Haldia Petrochemicals Ltd

- Oman Oil Company

Notable Milestones in India Oil and Gas Downstream Industry Sector

- 2019: Indian Oil Corporation Limited commissions its first petrochemical plant at Paradip, Odisha, enhancing its petrochemical integration.

- 2020: Bharat Petroleum Corporation Limited announces expansion plans for its Bina refinery, focusing on increasing capacity and product diversification.

- 2021: Reliance Industries Limited continues to expand its Jamnagar refinery's petrochemical capabilities, focusing on advanced polymers and specialty chemicals.

- 2022: GAIL (India) Limited commissions new petrochemical units, increasing its product portfolio and market reach.

- 2023: Nayara Energy Limited announces significant investments in upgrading its Vadinar refinery to produce cleaner fuels and petrochemical feedstocks.

- 2024: The Indian government actively promotes Ethanol Blending Programme, leading to increased demand for fuel-grade ethanol and its integration with gasoline.

- Ongoing: Continuous modernization and debottlenecking projects across major refineries to enhance efficiency and meet BS-VI fuel standards are a constant feature.

In-Depth India Oil and Gas Downstream Industry Market Outlook

The future market outlook for India's oil and gas downstream industry is exceptionally bright, underpinned by an unwavering demand for energy and petrochemical products. Key growth accelerators include the strategic expansion of refining and petrochemical capacities, driven by anticipated economic expansion and a growing population. The government's sustained policy support, including incentives and a focus on energy security, will continue to be a significant enabler. Digital transformation and the adoption of Industry 4.0 technologies are poised to revolutionize operational efficiencies and reduce costs. Furthermore, a growing emphasis on sustainability and the development of greener technologies, including advanced recycling and the potential for hydrogen production, will shape the industry's long-term trajectory. Strategic partnerships and the pursuit of high-value specialty chemicals will be crucial for companies aiming to maximize profitability and competitive advantage in this dynamic market. The industry is on a robust growth trajectory, driven by domestic demand and a proactive policy environment.

India Oil and Gas Downstream Industry Segmentation

-

1. Refineries

- 1.1. Market Overview

- 1.2. Key Project Information

-

2. Petrochemical Pants

- 2.1. Market Overview

- 2.2. Key Project Information

India Oil and Gas Downstream Industry Segmentation By Geography

- 1. India

India Oil and Gas Downstream Industry Regional Market Share

Geographic Coverage of India Oil and Gas Downstream Industry

India Oil and Gas Downstream Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Refineries

- 5.1.1. Market Overview

- 5.1.2. Key Project Information

- 5.2. Market Analysis, Insights and Forecast - by Petrochemical Pants

- 5.2.1. Market Overview

- 5.2.2. Key Project Information

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. India

- 5.1. Market Analysis, Insights and Forecast - by Refineries

- 6. India Oil and Gas Downstream Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Refineries

- 6.1.1. Market Overview

- 6.1.2. Key Project Information

- 6.2. Market Analysis, Insights and Forecast - by Petrochemical Pants

- 6.2.1. Market Overview

- 6.2.2. Key Project Information

- 6.1. Market Analysis, Insights and Forecast - by Refineries

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Oil and Natural Gas Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Bharat Petroleum Corporation Limited

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Haldia Petrochemicals Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Hindustan Petroleum Corporation Limited

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Reliance Industries Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 GAIL (India) Limited

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Nayara Energy Limited

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Indian Oil Corporation Limited

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Oman Oil Company

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Oil and Natural Gas Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India Oil and Gas Downstream Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: India Oil and Gas Downstream Industry Share (%) by Company 2025

List of Tables

- Table 1: India Oil and Gas Downstream Industry Revenue million Forecast, by Refineries 2020 & 2033

- Table 2: India Oil and Gas Downstream Industry Revenue million Forecast, by Petrochemical Pants 2020 & 2033

- Table 3: India Oil and Gas Downstream Industry Revenue million Forecast, by Region 2020 & 2033

- Table 4: India Oil and Gas Downstream Industry Revenue million Forecast, by Refineries 2020 & 2033

- Table 5: India Oil and Gas Downstream Industry Revenue million Forecast, by Petrochemical Pants 2020 & 2033

- Table 6: India Oil and Gas Downstream Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Oil and Gas Downstream Industry?

The projected CAGR is approximately 3.5%.

2. Which companies are prominent players in the India Oil and Gas Downstream Industry?

Key companies in the market include Oil and Natural Gas Corporation, Bharat Petroleum Corporation Limited, Haldia Petrochemicals Ltd, Hindustan Petroleum Corporation Limited, Reliance Industries Limited, GAIL (India) Limited, Nayara Energy Limited, Indian Oil Corporation Limited, Oman Oil Company.

3. What are the main segments of the India Oil and Gas Downstream Industry?

The market segments include Refineries, Petrochemical Pants.

4. Can you provide details about the market size?

The market size is estimated to be USD 166.93 million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Investments in Renewable Energy Generation 4.; Supportive Government Policies Towards Green Energy.

6. What are the notable trends driving market growth?

Refineries to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Challenges In Installing Renewable Power in the Circulated Structure.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Oil and Gas Downstream Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Oil and Gas Downstream Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Oil and Gas Downstream Industry?

To stay informed about further developments, trends, and reports in the India Oil and Gas Downstream Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence